Is the downward revision of Russia’s growth forecasts now in its “final stages”?

Author: Klaus Dormann

Many forecasts for Russia’s economic growth this year are currently being lowered even further. However, almost all remain higher than the Russian government’s forecast. On May 12, it was unexpectedly slashed from 1.3 percent to just 0.4 percent. This placed the government at the lower end of the range of forecasts by international economic organizations, research institutes, and banks for the growth of the Russian economy in 2026. A very unusual picture. After all, governments usually paint as positive a picture as possible of their economies’ development. Moreover, the Russian government is frequently accused of presenting its statistics in a way that makes the economic situation look better than it really is.

Central Bank Survey: Analysts Expect More Growth Than the Government

The analysts regularly surveyed by the Russian Central Bank ahead of its key interest rate decisions now also expect, on average, more growth this year than the government does. In early April, they had still anticipated that the Russian economy would grow by 1.0 percent this year, as it did in 2025. Now, according to the survey published last week, they expect real gross domestic product growth to slow to 0.7 percent in 2026. Next year, however, the approximately 35 survey participants—including some foreign analysts—still expect growth to accelerate to 1.5 percent. The Russian government does expect a significant recovery in growth from 0.4 to 1.4 percent by then. However, this figure will still remain just below the “consensus” of analysts in the Central Bank survey next year as well.

However, the “Kiel Institute for the World Economy” in Russia now expects even less growth than the Russian government. In its “Summer Forecast” published last week, it lowered its forecast for Russia for the current year to just 0.2 percent growth. By 2027, Russia’s GDP growth is expected to rise to just 0.5 percent. In contrast, the Berlin-based DIW and the Halle Institute for Economic Research forecast that the Russian economy will grow by one percent in 2026, as it did in 2025.

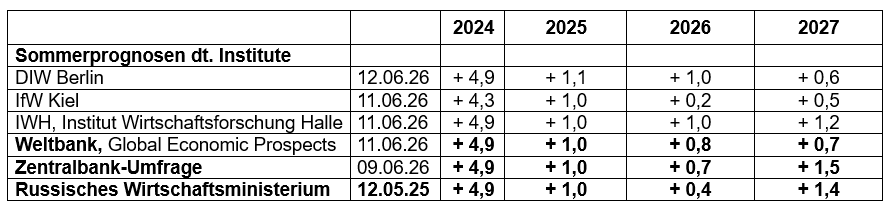

GDP Forecasts for Russia 2024–2027

Year-over-year change in real gross domestic product, in percent

The World Bank is not further lowering its growth forecasts for Russia

The World Bank had already lowered its forecasts for Russian economic growth in early April. In its recently published “Global Economic Prospects,” it maintains its view that Russia’s economic growth will slow to 0.8 percent in 2026 and further to 0.7 percent in 2027. Unlike the government and analysts, it does not expect growth to accelerate next year.

The World Bank’s baseline scenario assumes that the “most acute phase” of disruptions in commodity trade will end in July and that the number of ship transits through the Strait of Hormuz will recover so significantly in the second half of the year that global energy supplies will gradually return to pre-crisis levels.

In Russia, the World Bank estimates that the impact of the Middle East conflict on economic activity will be limited. The World Bank expects the Russian government to use additional oil revenues primarily for fiscal consolidation.

The Central Bank is sticking to its “growth range” of 0.5 to 1.5% for 2026

According to its “Medium-Term Forecast” released on April 24, the Russian Central Bank expects Russia’s GDP growth in 2026 to range between +0.5% and +1.5%. According to the Central Bank’s “calendar,” this forecast will not be updated again on Friday when the next key interest rate decision is made, but rather on July 24. Following the government’s downward revision of its 2026 growth forecast to just +0.4 percent, it is particularly interesting to see whether the Central Bank will follow the government’s assessment and "zero growth" to a range of +0.0 to +1.0.

