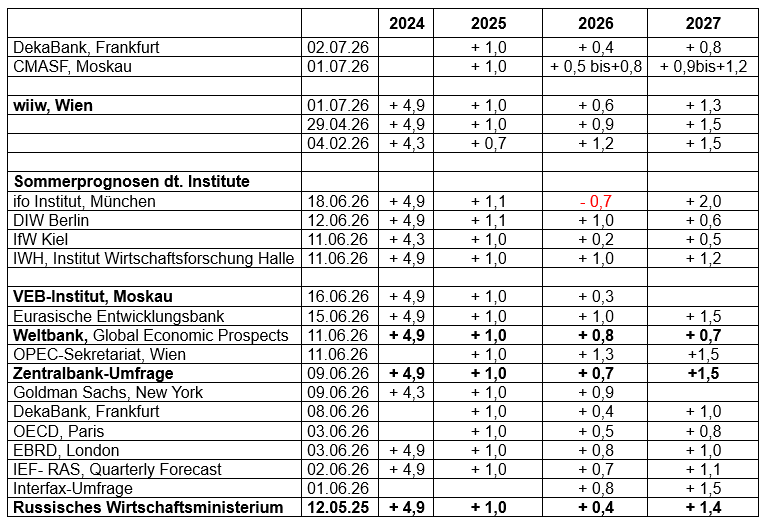

The wiiw is also lowering its 2026 GDP forecast for Russia even further

Author: Klaus Dormann

On July 1, the “Vienna Institute for International Economic Comparisons” further lowered its forecast for this year’s growth in the Russian economy in its “Summer Forecast” for economic developments in Central, Eastern, and Southeastern Europe. The wiiw now expects aggregate economic output to rise by only 0.6%. In early February, it had projected that the Russian economy would grow at twice that rate in 2026 (+1.2%).

The wiiw forecast largely aligns with the Central Bank’s analyst survey

The wiiw is thus following the trend in the Russian Central Bank’s analyst survey. As of early June, participants in that survey were already expecting, on average, economic growth of just 0.7 percent in Russia for 2026. Previously, in early May, the Russian government had unexpectedly cut its growth forecast for 2026 sharply to 0.4 percent. The Moscow-based “Center for Macroeconomic Analysis and Short-Term Forecasts” (CMASF) anticipates growth that is similarly weak to the government’s projection. Since the beginning of the year, its monthly forecasts have assumed that GDP growth in the current year could fall to as low as 0.5 percent.

For 2027, the CMASF expects growth to pick up to a maximum of 1.2 percent, similar to the wiiw’s forecast (+1.3 percent). The CMASF and wiiw thus remain slightly below the Russian government’s growth forecast for 2027 (+1.4 percent) and the result of the latest Central Bank survey on growth for next year (+1.5 percent).

Frankfurt-based DekaBank, the securities firm of the German savings banks, had already lowered its forecast for this year’s Russian economic growth to 0.4 percent in early June—as the government had done previously. Last week, it also further revised down its forecast for next year from 1.0 to just 0.8.

The vast majority of forecasts for this year’s growth in the Russian economy now range between 0.4 and 1.0 percent. For next year, nearly all observers expect growth to pick up slightly. However, the forecasts from the Munich-based ifo Institute fall outside this range. Ifo expects the Russian economy to plunge into a recession this year (-0.7 percent) but to grow by 2.0 percent next year.

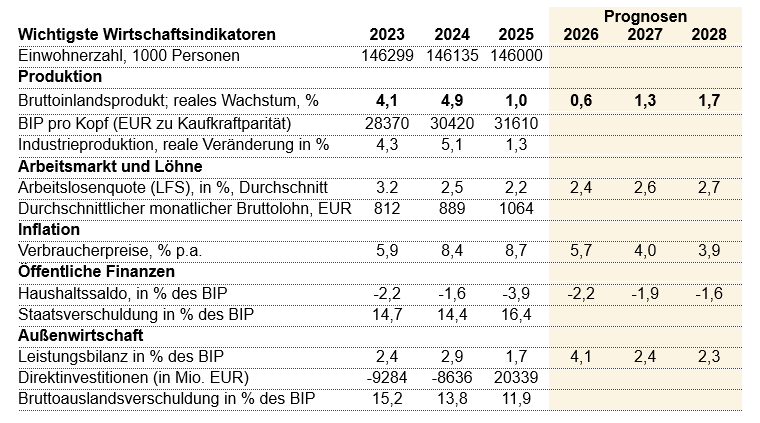

GDP Forecasts for Russia 2024–2027: Year-over-year change in real gross domestic product, in percent

