The effectiveness of the sanctions against Russia remains a topic of debate

Author: Klaus Dormann

The annual growth rate of the Russian economy, which reached 4.1 and 4.3 percent in the last two years despite numerous sanctions, is projected by the International Monetary Fund to slow to just 0.9 percent this year. Are the sanctions imposed on Russia a major contributing factor?

On August 9, Prof. Christian von Soest commented on the topic of “Sanctions and Their Limits” in the podcast “Zaren.Daten.Fakten” produced by the German-Russian Chamber of Foreign Trade. On August 14, Russia expert Elina Ribakova was interviewed for the “The Economics Show” podcast of the London-based “Financial Times” on the effectiveness of the sanctions and the current state of the Russian economy (“Why Russia’s wartime economy is starting to crack”).

Elina Ribakova had already expressed great skepticism about the growth potential of the Russian economy in earlier studies. Heli Simola, Senior Economist at the BOFIT research institute of the Bank of Finland, also noted in a recent blog post that the IMF currently assigns Russia one of the lowest long-term growth forecasts in the world, at just around 1 percent. The Russian Central Bank already considers a decline in growth to just 1 percent possible this year. The Institute for Economic Research at the Russian Academy of Sciences estimates that, on a seasonally adjusted basis, real gross domestic product fell in June to the level of October 2024.

Prof. von Soest: The sanctions are “a millstone around Russia’s neck”

Professor Dr. Christian von Soest is “Head of Policy Advisory and Berlin Office” at the Hamburg-based “German Institute for Global and Area Studies (GIGA).” He is the author of the book published in 2023 “Sanctions: A Powerful Weapon or a Helpless Maneuver?”, which was also included in the publication series of the Federal Agency for Civic Education (excerpt).

In a podcast by the German-Russian Chamber of Foreign Trade, Von Soest summarized his assessment of the effectiveness of Western sanctions in a conversation with Thomas Baier as follows:

We see how difficult it is for the West to influence an authoritarian regime like the Russian government through economic sanctions.

Russia has developed sophisticated strategies for its oil exports to circumvent Western sanctions by supplying countries—such as China or India—that do not join the coalition of sanctioning states. However, Russia often has to accept lower prices for these oil exports to so-called “third countries.”

In addition, the sanctions often increase Russia’s “transaction costs” when importing high-tech products. Due to the sanctions, it has become much more difficult for Russia to obtain technological components, and their costs have risen for Russia.

With the EU’s 18th sanctions package, the sanctions are indeed being significantly expanded and tightened. Among other things, it is now possible to sanction financial institutions in China and Turkey. However, it is “highly questionable” whether the effectiveness of the so-called “oil price cap” set by the EU—which is to be lowered from $60 to around $47.60 with the 18th EU sanctions package, is, however, “highly questionable” overall, partly because the EU is dependent on U.S. cooperation in this regard. The implementation of the tariff increases envisaged by U.S. President Trump against China and India to sanction their oil imports from Russia also does not appear realistic.

For Russia, China has become a “hub” for technology imports, partly due to China’s technological rise. Completely cutting Russia off from technology and international financial services is now impossible, partly because the importance of Western suppliers to Russia has significantly diminished.

Overall, Western sanctions are making life more expensive and difficult for Russia. For Russia, Western sanctions are “a millstone around its neck.” However, the impact of the sanctions should not be overestimated. While they are a burden on Russia’s “war machine,” However, the sanctions can only be part of the West’s response to Russia’s attack on Ukraine—alongside arms deliveries to Ukraine and financial support.

Ribakova: Sanctions are weighing on Russia’s growth potential

Elina Ribakova is, among other things, a “non-resident fellow” at the Brussels-based Bruegel Institute and the Washington-based “Peterson Institute for International Economics (PIIE).” Since 2023, she has also served as “Director of the International Program” at the Kyiv “School of Economics.”

In the spring of 2023, Ribakova argued in a publication by the Peterson Institute that sanctions are undermining Russia’s growth potential (“Sanctions against Russia will worsen its already poor economic prospects”). The sanctions made it significantly more expensive and difficult for Russia to obtain supplies. They would therefore also contribute to a slowdown in Russia’s economy.

