Russia's economy continues to grow by 1 percent, the IMF confirms

Author: Klaus Dormann

Headlines about the Russian economy rarely inspire confidence. In its “Summer Forecast,” the Kiel Institute for the World Economy projects that the Russian economy will be almost completely stagnant (2026: +0.2%). The Munich-based ifo Institute even expects a recession in Russia this year (-0.7%). And the Russian government itself had already revised its growth forecast for 2026 downward from 1.3% to just 0.4% in mid-May.

Nevertheless, the International Monetary Fund has now stood by its forecast that the Russian economy is likely to continue growing by about one percent in both 2026 and 2027, just as it did in 2025. It apparently assumes, above all, that the rise in energy prices will generate new revenue for Russia and thus support the growth of the Russian economy. However, the majority of forecasts currently emphasize that the destruction of many refineries in Russia by Ukraine will lead to significant production shortfalls and slower growth.

IMF: GDP growth of 1.1 percent is projected for both 2026 and 2027

During the overheated “arms boom” of 2023 and 2024, Russia’s economic growth had accelerated to 4.1% and 4.9%, respectively, before cooling to just 1.0% in 2025. In the update to its “World Economic Outlook,” the IMF now expects Russia’s real gross domestic product growth to remain similarly moderate in 2026 and 2027. As previously projected in its “Spring Outlook” in April, the IMF expects aggregate economic output to grow by 1.1% in each of those years.

Rising global energy prices are supporting growth in Russia

To explain this stable growth, the IMF points out that Russia, as a commodity and energy exporter, is benefiting from higher global market prices. It states that increased export revenues—which are partly a result of higher commodity prices—are providing relief to the Russian economy and keeping growth at 1.1% (“Stronger export revenues, in part because of higher commodity prices, provide partial relief to the economy in Russia, maintaining a growth rate of 1.1 percent.”).

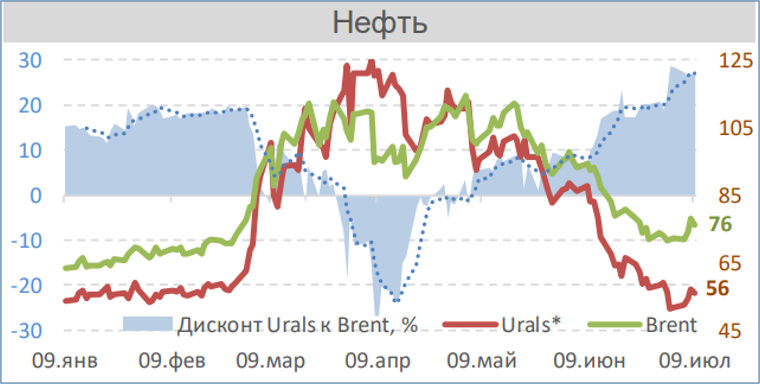

However, the price of Russian Urals crude (Trading Economics chart) has fallen so sharply since April that, at times in June, it was already lower than it had been before the start of the war in Iran at the end of February (red line in the figure below, right scale). On July 9, the Urals price, at $56 per barrel, was about 26% lower than the Brent price of $76 per barrel (this “price discount” is shown by the blue area on the left scale).

Prices of Urals and Brent crude oil in U.S. dollars per barrel (right scale)

Difference between the Brent price and the Urals price in percent (left scale)

VEB Institute: Global Economic and Market Outlook, July 10, 26

According to the chart above from the research institute of the state development corporation VEB, the Urals price on July 9 was just under a quarter lower than the Brent price.

IMF: The oil price will rise by nearly a third in 2026 but fall by about 12 percent in 2027

In its World Economic Outlook, the IMF forecasts oil price trends based on the average of the prices of the three grades: Brent, WTI, and Dubai (Table 1. Overview of the World Economic Outlook Projections, Page 12).