This is likely why the central bank’s Deputy President, Alexei Zabotkin, made it clear in a Vedomosti interview published on June 11: “The first-quarter results give us no reason to change our forecast for the full year.” He added that the figures for January and February had been significantly distorted by “one-off factors,” namely fewer working days than in the previous year, the unusually cold winter with heavy snowfall, and the bringing forward of many purchases of durable goods to 2025, as the value-added tax was increased at the beginning of 2026.

Overall, according to Zabotkin, current economic developments are in line with the Central Bank’s scenario, which assumes a gradual return of the economy to low inflation and balanced growth. Zabotkin added that the April data released in early June had confirmed positive annual trends for many indicators (1Prime.ru).

Central Bank: The GDP decline in the first quarter is now being offset

Regarding GDP development in the first quarter of 2026, dpa-AFX reported, among other things:

The Russian economy contracted in the first quarter for the first time since early 2023. According to Rosstat, gross domestic product fell by 0.2 percent compared to the same quarter of the previous year. In the fourth quarter of 2025, the economy had still grown by 1.0 percent.

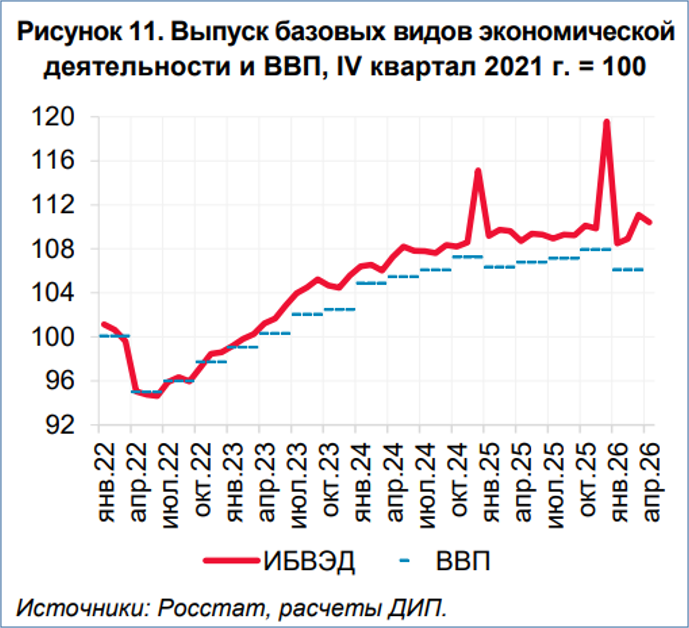

In the following figure from the Russian Central Bank’s bulletin on current economic trends (“What the trends say”) the dotted blue line shows the slight decline in the real gross domestic product index in the first quarter of 2026 compared to the first quarter of 2025.

The trajectory of the red line clearly illustrates how sharply production in the so-called “core sectors” of the Russian economy fluctuated at the end of 2025 and during the first four months of 2026 (core sectors include: industry, agriculture, construction, freight transport, and wholesale and retail trade). In April 2026, production in the economy’s “core sectors” was 0.8% above the average level for the first quarter, according to Central Bank calculations. Compared to April of the previous year, it rose by 1.7% according to Rosstat (Finmarket.ru).

Monthly trend in production in the “core sectors” (red line)

and quarterly trend in real gross domestic product (blue lines);

indices: Q4 2021 = 100

Sources: Rosstat, Central Bank

calculations; Bank of Russia: “What the Trends Say,” June 9, 2026

The Research and Forecasting Department of the Russian Central Bank expects the slight decline in production in the first quarter to be offset in the second quarter, partly due to the higher number of working days. According to the results of business surveys, economic activity increased in April and May compared to the first quarter (Finmarket.ru).

In a press release, the Central Bank notes that consumer demand continues to grow amid the sustained strong rise in incomes. The government budget continues to make a significant contribution to growth. Lower lending rates, driven by the key interest rates, are also supporting economic activity.

DIW and IWH expect significantly more growth in 2026 than the Kiel Institute

Last week, three of the five leading German economic research institutes published their “summer forecasts” for Germany and the global economy. The institutes’ assessments of the development of aggregate economic output in Russia once again varied considerably.

