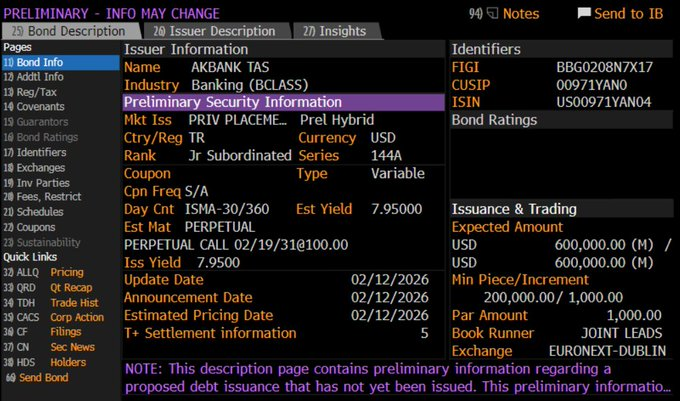

Akbank Sets Record with AT1 Bond

Akbank, which is listed on the Istanbul Stock Exchange, has set new standards with the issuance of a subordinated Additional Tier 1 (AT1) bond. On February 13, the bank issued a bond with a volume of 600 million U.S. dollars and a coupon rate of 7.95 percent—marking the first time it has fallen below the 8 percent threshold.

AT1 bonds are perpetual, subordinated instruments that can be used to strengthen equity capital in the event of a crisis. Akbank’s bond is callable after 5.5 years. Turkish banks typically exercise a call option after five years. For regulatory purposes, a ten-year maturity is reported.

The issuance was underwritten by Citigroup, Emirates NBD, First Abu Dhabi Bank, HSBC, JPMorgan, and Merrill Lynch. Fitch rates Akbank at BB-/Positive, and Moody’s at Ba3/Stable.

More Affordable Than Ever Before

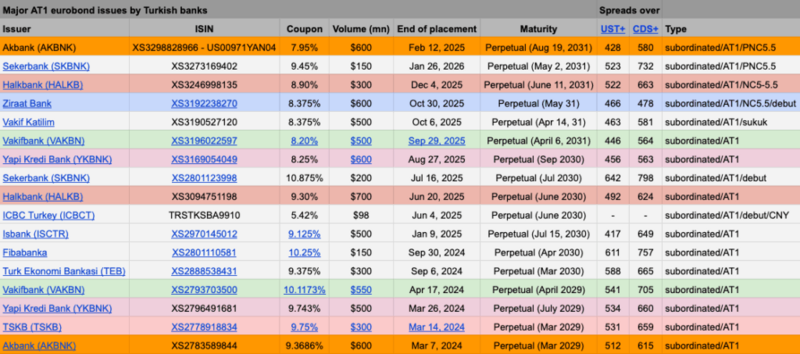

With a coupon of 7.95 percent, the bond is considered the most affordable AT1 issuance by a Turkish bank to date. As recently as August, Yapi Kredi had offered 8.25 percent; in October, Vakifbank undercut that rate with 8.20 percent. Akbank is now setting a new record—while also significantly improving its own terms: In March 2024, the bank had to pay 9.37 percent for a comparable bond.

Table: Key AT1 securities sold by Turkish banks.

The issuance is taking place in an environment where Turkey’s credit default swaps (CDS) continue to trade above 200 basis points, while the yield on ten-year Turkish government bonds denominated in euros is below seven percent.

Revival of the covered bond market

At the same time, Akbank announced the sale of a five-year, mortgage-backed covered bond with a volume equivalent to 100 million U.S. dollars to the International Finance Corporation (IFC). This marks the IFC’s first investment in a Turkish covered bond since 2017. As early as June 2025, the European Bank for Reconstruction and Development (EBRD) had already contributed to the revival of this market segment by purchasing a $100 million bond from Akbank.

Momentum is also evident at the broader level. According to Fitch Ratings, the total volume of outstanding debt securities issued by Turkish issuers is expected to exceed the 540 billion US dollar mark in 2026. At the end of 2025, it stood at $503 billion—a 14 percent increase over the course of the year. New issuances climbed 12 percent to $140 billion.

In 2025, Turkey was the fourth-largest issuer of U.S. dollar-denominated emerging market bonds, excluding China. At the same time, the sukuk market is gaining importance: Issuances rose by 54 percent to $18 billion and now account for 13 percent of the total volume.

Despite this momentum, the market remains vulnerable to interest rate and currency fluctuations, geopolitical risks, and persistently high inflation. The share of foreign investors in domestic government bonds fell to 7.6 percent by the end of 2025.

This article was produced in cooperation with our partner bne intelliNews