According to the IMF, the annual average oil price will rise by 31.8% to $89.27 per barrel in 2026. In April, the IMF had expected a less pronounced increase of 21.4% to $82.22 per barrel.

In 2027, however, the IMF expects prices to fall to $78.7 per barrel. According to the updated forecast, this decline will be 11.8% steeper than previously expected (–7.6%)

Interfax also reports on the oil price forecasts: The IMF report, which was prepared before the recent renewed escalation in the Iran conflict, assumes in these forecasts that the Strait of Hormuz will reopen in mid-July. The IMF expects the situation to return to pre-war levels by March 2027.

According to the IMF, a further reduction in inventories could prevent a severe shortage in global oil supplies. However, the IMF anticipates that shortages will occur in some emerging and transition economies that do not have sufficient stockpiles and are competing with wealthier countries for available supplies.

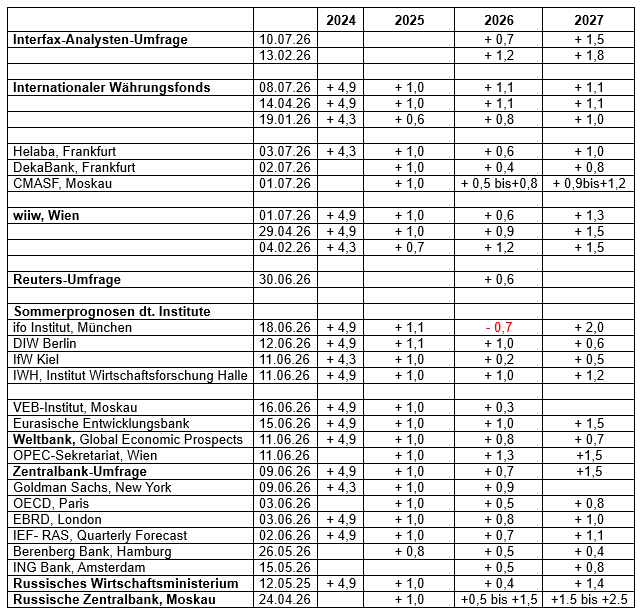

The IMF has raised its forecast for Russia since the beginning of the year, bucking the trend

Since January, the IMF has raised its forecast for Russia’s economic growth this year from 0.8% to 1.1%. At the same time, however, the “Vienna Institute for International Economic Comparisons” has halved its forecast for Russia from 1.2% to 0.6% (see the table below).

Average growth expectations in analyst surveys have fallen just as sharply as the wiiw forecast. In an Interfax survey published on July 10, average growth for 2026 was expected to be only 0.7%. By contrast, in February, the “consensus” on Russian economic growth in the Interfax survey had still stood at +1.2%. Participants in the most recent survey included: VTB Bank, the VEB development bank, Gazprombank, ING Bank, the Institute for Economic Policy, Promsvyazbank, Renaissance Capital, SberCIB, and Uralsib. The lowest growth forecast among the participants was +0.3%. Thus, none of them currently expects a recession.

A Reuters survey conducted in late June also projected an average economic growth rate of just 0.6% for Russia this year. In January, participants had expected an increase nearly twice as high (1.1%).

However, the IMF did not follow the downward revision of growth forecasts seen in the analyst surveys. The IMF’s growth forecast of around one percent is shared by, among others, the DIW Berlin, the IWH Halle, the Eurasian Development Bank, the OPEC Secretariat in Vienna, and Goldman Sachs. Overall, the growth forecasts for 2026 do not currently vary widely. Almost all range between 0.4 and 1.3%.

GDP Forecasts for Russia, 2024–2027

: Year-over-year change in real gross domestic product, in percent

The Russian Central Bank will update its forecasts ahead of its next key interest rate decision on July 24. So far, the IMF’s growth forecast of 1.1% for 2026 falls almost exactly in the middle of the Central Bank’s forecast range of 0.5 to 1.5%.