The “Kiel Institute for the World Economy” is particularly skeptical about Russia’s growth prospects. It significantly lowered its forecast for Russia’s growth this year. The IfW now expects only a very weak increase in output of 0.2 percent for 2026. In March, in its “Spring Forecast,” it had still expected Russia to maintain its growth rate—which had fallen to 1.0 percent in 2025—this year. The Kiel Institute also takes a relatively pessimistic view of Russia’s growth prospects for 2027: it maintained its spring forecast of 0.5 percent.

The “Halle Institute for Economic Research,” on the other hand, expects the Russian economy to continue growing by around 1 percent in 2026 and 2027. It has thus lowered its spring forecast for 2026 by only 0.1 percentage points. The IWH even raised its growth forecast for 2027 slightly, from 1.0 to 1.2 percent.

The Berlin-based “German Institute for Economic Research,” however, has now nearly halved its spring forecast for Russia’s growth in 2027 to just 0.6 percent. For the current year, however, the DIW, like the institute in Halle, expects the Russian economy to grow by 1.0 percent again. The RWI in Essen will publish its summer forecast on June 16, and the ifo Institute in Munich will release its forecast on June 18.

The table below shows the institutes’ spring forecasts for comparison.

GDP Forecasts for Russia 2024 to 2027

Year-over-year change in real gross domestic product, in percent

IfW Kiel: Russia’s oil and gas infrastructure has been “severely” affected

In its “Summer Forecast,” the Kiel Institute does not elaborate on why it assesses Russia’s growth prospects even more skeptically than the vast majority of analysts. In the forecast, it merely refers to “significant damage” to Russia’s oil and gas infrastructure caused by attacks from Ukraine:

“Russia is increasingly struggling to maintain its overall economic output, partly because Ukraine repeatedly succeeds in inflicting significant damage on the oil and gas infrastructure. Due to extensive damage to refineries and storage facilities, crude oil production has apparently had to be reduced in the meantime due to a lack of processing and storage capacity, and fuel shortages are increasingly occurring in some regions.”

At the same time, however, the IfW points out that Russian oil exports rose even though production was scaled back, because domestic oil processing had to be significantly reduced due to damage to refineries and storage facilities caused by Ukrainian drone attacks.

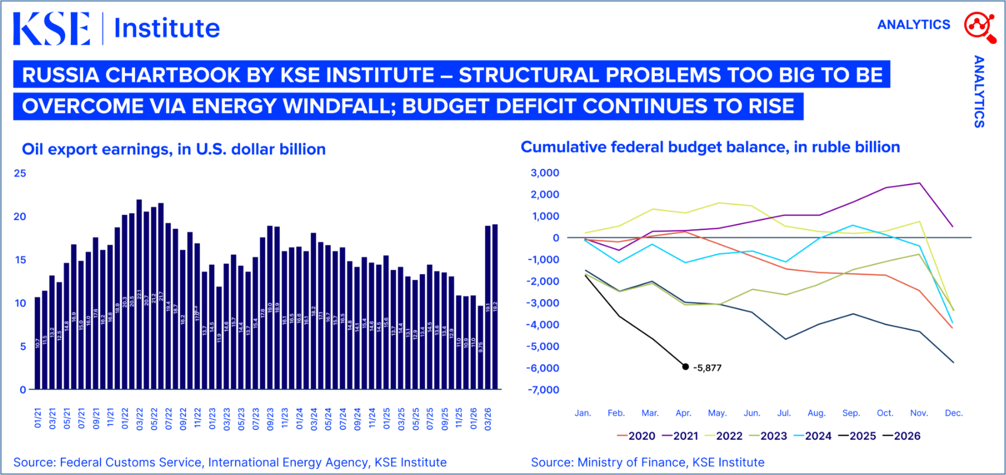

The following cover page of the “Russia Chartbook” published in early June by the Kyiv School of Economics shows on the left that Russia’s oil export revenues in March and April 2026 roughly doubled compared to February. The deficit accumulated in the federal budget during the first four months of 2026 was far higher than in previous years (right figure; black line).

