Russia's Central Bank Cuts Its Key Interest Rate Only Slightly

Author: Klaus Dormann

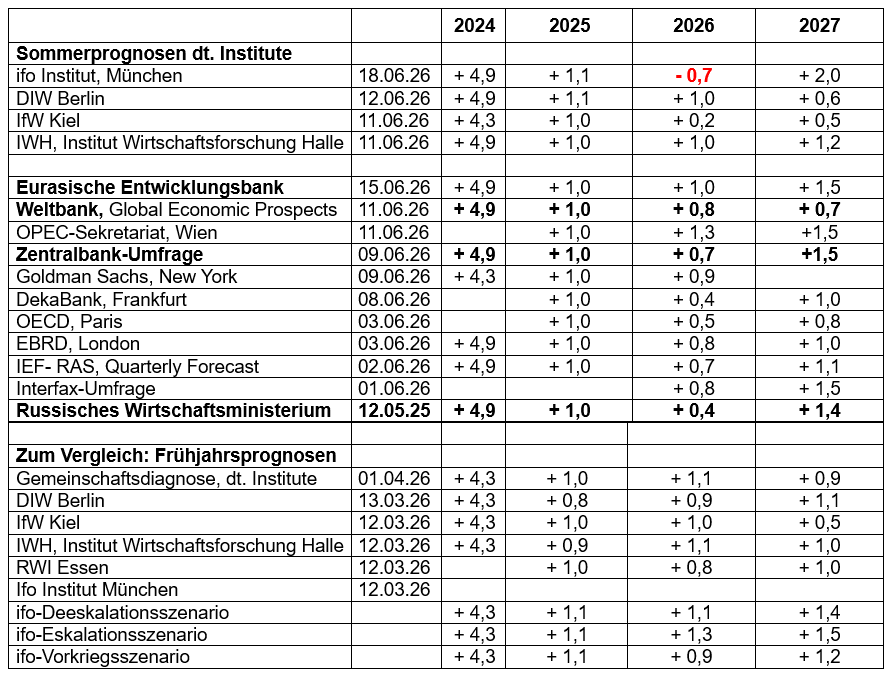

Four of the five leading German economic research institutes have also published new forecasts for the Russian economy as part of their “summer forecasts” since June 11 (DIW Berlin, IfW Kiel, IWH Halle, ifo Institute Munich). Six months before the end of the year, these forecasts reveal surprisingly large differences. The Munich-based ifo Institute now even expects a “recession” in Russia this year: It has drastically lowered its forecast for the development of aggregate economic output and now anticipates that real gross domestic product will contract by 0.7 percent in 2026.

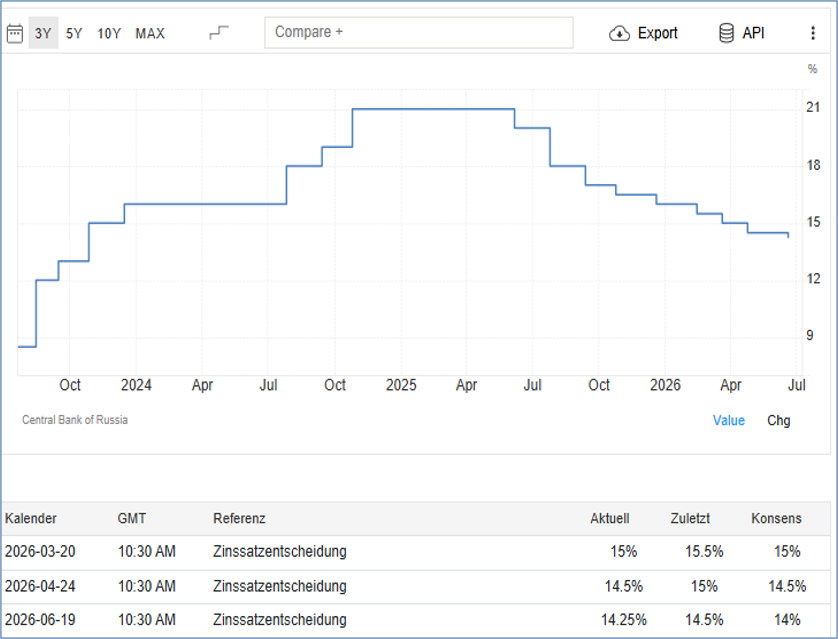

The central bank cut its key interest rate by only 25 basis points to 14.25 percent

If the Russian Central Bank had expected a decline in GDP as sharp as that projected by the ifo Institute, it would likely have cut its key interest rate more sharply on Friday. However, the central bank anticipates continued growth in Russia. In its “medium-term forecast,” it projects that the Russian economy will grow this year at a rate between 0.5 and 1.5 percent.

