Unexpectedly weak start for the Russian economy

Author: Klaus Dormann

Last week, the Federal State Statistics Service (Rosstat) released additional economic data for the month of January. A year-over-year comparison with January 2025 reveals an unexpectedly sharp decline in Russian economic output. The Ministry of Economic Development estimated that Russia’s real gross domestic product in January was 2.1% lower than in January 2025.

A certain slowdown in economic activity at the beginning of 2026 had indeed been expected. The Russian Central Bank anticipated that the upcoming 2026 VAT hike and the announced increase in the recycling fee for car purchases would only temporarily boost demand through the end of 2025. In contrast to this “growth spurt” at the end of the year, the Central Bank anticipated a decline in consumption growth at the start of 2026.

However, some of the economic data for January turned out to be significantly worse than expected. For example, an Interfax survey of analysts had predicted a 0.9 percent increase in industrial production for January. In fact, however, industrial production fell by 0.8% year-over-year in January. And real retail sales rose by only 0.7% in January, far less than analysts had anticipated (+1.9%). This is reported by Olga Belenkaya, chief economist at the brokerage firm FINAM, in a detailed analysis of the Russian economy’s “weak start” to 2026.

The state of the Russian economy at the turn of 2025/2026

In the Moscow-based business magazine Profile.ru, senior correspondent Vladislav Grinkevich summarized the current “problematic situation” of the Russian economy in early March as follows:

“In fact, the Russian economy faces numerous problems: growth is slowing, inflation remains high, the industrial sector is in decline, and the labor market is tight. Nevertheless, most experts agree that there is absolutely no question of a crisis, let alone a collapse of the Russian economy. However, one must acknowledge that this year will be the most difficult since 2022.”

Grinkevich points in particular to the rising federal budget deficit and the decline in production in many industrial sectors outside the defense sector.

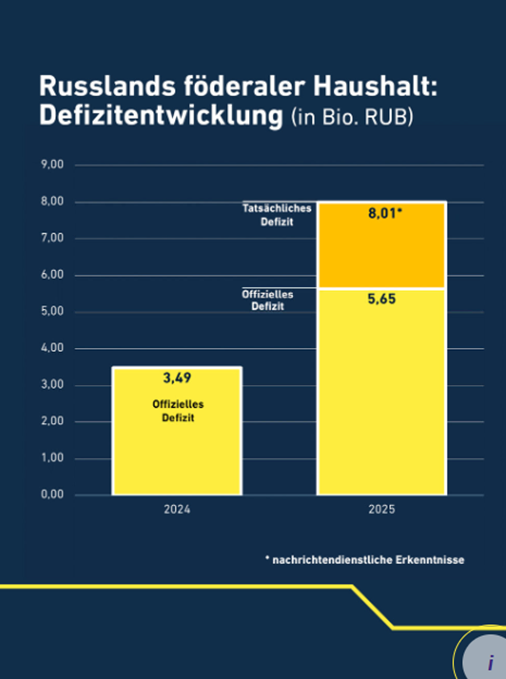

Russia’s federal budget deficit has risen significantly in 2025

According to Grinkevich, the budget deficit had already risen to 2.6 percent of GDP by 2025, even though a reduction to 0.5 percent of GDP had originally been planned.

According to “intelligence findings” from the German Federal Intelligence Service (BND), the deficit actually rose to 3.7 percent of GDP at 8.0 trillion rubles (Die Welt, ZDF). The BND reports that the deficit was thus approximately 42 percent higher than the government had stated.

BND illustration:

Rise in the Russian federal budget deficit

Federal Intelligence Service, BND: Russian Economy in the Red: Sanctions Take Effect, Deficit Rises Significantly, Investment Location Becomes an Unpredictable Risk, 03/04/26

Grinkevich: The decline in oil and gas revenues is manageable

According to Grinkevich, the main cause of the deficit increase in 2025 was the 24 percent decline in government revenues from the oil and gas sector due to low world market prices. Forecasts by the Finland-based independent “Centre for Research on Energy and Clean Air” (CREA) projected a further 27 percent decline in oil and gas revenues in 2026.