Kyiv School of Economics:

Russia’s budget deficit continues to grow – despite energy windfall

Kyiv School of Economics Institute: Russia Chartbook, May 2026; June 2, 2026

New “Kiel Report”: “Endgame: The State of the Russian Economy”

Along with its summer forecast, the IfW also published a new “Kiel Report” prepared in collaboration with the “Stockholm Institute of Transition Economics” titled “Endgame: The State of the Russian Economy.”

The IfW presents it in a press release as follows:

“Four years after Russia’s large-scale invasion of Ukraine, the Russian economy is showing clear signs of structural exhaustion. Evidence that the Russian economy is in its final stages is mounting. …

The Kiel Report “Endgame: The State of the Russian Economy,” authored by leading international experts on the Russian economy, concludes that Moscow’s fiscal reserves are largely depleted. This opens the door for decisive action by the West.

“In the early years of the war against Ukraine, the Russian economy proved more resilient than many had expected, but now the reserves are depleted,” says Moritz Schularick, President of the Kiel Institute for the World Economy and co-author of the report’s overview chapter. “The economic fundamentals have weakened significantly. Fiscal reserves are largely depleted, growth has stalled, and dependence on China is becoming increasingly pronounced. At the same time, higher oil prices resulting from the war in the Gulf are likely to have only temporary fiscal effects,” warns Schularick.”

Regarding the development of Russia’s public finances, the “Kiel Report” notes, among other things:

The liquid assets of the Russian sovereign wealth fund have shrunk from 6.5 percent of gross domestic product at the start of the war to just 1.8 percent in April 2026. At the same time, the federal budget deficit exceeded the target set by President Vladimir Putin’s government for the entire year already in the first three months. Furthermore, oil and gas revenues plummeted by 45 percent in the first quarter of this year compared to the same period last year.

IfW President Professor Schularick: “The final stage of Russia’s war economy has begun”; “They simply have no money left”

On the “Politico Berlin Playbook Podcast,” the president of the IfW Kiel, Professor Moritz Schularick, discussed the findings of the Kiel Report in detail with Rixa Fürsen (podcast title: “Russia on the Brink of Collapse”). According to Schularick, the central thesis of the Kiel Report is that “the final stage of Putin’s war economy” has begun. Summarizing his remarks (starting at min. 4):

We base our core thesis—that the final stage of Putin’s war economy

has begun, primarily because he has so far had the ability to finance the war through a national wealth fund, which ultimately holds Russia’s oil and gas revenues from previous years. This fund is now more or less depleted. The deficit budgeted in the Russian national budget for the entire year of 2026 was already exceeded in the first quarter. So, they simply have no money left.

In addition, Russian banks—at the government’s “request”—have extended large-scale loans to the defense sector. Russia’s “implicit” national debt has thus risen to about 50 percent of gross domestic product, while “officially” it stands at just under 20 percent. Slowly but surely, Russia’s national debt is reaching a level at which its own population has, in the past, been reluctant to lend money to the Russian state.

Slowly but surely, the door is closing, and then Putin will have to do some very unpleasant things. He must either say, “We are now making massive cuts elsewhere in the national budget.” The population might go along with that, but it certainly won’t make Putin any more popular.

Or he’ll look for a way out of the war, because he realizes he can’t win this war economically—at least not as long as Europeans stand united behind Ukraine.

Janis Kluge, however, does not currently want to speak of an “economic crisis”

In its press release, as well as in the executive summary by Torbjörn Becker and Moritz Schularick, the IfW sees increasing signs that the Russian economy is “in its final stages.” Many media outlets reported on this, stating that according to the Kiel Report, the Russian economy is on the verge of “collapse.”