However, in the summary of a detailed study published in September 2024, which she co-authored with Oleg Itskhoki (Harvard University), it is noted that the impact of the sanctions on the Russian economy is “mixed” despite their unprecedented scope. Official Russian statistics reported only a moderate “contraction”:

“Despite the unprecedented scope and scale of these sanctions, their impact on Russia’s economy has been mixed, with only moderate contraction reported by official Russian statistics” (PDF: Brookings Papers on Economic Activity: “The Economics of Sanctions: From Theory Into Practice,” Brookings Institution press release).

Ribakova on the FT podcast: Financial sanctions were the most effective

In the Financial Times podcast, Ribakova recently answered questions from “Economics Editor” Sam Fleming (“Why Russia’s wartime economy is starting to crack”). She commented primarily on the effectiveness of the sanctions imposed on Russia and on Russia’s economic cooperation with China. Below is a summary of some of Ribakova’s assessments in response to questions from the Financial Times.

Question: Which sanctions have been most effective and which least?

Ribakova: The sanctions imposed on Russia can be broadly divided into three categories.

First, there are sanctions against the Russian financial sector. However, access to the U.S. financial market is also very important for Russia. The U.S. dollar and the international payment systems based in the U.S. are of central global importance. That is why, when it comes to financial sanctions, the U.S. is in the strongest position to impose high costs on another country and weaken another economy.

Second, there are sanctions in the oil and gas sector, such as the price cap on Russian oil exports.

Third, there are controls in international trade that are essentially intended to prevent Russia from gaining access to modern military technology.

So far, sanctions in the financial sector have been the most effective, as the U.S. in particular has experience with them and knows how to enforce them. In the other two areas of sanctions—the oil price cap and export controls—there is, however, little experience. This is a key reason why Russia has been so successful in converting its economy to a war economy.

Setting a price cap on Russia’s oil exports pursues a dual objective that is very difficult to achieve. On the one hand, the aim is to keep Russian oil on the world market (to prevent a sharp rise in the world market price); on the other hand, the price cap on Russian oil is intended to simultaneously reduce Russian revenues from oil exports.

Question: Does the partnership with China alleviate the pressure of sanctions on Russia?

Ribakova: China dominates the partnership between Russia and China. For Russia, China is the largest trading partner and a crucial “pioneer.” For China, however, Europe and the U.S. are the most important export markets. Less than 4 percent of China’s foreign investments go to Russia (see also: Heli Simola, BOFIT Bank of Finland: Russia’s ever-increasing economic dependence on China).

The increase in Russia’s imports from China has two important consequences.

First, by providing cheaper access to Chinese consumer goods and cars, China enables the Russian economy to transition to a “war economy.” Put simply: If people in Russia can buy cheap cars from China, Russian automakers gain the opportunity to repair military vehicles. Imports from China give the Russian economy the leeway to transition to a war economy.

The second very important aspect is that Russia can circumvent trade sanctions through imports from China. For example, foreign components for the construction of Russian ballistic missiles reach Russia via China. Nearly 90 percent of the “circumventions” of sanctioned exports to Russia involve shipments from China in one way or another. Because Russia cannot produce more technically sophisticated products for its military domestically, this is of crucial importance.

Question: Was the recovery of Russian economic growth in 2023 and 2024 at rates of just over 4 percent to be expected?

Ribakova: I don’t think the recovery came as a complete surprise. Russia dominates the energy markets—that is, the markets for oil and gas as well as some other products. That is why we were a bit too hesitant when imposing sanctions. As a result, Russia benefited disproportionately from high commodity prices and its sustained high revenues from oil and gas exports. It then invested this money in the domestic economy, particularly in the war economy.

Question: How is the Russian economy performing right now?

Ribakova: The current downturn in the Russian economy, which we have been observing for the past six months, has been a long time coming. Russia faces the problem that its economy is struggling on the supply side of production factors. At some point, production capacity is simply exhausted; there is a shortage of labor, investment, and capital.

That is why we have seen such a sharp rise in inflation. According to official figures, the unemployment rate has fallen to around 2 percent. However, this rate is completely unrealistic for an emerging economy the size of Russia with structural problems.