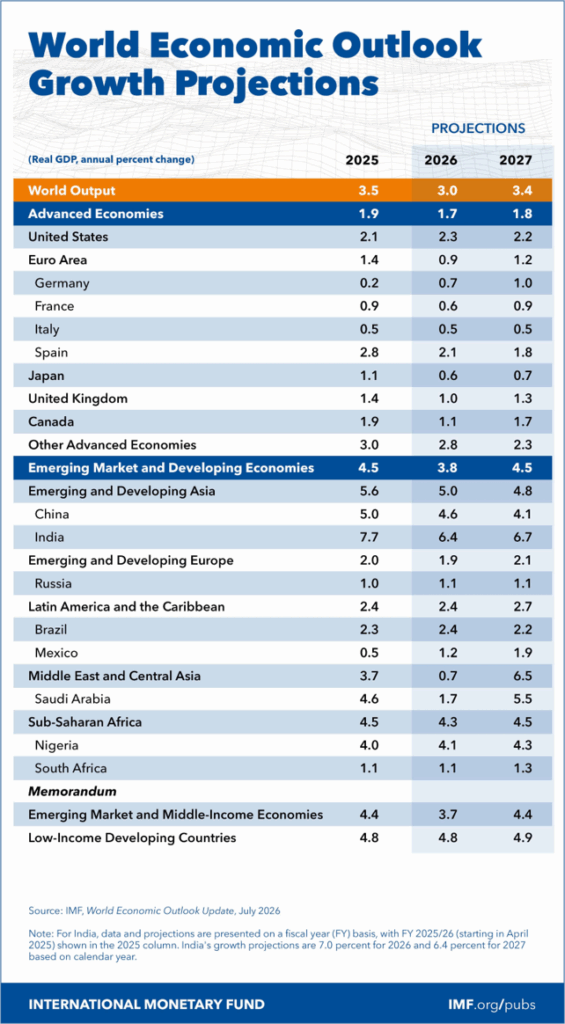

IMF: Russia Benefits as an Energy Exporter Outside the Middle East

The IMF titled the July edition of its “World Economic Outlook” “Global Economy in Crosscurrents of War and Technology.” It currently sees two main forces affecting the global economy. On the one hand, there is a “negative supply shock” due to the war in the Middle East. On the other hand, however, a “positive technology shock” is simultaneously at work.

According to the IMF, the negative effects of the war in the Middle East on global economic growth will be partially offset by accelerated demand growth in the technology sector driven by the development and application of artificial intelligence. Overall, the IMF estimates that these two opposing trends will lead to a slowdown in global economic growth from 3.5 percent in 2025 to 3.0 percent in 2026. At the same time, energy-exporting countries outside the conflict zone in the Middle East (such as Russia) could benefit from more favorable trade conditions (Finmarket.ru).

The IMF lowered its forecast for global growth in 2026 by only 0.1 percentage points to 3% compared to its April forecast. At the same time, it raised its forecast for global economic growth in 2027 by 0.2 percentage points to 3.4%.

IMF: World Economic Outlook Update, July 2026:

Global Economy in Crosscurrents of War and Technology, July 8, 2026

Russia’s growth in 2026 and 2027 will be slightly stronger than Germany’s

According to the IMF forecast above, the German economy will grow at a slightly slower pace—0.7% in 2026 and 1.0% in 2027—than the Russian economy, which is projected to grow at 1.1% in both years.

