The Implications of Hormus for Russia and Germany: Between Theory and Reality

In mid-May 2026, Russia’s gross oil revenues were in line with the $100-per-barrel scenario outlined in the German-Russian Chamber of Foreign Trade’s March model. According to Bloomberg, Urals averaged $94.87 per barrel in May—61% above the budgeted price of $59.

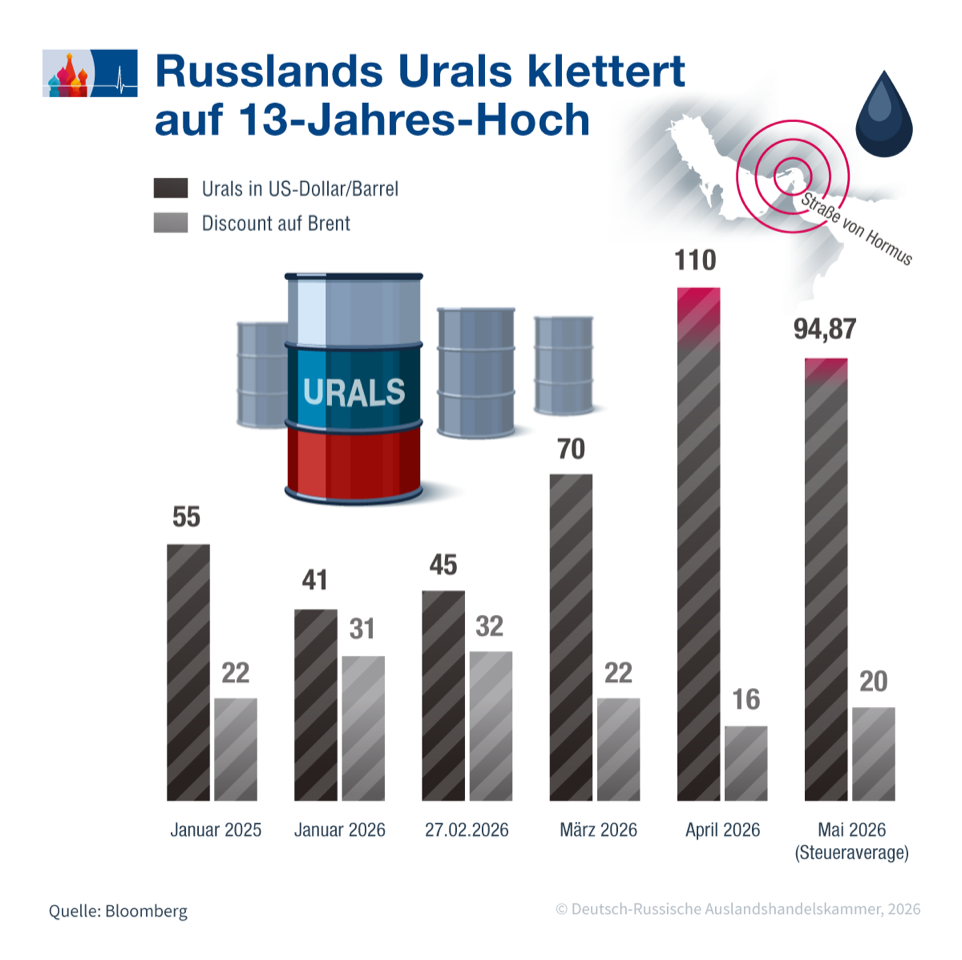

Urals at 13-Year High

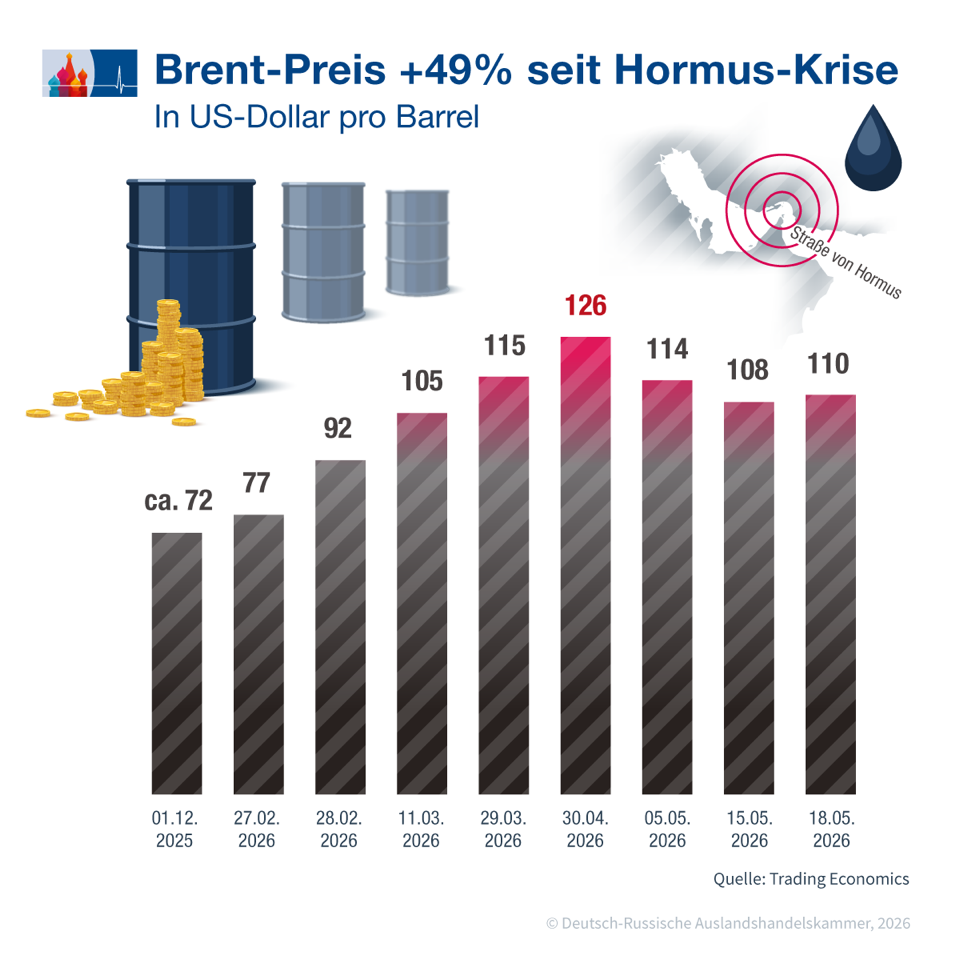

Since the start of the war on February 28, Brent has risen from $77 to a high of $126 on April 30 and was trading at $108 on May 20. The increase from the pre-war level of around $72 in early December 2025 is 49%, as data from Trading Economics shows.

The Russian Urals crude grade rose from $45 at the end of February to $70 in March and $110 in April. In May, the Russian benchmark grade averaged $94.87—the highest level since March 2013. The discount of Russian oil relative to North Sea Brent is also shrinking. At the start of 2026, the discount was still $31 per barrel, driven by U.S. sanctions against Indian buyers of Russian oil. With the elimination of Iranian competition and the U.S. Treasury Department’s 30-day sanctions waiver on March 8, the discount fell to $16 to $22. In May, it stands at around $20.