Growth in the Russian economy has been driven primarily by production in defense-oriented sectors. Many companies in the military-industrial complex also continue to receive interest subsidies.

The problem is that the Central Bank’s interest rate policy is likely to have the greatest impact on sectors focused on manufacturing products for the civilian economy. These sectors have not performed particularly well over the past three years. The Central Bank must therefore cut interest rates significantly.

Currently, even the military-industrial complex is beginning to shrink, partly due to interest rates, but also due to labor shortages and a lack of investment funds. We already saw signs of this toward the end of 2024.

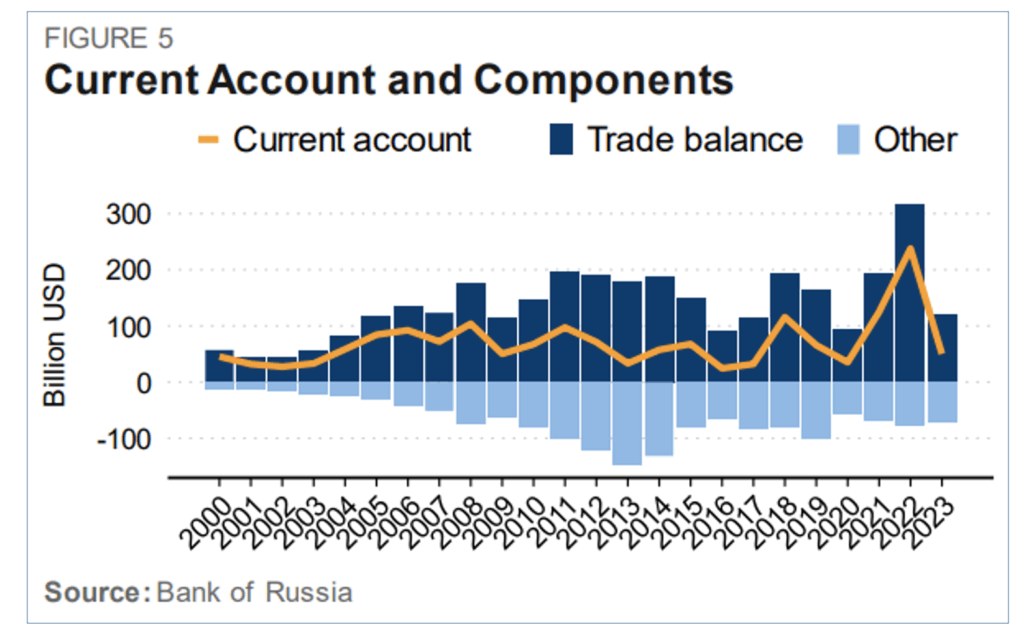

How much Russia’s current account surplus rose—and then fell—in 2022

Ribakova noted on the Financial Times podcast that Russia benefited from sharply rising commodity prices after the start of the war in Ukraine:

“Looking at Russia’s current account surplus in 2022, Russia took in more than $230 billion in just one year. Russia thus recouped the losses from the freezing of its foreign exchange reserves in just one year.”

This sharp increase in Russia’s current account surplus in 2022 is shown by the orange line in the following figure published by Elina Ribakova in the “Brookings Papers.”

Russia’s current account surplus and its components, in billions of dollars

Oleg Itskhoki, Elina Ribakova: The Economics of Sanctions: From Theory Into Practice; Brookings Papers on Economic Activity, September 25, 2024

Since 2022, Russia’s current account surplus has fallen sharply. According to the Russian Central Bank, it dropped to $7.3 billion in the second quarter of 2025, the lowest level since 2020. Compared to the second quarter of 2022 ($77.2 billion), the surplus decreased by approximately 91 percent (TradingEconomics; for the trade surplus, see BOFIT Weekly).