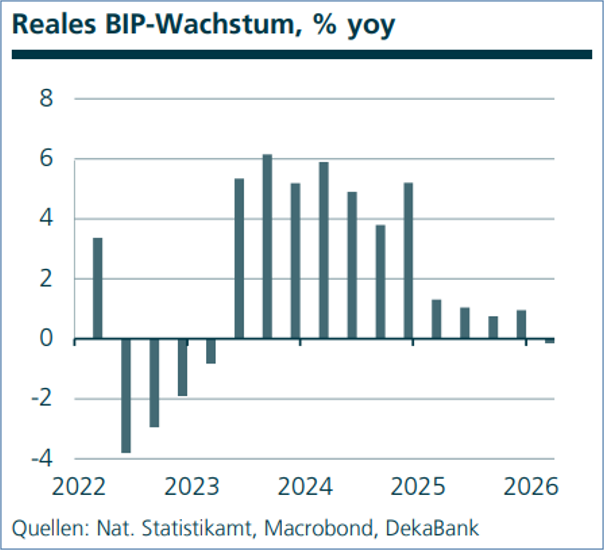

DekaBank: In the first quarter of 2026, Russia’s GDP fell by 0.2 percent

The following chart from DekaBank, taken from the July issue of “Emerging Markets Trends,” clearly illustrates how sharply Russia’s economic growth has slowed. The economic boost from war spending, which drove output in the Russian economy up by 4.1 percent in 2023 and 4.9 percent in 2024, resulted in growth of only 1.0 percent in 2025. In the first quarter of 2026, real GDP contracted by 0.2% compared to the same quarter of the previous year.

Real Gross Domestic Product,

Year-over-Year Changes in Percent

DekaBank: Emerging Markets Trends, July 2, 2026

The problems are currently worsening: fuel is in short supply

According to DekaBank’s assessment, there may have been a temporary revival of the Russian economy in the second quarter of 2026, as energy prices rose sharply for a time due to the blockade of the Strait of Hormuz and U.S. sanctions against the Russian oil industry were partially suspended. Nevertheless, the bank believes that Russia’s economic problems are worsening. It points in particular to problems with fuel supplies and the rise in the government budget deficit. In summary, the bank writes:

As a result of the Ukrainian drone attacks, eight of the ten largest refineries and several smaller ones were hit. Official statistics on fuel production have not been published since 2024. However, the long lines at gas stations and regional sales restrictions point to a severe shortage, at least of gasoline. Diesel, which is primarily important for the transportation sector and agriculture, also appears to be becoming scarce in some regions.

The fuel crisis portends a new wave of inflation in both the goods and services sectors. This limits the central bank’s room to maneuver for further interest rate cuts.

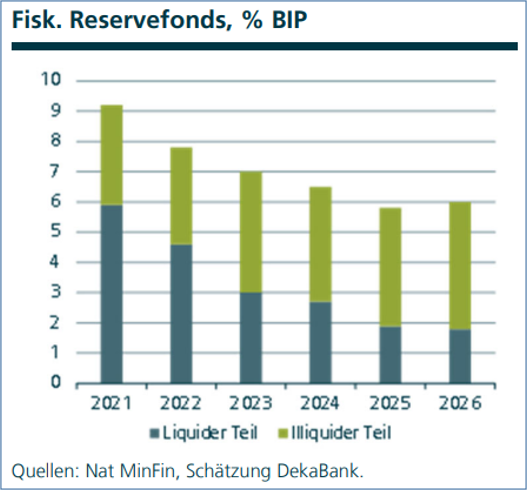

The liquid portion of the reserve fund has fallen sharply

DekaBank cites the rising budget deficit as another problem area. Under the burden of military spending (about 30% of total expenditures), the deficit-to-GDP ratio had already reached 2.6% by May, despite increases in taxes and levies. However, a deficit of only 1.6% of GDP is projected for the full year. The current fuel crisis is likely to place an additional strain on the budget on the expenditure side, while revenues will decline in tandem with falling oil prices.