This is likely one reason why it lowered its key interest rate on Friday by only 0.25 percentage points, from 14.5 to 14.25 percent. In surveys conducted prior to the interest rate decision, however, the vast majority of analysts had expected another cut of 0.5 percentage points to 14% (see preliminary report on the interest rate decision for the German-Russian Chamber of Foreign Trade).

Russian Central Bank’s Key Interest Rate in Percent per Year

Trading Economics: Russia Key Interest Rate, June 19, 26

The business association had called for a cut of one percentage point

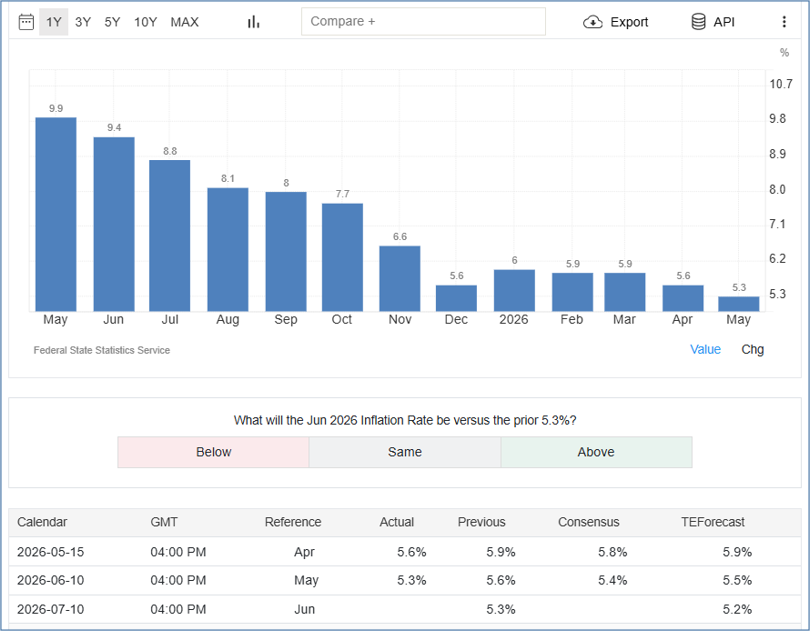

Alexander Schochin, chairman of the Russian Union of Industrialists and Entrepreneurs (RSPP), called for a cut in the key interest rate by a full percentage point to 13.5% ahead of the decision. Schochin justified his call by citing falling inflation and the increasing burden on businesses due to high financing costs. He pointed to the slowdown in the annual inflation rate to 5.3% in May. Against this backdrop, he said, a one-percentage-point interest rate cut would be a “logical step” (RSPP press release; russland.capital.de).

Year-over-year increase in consumer prices, in percent

Trading Economics: Russia Inflation Rate, June 19, 2026

Schochin expressed his disappointment with the modest cut in the key interest rate (RSPP press release):

“This is indeed disappointing. Just yesterday and in the days before, including at the International Economic Forum in St. Petersburg, I called for a more aggressive interest rate cut, with the goal of reaching a single-digit key interest rate—that is, below 10%—by the end of the year.”

Analysts’ comments on the modest key interest rate cut

Natalia Orlova, chief economist at Alfa Bank, commented diplomatically on the key interest rate decision:

“The good news is that interest rate cuts are continuing. The bad news is that the magnitude of the cut has decreased—which reflects the growing pro-inflationary risks in the economy.”

Economist Kirill Rodionov views the modest cut in the key interest rate as a solution to a dilemma facing the central bank. On the one hand, he noted, the central bank cannot lower key interest rates quickly due to the increased inflation risks resulting from fiscal policy easing. On the other hand, however, it could not ignore the calls for key interest rate cuts that were voiced during a meeting with President Putin. “The risks of a further increase in the budget deficit will, in any case, make the central bank’s task even more difficult,” Rodionov emphasized. (The Moscow Times.ru).

