The Russian Fertilizer Industry: World Leader in Exports and a Winner in Times of Crisis

Russia is the world’s largest exporter of fertilizers and continues to expand its production. Rising prices resulting from the war in the Middle East are boosting revenue potential, but limited capacity, government intervention, and political risks are likely to limit the benefits for manufacturers. Model calculations by the German-Russian Chamber of Foreign Trade show how much the industry and the Russian government could benefit from the price surge. The Chamber’s focus analysis provides an overview of the key producers and their financial figures.

Russian Fertilizer Production and Exports

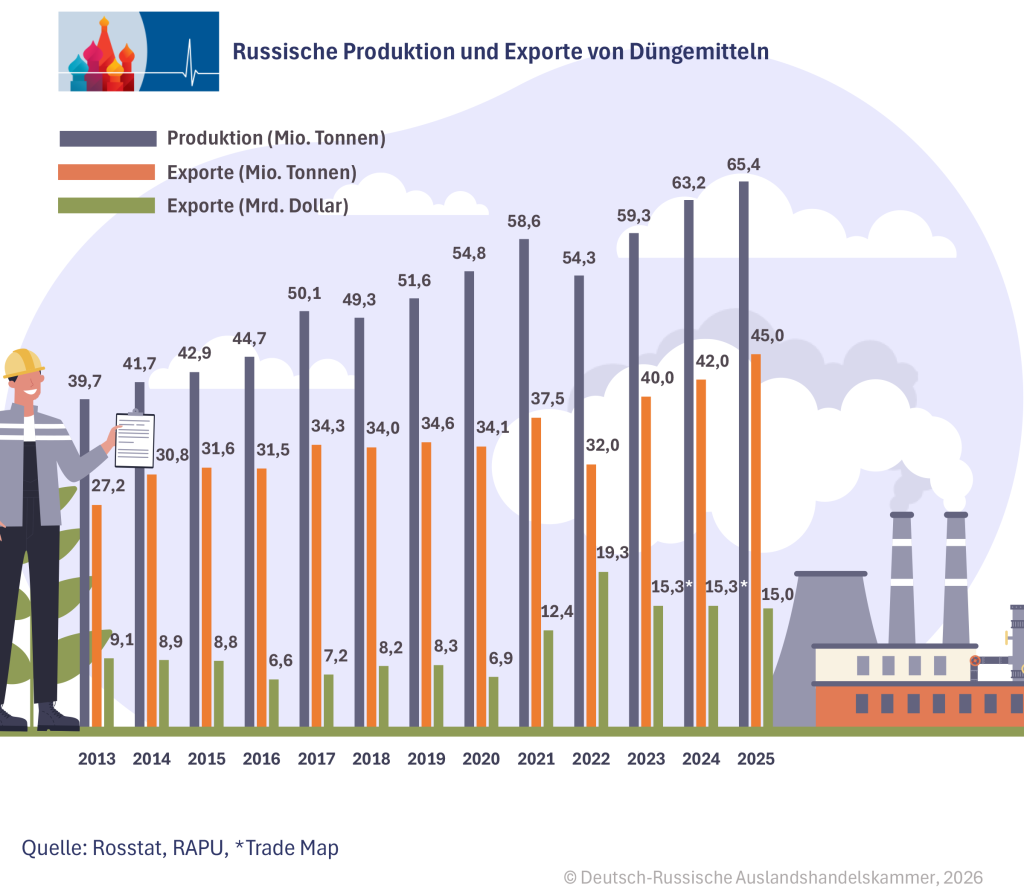

Russia is one of the leading producers and the largest exporter of fertilizers. Russian fertilizer production totaled 65.4 million metric tons in 2025, reports the Russian Association of Fertilizer Producers (RAPU), which brings together the industry’s largest players, citing data from the Federal State Statistics Service (Rosstat). This means the country has surpassed the U.S., India, and Canada and now trails only China, commented RAPU head Andrei Guryev on the figures.

In recent years, Russia has significantly expanded its fertilizer production. In 2013, it stood at 39.7 million tons of raw weight; by 2030, RAPU expects a further increase to 80 million tons. By comparison: The historical record from 1988 stands at 37.1 million tons, based on the entire Soviet Union at that time. This figure does not reflect the gross weight of the fertilizers, but only the actual nutrients they contain—the so-called 100% nutrient volume. The corresponding value for 2025 was 30.5 million tons. For the Russian republic of the USSR, scientific studies report a production of 17.3 million tons in 100% volume in 1985, which was below the 2013 figure of 18.5 million tons.