Grinkevich emphasizes, however, that this decline is “no cause for panic.” According to Sergei Khestanov (Associate Professor at the Russian Presidential Academy of the National Economy and Public Administration, RANEPA), the Russian government has reserves to cover the budget deficit. The liquid portion of the National Welfare Fund still amounts to about 4 trillion rubles. The potential for issuing government bonds amounts to an additional 3 to 3.5 trillion rubles.

According to “Die Welt,” analysts within the German federal government also do not expect Russia to have to end the war in Ukraine in the short term for financial reasons. Recently, the head of Finnish military intelligence, Pekka Turunen, told WELT that from a financial perspective, Russia could “continue the war at least this year and perhaps next year as well.”

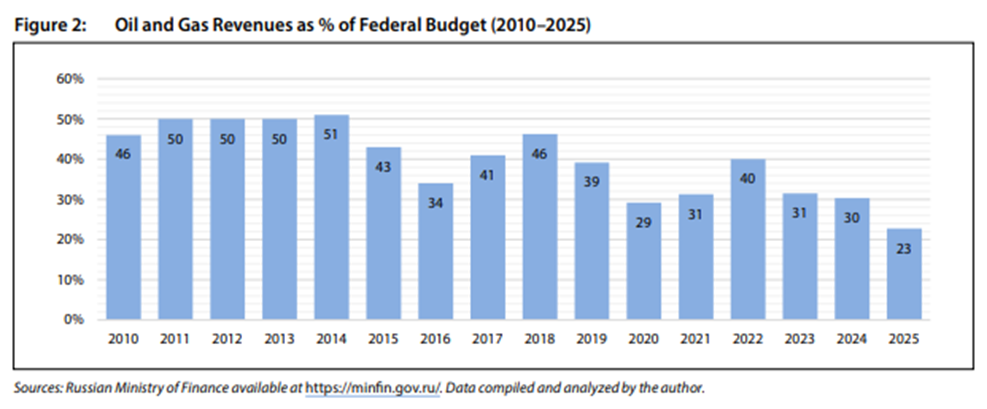

Since 2018, the share of revenue from the oil and gas sector in the federal budget’s total revenue has already halved. According to Tatiana Mitrova (Global Fellow at the Center on Global Energy Policy, Columbia University), it fell from 46 percent in 2018 to 23 percent in 2025.

Tatiana Mitrova (Columbia University): Russian Oil under Pressure: Adaptation, Fiscal Reconfiguration, and Domestic Constraints; in: RUSSIAN ANALYTICAL DIGEST No. 335, 02/18/26

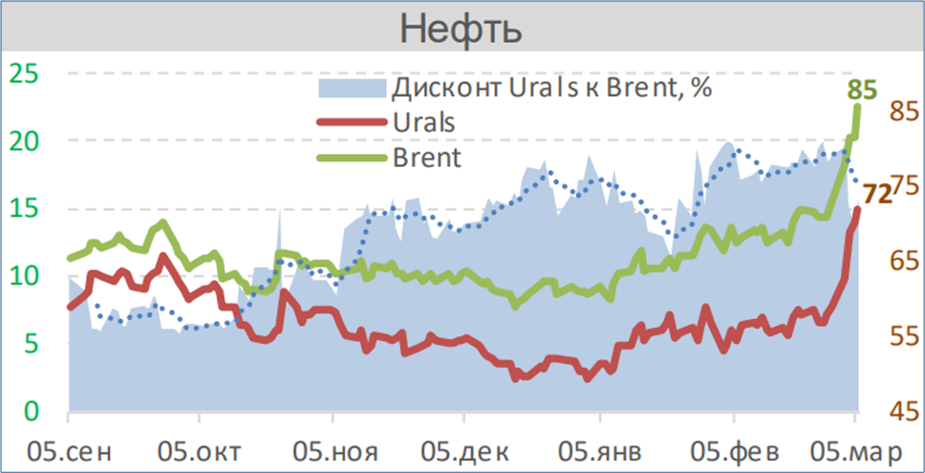

Can the rise in oil prices help Russia with budget financing?

