“Tough times for the Russian economy”

Author: Klaus Dormann

This is the title of a blog post by Laura Solanko, Senior Adviser at the BOFIT research institute of the Bank of Finland, published on January 22, discussing the impact of the war in Ukraine on the Russian economy.

Solanko notes that while the Russian economy grew “quite rapidly” in 2023 and 2024 due to the massive increase in government spending caused by the war (2023: +4.1%; 2024: +4.3%), it reached its growth limits in 2025. The rise in output is now limited to annual rates close to the Russian economy’s long-term growth potential of around one percent. In the “BOFIT Forecast for Russia” published at the end of March 2025, the “Bank of Finland Institute for Emerging Economies” had already estimated growth in the Russian economy for 2026 and 2027 at just 1.0 percent.

According to Solanko’s assessment, the war has exhausted Russia’s financial and human production capacities. Russia no longer has sufficient financial resources in its “war chest.” Labor is scarcer than ever before. The sanctions imposed on Russia have “worked.”

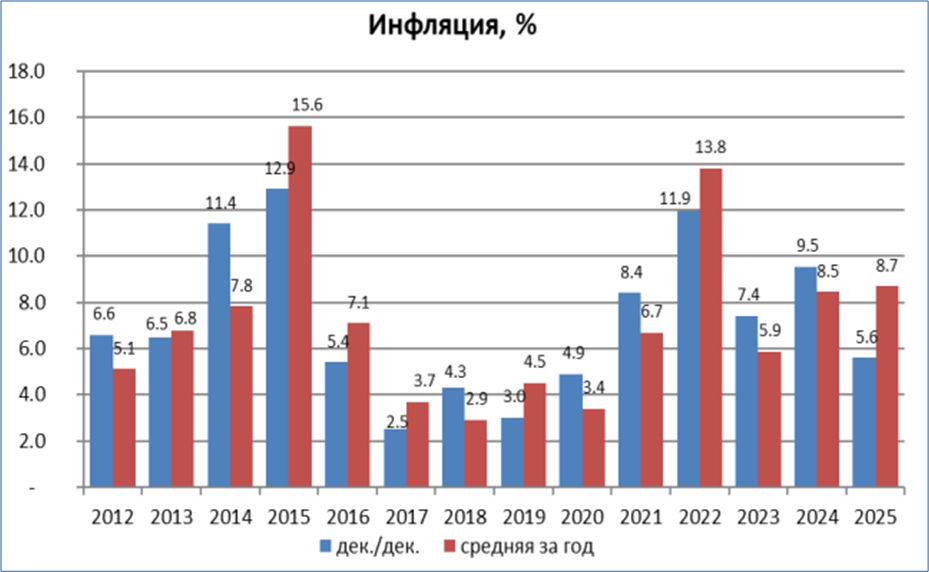

Solanko does not address the development of inflation in Russia in her commentary. The Russian statistics agency Rosstat reported on the development of consumer prices in December and for the full year 2025 on January 16. Press reports on the subject often gave the impression that the annual increase in consumer prices in 2025 was significantly lower than in 2024 (for example, by the French news agency AFP). In fact, however, the year-over-year inflation rate for 2025/2024, at 8.7 percent, was still slightly higher than the year-over-year rate for 2024/2023, which stood at 8.5 percent (see the end of this article for further details).

Sharp Rise in Russia’s Military Spending

A key focus of Laura Solanko’s commentary on the development of the Russian economy is the evolution of the federal budget and military spending.

The following Statista chart illustrates how sharply Russia’s military spending has already risen by 2024. The blue bars show that the share of Russian military spending in gross domestic product has risen from 3.6 percent in 2021 to 7.1 percent by 2024 (see Ostwirtschaft from Dec. 1, 2025: “Is Russia a War Economy?”).

Statista; J. Rudnicka: Russia’s Military Spending by 2024, Nov. 26, 2025;

“Stockholm International Peace Research Institute”: SIPRI Fact Sheet, April 2025

Laura Solanko also refers to the rise in Russian military spending, citing publications by Julian Cooper at the “Stockholm International Peace Research Institute” (SIPRI). Below is a summary of Solanko’s assessments regarding the development of military spending and its impact on Russia’s public finances.

Military spending could reach nearly 10 percent by 2025

According to Solanko, the Russian government has roughly doubled its spending on “defense” and “internal security” over the past four years: In 2021, the year before the war began, Russia’s military spending amounted to 3.6% of gross domestic product. The 2025 budget allocates 7.2% of GDP to war-related expenditures.

