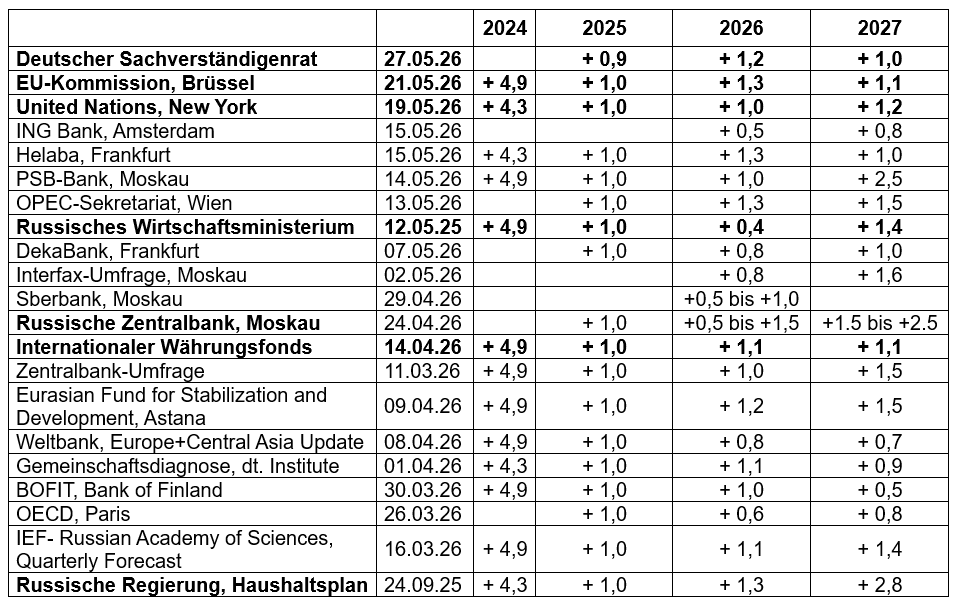

The EU expects significantly higher growth in Russia in 2026 than the government does

Author: Klaus Dormann

In its budget planning in September 2025, the Russian government had still assumed that Russia’s economic growth would pick up to 1.3% in 2026. However, on May 12, it announced in a new forecast that growth is likely to continue to slow. It is expected to drop from 1.0% in 2025 to just 0.4% in 2026 (Interfax.com).

The European Commission, however, expects the opposite trend this year. In the Russia chapter of its “Spring Forecast” published on May 21, the Commission “adopts” the Russian government’s previous growth forecast and now expects gross domestic product growth to accelerate to 1.3% in 2026.

In doing so, the Commission largely aligns with the view of the International Monetary Fund. The IMF had already raised its forecast for Russia’s economic growth this year from 0.8% to 1.1% in mid-April. In the “Update” to its global economic forecasts published on May 19, the United Nations Department of Economic and Social Affairs expects similarly strong growth in Russia this year (+1.0%). The same applies to the German Council of Economic Experts (+1.2%).

EU Economic Affairs Commissioner Valdis Dombrovskis pointed out that Russia’s economy is benefiting from rising energy prices. He once again firmly rejected any easing of sanctions against Russia (see the end of the article for further information).

The European Commission and the IMF expect Russia’s economy to grow by a further 1.1% in 2027. The UN Department of Economic and Social Affairs expects 1.2% growth next year, and the Russian government anticipates growth accelerating to 1.4% in 2027. However, this would be only half as high as the government had expected for 2027 just six months ago (+2.8%).

GDP Forecasts for Russia 2024–2027

Year-over-year change in real gross domestic product, in percent

EU footnote on the credibility of the Russian government’s economic data

Regarding the credibility of official Russian economic data, the European Commission notes in a footnote in the Russia chapter of its forecast:

“Some analysts have argued that the actual situation is worse than what the official Russian macroeconomic data portray. Although not all of the economic arguments put forward in this regard are entirely convincing, in the context of Russia’s war of aggression, the possibility of data manipulation cannot be entirely ruled out. It is noteworthy, however, that even the official data now clearly point to an economic downturn.”

How the EU views the current state of the Russian economy

From the Commission’s perspective, the Russian economy is “now divided into two parts.” The “military-industrial complex” continues to be supported by government contracts and enjoys access to particularly favorable credit terms. It is given preferential treatment over sectors of the “civilian economy.”