Sofia Donets, chief economist at T-Investments, said the modest rate cut was a sign that the central bank’s “conservatism” had hardened. If this slow pace of key interest rate cuts continues through the end of the year, the key interest rate will remain above 13% in 2026.

Investment banker Yevgeny Kogan agreed with this assessment. He pointed to the central bank’s warning that a growing budget deficit would require a more restrictive monetary policy. “I think this means we’ll still be living with double-digit interest rates next year. The central bank’s key rate forecast of 8 to 10% for 2027 might as well be forgotten,” said Kogan (The Moscow Times; Finam.ru).

Central Bank Warnings About Persistently High Budget Deficits

In explaining the modest rate cut, the central bank cited developments in fiscal policy as the primary reason. Central Bank Governor Nabiullina stated in her remarks on the key interest rate decision that “inflationary risks” had increased significantly. Her reasoning:

“Over the next three years, fiscal policy will be more expansionary than assumed in the Bank of Russia’s baseline scenario.

Credit growth has accelerated noticeably in recent months.

This may limit the scope for a further key interest rate cut, which is why we have taken a more cautious approach today.”

The annual increase in consumer prices rose to 5.6% in mid-June

Regarding the increased inflation risks, the Central Bank also cited the rise in fuel prices. The “pro-inflationary risks” have increased due to a decline in fuel production resulting from Ukraine’s attacks on Russian refineries, the bank explained. Reuters reports that Russia’s gasoline production in June was about 25% lower than a year ago. The average price of gasoline in Russia has risen by 6.6% since the beginning of the year.

President Elvira Nabiullina said at the press conference (video, starting at min. 14) that the rise in gasoline prices had been “one of the main reasons” for the moderate cut in the key interest rate of just 25 basis points. “The recent rise in fuel prices will affect inflation in June. The government is taking the necessary measures, but it may take some time for the supply situation to return to normal,” she added. Nabiullina emphasized: “The rise in gasoline prices could also affect inflation expectations, as gasoline is a relatively sensitive commodity for both individuals and businesses” (The Moscow Times).

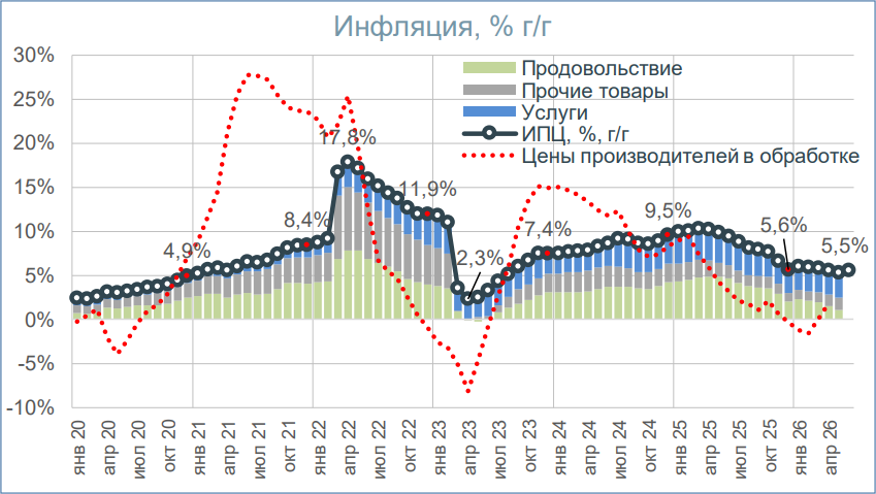

In its press release, the Central Bank noted that the annual increase in consumer prices reached 5.6% as of June 15. In the following chart from the VEB Institute, the line formed by black circles shows the trend in consumer prices through June 8, when the inflation rate stood at 5.5 percent after falling to 5.3 percent in May (see also Trading Economics).

Consumer price trends (black line)

and industrial producer price trends (red line);

year-over-year changes in percent

Research Institute of the State Development Corporation VEB.RF:

Global Economy and Markets, June 11, 26

However, the Central Bank reaffirmed its forecast that inflation will ease to between 4.5% and 5.5% by the end of 2026 and reach the target of 4% by the end of 2027.

Nabiullina: GDP is expected to have grown by 0.3 percent in the first half of the year

Commenting on current economic developments, the Central Bank President noted that economic indicators had improved in the second quarter, as expected. Factors that had temporarily slowed growth at the beginning of the year—including calendar and weather effects—are no longer having an impact or are now even accelerating growth. In particular, the construction sector has seen a “slight recovery” in production.