As a result of the war in the Middle East, oil prices have risen sharply. The following chart from the weekly report published on Friday by the Institute of the Russian state development corporation VEB.RF shows: The price of Brent crude rose to around $85 per barrel on March 5. Russian Urals crude was trading at around $72 per barrel. The “discount” of Urals crude relative to Brent was thus around 16 percent (gray area, left scale in the following figure).

Oil Prices: Urals and Brent in US$/barrel; Urals discount in %

VEB Institute: Global Economic and Market Outlook, March 6, 2026

Alexander Kolyandr, a senior fellow at the “Democratic Resilience Program” at the “Center for European Policy Analysis (CEPA),” argues, however, according to the headline of his CEPA article, that the war in Iran will not save Russia’s “ailing economy.” Russia is in serious trouble due to its growing budget deficit.

The conclusion of his article: While the war’s impact on oil prices could help Russia, unless oil prices remain at high levels in the long term and the ruble does not depreciate significantly, the budget problems would likely persist for a long time.

According to Kolyandr, the Russian government now appears ready to acknowledge its budget problems. Apparently, experts have succeeded in persuading President Putin to impose spending cuts. This would slow down the main driver of economic growth over the past three years. Since cuts in military spending are practically impossible, the already stagnating civilian sectors of the economy would be disproportionately burdened by the spending cuts.

Production in the “civilian” sectors of industry is stagnating or declining

Vladislav Grinkevich also sees the development of Russian industry as divided into two blocks: The first block, the defense industry, is prioritized by the state and is growing. Production in the second “civilian” block of industry, however, is stagnating or even declining.

According to Grinkevich’s assessment, the focus of public spending will remain on financing the “security forces” “in the near future” as well. According to the 2026 budget plan, spending on “National Defense” and “National Security” will amount to 12.1 trillion rubles and 3.8 trillion rubles, respectively—a combined total of nearly 16 trillion rubles. By comparison, spending on the civilian sector “National Economy” will amount to 4.8 trillion rubles.

How the government explains the GDP decline in January 2026

To explain the 2.1 percent decline in aggregate economic output in January 2026 compared to January 2025, the Ministry of Economic Development pointed to the high base of comparison from January of the previous year. In January 2025, real GDP rose sharply by 2.9% compared to the same month of the previous year.

In January 2026, there were only 15 working days—two fewer than in January 2025, which had 17 working days.

Another reason was this year’s significantly colder weather compared to January 2025. Due to weather conditions, construction output in January 2026 was 16 percent lower than a year ago.

The CSR Institute estimates the calendar-adjusted GDP decline at 0.8 percent

Taking into account that there were two more working days in January a year ago, GDP in January 2026 "calendar-adjusted" by only 0.8 percent compared to the same month a year ago, according to initial calculations by Daniil Nametkin, director of the Center for Investment Analysis and Macroeconomic Research (CSR) (press release; Public News Service OSN). Nametkin emphasized that the current decline in GDP in January is not a long-term trend. Future developments will depend largely on the monetary policy of the Russian Central Bank. Should the key interest rate be lowered further, a recovery in business activity and investment growth across a number of sectors is expected.

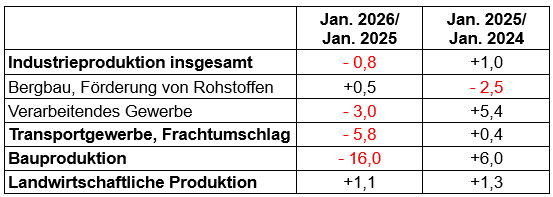

Here is how production in the “core sectors” developed in January

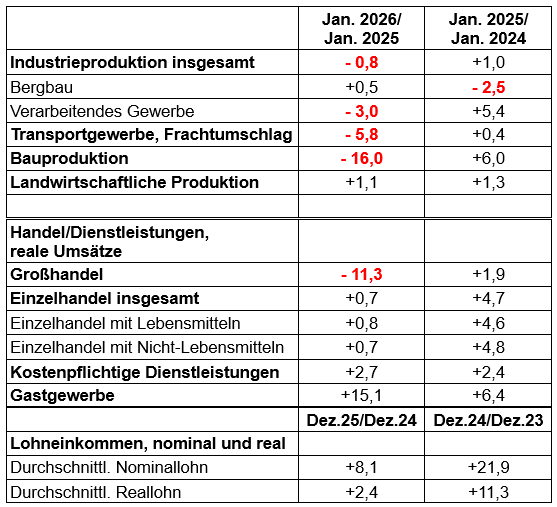

The index of goods and services production in the so-called “core sectors” of the Russian economy fell by 3.2% year-over-year in January.