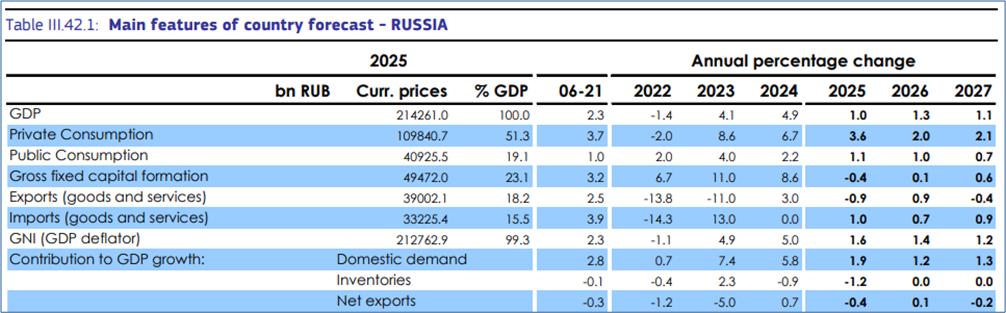

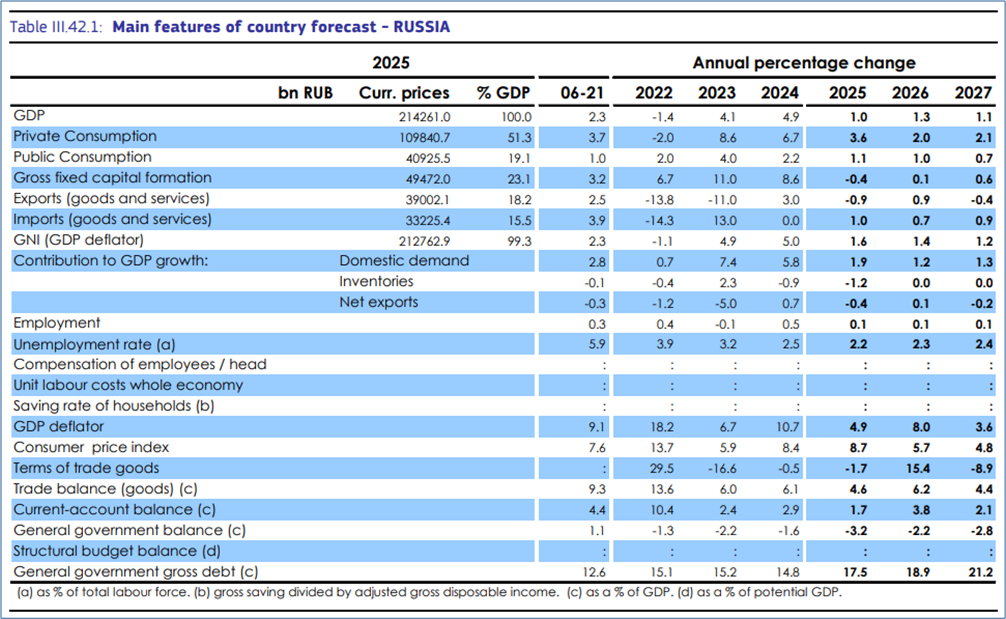

Looking back at developments in 2025, the European Commission summarizes: Economic growth slowed drastically in 2025 from 4.9% to 1%. “The war of aggression against Ukraine increasingly took its toll,” the Commission notes.

Growth weakened across all sectors of gross domestic product. Gross fixed capital formation even fell by 0.4% year-over-year (2024: +8.6%).

The rise in consumption roughly halved. Private consumption still grew by 3.6% (2024: +6.7%), while public consumption rose by 1.1% (2024: +2.2%). In particular, relatively resilient private consumption was instrumental in preventing an even sharper slowdown in economic activity in 2025.

The persistently tight labor market continued to drive real wage increases.

The average unemployment rate stood at a historic low of 2.2% in 2025. It is expected to rise to only 2.4% in 2027 (see also: Cash.ch; Bloomberg: Labor Shortage in Russia Worsens Due to War and Demographics, May 23, 2026).