In contrast, Janis Kluge, an expert at the Berlin-based “Stiftung Wissenschaft und Politik,” recently stated in an NDR interview that he does not currently want to speak of a “crisis” in the Russian economy, but that the economy is stagnating (minute 3:15). Speaking at the Economic Forum in St. Petersburg, Kluge summarized the development of the Russian economy as follows:

The economy has definitely cooled off over the past one to two years. There was previously a boom driven by defense spending. That boom is no longer there. The economy is now “stagnating.”

And there is a hole in the national budget that is currently growing larger. In this regard, of course, the war in Iran is helping Russia. Energy prices are now so high that Russia has more revenue than last year. But financing the war is becoming more difficult.

It’s also becoming harder to recruit soldiers for this war. And Ukraine is increasingly managing to attack targets in Russia—such as refineries—using long-range drones. If many refineries in Russia are attacked over an extended period, fuel will naturally become scarce, especially gasoline. Gasoline could become scarce again as early as this summer. The public will feel the impact of this, too, because they will then only be allowed to fill up with 10 or 15 liters.

Kluge: There is no compelling reason for the economy to “collapse”

In a concise presentation at Marburg City Hall in May, Janis Kluge, at the invitation of the citizens’ initiative “Zeitenwende Marburg” founded to support Ukraine, commented in detail on the development of the Russian economy: Under the title “War, Oil, and Sanctions – How Strong Is Russia’s Economy Really?”, Kluge primarily analyzed the effectiveness of the sanctions (video).

In this lecture as well, he pointed to the “cooling off” of the economy in Russia. This, he noted, also creates risks. Demand is declining, and the tax base is shrinking. An economic slowdown is generally a process from which a major crisis can emerge. At the same time, however, Kluge emphasized:

“I believe it is very important to note: There is no compelling reason for the Russian economy to collapse at any point.” (Minute 50:40).

Almost all Russians are better off economically today than they were before the war

According to Kluge, despite the strain of the war, Russia’s economic system can continue to function as it does now on a permanent basis. There are examples of countries that spent a significantly higher proportion of their budgets on the military over a much longer period than Russia does currently, such as Israel in the 1990s.

If one were to describe the slowdown in growth in Russia now as a “crisis,” Kluge says one must keep the following in mind:

“Unemployment remains minimal. This is effectively still full employment. And wages have risen very sharply in recent years. This means … the population has benefited greatly in recent years, because almost all Russians are better off economically today than they were before the full-scale invasion began.”

So far, debt is “not a hard limit” on continuing the war

Summarizing the current state of Russian public finances in his lecture (min. 48), Kluge said:

Last year, and even more so this year, there has been a larger deficit in the Russian national budget. Last year, it reached around 4% of gross domestic product in the general government budget. So it is not extremely high, for example compared to the U.S., where it is perhaps closer to 7%.

However, the debt is extremely costly for the Russian state. This is because interest rates are very high. In other words, the Russian state pays significantly more for its debt—which has now grown to around 20% of GDP—than the German government does. So the debt is certainly “an issue,” even if it is still relatively low overall and does not represent a “hard limit” on continuing the war.

Of course, this debt-financed war cannot be sustained indefinitely. It no longer leads to more growth because capacity is fully utilized. There is a widespread labor shortage. The

economy has “overheated” in recent years. Prices have been driven up, leading to inflation.

The growth of the Russian economy is, “in a sense, unhealthy growth.” The central bank was forced to raise interest rates very sharply to slow the economy down again. What we are currently seeing in terms of crisis symptoms—the slowdown in growth—is primarily a consequence of these extremely high interest rates, which are intended to reduce inflation.