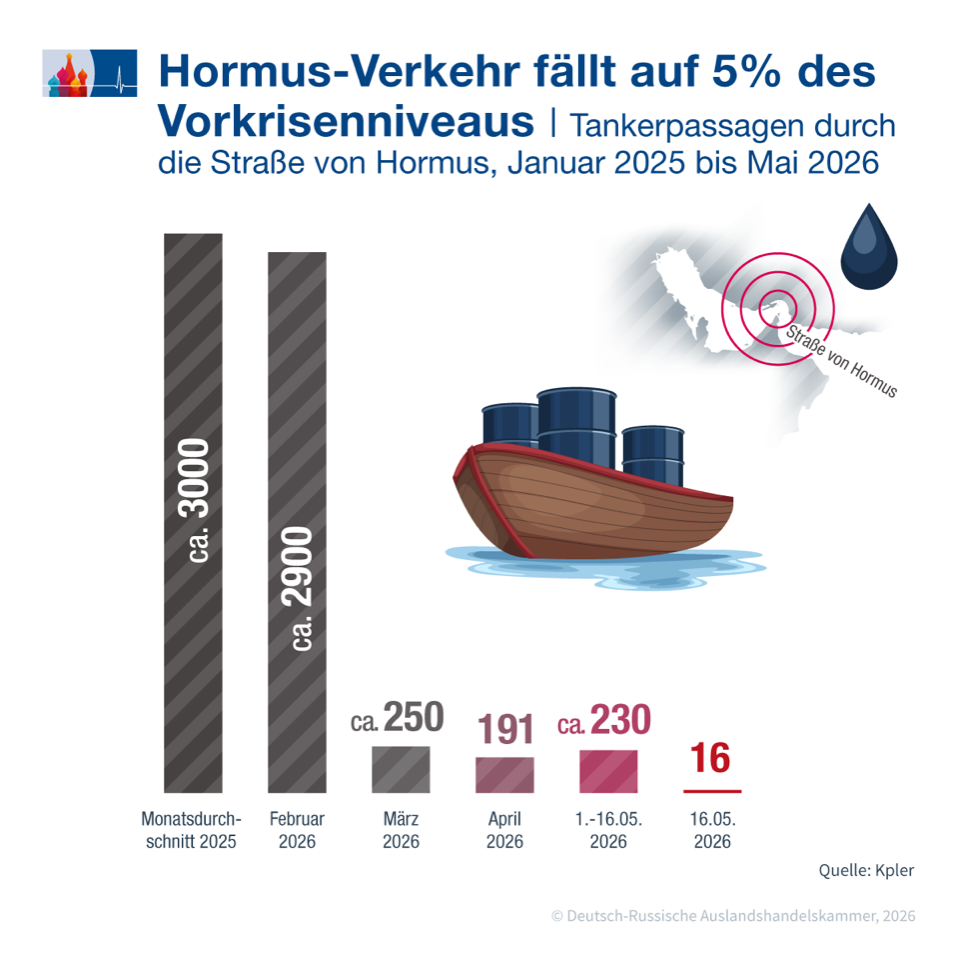

Tanker traffic through the Strait of Hormuz has effectively come to a standstill. According to ship data from industry analysts at Kpler, analyzed by the U.S. Naval Institute, only 14 to 15 tankers passed through the strait daily in the first half of May. Before the war began, around 3,000 tankers passed through the Persian Gulf each month. In April 2026, the figure was 191—a 94% decline. The Asia-Pacific region sources 46% of its oil imports from the Persian Gulf and is seeking alternatives.

The Chamber’s March Forecast Put to the Test

The model calculation by the German-Russian Chamber of Foreign Trade dated March 11, 2026, which was cited by numerous newspapers and television stations, had estimated Russia’s annual gross revenue from crude oil exports in six Urals price scenarios: $87.6 billion at $50 per barrel, $131.4 billion at $75, $175.2 billion at $100, $227.8 billion at $130, $262.8 billion at $150, and $350.4 billion in the extreme scenario of $200. The budgeted price was $59 per barrel of Russian oil.

The average tax revenue level in April of $94.87 is just below the $100 scenario. Extrapolated on an annual basis, this results in gross export revenues of around $166 billion—about $63 billion more than in the budget. Before the war began, Urals traded at $41 to $45, and revenues were below the budgeted figure. Within ten weeks, this has turned into a double-digit billion-dollar surplus.

Russian analysts, with their conservative expectations, were closer to the mark than Western commentators. Sergei Kaufman of the Moscow-based online broker Finam expected the discount to fall below 17 euros per barrel—which is exactly what happened. His colleague Nikolai Dudchenko projected additional revenue of up to 775 billion rubles—about 9 billion euros—based on an annual average Urals price of 51.7 to 55.9 euros. Alexander Frolov of the Institute for National Energy predicted that oil and gas revenues would rise by 30% to 50% starting in March. In fact, the April figure fell short of the upper limit, as dumping mechanism payments and the strength of the ruble absorbed a large portion of the price premium.