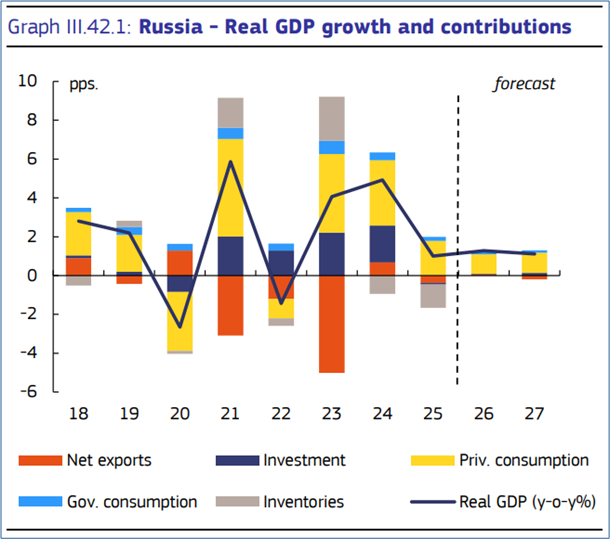

Russia’s real gross domestic product and its allocation

European Commission: Spring 2026 Economic Forecast; Full Document;

with forecast for: Russian Federation; excerpt; May 21, 2026

EU Commission forecasts for 2026 and 2027

The Commission expects Russia’s economic growth to accelerate “marginally” from 1.0% to 1.3% in 2026. However, according to its assessment, growth is likely to lose momentum again as early as 2027 and decline to 1.1% (see the black line in the figure below).

Real Gross Domestic Product and Its Components

Contributions to growth from the components net exports, investment, private consumption, government consumption, and inventory changes in percentage points

European Commission: Spring 2026 Economic Forecast; Russian Federation, May 21, 2026

According to the EU, private consumption growth is expected to continue to slow to around 2% in 2026 and 2027, although “certain positive spillover effects from high export revenues in the oil and gas sector” are anticipated. At the same time, investment activity is unlikely to increase significantly and is expected to “continue to act as a drag on growth” for the overall economy. The figure above shows that real GDP growth in 2026 and 2027 will be driven almost entirely by private consumption (yellow bar segments).

What growth impulses will the sharp rise in oil and gas prices bring?

According to the Commission’s assessment, the sharp rise in hydrocarbon prices triggered by the conflict in the Middle East will “support Russian GDP through various channels.” Overall, however, it assumes that a large part of the positive effects of these “windfall gains” will be dampened by persistent structural weaknesses in the Russian economy.

As for investment, the Commission expects it to begin growing slowly again in 2026 and 2027—aided by improved monetary conditions and the additional revenue from the hydrocarbon sector. However, according to the Commission, the majority of the additional revenue from higher oil and gas prices is unlikely to be used for investment by companies and the Russian government. It is expected to be used primarily to meet federal budget deficit targets and reduce corporate debt.

The Commission forecasts a further slowdown in private consumption growth compared to 2025, as wage growth is expected to slow despite the oil price boom. Additionally, consumer sentiment has deteriorated.

Regarding the volume of Russian exports, the European Commission expects only a slight increase. Russia’s oil production is already close to its capacity limit and is constrained by the quotas agreed upon by OPEC+.

European Commission: Spring 2026 Economic Forecast;