Goldman Sachs: Growth to drop to 0.9 percent in 2026 despite higher oil prices

Last week, Clemens Grafe, an analyst at Goldman Sachs, published an overview of current economic developments in Russia. asatunews summarized the report as follows:

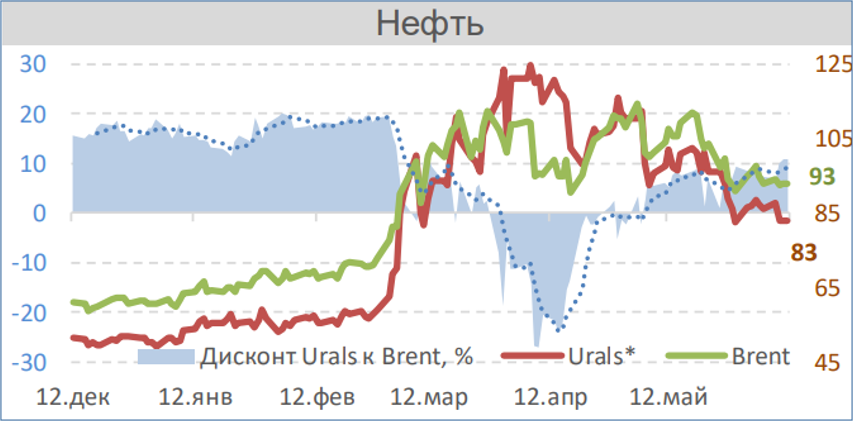

International futures contracts for Brent crude oil were recently trading at around $92 per barrel. This represents an increase of about 30 percent since the start of the war in Iran.

Oil price trends: Brent and Urals crude

in US dollars per barrel (right scale);

difference between Brent price and Urals price (left scale)

VEB Institute: Global Economy and Markets for the period from June 5 to June 11, 2026

Russian government revenues are benefiting massively from this rise in oil prices. Every $10 increase in the price of Russian oil exports generates around $21 billion in additional government revenue.

However, this does not lead to a sustainable economic upswing. According to Clemens Grafe, the Russian economy has little room for faster growth. The available labor force has shrunk by an estimated two million people due to military service and emigration in the wake of the war in Ukraine. According to Grafe, additional liquidity does not lead to the production of more goods or services due to the acute labor shortage and declining productivity.

For the current year 2026, Goldman Sachs expects economic growth in Russia of 0.9 percent, down from 1 percent in 2025.

However, due to rising oil prices, the country’s current account surplus is expected to double from 1.7 percent of gross domestic product in 2025 to 3.2 percent in 2026.

In its “Monthly Oil Market Report,” the Vienna-based OPEC Secretariat maintains its forecast that Russia’s economic growth is likely to accelerate to 1.3 percent in 2026 due to the improvement in the foreign trade situation.

Results of the Central Bank Survey on Inflation, Key Interest Rates, and Growth

The Russian Central Bank conducted another analyst survey approximately two weeks before its next key interest rate decision on June 19 (Survey Calendar). The survey took place from June 5 to 9, coinciding with and shortly following the St. Petersburg International Economic Forum, where President Putin and members of the Russian government commented on the development of the Russian economy.

Results of the Central Bank survey from June 5 to 9, 2026

(results of the April survey in parentheses)

Bank of Russia: Macroeconomic Survey of the Bank of Russia, June 10, 2026 (excerpt)