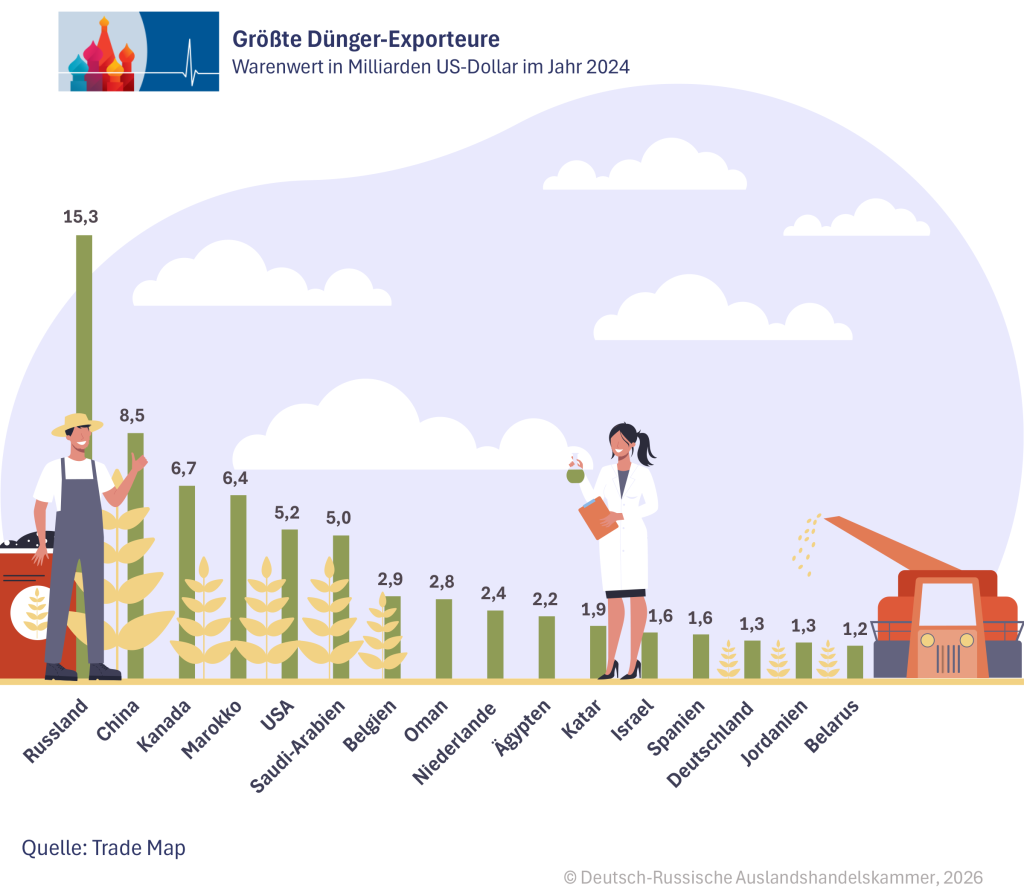

While other top producers such as China and the U.S. produce mainly for their own markets, exports account for the majority of Russian manufacturers’ output. As a result, Russia is by far the world’s largest fertilizer exporter. According to UN trade data, the value of Russian exports in 2024 amounted to $15.3 billion. China, which also imposes government restrictions on its exports, followed with $8.5 billion. Behind them came traditional exporting countries such as Canada and Morocco with $6.7 billion and $6.4 billion, respectively.

In 2025, Russian fertilizer exports totaled 45 million metric tons of gross weight, with export revenues of $15 billion. This is reported by RAPU, citing expert estimates. In a TV interview, however, Russia’s Minister of Agriculture Oksana Lut put 2025 exports at 43 million metric tons and $11 billion. Export figures from the statistics agency Rosstat are only available up to 2021, when they stood at 37.5 million tons and $12.4 billion,

respectively. Like production, exports and revenues have increased by about 65% since 2013. RAPU expects exports to rise to 58 million tons by 2030. Russia’s share of global trade would thus increase from 19% in 2025 to 25%.