According to DekaBank, Russia’s accumulated fiscal reserves are no longer sufficient to “plug the budget hole.” The freely available liquid portion of the reserves has fallen from nearly 6% of GDP in 2021 to just 1.8% of GDP (see the figure below).

DekaBank: Emerging Markets Trends, July 2, 2026

According to DekaBank, the Ministry of Finance is now resorting to additional borrowing as a solution for 2026. The bank estimates that while this may “work in the short term,” it will lead to “even greater macroeconomic instability” in the medium term.

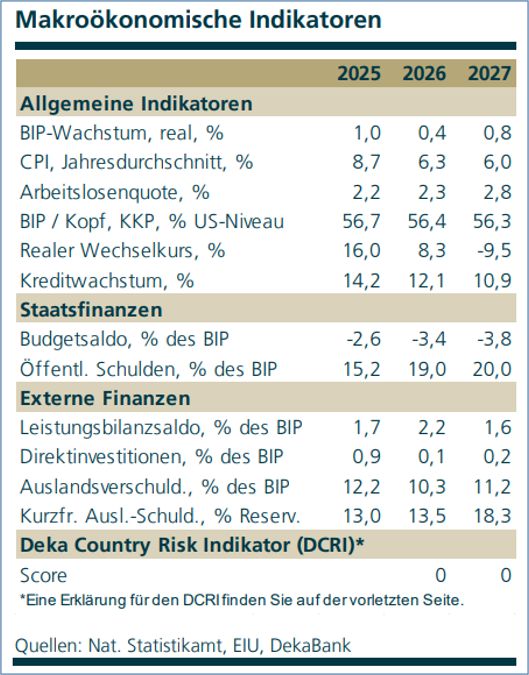

With weak economic growth, the budget deficit will rise in 2026 and 2027

DekaBank expects Russia’s federal budget deficit to rise from 2.6 percent of GDP in 2025 to 3.4 percent this year and to reach 3.8 percent of GDP in 2027.

The ratio of public debt to gross domestic product—which remains low by international standards—is thus likely to rise to 20 percent by 2027.

DekaBank: Emerging Markets Trends, July 2, 2026

Central Bank Vice President: The Fuel Crisis Is Weighing on Industrial Production

The crisis in the fuel market will impact Russia’s economic performance in the second quarter of 2026, said Alexei Zabotkin, deputy chairman of the Central Bank, on the sidelines of the “Bank of Russia” Financial Congress.

“This is clearly evident in the industrial production data for April and May: We have recorded a fairly significant decline in production in the fuel sector. This will, of course, be reflected in the second-quarter GDP figure.”

However, Zabotkin does not believe that the “fuel crisis”—following a 0.2 percent decline in gross domestic product in the first quarter—will lead to another year-over-year decline in production in the second quarter.

Previously, Central Bank President Nabiullina had estimated annual GDP growth for the period from January to April at 0.3% during the press conference following the latest key interest rate cut. She forecast growth of around 0.5% for the first half of the year (Interfax.ru).

wiiw: Russia is “in a veritable state of stagnation”

The “Vienna Institute for International Economic Comparisons” now forecasts only “minimal” growth of 0.6% for Russia’s total economic output in 2026, 0.3 percentage points less than in its “Spring Forecast” released at the end of April. In 2027, growth is then expected to pick up to 1.3% (spring forecast: 1.5%).

Although Russia’s energy revenues have temporarily increased due to rising prices caused by the war in Iran, the country is, according to the wiiw’s press release, “in a state of veritable stagnation.” Vasily Astrov, a Russia expert at the wiiw, explains it this way:

“The main reason for this is the central bank’s monetary policy, which remains too restrictive and is stifling the economy by making borrowing prohibitively expensive, especially for purchases of durable consumer goods and investments.”