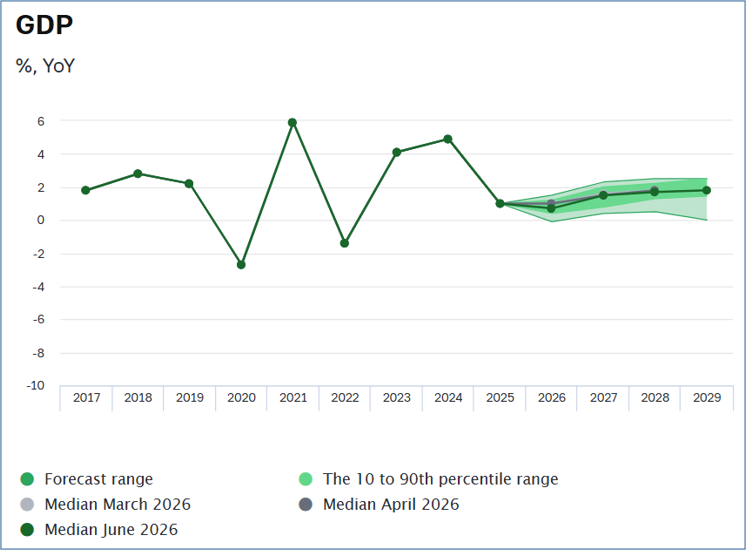

Analysts’ growth forecast for 2026 has dropped significantly

The main change in the Central Bank’s survey is the assessment of this year’s growth in the Russian economy. After the Russian government lowered its growth forecast for 2026 to 0.4 percent, survey participants now also expect lower growth. The median of their forecasts for this year’s increase in real gross domestic product fell from 1.0 to 0.7 percent. For next year, survey participants continue to expect an acceleration in the growth of aggregate economic output to 1.5 percent.

Real Gross Domestic Product

Year-over-year change in percent

Bank of Russia: Macroeconomic Survey of the Bank of Russia, June 10, 2026

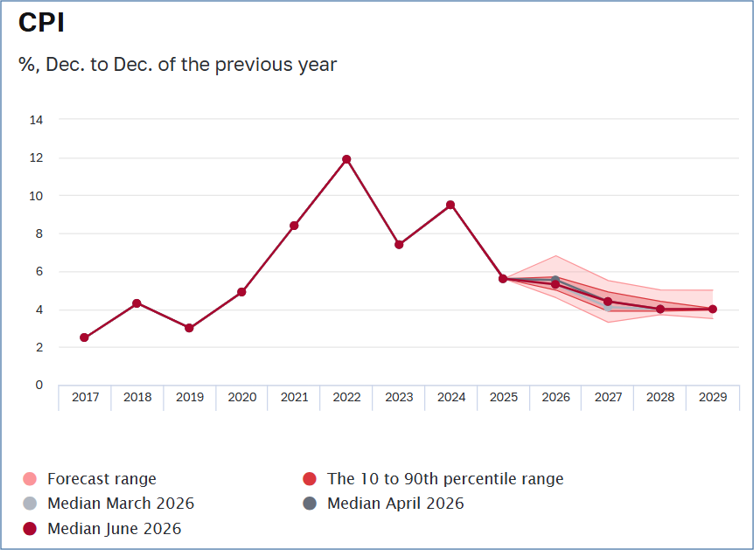

Analysts now expect a slightly faster decline in inflation in 2026

According to analysts’ estimates, the rise in consumer prices will slow from an annual average of 8.7% in 2025 to an annual average of 5.4% in 2026. The expected weaker economic growth could contribute to this. In April, survey participants had still expected a slightly higher annual average inflation rate of 5.6% for 2026.

At the same time, however, their assessment of the key interest rate’s trajectory remained unchanged in the latest survey. They expect the key interest rate to average 14.1 percent for the year, which is about 5 percentage points lower than in 2025.

The following chart from the central bank shows how the inflation rate is expected to develop by year-end according to the analyst survey. The central bank’s target inflation rate of 4.0 percent will not be reached until the end of 2028, based on the average of the survey participants’ estimates (dark red line). According to the survey, consumer prices will still rise by 5.3 percent in December 2026. Even by the end of 2027, the inflation target will not yet be reached, with a price increase of 4.4 percent, according to the survey.

Consumer

Price Index: Year-over-year increase in December

Bank of Russia: Macroeconomic Survey of the Bank of Russia, June 10, 2026

Recommended reading:

German-Russian Chamber of Foreign Trade

analyses, German; also Russian; (selection):

Economic Forecasts: Summer Forecasts from German Institutes

- DIW Berlin: DIW Weekly Report: Energy price shock slows German economy – global economy on a moderate growth path, June 12, 2026

- IWH Halle: Current Economic Outlook: Economy Between Energy Crisis and AI Boom; PDF, June 11, 2026

- IfW Kiel: The Global Economy in Summer 2026, PDF, June 11, 2026

Further Forecasts

- World Bank: Press Release: Middle East Conflict Sends Global Growth to Lowest Rate Since COVID-19; June 11, 2026; Global Economic Prospects Europe and Central Asia, June 2026, June 11, 2026