Full Document; with forecast for: Russian Federation, May 21, 2026

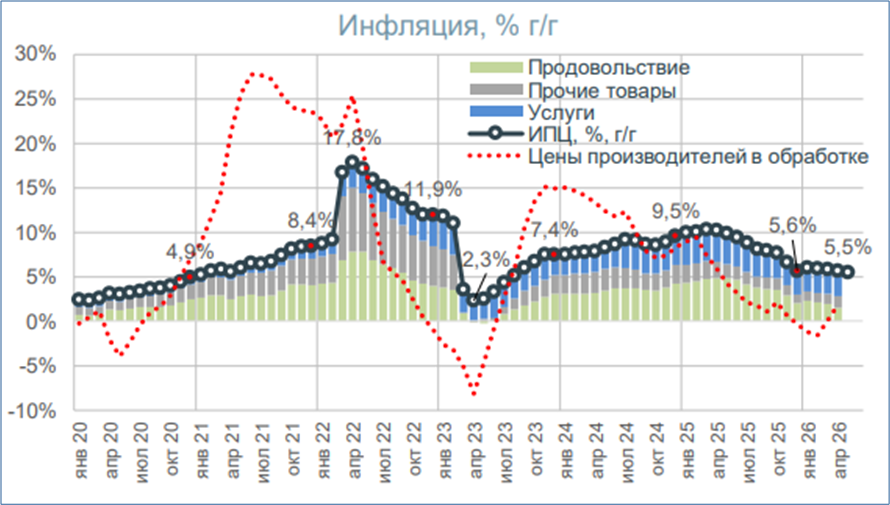

The slowdown in price increases is continuing gradually

Regarding consumer price trends, the Commission notes that the decline in the inflation rate observed since March 2025 came to a halt in January 2026 due to a 2-percentage-point increase in the value-added tax. The annual inflation rate rose by 0.4 percentage points to 6% in January. It remained largely at this level in February and March.

The following chart from the weekly report of the state development corporation VEB.RF shows that the annual increase in consumer prices was 5.6% in April. In the week ending May 14, it stood at 5.5%, according to the institute’s estimate, the same as the previous week.

Inflation trends in Russia

black line: Change in the consumer price index compared to the same month of the previous year

red line: Change in the industrial producer price index compared to the same month of the previous year

VEB Institute: Global Economy and Markets, May 15–21, 2026

According to the Commission, persistently high military spending is likely to exert further upward pressure on prices. However, the Commission estimates that the inflationary effects stemming from the current rise in commodity prices will be “largely dampened” in Russia due to fuel subsidies.

Regarding the central bank’s monetary policy, the Commission notes that, due to persistent price pressures, the central bank has so far only “cautiously” lowered its key interest rate, which continues to result in high real interest rates. Overall, the EU expects inflation in Russia to continue to decline, averaging 5.7% in 2026 and 4.8% in 2027.

The Russian Ministry of Economic Development expects the inflation rate to fall to 5.2% by the end of 2026. From Minister Reshetnikov’s perspective, this creates “increasingly more arguments” for further easing of monetary policy. However, the minister emphasizes that the specific decision regarding the pace and extent of interest rate cuts lies with the Central Bank Council (russland.capital.de with a video of Central Bank President Nabiullina’s statement on the Central Bank’s monetary policy).

Higher commodity prices will weigh on the federal budget deficit in 2026

In 2025, according to the European Commission, revenue from the oil and gas sector in the Russian federal budget was weighed down by low global oil prices, a strong ruble, and Western sanctions. Revenue fell by 24% year-over-year. At 2.6% of GDP, Russia recorded its highest federal budget deficit since the start of the pandemic. In the first quarter of 2026, revenues from the oil and gas sector plummeted by as much as 45% year-over-year.

However, according to the Commission’s assessment, the conflict in the Middle East has fundamentally altered the conditions for the budget’s future development.

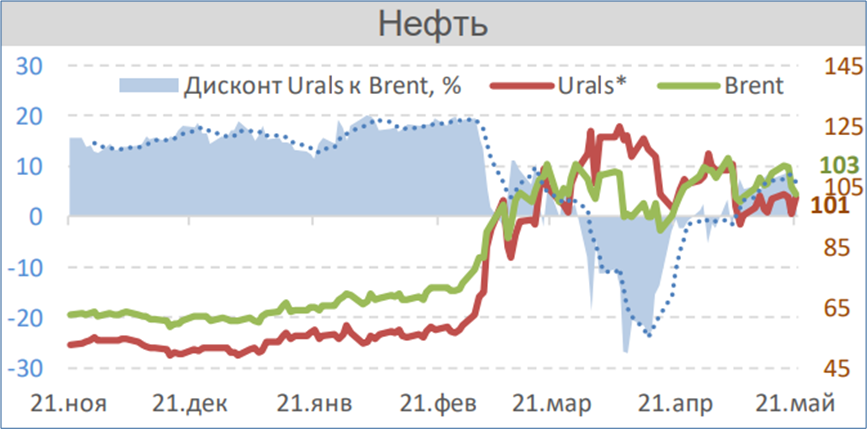

The following chart from the VEB Institute’s latest weekly report shows that prices for Brent crude (green line) and Russian Urals crude have risen sharply since the end of February. Most recently, Urals was trading at $101 per barrel, roughly twice as high as at the start of the year.