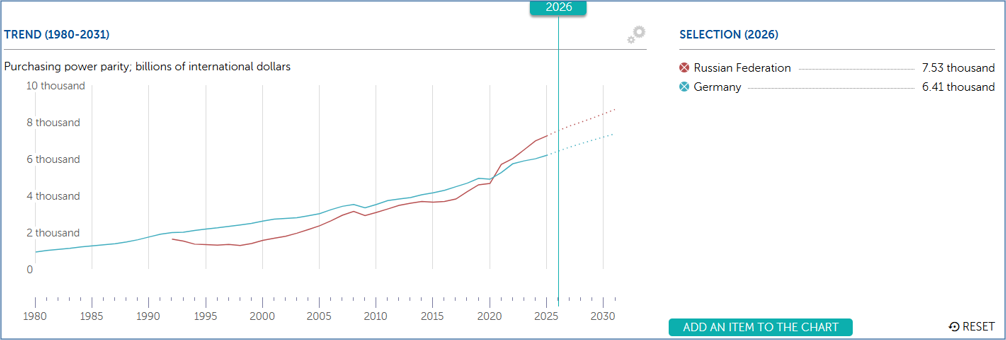

In the ranking of the world’s largest economies, Russia had already displaced Germany from fourth place by 2021, when gross domestic product is adjusted for the purchasing power of each country’s currency (known as “purchasing power parity” in “international dollars”). This is illustrated by the following IMF chart (see also the video by Vgraphs showing changes in this ranking). By 2026, Germany will rank only sixth in the international GDP rankings based on “purchasing power parity,” behind China, the U.S., India, Russia, and Japan (Cleartax provides further information on various “rankings”).

IMF Data Mapper: Russian Federation and Germany

GDP, current prices;

Purchasing power parity; billions of international dollars

IMF: Data Mapper, July 9, 2026

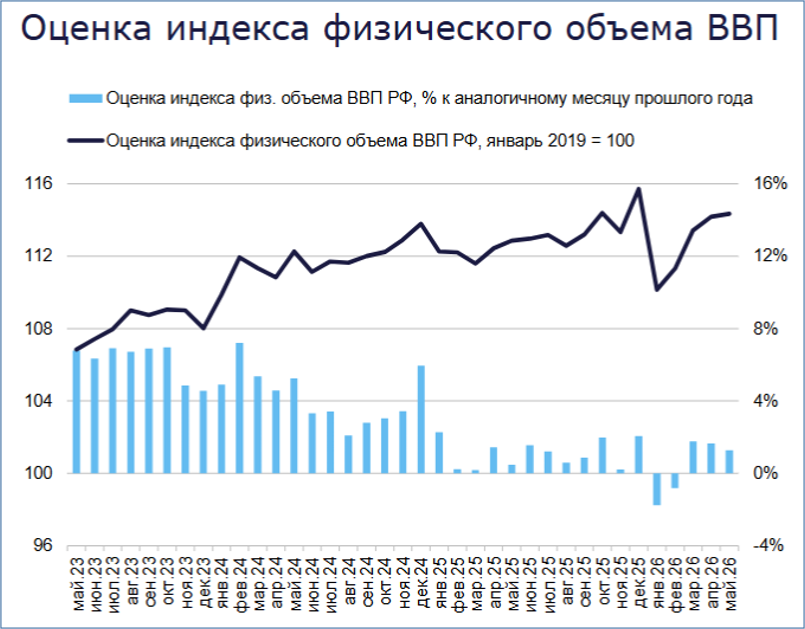

In the first five months, however, Russia’s GDP was barely higher than in the previous year

For Russia to still achieve year-over-year economic growth of around one percent this year, the annual increase in output must accelerate in the months from June through December. According to preliminary calculations by the Ministry of Economic Development, real gross domestic product in the first five months was only 0.2% higher than in the previous year (Interfax).

Last week, the “Institute for Economic Forecasting of the Russian Academy of Sciences (IEF-RAS)” published the following chart on GDP trends in the first five months in its “Analysis of Short-Term GDP Trends.”

The black line shows that the real gross domestic product index plummeted in January compared to the record high reached in December. The blue bars show that GDP declined in January and February 2026 compared to the same months of the previous year. Since then, the GDP index has largely recovered from the January slump. In May, it was roughly as high as it had been in October 2025. According to the IEF, the GDP index in May 2026 exceeded the level reached in May of the previous year by 1.3% (right blue bar).