- Business Insider; Huileng Tan: Russia’s Economy Suffers – Goldman Sachs Delivers a Harsh Verdict. Higher Oil Prices Help Putin – Why Russia’s Economy Still Won’t Recover, June 10, 2026

Reports on the Kiel Report: “Endgame: Russia’s Economy Under Pressure”

- Kiel Institute for the World Economy: Kiel Report No. 9. Endgame: Russia’s Economy Under Pressure; Executive Summary; Torbjörn Becker and Moritz Schularick: Russia’s Economy in Its Final Stages, June 11, 2026

- Politico Europe; Berlin Playbook Podcast; Rixa Fürsen: Interview with Moritz Schularick, President of the Kiel Institute for the World Economy: “Russia on the Brink of Collapse,” 36 min., June 13, 2026

- Münchner Merkur; Fabian Hartmann: “Clear Signs of Structural Exhaustion”: Analysis Sees Russia’s Economy Close to Collapse, June 14, 2026

- web.de; dpa: Economists see Russia’s economy as having reached the “final stage,” June 11, 2026

- Deutsche Welle: War in Ukraine: Economists see Russia’s economy at an end, June 11, 2026;

- Frankfurter Rundschau; Fabian Hartmann: Russia’s economy reaches “final stage”: It’s not just the close ties to China that are to blame, June 13, 2026

Current Economic Developments; Economic Data for April, May, June

- Finmarket.ru: According to the Central Bank, economic activity in Russia increased in April and May; GDP growth in the second quarter will be positive, June 10, 2026

- Joe Blogs Video: Russian war boom comes to an end. The mood at SPIEF 2026 has completely changed. High-ranking bankers, business leaders, and government officials openly discussed slowing growth, declining investment, labor shortages, demographic decline, and the growing risk of economic stagnation; 15 min., June 8, 2026

- Kommersant, Artem Chugunov: The Russian economy is recovering after a weak start to the year, June 8, 2026

Fiscal policy; national budget and oil prices

- Olga Belenkaya, FG Finam: Budget: Signs of stabilization emerged in May, June 8, 2026

- Tass.ru: Ministry of Finance: The budget deficit for the first five months of 2026 amounted to 6.01 trillion rubles; June 25, 2026

- Kommersant interview with Finance Minister Siluanov; Matvey Ivaschenko: Budget, taxes, and oil dependency. Key points from the interview with Anton Siluanov, May 27, 2026; “We must increase our financial safety margin.” Interview on the budget situation, tax administration, “cleaning up the economy,” and the prospects for IPOs of state-owned enterprises, May 27, 2026.

- New Eurasian Strategies Centre; Sergey Aleksaschenko: The Kremlin is bleeding money – but not running dry, May 14, 2026

- bne IntelliNews: Russian budget deficit jumps to 55% of annual target in 4M26, May 12, 2026

Monetary Policy: Economy Ahead of the Next Key Interest Rate Decision on June 19

- 1Prime.ru: The Central Bank reported growth in Russian GDP in the first quarter of the year. Deputy Central Bank Head Zabotkin: Russia’s GDP grew moderately in the first quarter, June 11, 2026

- Russia.capital: Russia’s economy hopes for lower interest rates – Central Bank remains cautious, June 7, 2026

Foreign Trade

- Deutsche Welle; Arthur Sullivan: Could Russia save the global economy? Global energy markets are still grappling with the price and supply shock caused by the war in Iran. Could Russia solve the problem? Business Beyond takes a closer look at US plans to bring Moscow back into the frame; Video, Interviews with Craig Kennedy, Elina Ribakova, Janis Kluge; 20 min., 06/08/26

- russland.capital: Moscow is once again courting Western companies—on Russian terms, 06/07/26

- MMI Russian Macro: OIL AND GAS REVENUES: Moderate growth despite such high prices; The reason appears to lie in physical export restrictions, 06/03/26