Prices of Brent and Urals crude oil in $/barrel (right scale)

Difference between the Urals price and the Brent price in % (left scale)

VEB Institute: Global Economy and Markets, May 22, 2026

According to the European Commission, the sharp rise in global hydrocarbon prices makes the revenue projections outlined by the government in the 2026 budget feasible. In contrast, the Commission considers the expenditures estimated in the budget to be “unrealistically low” against the backdrop of the ongoing war in Ukraine.

The Commission expects Russia’s general government deficit to narrow from 3.2% of GDP in 2025 to 2.6% of GDP in 2026 (before it is expected to rise again to 2.8% of GDP in 2027).

The general government debt-to-GDP ratio, which rose to 17.5% of GDP in 2025, is projected by the Commission to continue rising over the next two years to 18.9% and 21.2% of GDP, respectively, given this budgetary trajectory.

The risks to Russia’s economic outlook remain considerable

The European Commission cites further Ukrainian attacks on Russia’s hydrocarbon production and processing facilities as a “downside risk” to the Russian economy (Tagesschau, FR.de; t-online).

Another risk is the debt of Russian companies. It has risen significantly in recent years due to high interest rates and tightened sanctions. Loan defaults could weigh on economic growth.

Furthermore, if inflation proves more persistent than expected, renewed monetary tightening measures would further dampen growth.

According to the Commission’s assessment, the most significant “upside risk” to Russian economic growth is the further course of the conflict in the Middle East. If it lasts longer than expected or has far-reaching effects on energy infrastructure in the Middle East, this would lead to additional benefits for the Russian economy.

EU Commissioner Dombrovskis Rejects Easing of Russia Sanctions

Toward the end of his press conference on the EU’s spring forecast, Latvian EU Commissioner Valdis Dombrovskis emphasized that a recent meeting of G7 finance ministers had reaffirmed that now is not the right time to lift sanctions against Russia because Russia is profiting from the war in Iran and reaping significant gains (YouTube video, minute 46:59 and rev.com transcript).

In an interview with Euronews, Dombrovskis commented in detail on the EU’s sanctions policy toward Russia (article with video, min. 4:30 to 8). He explained that the EU should not alleviate the current ongoing energy crisis with cheap fossil fuels from Russia.

“On the contrary: We must tighten sanctions against Russia, not ease them,” Dombrovskis said on the Euronews program “Europe Today.” “Russia is profiting from the conflict in the Middle East and the rise in energy prices; it is making significant windfall profits. We shouldn’t make that any easier.”

When asked whether the EU might lift some of its sanctions on Russian oil and gas in light of high energy bills for consumers, Dombrovskis ruled that out. He said there was a “strategic decision” to further distance ourselves from Moscow.

“We already saw in 2022 that Russia used its fossil fuel supplies as a means of pressure and manipulation,” he said. “We have paid a high economic price for this dependence on Russia. There is no reason to return to that situation.”

The United Kingdom, on the other hand, has eased sanctions against Russia. The government decided that diesel and jet fuel may continue to be imported if they were produced in third countries from Russian crude oil (Frankfurter Rundschau).

Recommended reading:

EU Forecast and EU Sanctions Policy Toward Russia

- Euronews; Europe Today; Adrian Leal: EU Economic Commissioner Dombrovskis rules out easing of Russia sanctions, with video interview, May 22, 2026

- Reuters LIVE Video: EU Economic Commissioner presents economic forecasts, with comments on sanctions policy toward Russia; May 21, 2026

- Finmarket.ru: The European Commission has revised its forecast for Russian GDP growth this year upward, May 21, 2026

- European Commission: Spring 2026 Economic Forecast; Full Document; with forecast for: Russian Federation, May 21, 2026

UN Forecast

- United Nations: World Economic Situation and Prospects 2026 May Update, May 19, 2026

Forecast by the Russian government and overall economic policy

- russland.capital: Reshetnikov calls for room to lower interest rates and increase economic efficiency, May 20, 2026

- Reedus.ru; Olga Zheleznova: Reshetnikov Outlines Key Measures to Accelerate Russian Economic Growth, May 18, 2026

- RBC Interview with Economy Minister Reshetnikov; Yevgeny Kalyukov, Petr Kanaev: Interview with Maxim Reshetnikov by RBC. Key Points; May 18, 2026; Monocle.ru+; Alexey Dolzhenkov: Economic growth postponed until 2027, May 18, 2026