Furthermore, Russia’s war efforts are financed not only from the defense budget but also through funds from other budget areas such as education, social services, and the maintenance and construction of civilian infrastructure. Total military spending could amount to nearly 10% of GDP, Solanko estimates.

The Russian government also supports the defense industry by providing loan guarantees. Other sectors, however, have difficulty obtaining loans and are burdened with high debt service costs. Incentives for market-oriented investment in civilian production are therefore “minimal at best” in Russia.

The planned reduction in defense spending in 2026 is unlikely

Russia’s budget plan for 2026 does indeed call for a nominal reduction in defense spending. However, according to Solanko, this is “unlikely” as long as Russia does not end its war very soon.

Solanko expects that the deficit in the Russian federal budget will not decrease in 2026. It will likely be on par with the previous year’s and reach around 3% of GDP. The plan is for federal budget spending to rise by only 4% in nominal terms in 2026. This would represent a real decline. At the same time, federal budget revenues are projected to grow nominally by nearly 9 percent—more than double the rate of spending. Solanko considers this “quite optimistic.”

According to Solanko, Russia must finance its rapidly rising government spending through standard international measures, namely tax hikes, higher levies on state-owned enterprises, and increased government borrowing in the bond markets. If necessary, certain public expenditures could be cut.

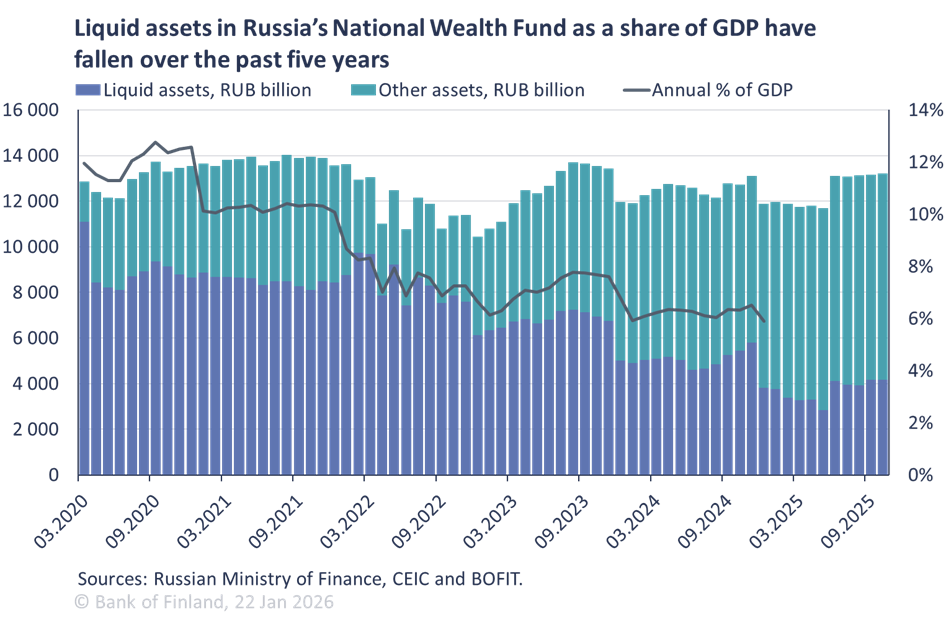

The liquid portion of the “National Welfare Fund” has fallen sharply

Laura Solanko points out that, like many other oil-producing countries, Russia established a sovereign wealth fund to invest revenues from hydrocarbon production, known as the “National Welfare Fund” (Ministry of Finance, Wikipedia).

The following BOFIT chart from Solanko’s blog post shows how the fund’s value in rubles evolved from March 2020 to October 2025 (left scale). The decline in the fund’s value by about a quarter during the first year of the war in 2022 had already been recouped by the fall of 2023. Since mid-2025, the fund’s total value has once again been slightly higher than in March 2020.

However, the trend shown by the blue bars in the figure indicates that the value of the fund’s “liquid assets” has fallen sharply since 2022. In 2024 and 2025, a large portion of the fund’s readily available assets was used to cover budget deficits.

The green bars show the “other investments” of the “National Welfare Fund,” which are primarily invested in Russian companies and banks on a long-term basis.

Russia’s National Welfare

Fund: Development of the value of liquid assets and other investments in billions of rubles; black line: value of the fund relative to gross domestic product in percent

Laura Solanko; BOFIT, Bank of Finland; Blog: Rough times for the Russian economy, Jan. 22, 2026

Relative to the value of Russia’s gross domestic product, the value of the fund has halved from around 12 percent in December 2020 to around 6 percent in December 2024. This is shown by the black line in the figure (right scale).