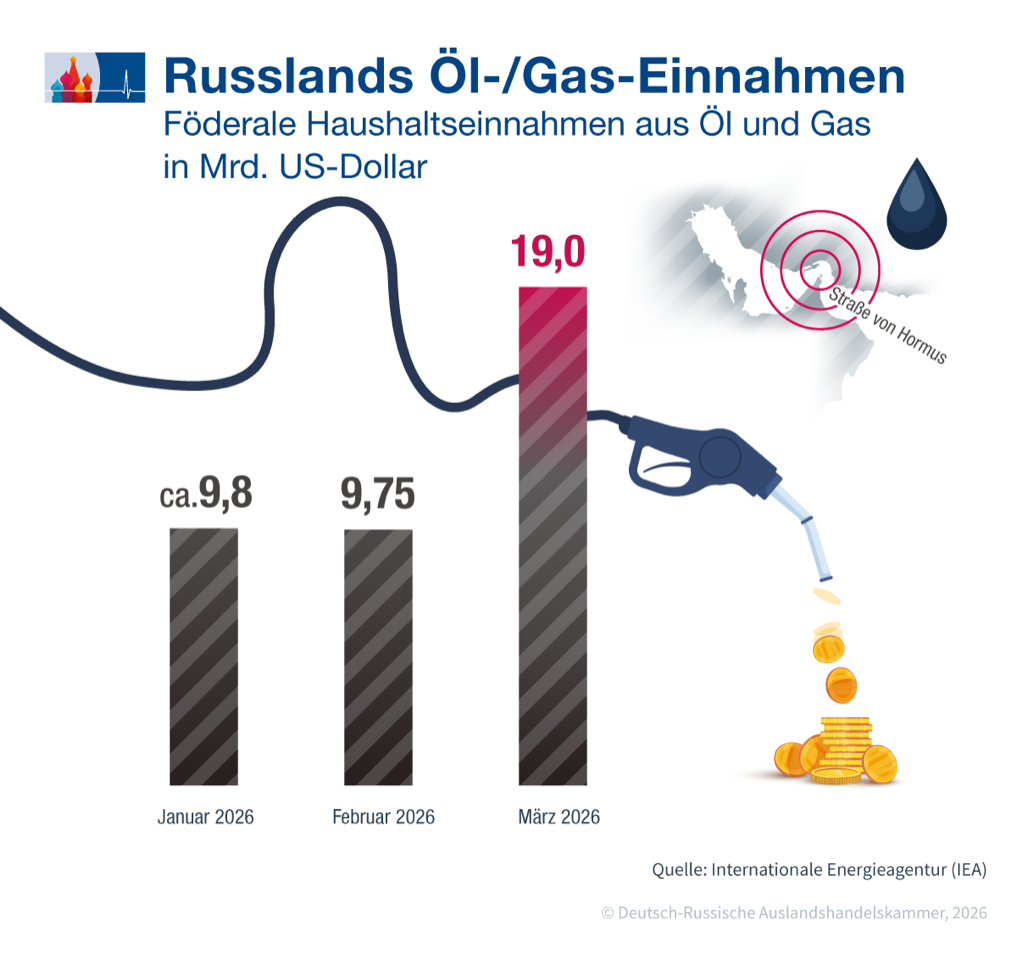

Budget: May Jump Compared to Last Year

Russia’s federal oil and gas tax revenues totaled 855.6 billion rubles in April, or 10.5 billion euros. That was 40% more than in March, according to the Russian Ministry of Finance. A Reuters projection for May 2026 showed a 39% increase compared to May 2025. Russia’s Gazprombank estimates that special revenues from the war in Iran amounted to 400 to 500 billion rubles—5 to 6 billion euros—in May alone, based on a Urals price of around $100.

Over the first four months of 2026, oil and gas revenues totaled 2.3 trillion rubles, around 28 billion euros, 38.3% below the same period last year. Low prices in January and February, as well as the strong ruble, are dragging down the annual average. Russian energy analyst Kirill Rodionov of the Moscow Center for Economic and Political Reforms told the business newspaper RBC in March that the average price of $40 in the preceding months had been “critical for the budget.” This critical phase ended with the Israeli-American attack on Iran on February 28.

EU Council President António Costa stated in Brussels as early as mid-March: Russia is gaining new resources to finance its military. James Henderson of the Oxford Institute for Energy Studies told the U.S. broadcaster NBC that it would “surprise no one if Russian military spending were to rise as a result.”