Looking at overall economic performance in the first half of 2026, Nabiullina said, “moderate growth” in the production of goods and services can be observed. In response to a question at the press conference regarding the current growth of the Russian economy, the president stated that the Central Bank estimates annual economic growth for the period from January to April at 0.3%. Economic activity also increased in May. The Central Bank also expects economic growth of around 0.3 percent for the first half of the year as a whole (video, starting at min. 34).

At the same time, however, the President noted that disparities in the performance of different economic sectors have widened. On the one hand, growth in government demand is increasing significantly. On the other hand, however, the potential for growth in private investment and consumer demand is declining due to limited resources.

According to the Central Bank’s press release, however, growth in consumer demand has accelerated in recent months. Investment activity has since recovered slightly following its slowdown in early 2026. It remains subdued, however.

According to Nabiullina, the situation on the labor market is slowly easing. She emphasized that a sustainable reduction in cost and price pressures stemming from the labor market requires a further narrowing of the gap between wage growth and labor productivity through the optimal utilization of the workforce.

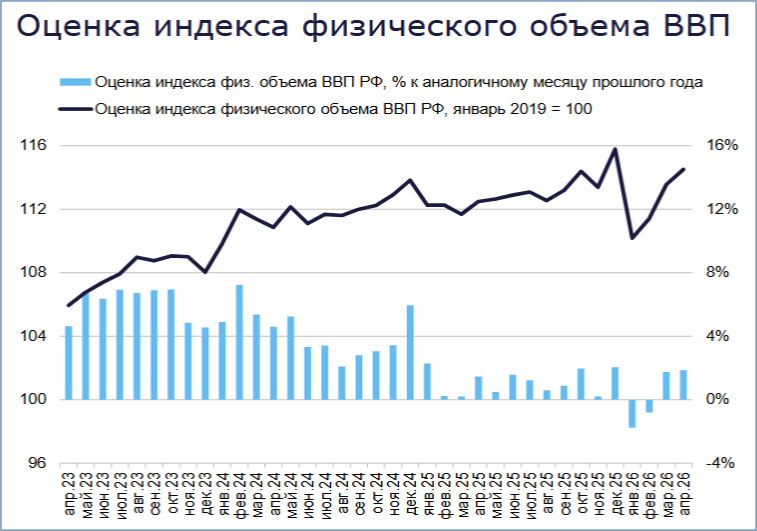

How Real GDP Developed in the First Four Months

On June 9, the Institute for Economic Forecasting of the Russian Academy of Sciences published an informative chart on the development of real gross domestic product in the first four months of 2026 in its monthly “Analysis of Short-Term GDP Dynamics.” The black line shows that the real gross domestic product index, which had reached a new high at the end of 2025, plummeted in January. However, it recovered significantly in the following three months. According to the Institute’s estimate, the GDP index in April was roughly back to the level seen in October.

Estimate of the real gross domestic product

index: black line—estimate of the real GDP index for the Russian Federation, January 2019 = 100

; blue bars—estimate of the year-over-year change in the real GDP index in %

IEF RAS: Analysis of Short-Term GDP Dynamics: June 2026, June 9, 2026

The right-hand blue bar shows that, according to the Institute’s estimate, the GDP index in April 2026 was 1.9 percent higher than in the same month of the previous year (right-hand scale).

GDP forecasts by German institutes now range from +1.0 to –0.7 percent

In their “Spring Forecasts” published three months ago in mid-March, German economic research institutes were still largely in agreement regarding this year’s growth of the Russian economy. They expected Russia’s aggregate economic output to rise by between 0.9 percent (DIW Berlin) and 1.3 percent (“escalation scenario” by the ifo Institute) in 2026. In their “Joint Assessment” published on April 1, the institutes agreed that, following 1.0 percent growth last year, the Russian economy was likely to grow by 1.1 percent this year.

Three months later, however, there is no longer any sign of broad consensus. The Berlin-based “German Institute for Economic Research” and the “Leibniz Institute for Economic Research Halle” revised their forecasts for this year’s growth in the Russian economy only minimally, by 0.1 percentage points each. The DIW and IWH now both expect the Russian economy to grow by 1.0 percent in 2026 as well. Incidentally, this forecast is also shared by the “Eurasian Development Bank,” which has now published its semi-annual update of economic forecasts for its member countries, including Russia.