Fertilizers as Russia’s Top Export

With export revenues recently totaling around $15 billion (€13 billion), fertilizers have become one of Russia’s most important export commodities. According to statistics from the Russian Customs Service, chemicals and plastics accounted for 8.1% of the value of Russian exports last year. This placed this product group in fourth place, behind oil and gas, metals, and food and agricultural products. According to RAPU, fertilizers accounted for 45% of export revenues in this product group, representing a 3.6% share of Russia’s total exports. In addition, export revenues for the overall chemicals and plastics group grew by 21.6% last year, which was the second-largest increase among the individual product groups. Only the “Machinery and Vehicles” group grew faster, at 26.6%, although this group likely also includes military equipment.

Russia’s strength in the global fertilizer market stems from its abundance of raw materials. It has large reserves of the three main types of fertilizer—nitrogen, phosphorus, and potash—wrote the German magazine Cicero in late 2021, when a global fertilizer shortage had emerged. This was triggered by sharply rising gas prices as a result of the global economy’s recovery from the COVID-19 pandemic. Natural gas, which is also abundant in Russia, is the raw material for the production of nitrogen-based mineral fertilizers, which consist of 90% natural gas and are essentially “refined gas,” as a report by Tagesschau explains.

Energy crises drive up fertilizer prices

During the 2021 crisis, the global market price for urea, a form of nitrogen fertilizer, roughly doubled within a few weeks and rose to $945 per ton by early December. After February 24, 2022, the energy and fertilizer crisis intensified, causing the price of urea to briefly spike to $1,025 per ton in early April. This was also exacerbated by the failure of a pipeline through which Russia had transported large quantities of ammonia through Ukraine to the Black Sea port of Odessa.

In the spring of 2026, another fertilizer crisis looms because the war in Iran has led to a de facto blockade of the Strait of Hormuz, the main shipping route for exports from the Gulf region. The price of urea rose from around $430 to $675 per ton between late February and mid-March 2026. During the 2021/2022 fertilizer crisis, fertilizer prices returned to normal starting in the fall of 2022. One factor in the recovery was that Russian fertilizer did not disappear from the market but was, in part, merely redirected to other buyer countries, explains a recent study by the Center for Agricultural Policy at North Dakota State University. In contrast, there is currently a “physical blockade” of large fertilizer export volumes in the Gulf region. As long as the Strait of Hormuz remains impassable, approximately 43% of global urea exports transported by ship, among other things, are at risk. Depending on the duration of the Strait of Hormuz closure, fertilizer prices could rise to the record levels of 2022 or even higher, the researchers state.