India and China Compensate for Iran Shortfall

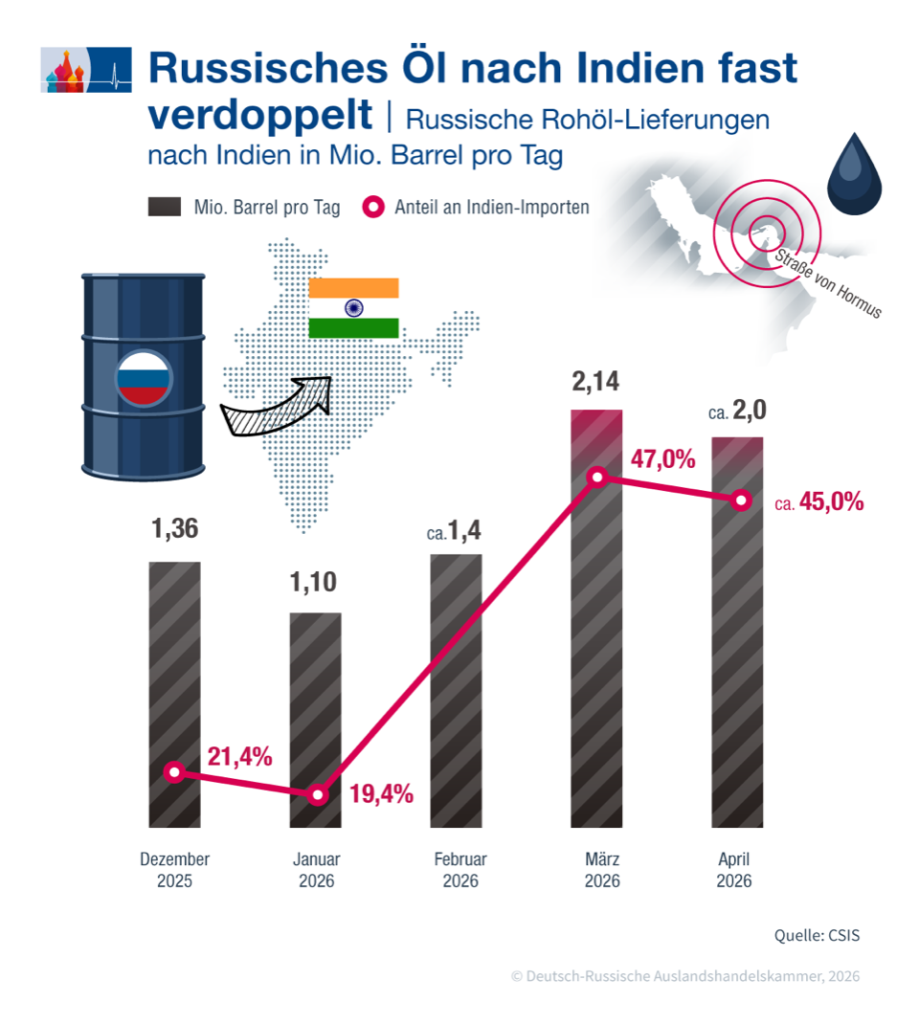

The largest shift in trade flows since the start of the military strikes against Iran and the blockade of the Strait of Hormuz involves India. According to the Washington-based think tank Center for Strategic and International Studies (CSIS), Russia supplied exactly 2.14 million barrels per day to India in March 2026—47% of all Indian oil imports. In December 2025, the figure was still 1.36 million barrels, representing a share of just 21.4%. Within three months, Russia’s market share in India has thus more than doubled. In April, the volume declined slightly to around 2.0 million barrels, while the market share remained at around 45%.

An Indian government official told the Reuters news agency on May 18 that the country would continue to purchase Russian oil regardless of U.S. sanctions.