Following the IfW Kiel, the ifo lowered its forecast for Russia even more sharply

However, the Kiel Institute for the World Economy and, above all, the Munich-based ifo Institute have sharply lowered their forecasts for Russia’s economic growth this year in their “Summer Forecasts.” The IfW revised its forecast down from 1.0 percent to just 0.2 percent (as reported by Ostwirtschaft.de).

The ifo Institute now even sees Russia’s economy entering a recession this year. It expects real gross domestic product to decline by 0.7 percent year-over-year (ifo Schnelldienst; Table 1.1, page 7). In its “Spring Forecast,” however, the Munich-based institute had still projected growth ranging from 0.9 percent (“pre-war scenario”) to 1.3 percent (“escalation scenario”) across three scenarios. Unfortunately, no explanation is provided for this significant “downward revision.”

However, the ifo Institute expects 2 percent growth in Russia in 2027

Following this year’s “plunge” into recession, however, the ifo Institute anticipates a rapid recovery of the Russian economy next year. It assumes that Russia’s real gross domestic product will rise by 2.0 percent in 2027. The other German institutes, on the other hand, expect GDP growth next year of only between 0.5% (IfW Kiel) and 1.2% (IWH Halle).

Looking at the years 2026 and 2027 together, the ifo Institute expects more growth in Russia than the IfW in Kiel, which—following very weak growth this year (+0.2%)—does not anticipate any significant acceleration next year either (+0.5%).

The RWI in Essen has not yet published any new forecasts for the Russian economy in its economic reports this summer (RWI spring forecast for Russia’s growth in 2026: +0.8%).

GDP Forecasts for Russia 2024–2027

: Year-over-year change in real gross domestic product, in percent

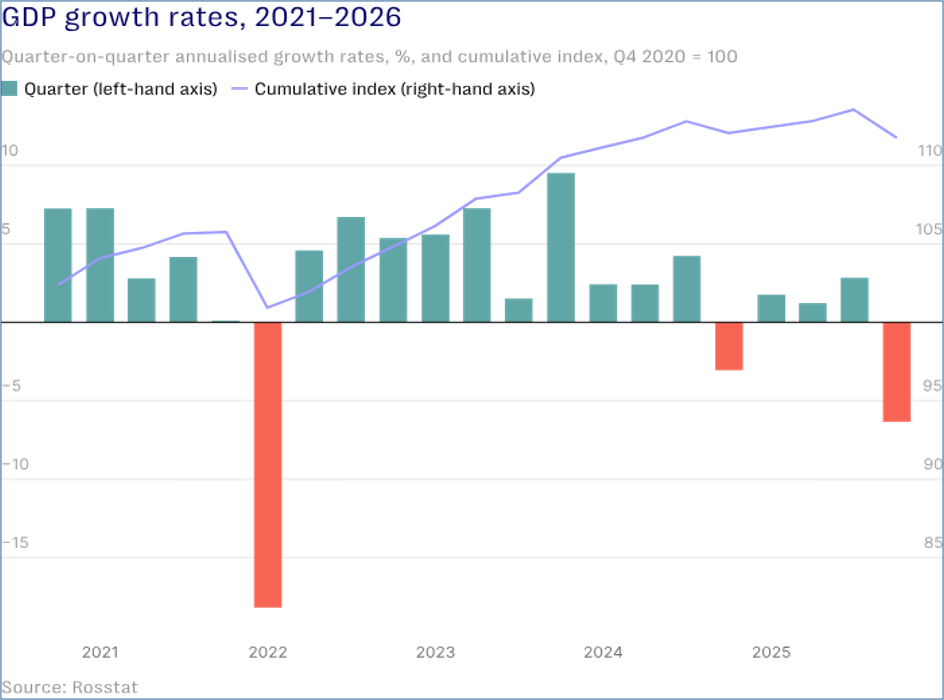

Sergey Aleksachenko: GDP growth of 1.0% is unlikely in 2026

However, in an analysis for the London-based “New Eurasian Strategies Centre,” Sergey Aleksachenko, former Deputy President of the Russian Central Bank, considers it unlikely that Russia will again achieve 1 percent economic growth in 2026 (as expected by the DIW and IWH).