The institute points out that investment activity fell by about 14% in the first quarter of 2026—partly due to the bleak economic outlook and the fact that opportunities to replace imports with Russian products have been exhausted.

Regarding the economic consequences of the “massive Ukrainian drone attacks” on Russian energy facilities, the wiiw notes that, according to estimates, one-third of Russia’s refining capacity has already been crippled by the attacks. Russia expert Astrov:

“There are fuel supply shortages in many places. This will, of course, have negative effects on economic activity in the country and, along with internet blackouts, war fatigue, and the economic slump, was one of the reasons why President Putin’s popularity has recently declined significantly.”

At the same time, however, Astrov emphasizes that Russia will still be able to continue and finance its war of aggression against Ukraine.

wiiw Country Overview: Inflation Rate to Fall to 4 Percent in 2027

In its updated “Country Overview: Russia,” the wiiw notes regarding production trends that the 0.3% increase in industrial production during the first four months was primarily due to continued growth in the production of military equipment. Private consumption, on the other hand, is developing “quite stably”: Retail sales rose by 4.3% in real terms.

wiiw Country Overview: Russia

The wiiw’s forecasts for the rise in consumer prices largely align with the Central Bank’s “Medium-Term Forecast.” In the current year, the annual average inflation rate is expected to fall to 5.7 percent (Central Bank forecast: 5.1 to 5.6 percent). In 2027, the wiiw, like the Central Bank, expects the Central Bank’s inflation target of 4.0 percent to be achieved.

DekaBank, on the other hand, anticipates significantly higher inflation in Russia. In 2026, the rate will fall to only 6.3 percent, and in 2027, it will barely decline further to 6.0 percent.

Controversial Forecasts on the Development of the Budget Deficit

The wiiw also assesses the trend in the budget deficit as much more favorable than DekaBank does.

The wiiw expects the deficit-to-GDP ratio to be cut in half, from 3.9 percent of GDP in 2025 to just 1.9 percent in 2027. However, the deficit ratio cited by the wiiw is not the most commonly cited deficit ratio in the Russian federal budget, but rather the deficit ratio in the “consolidated government budget” (the sum of the deficits of the federal budget, regional budgets, and state extrabudgetary funds; see: The Moscow Times).

At the same time, DekaBank expects the federal budget deficit ratio to rise from 2.6 percent in 2025 to 3.8 percent in 2027 (see, for example, bne Intellinews for information on the development of the federal budget).

From January through May 2026, the federal budget deficit-to-GDP ratio also stood at 2.6 percent (TASS).

Finance Minister Siluanov: The budget deficit will “rise slightly” in 2026

At the SPIEF in St. Petersburg and previously in an interview with the newspaper Kommersant, Finance Minister Siluanov commented on budget developments. He explained that this year’s federal budget deficit would “rise slightly” compared to the previously planned 1.6% of GDP. However, this should “not result in any significant changes to the level of domestic debt.” The reasons for the revision are “changes in macroeconomic conditions compared to the original plans, as well as the need to focus resources more strongly on key priorities” (Finam.ru).

- BOFIT: Federal budget spending continues to rise rapidly

The BOFIT research institute of the Bank of Finland, however, states in its latest weekly report on the federal budget’s development:

“Russian federal budget expenditures have skyrocketed in the first five months of this year, significantly exceeding the increase of a few percent envisaged in the official budget. According to preliminary figures, federal budget spending rose by 17 percent in the first five months of this year compared to the previous year.”

“Revenue growth has not kept pace with spending growth. From January through May, total federal budget revenue was on par with the same period last year.

Following a weak start to the year, oil and gas revenues remained 30% below the previous year’s level. The rise in oil prices caused by the war in Iran did not become apparent in the Russian budget until May, when oil and gas revenues rose by 33 percent compared to the previous year. However, the impact of high oil prices on budget revenues was partially offset by government compensation payments. These were intended to encourage oil refineries to sell their products to domestic consumers rather than export them.

Other federal budget revenues grew by 12% year-over-year in the first five months of this year, primarily due to higher value-added tax (VAT) revenues.