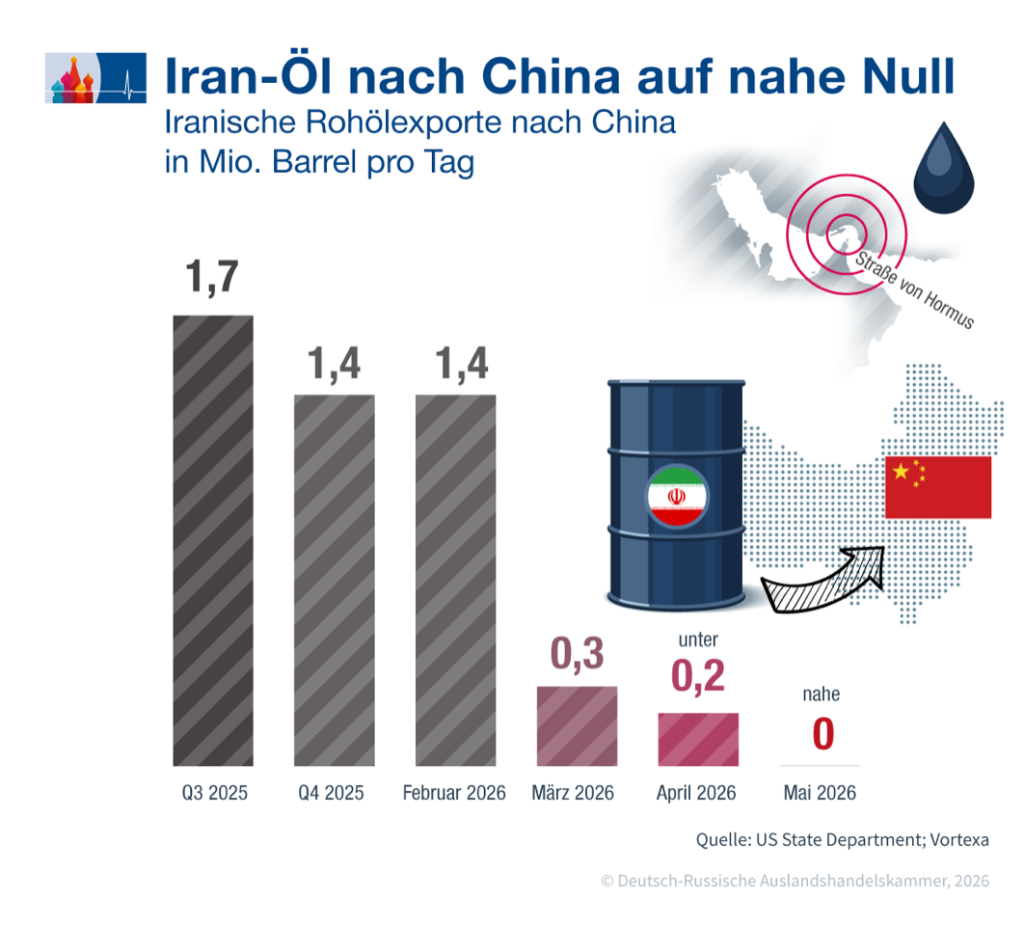

China is also purchasing more Russian oil because Iranian crude has disappeared from the market since the U.S. blockade. According to the U.S. State Department and the market intelligence provider Vortexa, Iranian crude oil exports to China fell from 1.7 million barrels per day in the third quarter of 2025 to 1.4 million in February 2026, then to 0.3 million in March, later to below 0.2 million in April, and to nearly zero in May. The Iranian shortfall roughly corresponds to the increase in Russian shipments to India.

Russian exports are rising

Russia’s oil exports via the ports of Primorsk, Ust-Luga, and Novorossiysk rose by about 150,000 barrels per day in the first half of May, according to Reuters—an increase of roughly 9% compared to April—to between 2.35 and 2.4 million barrels per day. According to British analysts, this is due to ongoing drone attacks on Russian refineries, which are forcing Moscow to export more crude oil instead of refined products.

Market participants warn that spare capacity in the pipeline network of state-run operator Transneft is nearing its upper limit. The port of Novorossiysk processed around 1 million tons of backlogged April volume in the first ten days of May. A drone attack there had briefly halted tanker loading in April. Loading rates at the three ports currently stand at 1.1 million (Primorsk), 0.7 million (Novorossiysk), and 0.6 million barrels per day (Ust-Luga).

Fertilizer: Liebig’s Law Strikes

According to the Washington-based International Food Policy Research Institute (IFPRI), a research institution of the World Bank Group, the Persian Gulf supplies 36% of the globally traded urea, 29% of anhydrous ammonia, 26% of diammonium phosphate, and 13% of monoammonium phosphate. The closure of the Strait of Hormuz thus effectively blocks half of global nitrogen and phosphate fertilizer flows.