According to Aleksachenko, if one extrapolates the GDP decline in the first quarter of 2026 compared to the fourth quarter of 2025 to an annual rate, this results in an “annualized” decline in Russian economic output of 6.4 percent in the first quarter of 2026 compared to the previous quarter (right red bar, left scale).

Real Gross Domestic Product Growth Rates 2021–2026

Left scale: annualized rates of change compared to the previous quarter in %;

right scale: real gross domestic product index, 4th quarter 2020=100

New Eurasian Strategies Centre; Sergey Aleksashenko, Senior Research Fellow: “The Illusion of Normalization: Tensions in the Kremlin Have Eased, but Anxiety Remains,” June 16, 2026

According to Aleksashenko’s calculations, in order to achieve 1 percent GDP growth year-over-year from 2025 to 2026, “annualized” growth rates of around 4 percent would need to be achieved in each of the remaining three quarters of 2026. This is unlikely, because such high growth rates were only consistently recorded during the period of rapid increases in military spending from mid-2022 to early 2024, as the figure above shows.

Recommended reading:

Monetary Policy: Key interest rate cut from 14.5 to 14.25 percent on June 19

- Onvista; Reuters: Russian Central Bank cuts key interest rate less sharply than expected, June 19, 2026; MarketScreener, Reuters: Russian Central Bank cuts key interest rate by 25 basis points to 14.25% – risks from fuel supply and fiscal policy, June 19, 2026

- RSPP: Alexander Shokhin: Companies are disappointed by the Central Bank’s interest rate decision, June 19, 2026; Comment by RSPP Vice President Alexander Murychev on the Central Bank’s key rate decision, June 19, 2026

- The Moscow Times.com: Russian Central Bank Slashes Key Rate to 14.25; June 19, 2026

- Moscow Times.ru: Nabiullina warned of accelerating inflation due to the fuel crisis and an explosive rise in budget spending; June 19, 2026

- Interfax.ru: Nabiullina pointed out the already present risk of a revision to fiscal policy; June 19, 2026

- Olga Belenkaya; Head of the Macroeconomic Analysis Department, FG Finam: Bank of Russia: The pace of key rate cuts has slowed, and the scope for further cuts has narrowed; June 19, 2026

- Dmitry Nikitin, Columnist for Finam.ru: The Central Bank as Goalkeeper. What Will Happen to the Market and the Ruble Under a More Restrictive Monetary Policy? Analysts on the Key Rate Cut; June 19, 2026

- Interfax.ru: The Russian Central Bank expects GDP growth of 0.5% in the first half of the year; June 19, 2026; Interfax.ru: The Russian Central Bank confirmed its inflation forecast for 2026 in the range of 4.5 to 5.5 percent; June 19, 2026

- Bank of Russia, Press Release: Bank of Russia cuts the key rate by 25 basis points to 14.25% p.a.; June 19, 2026

- Bank of Russia: Statement by Bank of Russia Governor Elvira Nabiullina following the Board of Directors meeting on June 19, 2026; June 19, 2026; Video of the press conference; June 19, 2026

Preliminary reports on the key interest rate decision on June 19

- russland.capital: Russian industrial lobby calls for a more significant key interest rate cut, June 19, 2026

- German-Russian Chamber of Foreign Trade: Will Nabiullina cut the key interest rate tomorrow despite the record deficit? June 18, 2026

- RSPP: Alexander Shokhin: The Russian Union of Industrialists and Entrepreneurs (RSPP) calls on the Central Bank to further lower interest rates in light of waning demand, June 18, 2026

- bne IntelliNews, Ben Aris: Putin makes a rare call for a rate cut, arguing that thanks to falling inflation, the regulator should cut rates faster to boost economic growth, June 11, 2026

- 1Prime.ru: The Central Bank reported growth in Russian GDP for the first quarter of the year. Deputy Central Bank Governor Zabotkin: Russia’s GDP grew moderately in the first quarter, June 11, 2026

- bne IntelliNews, Ben Aris: Where is Nabiullina? June 9, 2026

- Russland.capital: Russia’s economy hopes for lower interest rates—Central Bank remains cautious, June 7, 2026

Current Economic Developments; Economic Data for April, May, and June

- Finanzmarktwelt; Josephine Bollinger-Kanne: Putin’s Fight Against Economic Apocalypse in Russia, June 20, 26

- Tagesschau.de; Angela Göpfert, ARD Finance Desk: Putin’s War Economy Is Under Increasing Pressure. The war in Iran has only given Russia a brief respite. Falling oil prices, Ukrainian drone attacks, and the strong ruble are increasingly weighing on the economy; June 19, 26