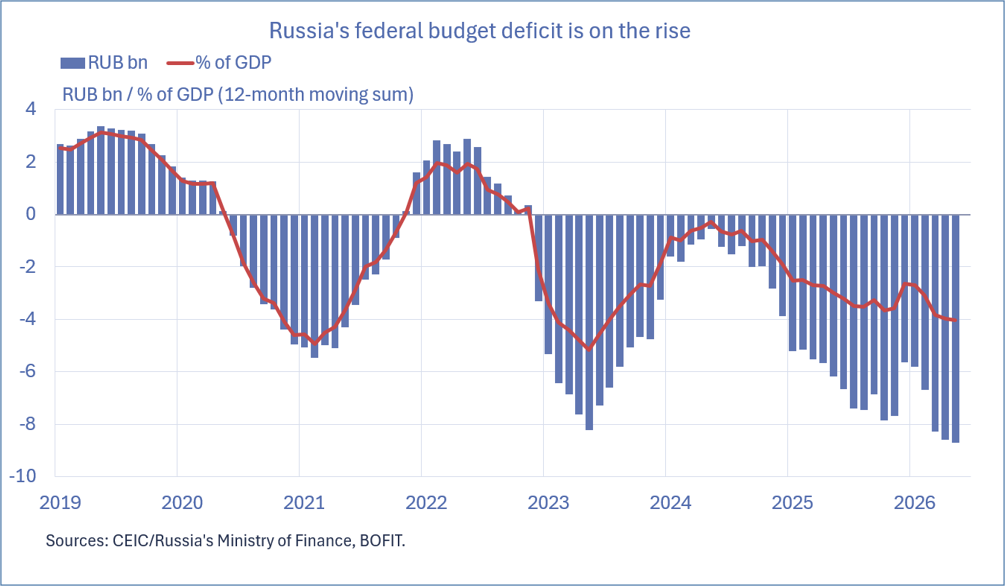

The federal budget deficit rose to 6 billion rubles (2.6% of GDP) from January through May—double the amount projected for the entire year of 2026.

The Russian federal budget deficit is rising by

billion rubles and as a percentage of GDP

(rolling 12-month total)

BOFIT, Bank of Finland: Russia faces increasing challenges in balancing its economic policies; July 3, 2026

BOFIT: Russia’s economic policy faces increasing challenges

Overall, BOFIT sees the Russian government facing increasing challenges “in balancing its economic policies.” The institute explains this as follows:

“The rising costs of the war in Ukraine have forced the Russian government to increase spending, causing the budget deficit to rise further.

The high growth in spending is exacerbating inflationary pressures and making it more difficult for the central bank to lower the key interest rate. High interest rates are dampening investment and reducing profits, particularly for companies without access to government-subsidized financing. …

High interest rates also increase the cost of debt service, which is particularly concerning because Russia’s growing deficit is being financed through borrowing.”

CMASF: What is currently going “well” and what is going “poorly” in the Russian economy?

The Moscow-based “Center for Macroeconomic Analysis and Short-Term Forecasts” has once again compiled a list of key positive and negative current developments in its July economic report, “Analysis of Macroeconomic Trends.” Here is a selection:

“Good” news:

- The relatively favorable situation on the international oil and metals markets continues.

- Growth in private consumption has resumed.

- Real wages continue to rise.

- Growth in wholesale trade has resumed (likely an indication of a pickup in overall economic growth).

- Government fiscal policy is providing a positive stimulus to the economy.

Signs of improvement include:

- The central bank continues to lower its key interest rate (slowly).

- Profitability in the industrial sector has improved slightly.

- The public’s assessment of their personal financial situation has improved somewhat.

On the “negative” side:

- In most “civilian” industrial sectors, production is stagnating or declining.

- The decline in investment is accelerating, particularly in machinery and equipment.

- The population’s real disposable income has fallen on a seasonally adjusted basis (which is most likely due to declining returns on financial investments).

- A noticeable inflationary impulse has emerged. However, it is clearly of a “non-monetary nature.” The main causes of the price surge are rising prices for fruits and vegetables, rising fuel prices, and increasing burdens from tariffs in the “domestic tourism and leisure” sector.