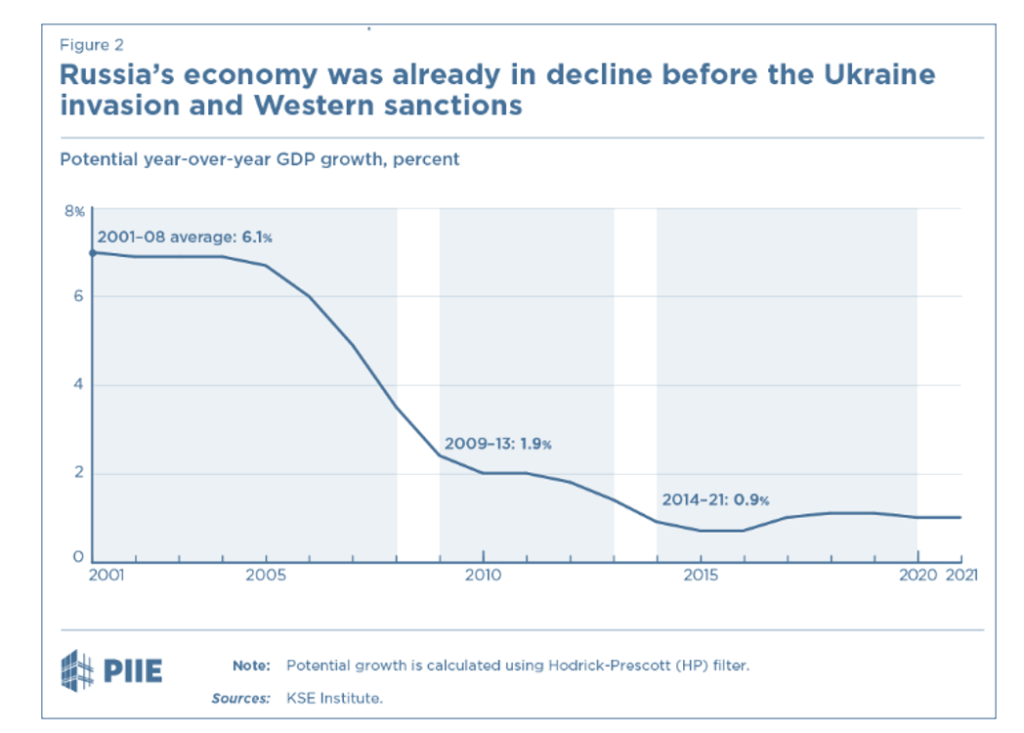

How low Ribakova estimates Russia’s growth potential

In her study published by the Peterson Institute in April 2023, Ribakova used a figure to point out that, according to the Kyiv School of Economics, the Russian economy’s growth potential had already fallen to just under 1 percent in 2014. “Russia’s economy was already in decline before the invasion of Ukraine and Western sanctions” is the caption of the following figure.

Annual growth potential of the Russian economy in percent

Elina Ribakova (PIIE): Sanctions against Russia will worsen its already poor economic prospects, April 19, 2023

Regarding the growth prospects of the Russian economy, Ribakova noted in her study that, in the medium term, Russia will continue to suffer from its weak growth potential. The sanctions alone would not “knock Russia down,” but they could block its access to high-tech applications, including for the military, and erode Russia’s growth potential. Russia’s already existing prospects of chronically low investment, weak productivity growth, and a labor shortage would be cemented by the sanctions:

“Over the medium term, Russia will continue to suffer from weak potential growth. Sanctions alone will not defeat Russia, but they can cut off access to high-tech inputs, including for the military, and erode Russia’s potential growth. Sanctions will deepen the preexisting fault lines in Russia’s outlook of chronic underinvestment, poor productivity growth, and labor shortages.”

BOFIT also estimates Russia’s growth potential at only around 1 percent

Heli Simola, “Senior Economist” at the BOFIT research institute of the Bank of Finland, expressed similar skepticism to Ribakova regarding the long-term growth prospects of the Russian economy in May 2025 on the “BOFIT Blog.” Simola writes:

“Between 2015 and 2019, Russia’s average GDP growth was merely 1 percent per year, and long-term growth potential was generally estimated at around 1.5 percent per year (BOFIT Policy Brief).

The Russian economy faces numerous structural challenges, including unfavorable demographic trends, a lack of investment, and weak productivity growth. The war and the resulting sanctions against the Russian economy have exacerbated these problems and further weakened Russia’s growth potential.”