- Marina Voitenco; Politcom.ru: Investment Activity—Restrictions, Risks, Prospects; June 18, 26; Macro-Dynamic Arrhythmia and the Government’s Response, June 12, 26

- Finmarket.ru: Rosstat confirmed its estimate of a 0.2% decline in Russian GDP in the first quarter, June 17, 2026

- Sergey Aleksashenko, Senior Research Fellow at the New Eurasian Strategies Centre: The Illusion of Normalization: Tensions in the Kremlin Have Eased, but Anxiety Remains, June 16, 2026

- VEB Institute: GDP Index: Monthly GDP Estimate – April 2026; June 16, 2026

- EuroNews; Sasha Vakulina: “Significantly worsened”: These 3 factors are hurting Russia’s economy, says IMF Managing Director Kristalina Georgieva; June 12, 2026

- Münster aktuell; Tim Eichler: Russia’s Economy Under Pressure from Interest Rate Hikes and Sanctions, June 11, 2026

- VEB Institute: Global Economy and Markets, June 11, 2026

- Silicon Curtain: Interview with Nigel Gould-Davies, Senior Fellow for Russia and Eurasia at the International Institute for Strategic Studies (IISS) in London: Is Russia’s economy REALLY collapsing, or is it more resilient? June 10, 2026

- Finmarket.ru: According to the Central Bank, economic activity in Russia increased in April and May; GDP growth in the second quarter will be positive, June 10, 2026

- IEF RAS: Analysis of Short-Term GDP Trends: June 2026, June 9, 2026

- Joe Blogs Video: Russia’s war-driven boom is coming to an end. The mood at SPIEF 2026 has completely changed. High-ranking bankers, business leaders, and government officials openly discussed slowing growth, declining investment, labor shortages, demographic decline, and the growing risk of economic stagnation; 15 min., June 8, 2026

- Kommersant, Artem Chugunov: The Russian economy is recovering after a weak start to the year, June 8, 2026

- Finanzmarktwelt; Josephine Bollinger-Kanne: The Four Horsemen of the Apocalypse for Economic Growth in Russia. In Russia, key interest rates, taxes, a strong ruble, and administrative hurdles are cited as major burdens; June 6, 26

Economic Forecasts: Summer Forecasts from German Institutes

- ifo Institute Munich: ifo Economic Forecast Summer 2026: Rising Energy Prices Slow Growth—Fiscal Policy Provides a Boost; in: ifo Express Service: Rising Energy Prices Slow Growth—Fiscal Policy Provides a Boost, June 18, 2026

- DIW Berlin: DIW Weekly Report: Energy price shock slows German economy – global economy on a moderate growth path, June 12, 2026; Energy price shock slows German economy – global economy on

- IWH Halle: Current Economic Outlook: The Economy Between the Energy Crisis and the AI Boom; PDF, June 11, 2026

- RWI Essen: RWI Economic Report: Despite the Energy Price Shock: Industry Proves Resilient – Inflation Spreads to More and More Sectors; Press Release dated June 16, 2026

- IfW Kiel: The Global Economy in Summer 2026, PDF, June 11, 2026; Politico Europe; Berlin Playbook Podcast; Rixa Fürsen: Interview with Moritz Schularick, President of the Kiel Institute for the World Economy: “Russia on the Brink of Collapse,” 36 min., June 13, 2026

Discussion contributions on the Kiel Report: “Is Russia’s Economy on the Brink of Collapse?”

- “Die Presse” podcast “Russia – Gas, Sanctions, Oligarchs”; Eduard Steiner in conversation with Vasily Astrov, wiiw: Is Russia’s economy truly in its final stages? German and Swedish economists claim that Russia’s economy is in its final stages. Are they right? Can it only be saved by an end to the war in Ukraine? And whom has the elite chosen as the scapegoat for the disaster? 38 min., June 17, 26

- Prof. Dr. Alexander Libman; in: Freie Universität Berlin; Campus.Leben; The Online Magazine of FU Berlin;: Is Russia on the Brink of Economic Collapse? Since the outbreak of full-scale war, predictions of a rapid collapse of the Russian economy have been mounting. But how realistic are they? June 17, 2026