Laura Solanko notes: Although Russia is one of the world’s leading oil exporters, its sovereign wealth fund is relatively small compared to those of other oil-producing countries. The value of the Saudi pension fund corresponds to about 85% of the country’s annual gross domestic product. The Norwegian sovereign wealth fund even amounts to around 400% of Norway’s gross domestic product.

The labor market is tighter than ever before

Laura Solanko also points to the further labor shortage in Russia caused by the war in Ukraine:

According to estimates, the war has reduced the available labor force by about 1.5 million people. Russia’s unemployment rate was already low before the war. Due to conscription for the war in Ukraine, the deaths and injuries of soldiers, as well as the decline in immigration to Russia, the labor market is tighter than ever before.

To sustain the war effort, the government must send approximately 30,000 men to the front each month. Following the partial mobilization of reservists in the fall of 2022, these were mostly individuals lured by high bonuses or prisoners who were offered release from prison if they performed military service.

“The sanctions have worked”: They are weighing on businesses and consumers and have isolated Russia more than ever

Laura Solanko considers the sanctions imposed on Russia in the financial markets to be “extremely effective.” She says:

“Although the sanctions were not consistently enforced at the international level, the measures focused on the financial markets were extremely effective, as they cut Russia off from the international market. Both the Russian government and Russia’s largest corporations were forced to finance their business operations out of their own pockets or through loans from domestic lenders. Borrowing from domestic lenders is more expensive than financing on international markets.”

Solanko also points out that the sanctions have forced Russia to lower the prices of its key export products.

“The clearest example is the export price for crude oil. Even with the shadow fleet and various strategies to circumvent the sanctions, Russia’s main export grade, Urals, was sold in 2024/25 at a discount of $14 per barrel compared to the benchmark price for Brent crude. Before the invasion of Ukraine in 2022, the price difference between Urals and Brent was typically only $1 to $2 per barrel. The sanctions imposed at the end of 2025 drove the price difference between Brent and Urals to over $20 per barrel. The current average price for Urals (below $40 per barrel) is expected to increase the budget deficit by about 1.5% of GDP.”

Regarding the effectiveness of sanctions on imports to Russia, Solanko states:

“Russian imports of goods and services have fallen relative to GDP. For consumer goods, the decline in imports has particularly severely impacted choice and prices. Western export restrictions and financial market sanctions have made it impossible for Russian companies to import certain goods directly. This has led to higher transportation costs and forced consumers to accept inferior alternatives. Since the invasion, only a few industries have managed to substitute imports.”

Solanko’s conclusion on the effectiveness of the sanctions:

“The sanctions are weighing on the economy every day, reducing government revenue and increasing costs for everyone involved. The war has also ended cooperation between companies and universities and many of their foreign partners, isolating Russia more than ever.”

You can hear how Janis Kluge, a Russia expert at the German Institute for International and Security Affairs (SWP), assesses the effectiveness of the sanctions here (NDR interview from October 28, 2025) and read about it here (analysis from February 2025).

A return to “pre-war growth” will be “very challenging”

In early September, BOFIT had already published a “Policy Brief” by Laura Solanko in which she analyzed in detail the development of Russian economic policy since 1995

("Macroeconomic policies in Russia 1995–2025 – from barter arrangements to an emerging war economy"). She concludes there:

“The costs of the war, both material and human, have placed a heavy strain on Russia’s stabilization fund and fueled persistent inflation. In the longer term, the shrinking working-age population and the ongoing structural transformation of the Russian economy will lead to lower growth rates. Once the war-driven growth in government spending comes to an end, Russia’s weak growth prospects and the deterioration of the business climate (e.g., due to restricted property rights) will make a return to pre-war growth rates very challenging.”

Russia’s inflation rate was still slightly higher in 2025 than in 2024

The following chart from the monthly economic report of the Russian “Economic Expert Group,” which works closely with the Ministry of Finance, illustrates just how persistently high the rise in Russian consumer prices was in 2025 compared to the previous year. According to the statistics agency Rosstat, the annual increase in Russian consumer prices was 8.7 percent in 2025, slightly higher than the 8.5 percent recorded in 2024 (see red bars).

Annual increase in consumer prices in percent

Blue bars: Dec./Dec. of the previous year in %

Red bars: Year-over-year in %

Economic Expert Group: Economic Analysis January 2026, Jan. 27, 2026

The picture changes when analyzing how the price level developed in December compared to the same month of the previous year. The annual inflation rate in December 2025, at 5.6 percent, was significantly lower than a year earlier in December 2024, at 9.5

percent (blue bars). With its often sharply criticized restrictive monetary policy, the Russian Central Bank thus made considerable progress in 2025 toward its target inflation rate of 4 percent (see also Trading Economics chart).