Signs of a deterioration include:

- The increase in the influx of competing imports.

- In the income structure of GDP, the share of profits (available investment capital) has decreased, while the share of wages has increased.

- Management’s negative assessment of the economic situation persists.

- The interest burden on companies is extremely high.

The CMASF draws the following conclusion: Although a recovery has been observed in some macroeconomic indicators, GDP growth this year is unlikely to exceed one percent, even taking into account the improved external economic situation, given the sharp decline in investment.

In its “Base Scenario of the Macroeconomic Forecast for the Period 2026–2029,” , the CMASF projects GDP growth of 0.5 to 0.8 percent for 2026 and 0.9 to 1.2 percent for 2027.

In the first five months of 2026, the economy grew by only 0.2 percent

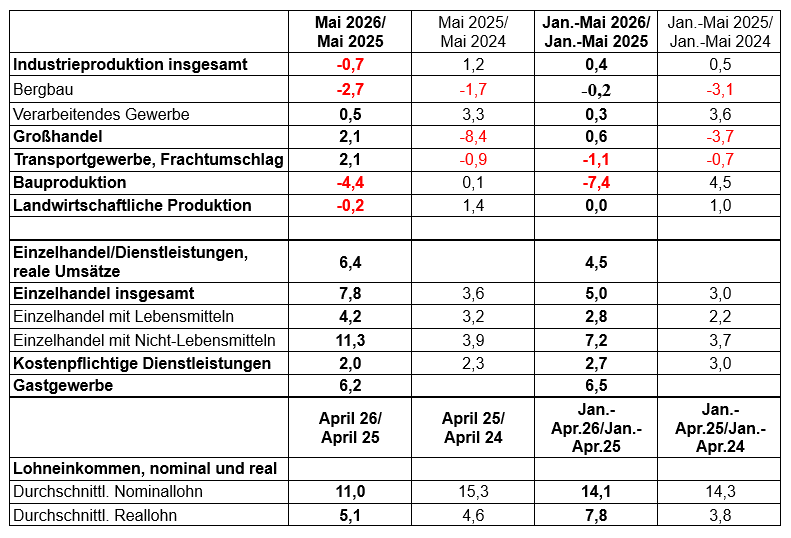

According to the Russian Ministry of Economic Development, growth in aggregate economic output continued in May 2026. According to preliminary estimates, real gross domestic product was 0.3% higher than in May of the previous year. In the first five months of 2026, the economy grew by 0.2% year-over-year, the same as in the first four months, according to the ministry’s report.

Further results of economic performance through May

In the so-called “core sectors” of the Russian economy, production in May 2026 stagnated at the level reached in the same month of the previous year. The production index for these core sectors is calculated based on data regarding changes in production volume in industry, agriculture, construction, freight handling in the transportation sector, and retail and wholesale trade. From January through May 2026, production in these core sectors fell by a total of 0.1% compared to the previous year.

Industrial production fell by a total of 0.7% in May 2026 compared to the previous year (January through May: +0.4%). Production in the “mining” sector declined by 2.7% in May. In the manufacturing sector, it rose by 0.5%.

The decline in production in the petroleum processing sector accelerated significantly: According to Rosstat, production of coke and petroleum products fell by 13.5% year-over-year in May, a decline likely linked to the intensified attacks on oil refineries (Olga Belenkaya in Finam.ru).

Wholesale trade rose by 2.1% in May (January–May: +0.6%).

Freight transportation also increased by 2.1% in May (January–May: -1.1%).

Construction output fell by 4.4% in May (January–May: -7.4%).

Agricultural production in May was 0.2% lower than a year earlier (January through May: stagnation at the previous year’s level).

Real retail sales rose by 7.8% in May (January–May: +5.0%).