Declines in production compared to January 2025 were recorded in: manufacturing (-0.8%), construction (-16%), wholesale trade (-11.3%), and freight transport (-5.8%).

Regarding the 0.8% decline in industrial production, Kommersant editor Artem Chugunov drew the following conclusion:

“Although the ministry attributes the decline to calendar effects, analyst estimates and data from business surveys point to a continuing trend: the civilian industrial sector is stagnating, and production growth has returned to zero or even turned negative following a sharp rise in December.”

Real retail sales growth slowed to 0.7% year-over-year in January. At the same time, sales of services to the public continued to grow by 2.7%. The increase in sales in the hospitality sector even accelerated to 15.1% (despite press reports of restaurant closures).

Economic indicators at the start of 2026

Year-over-year changes in %

Finam.ru; Olga Belenkaya: January 2026 Results – A Weak Start to the Year, 03/05/26

Wages rose significantly more slowly in December

Wage growth slowed significantly in both nominal and real terms in December (Rosstat has not yet published data for January). Olga Belenkaya sees this as another sign of easing in the labor market amid the ongoing economic slowdown. Wage growth is thus approaching the rate of labor productivity growth. According to the Central Bank, this is an important prerequisite for reducing persistent inflationary pressures.

In nominal terms, wage growth slowed to +8.1% year-over-year in December (down from +12.8% in November). In real terms, wage growth fell to +2.4% (after +5.8% in November). However, when considering this sharp slowdown in wage growth in December, it must be noted that wages rose very sharply a year earlier in December 2024, as the payment of annual bonuses was brought forward to December 2024 ahead of the implementation of a steeper income tax progression. In December 2024, wages thus rose by 21.9% in nominal terms and by 11.3% in real terms compared to the previous year.

Industrial production in January was 0.8 percent lower than a year ago

For the first time since February 2025, industrial production fell again in January 2026 compared to the previous year. After having risen sharply in December (+3.7% year-on-year), it was 0.8% lower in January than a year ago (Finmarket.ru). Industry contributed to Russia’s annual real GDP growth of 1.0% last year with a 1.3% increase in production in 2025.

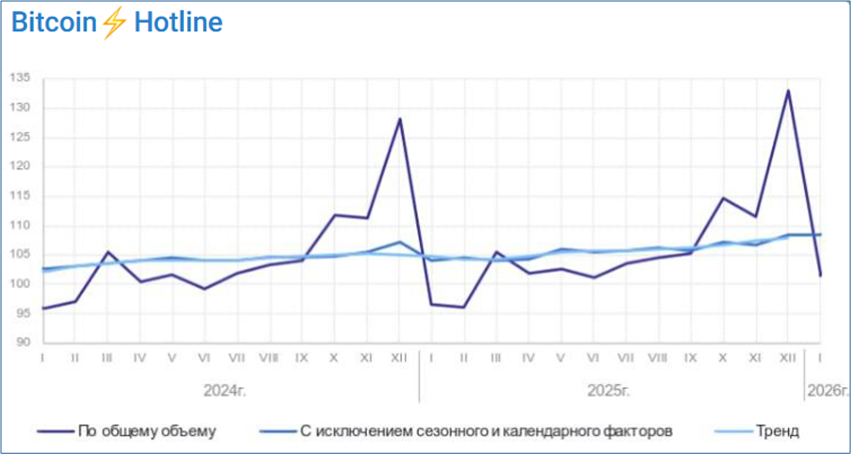

In January 2026, according to a preliminary estimate by the Federal State Statistics Service (Rosstat), seasonally and calendar-adjusted industrial production stagnated at the level reached in December 2025. Evgeny Kogan’s Bitcoin Hotline published the following copy of a Rosstat chart on this topic. The stagnation of the seasonally and calendar-adjusted industrial production index is shown by the gray line, which is partially overlapped by the light blue trend line calculated by Rosstat.