However, a look at the annual average increase in consumer prices (red bars) reveals a persistently high rate of inflation for the years 2024 and 2025 (2024/2023: 8.5 percent; 2025/2024: 8.7 percent). However, the annual inflation rate of 8.7 percent in 2025 was scarcely reported—even by the Russian Central Bank. As is customary in Russia, the focus of reporting was on the inflation rate reached in December at the end of the year.

In doing so, no distinction was often made between the annual inflation rate in December and the annual inflation rate for the full year 2025. Even the Russian Central Bank stated in a bold subheading in its press release of January 21: “Inflation in 2025 was 5.6%.” And in a table at the end of the press release, the annual inflation rate for 2024 is listed as 9.5 percent.

Finmarket.ru also reported: “Inflation in Russia stood at 5.59% in 2025.”

The Moscow Times reprinted an AFP report titled: “Russian Inflation Drops Sharply in 2025.” It states: “Price growth slowed to about 5.6 percent last year, according to the statistics agency Rosstat. This represents a significant decline from the 9.5% recorded in 2024.”

Recommended reading:

- Podcast “Tsars, Data, Facts”

by the German-Russian Chamber of Foreign Trade, hosted by Thomas Baier: - Fake News! Russian Inflation Is Misrepresented, 12 min., Jan. 30, 2026

- Outlook 2026/Review 2025, 15 min., Jan. 21, 2026

- German-Russian Chamber of Foreign Trade:

Focus analyses, German; also Russian; (selection): - Will Russia Go Bankrupt in 2026? Jan. 14, 2026

- Review of 2025 – Outlook for 2026, Jan. 12, 2026

- Politcom.ru; Marina Voitenko: Foreign Trade Sector – Transformation Strategies, Jan. 29, 2026

- ZDF, Felix Klauser: Inflation in Russia. Why a Putin poster is causing a stir, Jan. 28, 2026

- Meduza; Yulia Starostina: Russia’s oil and gas revenues are shrinking. Meduza explains what that means for the Kremlin’s war chest, January 28, 2026

- Economic Expert Group: Economic Analysis January 2026, Jan. 27, 2026

- German Sakharov Society: Envy and Fear: How the Kremlin Shapes the View of the World; Publication of the German translation of a study by the Moscow Levada Center: Russia and the World: Enemies, Opponents, Partners; Jan. 27, 2026

- Riddle.io; Vakhtang Partsvania, Professor of Management at Caucasus University: The Gray Zone: Why Sanctions Against Rosneft and Lukoil Could Be Decisive. On the cumulative effects of sanctions and the shrinking scope for Russia’s oil revenues, Jan. 26, 2026

- Moskauer Deutsche Zeitung; Xenija Melnikowa: Not all gas taps were turned off in 2025, 01/25/26

- Vedomosti Kazakhstan; Andrey Vilde: Negative Choice: How War and Sanctions Are Slowly Plunging Russia’s Economy into Chaos, Jan. 25, 2026

- DW.com; Evgeniy Dyuk, Murali Krishnan: Russia looks to India to fill labor shortage. Why Moscow is shifting its migration strategy, and what awaits Indians arriving in Russia, Jan. 25, 2026

- Politcom.ru; Marina Voitenko: VAT has increased price pressure, Jan. 23, 2026

- Kyiv Post; EuvsDisinfo: In 2026, the Russian economy is in serious trouble, Jan. 23, 2026

- RBC.ru: The Central Bank explained the need for a cautious cut in the key interest rate, Jan. 23, 2026.

- Interfax.com: Central Bank of Russia emphasizes the importance of monthly data amid a surge in inflation in the first half of January, Jan. 23, 2026

- Finam.ru: Egor Susin, author of the Telegram channel TruEcon: Annual inflation could accelerate to 6.4–6.5% in January, Jan. 22, 2026

- Laura Solanko; BOFIT, Bank of Finland; Blog: Rough times for the Russian economy, Jan. 22, 2026

- Carnegie Politika video: Alexandra Prokopenko: How will the Russian economy develop in 2026? Alexandra Prokopenko, Carnegie Berlin Center, spoke with Vladislav Gorin, among others, about the impact of low oil prices on the Russian state budget and which indicators are particularly important for understanding the Russian economic situation; Video, 56 min, Jan. 21, 2026