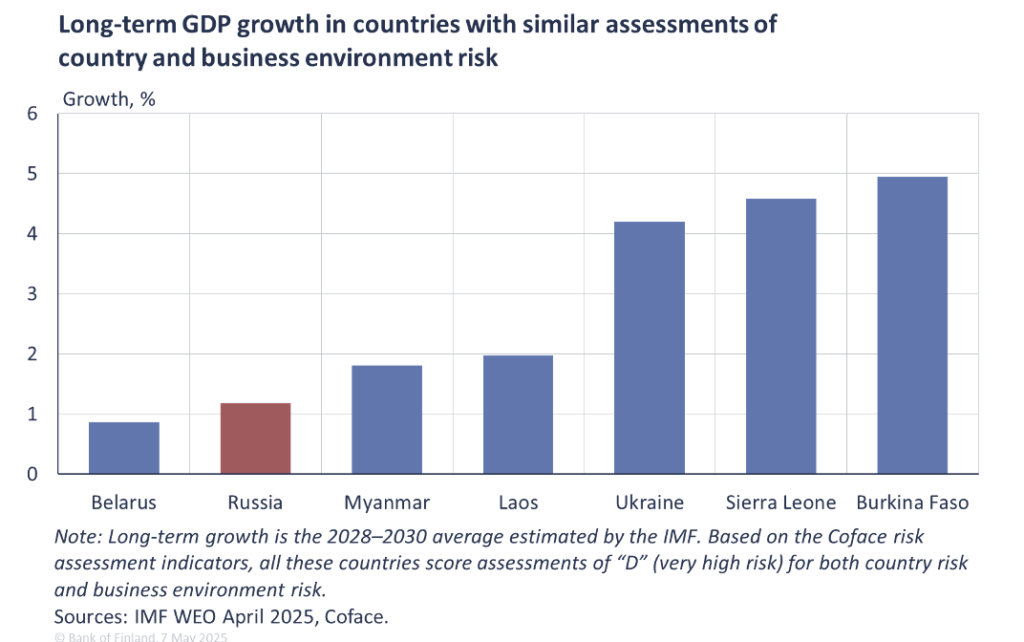

Simola has determined the average annual growth rate the IMF expects for Russia from 2028 to 2030 in its April 2025 “World Economic Outlook.” In the following figure, she compares this rate of just over one percent with the IMF’s growth forecasts for countries that, like Russia, have been classified by the rating agency Coface as “very high risk.”

Long-term growth rates of Russia and comparable countries; IMF estimates for average annual growth from 2028 to 2030

Heli Simola; BOFIT, Bank of Finland:

War has degraded Russia’s long-term economic outlook and business environment

As a result of this comparison, Simola notes:

“Russia currently has one of the world’s lowest projected long-term growth rates and a high country risk. Only Belarus exhibits a similarly poor combination of growth and risk.”

How calmly Russia’s central bank is commenting on current developments

On August 21, Andrey Gangan, Director of the Monetary Policy Department at the Russian Central Bank, also addressed the issue of labor shortages and the low growth in labor productivity in the Russian economy in an interview with the government newspaper “Rossiiskaya Gazeta.” Regarding the current state of the Russian economy, he noted that following the overheating of the past two years, the economy continues to move toward balanced growth rates. According to TASS, Gangan expects the following:

“Overall, the economy will continue to grow this year and next. Preliminary data on GDP growth for the first quarter of 2025 stands at 1.4% and for the second at 1.1%, with a forecast of 1 to 2% for the full year. The situation is developing in line with our expectations, although the Ministry of Economic Development’s spring forecast was slightly higher at 2.5%.”

Gangan noted that the Russian economy had grown by a solid 4 percent in each of the past two years, outpacing the global economy. At the same time, he emphasized that the Russian economy has now exhausted nearly all available production capacity, logistics capabilities, and infrastructure. Regarding the labor shortage, he explained:

“It is now difficult to find new workers. We need… new approaches to increase labor productivity. Otherwise, all wage growth will inevitably be eroded by inflation, and the working population will ultimately gain nothing.”