Industrial production indices according to Rosstat

dark blue line: unadjusted; gray line: seasonally and calendar-adjusted; light blue line: trend

Source: Evgeny Kogan: Russian industry stagnates after a turbulent December; 02/27/26

Manufacturing output was 3 percent lower in January

The 0.8 percent year-over-year decline in total industrial production in January 2026 was primarily due to a 3.0 percent drop in manufacturing output.

In contrast, production in mining and raw materials extraction was 0.5% higher in January than a year ago. According to Interfax estimates, natural gas production rose by 6.5% year-over-year in January (the highest increase in the last four years), attributable to cold weather. Coal production, however, fell by 6.6%.

Among the few “growth drivers” in the manufacturing sector in January were two sectors of the defense industry: Production of “other transport vehicles and equipment (including aircraft manufacturing, shipbuilding, etc.)” rose by nearly a quarter (+24.5%). Production of computers, electronic, and optical products grew by nearly one-tenth (+9.8%). The manufacture of metal products, however, recorded a 6% year-over-year decline.

Automotive production continued to decline sharply in January (-21.3% year-over-year) following a 20.2% drop in December. Passenger car production fell by 13% year-over-year in January, while truck production dropped by nearly 36%.

Finam.ru; Olga Belenkaya: January 2026 Results – A Weak Start to the Year, 03/05/26

Freight turnover in the transport sector fell by 5.8% year-over-year in January (the sharpest decline since October 2022), following a 1.3% decline in December. Construction output was 16% lower—due to weather conditions—while agricultural output rose (+1.1%).

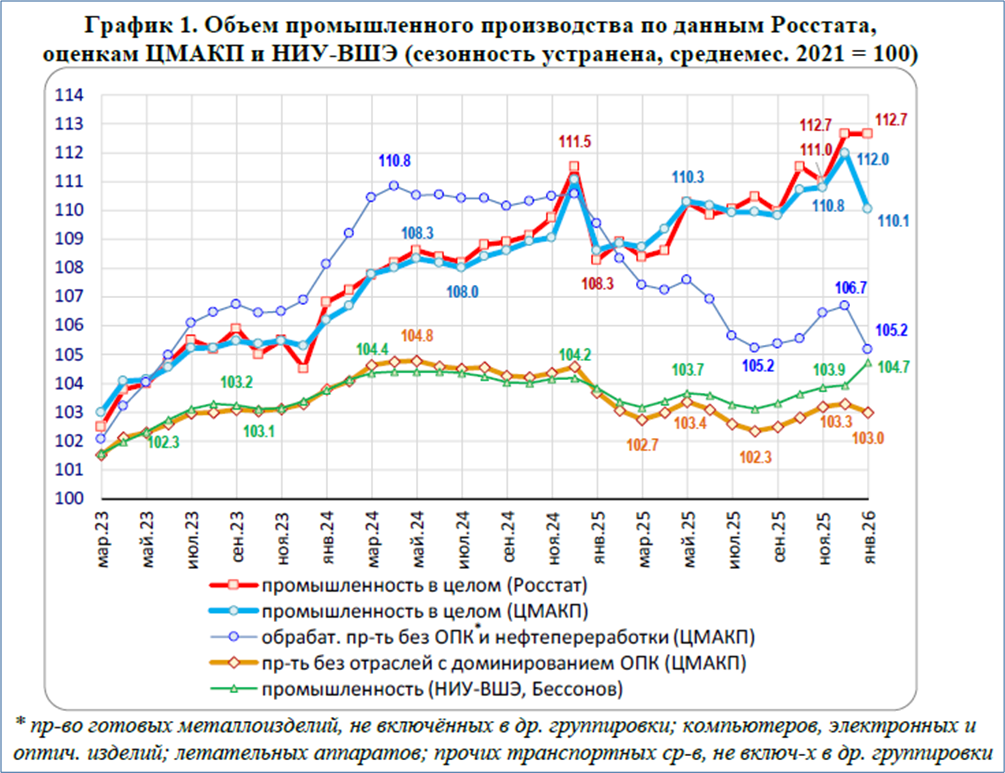

Highly conflicting estimates regarding seasonally and calendar-adjusted trends

While according to initial Rosstat estimates, seasonally and calendar-adjusted industrial production in January 2026 stagnated at the December 2025 level, other estimates yielded significantly different results. The Moscow-based “Center for Macroeconomic Analysis and Short-Term Forecasting” (CMASF) has compared its own estimates with Rosstat’s estimates and those of the Moscow “Higher School of Economics” (HSE) in the following figure.