However, compared to the previous month of April, the GDP index rose by only 0.1% on a seasonally adjusted basis in May 2026, according to the institute’s estimate. In March, it had risen by 1.9% month-over-month, and in April by 0.7%. The institute believes this could indicate the end of the recovery phase in economic activity following the sharp decline in early 2026.

Estimate of the real gross domestic product

index: blue bars—changes in real GDP compared to the same month of the previous year in %; black line—estimate of the real GDP index; January 2019 = 100

Institute for Economic Forecasting of the Russian Academy of Sciences (IEF-RAS):

Analysis of Short-Term GDP Dynamics: July 2026, July 7, 2026

IEF: These Are the Risks to Growth and Price Trends in the Second Half of the Year

However, the “Institute for Economic Forecasting” points to significant risks to the growth of the Russian economy in the second half of 2026. Given the geopolitical uncertainty and the Russian Central Bank’s gradual easing of monetary policy, there could be a sustained decline in investment.

In addition, production shortfalls at Russian oil refineries are likely to have a negative impact on overall economic performance through the following “four channels.”

First, the loss of refinery capacity will hamper the growth of overall industrial production, likely even more so in June than in previous months.

Second, this will accelerate inflation because fuel prices are rising and higher transportation costs are being passed on to consumers. According to Rosstat, fuel prices rose by about 7% in May alone. It is very likely that these price increases will also be reflected in consumer prices. This trend is being fueled by strong growth in consumer demand.

Third, fuel shortages could lead to disruptions in passenger travel as well as restrictions on freight transport.

Fourth, inflation accelerated by the fuel crisis and rising inflation expectations could slow the pace at which the central bank eases monetary policy.

Based on the latest economic developments, the “Institute for Economic Forecasting of the Russian Academy of Sciences (IEF-RAS)” in its “Analysis of Short-Term GDP Trends” that Russia’s overall economic output is likely to grow by 1.1 percent in 2026 (as expected by the IMF). However, this “short-term forecast” is based on the assumption that current trends in key indicators will continue.

In its “Quarterly GDP Forecast” published in early June, the institute lowered its growth forecast for 2026 to 0.7 percent. Next year, however, the IEF—like the IMF—expects Russia to see growth of 1.1 percent.

What consequences the “fuel crisis” will have, according to the Interfax survey

The results of the Interfax survey published on July 10 indicate that survey participants also expect the destruction of Russian refineries by Ukraine (Tagesschau.de) to have significant macroeconomic implications: Growth in industrial production will be even weaker than previously expected, inflation will be higher, and the key interest rate will fall more slowly.

Overall, industrial production had already declined unexpectedly sharply by 0.7% in May. Survey participants have now more than halved their forecast for industrial production growth for the full year 2026. While they were still expecting a 1.2% increase a month ago, they now anticipate growth of only 0.5%. This is also nearly in line with the Ministry of Economy’s forecast (+0.6%).

Driven by rising fuel prices, analysts estimate that the increase in consumer prices will still reach 5.7% in 2026. A month ago, they had expected a sharper decline to 5.3%. For 2027, analysts expect an inflation rate of 4.6% (a month ago: 4.5%).

According to the survey, the key interest rate will also decline more slowly by the end of 2026. The “consensus forecast” for the key interest rate is now 13.3%. A month ago, survey participants had, on average, still expected it to be lowered to 12.4% by the end of 2026. For the annual average in 2026, participants now expect a key interest rate of 14.5% (last month’s forecast: 14.1%).

Russia’s budget deficit in 2026 remains much higher than planned

The temporary sharp rise in oil prices following the start of the war in Iran and the blockade of the Strait of Hormuz has not yet led to an increase in oil and gas revenues in the Russian federal budget. According to the Ministry of Finance, “oil and gas revenues” actually fell by 22.7% year-over-year to 3.66 trillion rubles in the first half of 2026.