Economic Indicators for May 2026 Compared to May 2025

: Year-over-Year Changes in %

Olga Belenkaya; Finam.ru:

May 2026 Results: Accelerated Consumer Spending Growth, Industry Posts Losses; July 2, 2026

Recommended Reading:

German-Russian Chamber of Foreign Trade:

Analyses, in German; also in Russian; (selection):

- Gasoline Crisis in Russia, June 30, 2026

- Small Interest Rate Hike Dampens Business Hopes, June 23, 2026

- Prof. Dr. Alexander Liebmann in conversation with Thomas Baier on the German-Russian Chamber of Foreign Trade’s podcast “Tsars, Data, Facts”: Russia’s Economy: Between Stagnation and Recession, 27 min., In this episode, Prof. Alexander Liebmann of the Free University (FU) of Berlin explains that, as he predicted, the Russian economy has been moving toward stagflation: Growth is near zero while inflation remains high. He does not view the central bank as the main cause of the economic slowdown, as structural factors such as labor shortages, full employment, and high military spending are limiting growth; June 16, 2026

Economic Forecasts:

- DekaBank: Emerging Markets Trends, Russia: Gasoline Shortages Due to Ukrainian Attacks, July 2, 2026

- CMASF: Forecast of Russia’s Socioeconomic Development for 2026–2029, July 1, 2026

wiiw Summer Forecast:

- bne Intellinews; Clare Nuttall: Growth in Central, Eastern, and Southeast Europe Holds Firm in 2026, Says wiiw; July 1, 2026

- Vienna Institute for International Economic Comparisons; wiiw: Summer Forecast 2026;

Andreas Knapp: Summer Forecast: War in Iran Will Have Only a Minor Impact on Growth in Eastern Europe, July 1, 2026; Press Releases: English; German - wiiw Country Overview: Russia; Additional Press Coverage: wiiw in the press

- “Die Presse” podcast “Russia – Gas, Sanctions, Oligarchs”; Eduard Steiner in conversation with Vasily Astrov, wiiw: Is Russia’s Economy Really in Its Final Stages? 38 min., June 17, 2026

Current Economic Developments

- BOFIT, Bank of Finland: Russia faces increasing challenges in balancing its economic policies; Weekly Review 27/2026, July 3, 2026

- Lenta.ru: The Central Bank has identified the conditions for sustainable growth in the Russian economy. To return Russian GDP to a sustainable growth path, labor productivity must be increased. July 3, 26

- Interfax.ru: The deputy chairman of the Central Bank expects the fuel situation to dampen GDP growth in the second quarter; July 3, 2026

- Interfax.ru: According to the Central Bank, real wages are growing faster than productivity; July 3, 2026

- Olga Belenkaya; Finam.ru: May 2026 Results: Accelerated Consumption Growth, Manufacturing Suffers Losses; July 2, 2026

- Prime.ru: An expert explained the factors that supported Russian GDP growth in May. Nametkin: The consumer sector supported Russian GDP growth in May, July 1, 2026

- Interfax.ru: Russia’s GDP grew by 0.3% year-over-year in May and by 0.2% from January through May, July 1, 26

- Interfax.ru: The share of consumer spending in Russian GDP rose by 3.5 percentage points in the first quarter; Rosstat confirmed its estimate of a 0.2% year-over-year decline in GDP for the first quarter of 2026; July 1, 2026

- Interfax.ru: Production in Russia’s key sectors showed no growth in May; July 1, 2026

- InvestFuture, TASS: Revenue growth in the restaurant industry is accelerating, reaching 520.6 billion rubles in May, July 1, 2026

- MEC Analytics: Industrial Production: External Factors Remain the Cause of the Decline, June 26, 2026

- Finmarket.ru: Industrial production in Russia fell by 0.7% in May, June 24, 2026

- russland.capital: German Gref warns of a slowdown in the Russian economy, July 1, 2026

- Interfax.ru: Reshetnikov called the timing of the resumption of investment growth in Russia a difficult question, June 30, 2026

- AOL, Mark Trevelyan; Reuters: Economic pessimism among Russians at its highest in at least 20 years, Gallup poll shows, June 30, 2026

- FR.de; Fabian Hartmann: Russia’s economy is struggling, but it’s probably not over yet; June 30, 2026

- Janis Kluge, German Institute for International and Security Affairs (SWP), in conversation with Mary Abdelaziz-Ditzow on the “Im Loop” podcast: Have the sanctions against Russia fizzled out? Kluge outlines the current situation and analyzes the key mechanisms behind Russia’s resilience, video, 71 min., June 27, 2026

Monetary Policy: Is Russia’s Economy “Overcooled” Due to High Interest Rates?