In his article for the industry portal OilPrice, American energy journalist Kurt Cobb recalls the law of mineral nutrition formulated by German chemist Justus von Liebig (1803–1873): If an essential nutrient is missing, the deficiency cannot be compensated for by using more of others. According to Reuters, Argentine wheat farmers are already reducing their use of urea, while Egyptian farmers are halving their planted acreage. A survey by the American Farm Bureau Federation found that 70% of U.S. farmers will be unable to meet their fertilizer needs by 2026.

With exports of 45 million tons of fertilizer and export revenues of $15 billion in 2025, Russia is the world’s largest fertilizer exporter. The model calculation by the German-Russian Chamber of Foreign Trade dated March 30, 2026, projected additional revenue of $6.4 to $10.2 billion compared to 2025 under medium-price scenarios.

Helium: Russia as a Potential Emergency Supplier

The Iranian attack on Qatar’s Ras Laffan gas facility in late March 2026 threw the global helium market out of balance. About one-third of the global supply disappeared overnight. Qatar had previously accounted for one-third of global production—63 million cubic meters out of 190 million cubic meters—according to the U.S. Geological Survey (USGS). An analysis by the German-Russian Chamber of Foreign Trade dated April 14, 2026, highlights Russia’s role in this market.

Russia has been the third-largest helium producer since 2024. Production grew from 4.5 million cubic meters in 2020 to 18 million cubic meters in 2025—a fivefold increase in five years. The capacity of Gazprom’s Amur gas processing plant is theoretically 60 million cubic meters, the former level of Qatar. In reality, the plant produces 18 million cubic meters, far below its potential. The German plant manufacturer Linde left Russia in June 2022; Gazprom is continuing the ramp-up without a Western licensor.

Europe consumes 40 million cubic meters of helium annually and produces only 3 million itself—primarily in Poland. The French industrial gas group Air Liquide declared force majeure on March 17, 2026, and announced that it would be able to supply only 50% of its usual volumes. Spot prices in Europe rose 30% to 50% above global levels. The major U.S. bank Bank of America estimates that even with a rapid ceasefire, the global market will face a 15% shortfall in demand well into 2027. Russia’s Amur plant remains the only source capable of increasing production in the short term.

Steingart’s Five Theories on the Costs of Hormuz

In his Pioneer Morning Briefing, German journalist and publisher Gabor Steingart summarized the global costs of the crisis in five points. First, it is hitting U.S. households: According to Brown University’s Watson School of International and Public Affairs, Americans have spent more than $42 billion extra on gasoline and diesel since the war began—$320 per household. Gas prices per gallon (3.8 liters) have risen by over 50% since Trump took office.

Second, energy costs are weighing on businesses. A Reuters analysis of publicly traded companies in the U.S., Europe, and Asia puts the cost of the crisis so far at $25 billion. According to UBS strategist Gerry Fowler, consumer-facing sectors such as automotive, telecommunications, and household goods must factor in profit revisions of more than 5%.

Third, lost growth is dragging down the global economy. Before the war, the International Monetary Fund (IMF) had forecast global growth of 3.4% for 2026. In the worst-case scenario, the IMF now expects 2%—a decline of 1.4 percentage points. With a nominal global GDP of $125 trillion, this equates to $1.75 trillion in lost economic output. Steingart calls it “the biggest drag on growth outside of times of world war and pandemic.”

Fourth, inflation is rising. In the U.S., the inflation rate is already at 3.8%, and in Europe at 3%. In its worst-case scenario, the IMF expects global headline inflation to reach 5.8% in 2026, compared to 3.9% in the pre-war forecast.

Fifth, interest rates are rising. Since the start of the war, the average 10-year interest rate in G7 countries has climbed from 3.2% to just under 4%, while the 30-year rate has risen to 4.6%. With a debt burden of $65.6 trillion, the 80-basis-point increase translates to roughly $520 billion in additional interest pressure per year once the old bonds mature.

Steingart comments pointedly: “The man in the White House has not only disappointed his voters, but betrayed them. The bill—and this is the bitter news for Europe—will be delivered worldwide. The German government should consider suing the U.S. for damages.”