The Impact of the Hormuz Crisis on Export Revenues and Government Revenue

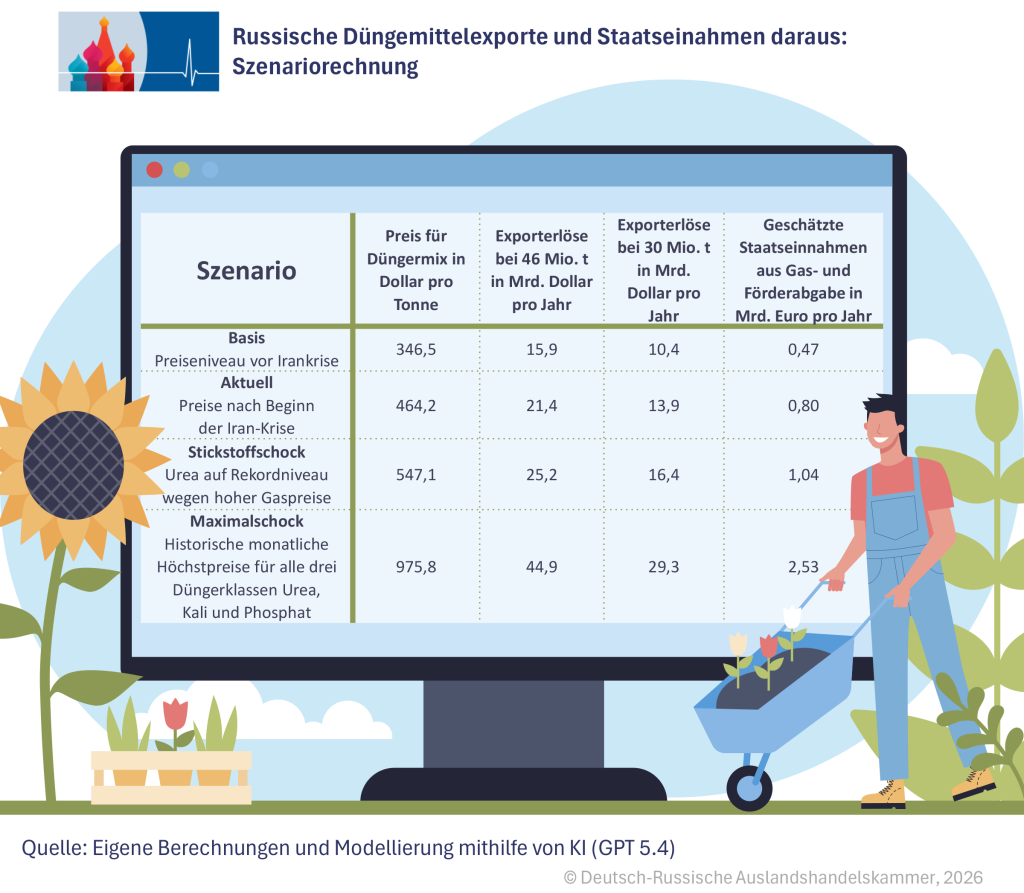

In the crisis year of 2022, Russian export revenues had risen to $19.3 billion (€16.8 billion), according to RAPU, the Association of Russian Fertilizer Producers, with a relatively low export volume of 32 million tons. This translates to an average price of $603 per ton. Even before the Iran crisis, RAPU had forecast total Russian exports in 2026 at 46 million tons of fertilizer. If prices were to reach the 2022 level throughout the entire year, Russian export revenues in 2026 could thus theoretically reach $27.7 billion, equivalent to 24 billion euros.

Going beyond this simple extrapolation, the analysis team at the German-Russian Chamber of Foreign Trade has calculated and estimated potential export revenues and government revenues more precisely for various price scenarios. Depending on the level of world market prices for fertilizers, Russia’s fertilizer exports could total between $15.9 billion and $44.9 billion, equivalent to approximately €14 billion to €39 billion. In the two middle scenarios, gross export revenues range from $21.4 billion to $25.2 billion, or €18.6 billion to €21.9 billion. The additional export revenues on an annual basis would be $6.4 to $10.2 billion higher in the middle scenarios compared to the 2025 figure, equivalent to an increase of €5.6 to €8.9 billion.

In our maximum shock scenario, which anticipates higher prices overall over a period longer than 2022, Russia would generate $44.9 billion—equivalent to €39 billion—in fertilizer exports. Even if export volumes were to decline from the projected 46 million to 30 million tons, revenues in this scenario would still be nearly double those of 2025 at $29.3 billion (€25.5 billion).

According to the Chamber’s model calculation, the direct government revenues derived from the price scenarios would range between 46 and 247 billion rubles per year, equivalent to approximately 474 million to 2.53 billion euros. In the two middle scenarios, the figure would be 73 to 101 billion rubles, equivalent to 0.8 to 1.04 billion euros. For 2025, government revenues were estimated at 46 billion rubles (474 million euros).

The Price-Revenue-Tax Model in Detail

The table shows the complete scenario calculation for Russian fertilizer exports and the resulting government revenues. The calculations are based on RAPU’s forecast of 46 million tons in exports. Additionally, calculations are performed for a lower export volume of 30 million tons, as Russia could restrict exports during times of crisis or a portion of shipments could be canceled for other reasons. In line with the known export structure for 2024, the modeled exports consist of 31.7% potash fertilizer, 23.1% urea (a nitrogen fertilizer), and 11.4% phosphate fertilizer. The remaining 33.8% consists of other fertilizers such as ammonium nitrate and compound fertilizers. Export revenues were calculated using a weighted price for the total mix of urea, potash, and phosphate. For the category of other and compound fertilizers, the model assumes the weighted average price of the first three categories.

Russian government revenue from fertilizers includes resource extraction taxes on potash and phosphate raw materials as well as the gas tax on natural gas for ammonia production (more on this below). The starting point for the scenario analysis is the Ministry of Finance’s 2025 revenue estimate of 24.7 billion rubles in resource extraction taxes and 21.5 billion rubles in gas taxes. The levies are based not on fertilizer exports but on production. The scenario analysis assumes that the total volume and composition of production in 2025 will remain unchanged. It consisted of 44.2% nitrogen fertilizer, 27.5% potash fertilizer, and 28.3% phosphate and compound fertilizers. A rough estimate of the levies is possible, as their amount is linked to the world market prices of urea, potash, and phosphate.