The upper red line shows that, according to Rosstat, industrial production stagnated in January at an adjusted index level of 112.7.

The CMASF estimates, shown by the light blue line, had previously deviated only slightly from Rosstat’s estimates. In January, however, industrial production fell by 1.7% month-over-month according to the CMASF.

According to the HSE Center for Economic Research (green line), however, production rose by 0.8% compared to December.

Industrial production according to Rosstat, CMASF, and HSE estimates

(seasonally adjusted, monthly average 2021 = 100)

* Manufacture of metal products not classified elsewhere; computers, electronic, and optical products; aerospace industry; other transport vehicles not classified elsewhere

The dark blue line shows CMASF estimates of how production in the “manufacturing sector” is developing, excluding production in the defense industry and petroleum refineries. It fell sharply over the course of 2025 and reached a new low in January 2026.

The lower brown line shows CMASF estimates of how total industrial production would have developed without sectors dominated by the defense industry.

Academic Director of the HSE: “We need to wait for the quarterly results”

Georgy Ostapkovich, Academic Director of the Center for Market Research at the Higher School of Economics, told the Moscow business portal globalmsk.ru regarding the economic data for January released so far that while there has been a significant decline in the manufacturing sector—the main driver of GDP growth, accounting for over 30% of GDP— However, he said it was still too early to draw conclusions:

“One must bear in mind that this data comes from the Ministry of Economic Development and Trade. This agency performs all calculations using its own methods. …

January has always been an unsuitable month for accurate economic analysis, so we’ll have to wait for the April data when Rosstat compiles the quarterly results.”

Recommended reading:

- German-Russian Chamber of Foreign Trade:

Focus analyses, German; also Russian; (Selection):

Economic Consequences of the Iran War: Oil Prices, Russia, Tourism; 03/02/26 Weak Growth, Dwindling Reserves, and High Military Spending; 02/18/26 - Podcast “Tsars, Data, Facts” by the German-Russian Chamber of Foreign Trade, hosted by Thomas Baier:

Low gas storage levels: Europe’s challenge in the energy market; Guest: Dr. Heiko Lohmann, “energate Gasmarkt”; 34 min., 03/01/26

From Boom to Stagnation: Russia’s Economy in 2026; Guest: Vasily Astrov, 36 min., 02/17/26; - globalmsk.ru: Russia’s GDP slipped into negative territory in January, March 6, 2026

- SberCIB Investment Research: Oil Market: The Impact of the Middle East Conflict and the Blockade of the Strait of Hormuz on Global Oil Prices and Russia, 03/06/26

- Joe Blogs video: Russia crippled. Russia’s oil industry is facing a growing list of problems — and rising global oil prices may not be enough to solve them, 10 min., 03/05/26

- CEPA; Alexander Kolyandr: Iran War Won’t Save Putin’s Crumbling Economy. Russia is in serious trouble due to a ballooning budget deficit. Rising oil prices are unlikely to change the math, 03/04/26

- nv.ua: Pro-Kremlin economists warn Russia’s economy shows signs of stagflation, March 4, 2026

- Politcom.ru; Marina Voitenko: February 2026: Leading Indicators and Forecasts, 06/03/26

- VEB Institute: GDP Index December 2025. 03/03/26

- GIS Report; Carole Nakhle: Shadow fleet keeps Russia’s oil exports beyond Western reach, March 2, 2026

- FinanceRambler: Oil and gas prices rise due to the war in the Middle East: What does this mean for Russia and the ruble? 03/02/26