- Vedomosti.ru; Anna Milkina: Is the Russian economy facing a recession? Rising wages and increased government spending on the military-industrial complex and defense are no longer the drivers of GDP growth. Analysts examine these issues. May 15, 2026

- News Chronicle.ru: Rosstat reported a 0.2% decline in Russia’s GDP in the first quarter of 2026, May 15, 2026

- German-Russian Chamber of Foreign Trade: Infographics: The Ministry of Economic Development has revised its GDP forecast downward, May 14, 2026

- mec-analytics.ru; Igor Safonov: The forecast for the socioeconomic development of the Russian Federation for the period 2027–2029 has been published; May 14, 2026

- newstek.fm: Inflation and GDP forecasts for Russia in 2026 have been revised, May 12, 2026

Monetary Policy and Inflation

- Moscow Region Today; mosregtoday.ru: The Central Bank’s hands are tied: Scientists have found a way to prevent a rise in the key interest rate, May 22, 2026

- Frank Media; Mikhail Maseyev: Within a month, a second research center has proposed a change in the Central Bank’s powers. The Russian Academy of Sciences believes that the Central Bank should sometimes wait until the government has combated inflation. May 21, 2026

- Institute for Economic Forecasting of the Russian Academy of Sciences; INP RAS: “Monetary and Fiscal Policy in Russia: Specifics of Interaction,” May 21, 2026

- russland.capital: Reshetnikov calls for room to lower interest rates and increase economic efficiency, with a video statement from Central Bank President Nabiullina; May 20, 2026

Foreign Trade: Sanctions and the Ruble Exchange Rate

- Alfa Bank; Arseniy Anatolyev: The ruble exchange rate has peaked, May 22, 2026

- wallstreetONLINE; Ingo Kolf: Revenues are pouring in. Russia is benefiting massively: The secret winner of the Middle East war, May 21, 2026

- Frankfurter Rundschau; Marcel Reich: Putin’s Oil via Detours: Why London Is Backing Down on Russia Sanctions, May 21, 2026

- BANKNN:RU: The dollar exchange rate fell below 70 rubles for the first time since 2023, May 21, 2026.

- Inosmi.ru: The ruble has appreciated against the dollar more than ever before: What’s behind this? BZ: Reliable mechanisms of the Central Bank of Russia contributed to the ruble’s strengthening. May 20, 2026; Original article: Berliner Zeitung, Liudmila Kotlyarova: Ruble Gains Most Against Dollar Worldwide: What’s Behind It? The ruble lost significant value after the start of the Iran war. Now, according to Bloomberg, it is the biggest global winner against the U.S. dollar. How is that possible? May 19, 2026

- Inosmi.ru: The ruble is performing better than all other currencies: Russia benefits from the oil boom caused by the Iran war: Bloomberg original article; May 19, 2026

- Alfa Bank, Arseniy Anatolyev: The Ministry of Finance’s currency purchases were unable to stop the exchange rate from appreciating, 05/15/26

Overall economic development in Russia

- Maeil Business: Trade surplus jumps 175% in March. Market outlook optimistic despite Russia’s negative growth, May 23, 2026

- Business Insider; Huileng Tan: Despite Oil Revenues from the Iran War: Why Putin’s War Economy Is Hard to Save, May 22, 2026; Article on: Nigel Gould-Davies, Senior Fellow at the International Institute for Strategic Studies: The Coming Crisis in Russia’s Political Economy, May 19, 2026

- BankNNRU: Russian retail faces its biggest crisis in 20 years, May 22, 2026

- russland.capital: Reshetnikov calls for room to lower interest rates and increase economic efficiency, May 20, 2026

- Reedus.ru; Olga Zheleznova: Reshetnikov Outlines Key Measures to Accelerate Russian Economic Growth, May 18, 2026

- MK.ru; Dmitry Dokuchaev: Why low inflation is no cause for celebration: Analyst Goykhman explains. Inflation is falling as GDP declines: What is happening to the economy? May 17, 2026

- Merkur.de; Richard Strobl: Russia’s economic bluff is exposed: Putin boasts—but even his own ministry contradicts him, May 17, 2026

- Vedomosti.ru; Anna Milkina: Is the Russian economy heading for a recession? Rising wages and higher government spending on the military-industrial complex and defense are no longer the drivers of GDP growth. Analysts are examining these questions, May 15, 2026