At least the decline in these revenues in June was less severe than before. After five months, oil and gas revenues had still been nearly 30 percent below the previous year’s level. This improvement suggests that higher oil prices have recently been reflected, at least in part, in the budget, according to an analysis of budget trends by russland.capital.

Overall, federal budget revenues rose to 18.6 trillion rubles in the first half of the year. However, the 5.8 percent increase was not enough to offset the sharp rise in spending. Federal budget expenditures grew nearly three times as fast in the first half of the year, rising by 16.1 percent to 24.35 trillion rubles.

As a result, the federal budget deficit for the first half of 2026 amounted to 5.73 trillion rubles, equivalent to 2.5 percent of gross domestic product. This shortfall is already significantly higher than the deficit of 3.8 trillion rubles—or 1.6 percent of GDP—projected for the entire year.

Dr. Janis Kluge, an expert at the German Institute for International and Security Affairs (SWP), pointed out in a ZDF interview at the end of June that oil and gas revenues in the Russian federal budget in 2026 were lower as a percentage of gross domestic product than in any other year since 2000.

Bruegel: The temporary rise in oil prices brought Russia additional revenue

In an article published by the Brussels-based Bruegel Institute, Professor Marek Dabrowski compared the Russian federal budget revenues from March through June with those of the first two months of 2026—that is, the period before the start of the war with Iran in late February. According to Dabrowski’s calculations, a comparison of Russia’s revenues from the hydrocarbon sector between March and June with the average figures for January and February shows that the additional revenues related to the Iran conflict amount to approximately 0.5% of Russia’s nominal GDP.

At the same time, however, Dabrowski also points out that budget revenues from hydrocarbons in the first half of 2026, at 3.66 trillion rubles, were about 23 percent lower than those of the same period the previous year (4.73 trillion rubles), even though the average Urals price was higher.

Dabrowski does not consider Russia’s additional revenue of 0.5% of GDP and other macroeconomic benefits related to the war in Iran to be “groundbreaking.” However, they would provide relief to the Russian budget, which is under increasing pressure due to war-related expenditures. At least temporarily, this has expanded Russia’s financial leeway to continue its war of aggression against Ukraine.

Recommended reading:

German-Russian Chamber of Foreign Trade:

Analyses, in German; also in Russian; (selection):

- Experts: Is Russia’s Economy on the Verge of Collapse? July 9, 26

- Gasoline Crisis in Russia, June 30, 26

- Small Interest Rate Hike Dampens Business Hopes, June 23, 2026

- Prof. Dr. Alexander Liebmann in conversation with Thomas Baier on the German-Russian Chamber of Foreign Trade’s podcast “Tsars, Data, Facts”: Russia’s Economy: Between Stagnation and Recession, 27 min., In this episode, Prof. Alexander Liebmann of the Free University (FU) of Berlin explains that, as he predicted, the Russian economy has been moving toward stagflation: Growth is near zero while inflation remains high. He does not view the central bank as the main cause of the economic slowdown, as structural factors such as labor shortages, full employment, and high military spending are limiting growth; June 16, 2026

Podcasts, Videos:

- DW News, The Dip Podcast: Russia’s Oil Empire Under Pressure: Can Putin Still Afford the War in Ukraine? Janis Kluge and Sergey Aleksashenko explain how the war in Ukraine is affecting ordinary Russians, why fuel shortages and rising gasoline prices are becoming a major political problem for Vladimir Putin, and whether Russia’s oil-dependent economy can withstand mounting pressure from the war and sanctions; 28 min., July 5, 2026

- Janis Kluge, German Institute for International and Security Affairs (SWP), in an interview with ZDF heute live: Putin acknowledges fuel shortages, but economic expert Kluge sees no evidence of falsified Russian economic data. He says on ZDF heute live that an economic collapse is not currently to be expected; 12 min.; June 29, 2026

Economic Forecasts:

- Finmarket.ru; Interfax survey: Analysts forecast a 0.1 percent decline in industrial production in Russia for June, with inflation at 0.85 percent, July 10, 2026