The baseline scenario assumes that the annual average prices for the three fertilizer classes will correspond to the levels seen in January 2026. This is likely to represent a lower bound for expected export revenues and government revenues. The maximum shock scenario, on the other hand, represents an upper bound. It is based on the assumption that the annual average prices for all three fertilizer classes will be at the level of their respective historical monthly highs, i.e., $925 per ton for urea and $1,202 for potash (both April 2022) and $450 for phosphate (October 2008 to March 2009). The Current scenario assumes that prices will average at the already elevated level seen at the end of March 2026. For urea, the scenario uses the price from March 27; for potash and phosphate, it uses the known monthly figures from February 2026 plus an estimated premium of 10% for potash and 20% for phosphate. The third scenario, the nitrogen shock, is based on the experiences of spring 2022, when high gas prices led to a record increase in the urea price. The urea price is set at the record-high monthly value from April 2022, while for potash and phosphate, the slightly higher prices from the Current scenario are used.

Buyers of Russian Fertilizer

The most important buyer of Russian fertilizer is Brazil, which is also the world’s largest importer of fertilizers. In 2025, Brazil imported 11.1 million tons of fertilizer from Russia, according to an analysis of national trade statistics by the Russian investment firm Veles Capital. India ranked second with 5.5 million tons. According to RAPU, more than three-quarters of Russian exports go to countries in the “friendly” BRICS group. This group also includes China, which purchased 4.9 million tons of fertilizer from Russia last year. The two major customers in the West saw differing trends. While the U.S. increased its imports from Russia by 26.7% to 5.1 million tons, the EU reduced them by 5.1% to 4.7 million tons.