- Austrian Academy of Sciences; Prof. Wolfgang Müller: Is Russia’s Economy on the Verge of Collapse? High inflation, skyrocketing military spending, shrinking growth: Under the pressure of war and sanctions, Russia’s economy is showing clear cracks. ÖAW historian and Eastern Europe expert Wolfgang Müller analyzes where the Kremlin is actually vulnerable—and what has kept it afloat so far; June 16, 2026

- Prof. Dr. Moritz Schularick, President of the Kiel Institute for the World Economy, in an interview with Rixa Fürsen; Politico Europe; Berlin Playbook Podcast: “Russia on the Brink of Collapse,” 36 min., June 13, 2026

Reports on the Kiel Report: “Endgame: Russia’s Economy Under Pressure”

- Kiel Institute for the World Economy: Kiel Report No. 9. Endgame: Russia’s Economy Under Pressure; Executive Summary; Torbjörn Becker and Moritz Schularick: Russia’s Economy in Its Final Stage, June 11, 2026

- Joe Blogs: Russian Endgame Disaster; A bombshell new report from one of Europe’s leading economic research institutes claims Russia’s wartime economy is entering a dangerous new phase. …The report reveals a dramatic surge in hidden corporate debt, growing stress within Russia’s banking system, rapidly shrinking financial reserves, falling oil and gas revenues, and increasing dependence on China, June 16, 2026

- Münchner Merkur; Fabian Hartmann: “Clear Signs of Structural Exhaustion”: Analysis Sees Russia’s Economy Close to Collapse, June 14, 2026

- Frankfurter Rundschau; Fabian Hartmann: Russia’s economy reaches “final stage”: Close ties to China are not the only cause, June 13, 2026

- web.de; dpa: Economists see Russia’s economy as having reached the “final stage,” June 11, 2026

- Deutsche Welle: War in Ukraine: Economists See Russia’s Economy at an End, June 11, 2026;

- Handelsblatt, dpa: Institute for the World Economy: Economists See Russia’s Economy at Its Limit. According to a report by economists, Russia’s economy is on the verge of collapse. The report also highlighted opportunities for the West, June 11, 2026

Further Forecasts

- Eurasian Development Bank: Macroeconomic Forecast 2026–2028, June 15, 2026

- World Bank: Press Release: Middle East Conflict Sends Global Growth to Lowest Rate Since COVID-19; June 11, 2026; Global Economic Prospects: Europe and Central Asia, June 2026, June 11, 2026

- Business Insider; Huileng Tan: Russia’s Economy Is Suffering—Goldman Sachs Delivers a Harsh Verdict. Higher Oil Prices Help Putin—Why Russia’s Economy Still Won’t Recover, According to Goldman Sachs, June 10, 2026

Fiscal Policy; National Budget and Oil Prices

- Olga Belenkaya, FG Finam: Budget: Signs of Stabilization Emerged in May, June 8, 2026

- Tass.ru: Ministry of Finance: The budget deficit for the first five months of 2026 amounted to 6.01 trillion rubles; June 25, 2026

- Kommersant interview with Finance Minister Siluanov; Matvey Ivaschenko: Budget, Taxes, and Oil Dependence. Key points from the interview with Anton Siluanov, May 27, 2026; “We must increase our financial safety margin.” Interview on the budget situation, tax administration, “cleaning up the economy,” and the prospects for IPOs of state-owned enterprises, May 27, 2026.

- New Eurasian Strategies Centre; Sergey Aleksaschenko: The Kremlin is bleeding money—but not running dry, May 14, 26

- bne IntelliNews: Russian budget deficit jumps to 55% of annual target in 4M26, May 12, 26

Foreign Trade

- Deutsche Welle; Arthur Sullivan: Could Russia save the global economy? Global energy markets are still grappling with the price and supply shock caused by the war in Iran. Could Russia solve the problem? Business Beyond takes a closer look at U.S. plans to bring Moscow back into the picture; Video, Interviews with Craig Kennedy, Elina Ribakova, Janis Kluge; 20 min., June 8, 2026

- russland.capital: Moscow is once again courting Western companies—on Russia’s terms, June 7, 2026

- Euronews; Angela Skujins: O’Sullivan: China Remains a Major Problem for EU Sanctions Against Russia, June 3, 2026

- MMI Russian Macro: OIL AND GAS REVENUES: Moderate growth despite such high prices; The reason appears to lie in physical export restrictions, June 3, 2026