- IMF: World Economic Outlook Update, July 2026: Global Economy in Crosscurrents of War and Technology, July 8, 2026; Press Briefing Transcript: World Economic Outlook (WEO) Update, July 8, 2026

- Finmarket.ru: The IMF Praised the Global Economy and Symbolically Revised Its Forecast for 2026–2027, July 8, 2026

- Institute for Economic Forecasting of the Russian Academy of Sciences; IEF-RAS: Analysis of Short-Term GDP Trends: July 2026, July 7, 2026

Current Economic Trends; Overall Economic Situation

- FR.de; Lennart Niklas, Johansson Schwenck: Russia’s Economy Is Crumbling: How War, Interest Rates, and Drones Are Eroding Putin’s Economic Model, July 12, 26

- VEB Institute: “Global Economy and Markets,” Weekly Report July 3–9, 26; July 10, 26

- Welt+; Eduard Steiner: Nine Reasons for the Decline of the Russian Economy. Now in its fifth year of war, the Russian economy suddenly finds itself facing nothing but problems. Growth is nowhere in sight. Leading Russian economists explain the main reasons for this here, July 9, 2026

- Finam.ru: Novak stated that the situation in the Russian economy is fully under control. The Ministry of Finance was tasked with reporting on the situation on the stock market, July 7, 26

- BondGuide; Russia: Prices aren’t rising—they’re “changing,” July 7, 2026

- AOL; Reuters; John Irish and John O’Donnell: War threatens Russian banking crisis, European intelligence report says, July 5, 2026

- Russland.capital: Russia’s industry is showing growth for the first time in over a year. S&P Global’s Purchasing Managers’ Index (PMI) rose to 50.3 points in June; July 4, 2026

- BOFIT, Bank of Finland: Russia faces increasing challenges in balancing its economic policies; Weekly Review 27/2026, July 3, 2026

- Lenta.ru: The Central Bank has identified the conditions for sustainable growth in the Russian economy. To return Russian GDP to a path of sustainable growth, labor productivity must be increased; July 3, 2026

- Olga Belenkaya; Finam.ru: May 2026 Results: Accelerated Consumer Spending Growth, Manufacturing Suffers Losses; July 2, 2026

Fuel Supply, Energy Sector, Oil Prices

- Tagesschau.de: Fuel Crisis: Long Waits at Russian Gas Stations, July 10, 2026

- Monocle.ru: Oil prices began to rise rapidly. July 9, 2026

- Vedomosti, Mikhail Belyaev: Key points from Putin’s meeting on the fuel situation in Russia. Export ban on diesel fuel, a one-third increase in demand, and supply via a network of small refineries, July 8, 2026

- FR.de, Christian Stör: Continuous drone strikes are having an effect: Russia’s economy is on the verge of collapse—“explosive situation,” July 8, 2026

- Telepolis; Marcel Kunzmann: From Moscow to Siberia: Russia’s fuel crisis is coming to a head, July 7, 2026

- LBBW: Oil prices exhibit very high volatility; Mid-Year Outlook 2026 | War in Iran triggers temporary oil rally—Brent climbed to nearly $120 in March; July 7, 2026.

- Merkur.de; Jens Kiffmeier: “As Long as There’s No Beer Shortage”: How Gasoline Frustration Is Eroding Support for Putin’s War, July 6, 2026

- Finanzmarktwelt; Dói Ennoson: Sanctions prevent higher revenues. Russian oil: India overtakes China. Drone attacks force record oil exports; July 6, 2026

- CNN: Clare Sebastian, Zahra Ullahva, Katharina Krebs, Lou Robinson: “Almost every Russian region hit by fuel crisis, as Ukraine escalates drone attacks,” July 6, 2026

- U.S. Energy Information Administration: Short-Term Energy Outlook; Release Date: July 7, 2026