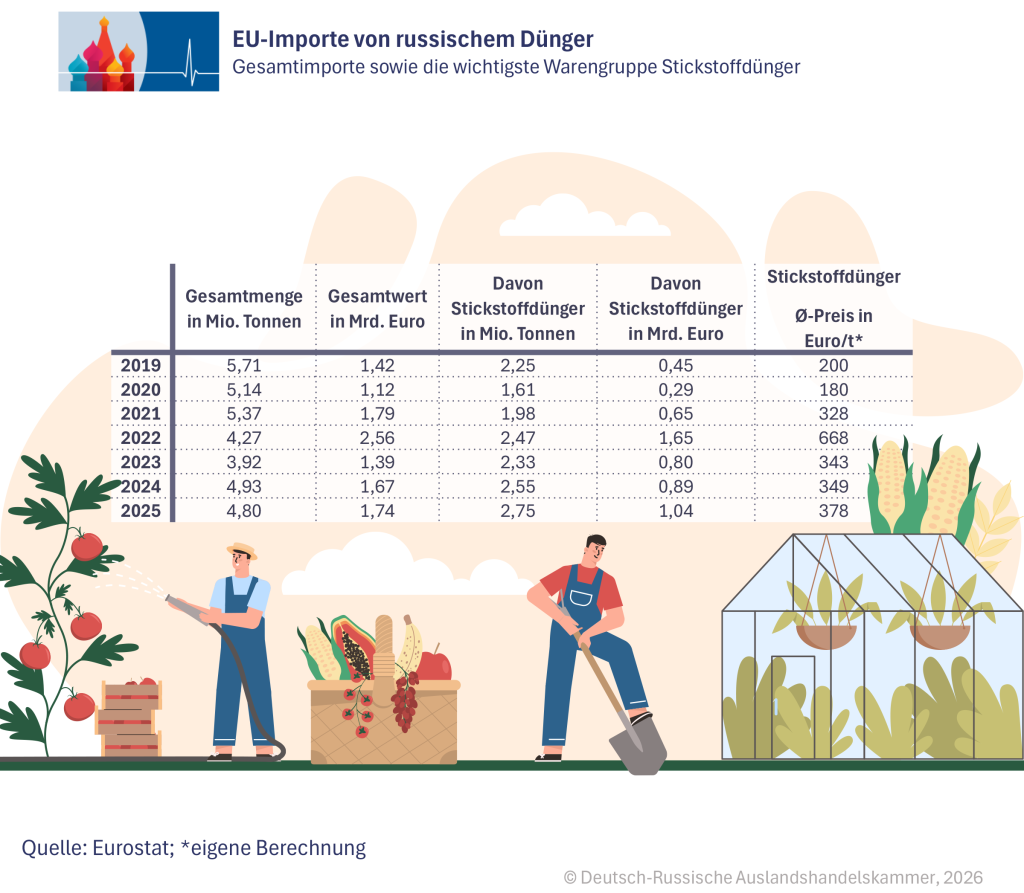

EU: Tariffs Instead of Sanctions on Russian Fertilizer

Since 2022, Russia has redirected numerous trade flows from West to East. In the fertilizer sector, there was less movement among the key destination countries. As early as 2021, Brazil was by far the largest customer, followed by the U.S. and China. According to Eurostat, imports into the EU in that pre-crisis year, with a total value of 1.79 billion euros, were roughly on par with the previous year’s figure of 1.74 billion euros. The total volume of fertilizer imports from Russia fell from 5.37 to 4.8 million tons, which still accounts for about a quarter of total EU imports of nitrogen fertilizer. However, the decline in imports from Russia has accelerated since mid-2025. In the second half of the year, imports stood at 1.53 million tons, 44% below the level of the same period in 2024.

On July 1, additional tariffs on Russian fertilizer came into effect in the EU, aimed at reducing imports from Russia. By 2028, the tariffs are set to be gradually increased nearly tenfold, which, according to Veles Capital, would effectively amount to an import ban on Russian fertilizer. Given the importance of fertilizers for the global food supply, the EU has so far refrained from imposing direct sanctions on the Russian fertilizer industry. Measures have been taken only against individual producers and, in particular, their owners.

In the U.S., however, fertilizers are largely exempt from import tariffs. According to analyst Maxim Shaposhnikov, U.S. companies are taking advantage of this by increasing imports of Russian fertilizers for the domestic market and exporting their own production to the EU.

How the State Profits from Fertilizers

The Russian government captures the profits of fertilizer manufacturers primarily through corporate income tax and, since 2025, through increased taxation on raw materials and intermediate products. This includes higher resource extraction taxes (NDPI) on potash and phosphate raw materials, as well as a newly introduced tax on natural gas for ammonia production, which is linked to export prices. For 2024, the Ministry of Finance expected total revenues of 111 billion rubles (1.14 billion euros), of which 89 billion rubles (910 million euros) came from export duties, which will no longer be levied starting in 2025. For 2025, it projected total revenue of approximately 46 billion rubles (472 million euros). This figure consists of resource extraction taxes amounting to 24.7 billion rubles (253 million euros) and natural gas taxes amounting to 21.5 billion rubles (231 million euros).

A large portion of government revenue is likely to come from corporate income tax. The net profits of the largest fertilizer manufacturers, presented later in this analysis, totaled approximately 400 to 500 billion rubles, equivalent to 4.1 to 5.1 billion euros. This estimate is based on an extrapolation of data available for various time periods in 2024 and 2025, as listed below. With a corporate income tax rate of 20% in 2024 and 25% in 2025, the tax contributions of the seven companies presented could theoretically have amounted to around 140 billion rubles (1.4 billion euros). By comparison: The state’s revenue from oil and gas amounted to 8.48 trillion rubles (87 billion euros) in 2025; in 2024, it was as high as 11.1 trillion rubles (114 billion euros). In addition, oil and gas companies are also subject to corporate income tax. The reported profits of the major industry players totaled nearly 5.5 trillion rubles (59 billion euros) in 2024, roughly exceeding the profits of the major fertilizer producers by more than tenfold.

Fertilizer stocks rise, doubts remain

Investors also expect the Russian fertilizer industry to benefit from the crisis. Shares of the only two major producers listed on the Moscow Stock Exchange, PhosAgro and Acron, have risen by 8–9% since the start of the war in Ukraine through March 17, the business newspaper Kommersant noted. The Moscow Exchange’s benchmark index, IMOEX, also posted gains during this period, making it one of the few globally to show positive performance. However, with a gain of just under 2%, it lagged significantly behind fertilizer stocks.

Some observers predict, however, that Russian manufacturers will benefit only to a limited extent from sharply rising fertilizer prices. As the news agency Reuters learned from industry insiders, production capacities are largely at full capacity and would first have to meet domestic demand. However, prices on the domestic market have been capped by the government for years. The opening of new production facilities for export is not expected until 2027 at the earliest. In addition, the government is likely to skim off a large portion of the additional revenue. In the past, it has used one-time windfall taxes and export duties for this purpose. Analyst Maxim Shaposhnikov also warns against a sharp expansion of production and exports, as Western countries could respond with tougher sanctions against Russian fertilizer.