- Profile.ru; Vladislav Grinkevich: Hold Your Breath: The Russian Economy Will Have to Survive the Next Year on Old Reserves, 03/01/26

- MaresMedia.se; Alexander Dionisius: Russia’s economy is eating itself alive – Putin’s war is destroying the future, 02/25/26

Economic data and forecasts:

- Public News Service — OSN, Tatyana Ponomareva: Economist Nametki, director of the Center for Investment Analysis and Macroeconomic Research (CSR), cites the reasons for the 2.1% decline in GDP, 03/05/26

- Elitetrader.ru; Promsvyazbank The Russian Ministry of Economic Development estimated the decline in real GDP in January at 2.1% year-over-year, March 5, 2026

- Finam.ru; Olga Belenkaya: January 2026 Results – A Weak Start to the Year, 03/05/26

- Kommersant, Artem Chugunov: Private demand remains. The economic slowdown is only now reaching the labor market, 03/05/26

- Hard Numbers: Table: Development of Key Economic Indicators May 25 to Jan. 26; 03/04/26

Purchasing Managers’ Indexes February 2026:

- bne IntelliNews: Russia’s service sector PMI loses momentum in February, dropping to 51.3; March 4, 2026

- bne IntelliNews: Russia’s manufacturing PMI downturn eases to 49.5 but confidence remains fragile, March 3, 2026

Gross Domestic Product in January 2026:

- Finmarket.ru: Russia’s GDP fell by 2.1% year-on-year in January, 03/04/26

- Vedomosti: The Ministry estimated a 2.1% decline in GDP for January, 03/04/26

Additional economic data for January 2026:

- Finmarket.ru: Output from core activities in Russia fell by 3.2% in January, March 4, 2026

- Finmarket.ru: Retail sales growth slowed to 0.7% in January, 03/04/26

- Finmarket.ru: Real wages in Russia rose by 4.4% through 2025, March 4, 2026

- Finmarket.ru: The unemployment rate in Russia remained at 2.2% in January, 03/04/26

- Bitcoin Hotline: The Russian labor market remains overheated, 03/04/26.

- Monocle.ru: Fourth-quarter GDP growth is most likely a statistical artifact, March 2, 2026

- Reuters; Gleb Stolyarov: Russian rail freight decline deepens in February as economy slows, 03/02/26

- Handelsblatt; Jan Wöller: Ranking. The world’s ten largest economies, March 2, 2026

Industrial production in January 2026:

- CMASF: Industrial production trends in January 2025, 03/05/26

- Kommersant; Artem Chugunov: The industrial sector started the year with a decline. The sector’s performance fell short of analysts’ expectations; 03/02/26

- Finmarket.ru: Industrial production in Russia fell by 0.8% in January; 02/27/26

- Russland.capital.de: Russian industrial production fell in January 2026 for the first time since February 2025, March 3, 2026

- Raiffeisenbank; Focus-Pocus: Industry in January: Stagnation following a strong December upturn, 03/02/26

- RBC.ru: Rosstat reported a decline in industrial production in January, 02/27/26

- Evgeny Kogan: Russian industry stagnates after a turbulent December; Rosstat; 02/27/26

- Hard Numbers: Industrial Production: It’s Not All That Simple, 02/27/26

- Kyiv School of Economics: Russia Chart Book February 2026, 02/27/26

- CMASF, Moscow: Base version of the macroeconomic forecast for 2026–2029, 02/27/26

- CMASF, Moscow: “Analysis of Macroeconomic Trends,” 02/27/26

- SberCIB Investment Research: Inflation in Russia in 2026: Price trends since the start of the year and forecasts by analysts, the Central Bank, and the Ministry of Economic Development, 02/27/26 2026Interfax.ru: Inflation in Russia stood at 0.19% from February 17 to 24, slowing to 5.8% year-over-year; February 27, 2026

- Interfax-Russia.ru: A key interest rate of 15.5% amid a noticeable slowdown in inflation still constitutes a restrictive monetary policy that curtails lending, according to the Central Bank. 02/27/26

- Reuters; Elena Fabrichnaya and Gleb Bryanski: Russian ruble expected to fall sharply this year as oil sales decline and the deficit rises, 02/26/26