- NAGA: Oil Forecast and Price Predictions H2 2026: Prices are expected to moderate. Global oil prices surged over 50% after the U.S.–Israel–Iran conflict erupted on February 28, 2026. Will oil prices continue to rise in H2 2026? Here are the latest oil forecasts and price predictions, July 6, 2026

- russland.capital: Russia Reassures the Public on Gasoline—But the Crisis Remains Tangible, July 2, 2026

Monetary Policy: Previews of the Key Interest Rate Decision on July 24

- russland.capital: Business Association Does Not Expect Another Interest Rate Cut, July 8, 2026

- Finam.ru; Post-Meeting Analysis: The Central Bank Has Pulled the Emergency Brake. Could It Now Follow Up With an Interest Rate Hike? July 5, 2026

Warnings of a banking crisis and high corporate debt

- russland.capital: Russian corporate debt rises to record levels, July 8, 2026

- Gießener Allgemeine; Mark Simon Wolf: EU Targets Russian Banking Sector—Is Putin’s Financial System Facing a “Lehman Moment”? The EU is preparing its 21st package of sanctions against the Russian economy. The focus is on the banking system and crypto networks; July 7, 26

- ORF: Intelligence report warns of Russian banking crisis, July 6, 2026

- Finance Yahoo; The Telegraph, Melissa Lawford: Half a million Russians go bankrupt as Putin risks banking crisis, July 6, 2026

- AOL; Reuters; John Irish and John O’Donnell: War threatens Russian banking crisis, European intelligence report says, July 5, 2026

Fiscal Policy; National Budget and Oil Prices

- Focusonline; Lars-Eric Nievelstein: War in Ukraine. Russia’s economy is $75 billion in the red. Russia is losing a lot of money because oil and gas are no longer generating enough revenue, July 12, 2026

- russland.capital: Russia’s budget deficit remains larger than planned—despite a slight easing in June, July 10, 2026

- Finmarket.ru: In the first half of the year, the Russian budget deficit amounted to 5.7 trillion rubles, July 9, 2026

- Bruegel; Marek Dabrowski: How much has the Russian budget gained from higher oil prices related to the war in Iran? Russia has gained some fiscal headroom from higher oil prices, though not enough to fully offset budgetary difficulties from the war in Ukraine, July 8, 2026

- The Conversation; Alexander Titov; Lecturer in Modern European History, Queen’s University Belfast: The war in Ukraine is not going well for Russia—how dangerous is this for Vladimir Putin? July 7, 2026

- FG Finam, Nikolaj Dudchenko: Oil prices are falling, the budget is under threat; July 7, 2026

- Finanzmarktwelt; Dói Ennoson: Sanctions are preventing higher revenues. Russian oil: India overtakes China. Drone attacks force record oil exports; July 6, 2026

- Business Insider Germany: Russia’s War Chest at Its Limit: This Scenario Could Force Putin to End the War; Russia’s War Financing Reaches Its Limits: At the current intensity of fighting, Moscow still has funds for a maximum of one and a half years. In an interview with the “Frankfurter Allgemeine Zeitung,” economist Alexandra Prokopenko paints a picture of growing structural problems, July 6, 2026

Political Environment; Nord Stream 2; Miscellaneous

- Russia Analyses No. 485; Theodore P. Gerber: Inequality in the Era of the Russian War Economy; Ranking: Russians on the Forbes List of Global Billionaires 2026; July 8, 2026

- russland.capital: Nord Stream 2 Will Not Receive Insurance Payouts for Pipeline Explosion, July 8, 2026

- Berliner Zeitung; Michael Maier: Nord Stream Loses Case in London Court: Interesting Theories About the Perpetrators. The operators of the Nord Stream gas pipelines had filed a lawsuit against Lloyd’s Insurance Company and Arch Insurance in 2024; July 7, 26

- Overton: Uwe Froschauer: Germany Continues to Pay Ukraine—Despite Nord Stream, July 7, 26