The Largest Russian Fertilizer Producers

The Russian fertilizer industry is concentrated among a few large producers. Unlike in the oil and gas industry, the market leaders are privately owned. The industry association RAPU stated in the fall of 2024 that its then-13 member companies accounted for nearly 80% of total production. The largest player in the market is the Uralchem Group, which includes the three producers Uralchim, Uralkali, and TogliattiAzot (TOAZ). The group estimates its total capacity at 25 million tons per year, with the eponymous nitrogen fertilizer manufacturer Uralchim accounting for approximately 8 million tons, Uralkali for approximately 12 million tons, and TOAZ for up to 5 million tons of capacity. Financial figures are available only for individual companies.

Uralkali is one of the world’s largest producers of potash fertilizer. Only the Canadian group Nutrien is likely to be larger, as suggested by a report from the U.S. Geological Survey (USGS). In 2024, Uralkali’s production reached a record volume of 12.9 million tons of potash fertilizer. More recent figures are not available. Revenue rose by 10.5% to 463 billion rubles (4.75 billion euros) for the full year 2025, while net profit more than quintupled to 149.6 billion rubles (1.5 billion euros). The third company in the Uralchem Group, TOAZ, is one of the world’s largest producers of ammonia—the key feedstock for nitrogen fertilizers—with an annual capacity of 3.6 million tons. In 2024, TOAZ produced 1.9 million tons of ammonia, 21% more than in 2023, and 1.8 million tons of urea (+9%), a type of nitrogen fertilizer.

EuroChem is likely the largest single Russian company in the fertilizer industry. In 2024, it produced approximately 13 million tons of fertilizer, including 6.2 million tons of nitrogen products, 3.5 million tons of potash fertilizer, and 4 million tons of phosphate and complex fertilizers. These figures also include overseas facilities located in Belgium, Brazil, Lithuania, and Kazakhstan. In the most recent full annual report, which EuroChem submitted for 2023, the company reported revenue of 363 billion rubles (3.7 billion euros), with a net profit of 112 billion rubles (1.1 billion euros).

PhosAgro is one of the world’s largest producers of phosphate fertilizer. Its total production increased by 4.3% to 9.15 million tons in the first nine months of 2025. Of this, 7 million tons were phosphate fertilizers (+5.5%) and 1.94 million tons were nitrogen fertilizers (+1.9%). Revenue for the first three quarters amounted to 441.7 billion rubles (4.53 billion euros), with a net profit of 95.7 billion rubles (982 million euros). Compared to the same period last year, revenue rose by 19.1% and net profit by 47.6%.

The number four player in the Russian fertilizer market is Acron, a major producer of complex fertilizers that combine multiple plant nutrients. The company produced a total of 7 million tons of fertilizer last year, 4.1% more than in 2024. Among the fertilizer categories, nitrogen fertilizers dominate with 4.55 million tons (+7.3%). Compound fertilizers accounted for 2.41 million tons (+0.4%). Revenue rose by 20% to 237.6 billion RUB (2.44 billion euros), and net profit by 30% to 36.7 billion rubles (380 million euros).

The Azot Group is Russia’s fifth-largest producer of nitrogen fertilizers, according to the rating agency Expert RA. The company itself estimates its total capacity in 2024 at just under 4.3 million tons of nitrogen fertilizer and 1.9 million tons of the raw material ammonia. The company reports total production in 2024 at 4.2 million tons of fertilizer. According to financial portals, GK Azot’s revenue in 2024 amounted to 115.2 billion rubles (1.2 billion euros), with profits totaling 7.7 billion rubles (79 million euros).

Another of the few other major fertilizer producers is the chemical company KuibyshevAzot. The company reports production volumes for the first half of 2025 at approximately 0.55 million tons of ammonia (-1.6%) and 1.04 million tons of nitrogen fertilizer (+7.4%). Fertilizers accounted for slightly more than half of its business. Revenue for the six-month period remained nearly at the same level as the prior-year period at 44.1 billion rubles (450 million euros) (+1%), while net profit rose by 48% to 3.46 billion rubles (40 million euros). Revenue from ammonia and nitrogen fertilizers alone totaled 25.6 billion rubles (263 million euros).

This article first appeared in the exclusive newsletter of the German-Russian Chamber of Foreign Trade