Hormuz Effect: German Economic Recovery Fails to Materialize

According to the International Energy Agency (IEA), Germany imports around 1.8 million barrels of crude oil daily. With an oil price of $100, the annual import bill rises to €60.4 billion—double the $50 level before the war began. At $130, it would be 78.6 billion euros. The total federal budget for 2026 amounts to 480 billion euros in expenditures.

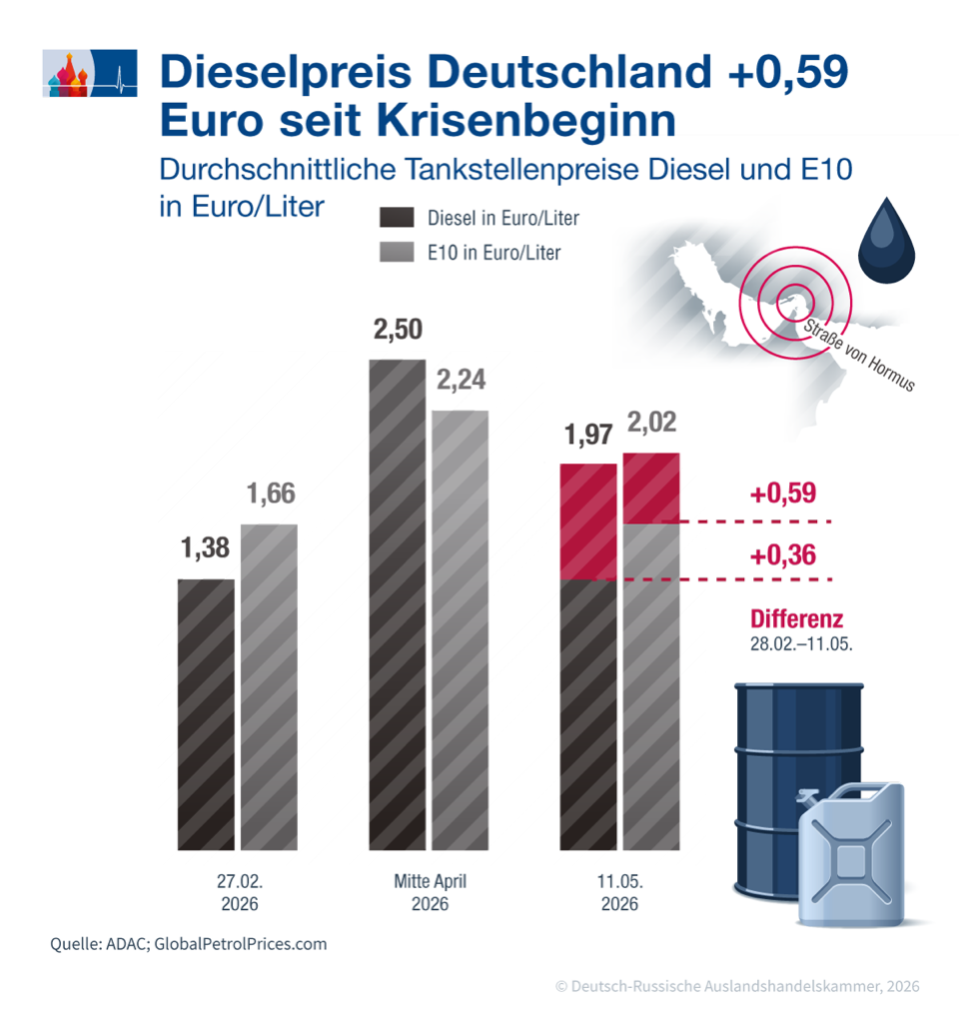

The burden is already visible at gas stations. The ADAC average price for diesel climbed from February 27, 2026 (€1.38 per liter) to €1.97 in mid-May—an increase of €0.59 or 43%. E10 rose from 1.66 to 2.02 euros, an increase of 0.36 euros. Peak prices stood at 2.50 euros per liter of diesel in mid-April.

Sebastian Dullien, scientific director of the Düsseldorf Institute for Macroeconomics and Economic Research (IMK), had already concluded in March that the recovery of the German economy hoped for in 2026 was “definitely off the table” due to the war. This article was prepared for the German-Russian Chamber of Foreign Trade.