- Finmarket.ru: Central Bank Chief: There is now room for an interest rate cut, but the timing and pace depend on how the situation develops, July 3, 2026

- russland.capital: Nabiullina contradicts Gref: The Russian economy is not “overcooled”; with Russia TV video, July 2, 2026

- russland.capital: German Gref warns of an “overcooling” of the Russian economy, with a Russia TV video of Gref’s statements at Sberbank’s annual general meeting; July 1, 26

- Interfax.ru: Reshetnikov called the timing of the resumption of investment growth in Russia a difficult question, June 30, 2026

Fiscal Policy; National Budget and Oil Prices

- Public News Service; Roman Kotlov: Dmitriev rejected Western assessments of the Russian economy, national debt, and budget deficit; June 25, 26

- TopWar.ru; Alexey Volodin: Russian oil has once again reached the “budget planning” price level, June 24, 2026

- Tass.ru: Ministry of Finance: The budget deficit for the first five months of 2026 amounted to 6.01 trillion rubles; June 25, 2026

- Olga Belenkaya, FG Finam: Budget: Signs of stabilization emerged in May, June 8, 2026

- SFG Media, Dmitry Fesenko; Reuters: Russia’s Oil and Gas Budget Revenue Rose 32% in May—Driven by High Oil Prices and the Suspension of U.S. Sanctions; June 23, 2026

- Military & History; Torsten Heinrich: Russia’s Oil Crisis Is Becoming Dramatic!; Video, 17 min., June 22, 2026

- Kommersant Interview with Finance Minister Siluanov; Matvey Ivaschenko: Budget, Taxes, and Oil Dependence. Key Points from the Interview with Anton Siluanov, May 27, 26; “We must increase our financial safety margin.” Interview on the budget situation, tax administration, the “cleaning up of the economy,” and the prospects for IPOs of state-owned enterprises, May 27, 26.

Fuel Supply, Energy Sector

- russland.capital: Russia Reassures the Public on Gasoline—But the Crisis Remains Tangible, July 2, 26

- t-online: Ukraine strikes Russia. Bankers call for an end to the war; the fuel situation in Russia is coming to a head. There is disagreement within the power structure over the course of action. July 2, 2026; Source: Politico.eu; Geoffry Smith: Putin’s economy is running on fumes after Ukrainian attacks. Drone and ballistic missile strikes are pushing Russia to the breaking point, July 2, 2026

- Brome.ai: Oil Prices Hit Pre-War Levels, June 27, 2026

- Inosmi.ru; Bloomberg USA: Russia Will Supply Record Amounts of Oil in 2026, June 24, 2026

- Telepolis; Bernd Müller: Gazprom Facilities on Fire: “Russia’s Economy Is in Its Final Stages,” June 22, 2026

- allsides.com: WSJ Journalist Publishes Book on Nord Stream Pipeline Sabotage, June 16, 2026

- Transparency International: Nord Stream. Gas, Gerd, and a Lot of Detailed Work. The Parliamentary Investigative Committee on the Mecklenburg-Western Pomerania Climate Foundation – For four years, an investigative committee has been examining the events surrounding the MV Climate Foundation and Nord Stream 2; Schwerin, June 15, 2026.

Foreign Trade; Russia in the Global Economy

- EURACTIV.com; Nikolaus J. Kurmayer: Brussels Rejects the AfD’s Calls for a Return to Russian Gas, June 30, 2026

- Reuters; John O’Donnell: AfD leader vows to restore German-Russian ties as she eyes the chancellery, June 30, 2026; Inosmi.ru: Haqqin.az Azerbaijan: The plan of Germany’s right-wing populists: Become chancellor and restore relations with Russia; Weidel: Germany has lost hundreds of thousands of jobs by breaking ties with Russia; June 30, 2026

- russland.capital: Western Companies Are Losing Billions in Russia, June 23, 2026