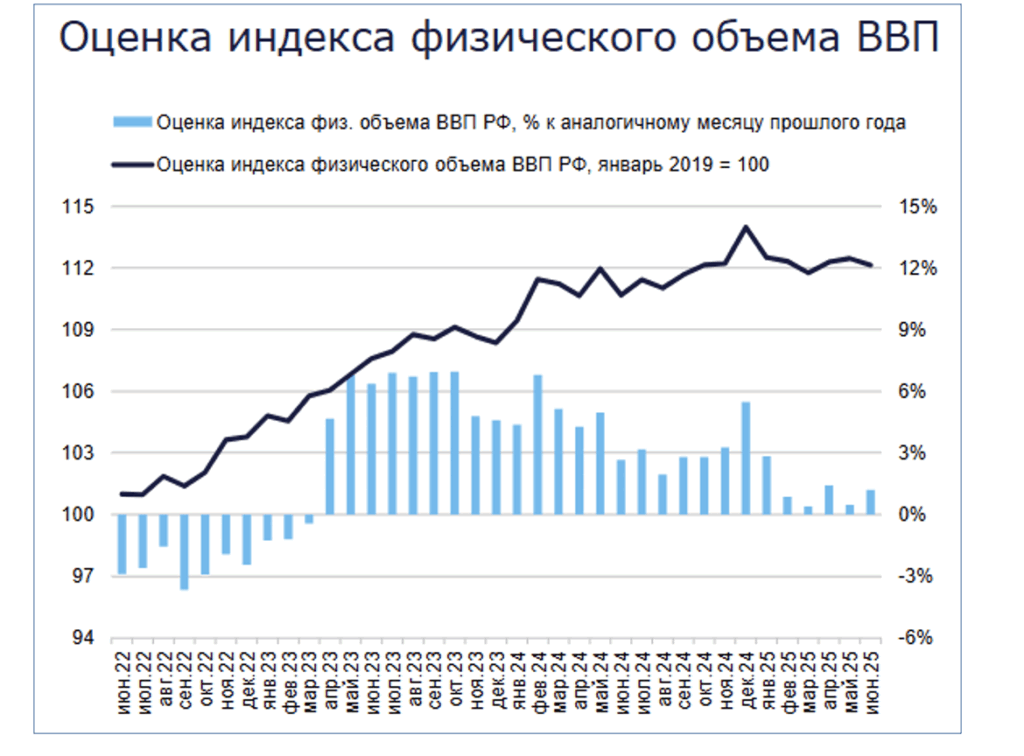

Economic Research Institute of the Russian Academy of Sciences:

In June, GDP fell to the level of October 2024

The Institute for Economic Forecasting of the Russian Academy of Sciences (IEF RAS) illustrated the current trend in aggregate economic output in Russia in its June economic report dated August 13 with the following figure:

Estimate of the real gross domestic product index (January 2019=100)

Blue bars: Year-over-year changes in percent

Institute for Economic Forecasting of the Russian Academy of Sciences:

Short-term analysis of GDP trends – August 2025, August 13, 2025

The Institute comments on the development of the real gross domestic product index (black line) as follows:

Calculations based on statistical data available in early August show that real gross domestic product in June 2025 fell by 0.3 percent on a seasonally adjusted basis compared to May 2025.

Over the course of the entire first half of the year, the estimated monthly GDP rose on a seasonally adjusted basis only in April and May compared to the respective previous month.

Economic output in June, on a seasonally adjusted basis, corresponds to the level of October 2024. It is 1.6% lower than in December 2024.

Prof. Dr. Alexander Libman (Head of the Politics Department at the Institute for Eastern European Studies at FU Berlin) describes Russia’s economy as being in a state of “stagflation” in the latest issue of “Zaren. Daten. Fakten.”

Recommended reading:

- Elina Ribakova (Senior Fellow at the Peterson Institute for International Economics, Bruegel Fellow, Vice President for Foreign Policy at the Kyiv School of Economics) with Sam Fleming on the Financial Times podcast “The Economics Show”: Why Russia’s wartime economy is starting to crack; with transcript; 08/18/25

- Bruegel; Benjamin Hilgenstock, Elina Ribakova: Why Russia’s economic model no longer delivers. A contracting economy and low oil prices are signs of potential constraints on Russia’s ability to maintain its military capabilities, July 16, 2025; Peterson Institute for International Economics; Benjamin Hilgenstock (KSE Institute) and Elina Ribakova (PIIE): Why Russia’s economic model no longer delivers, July 16, 2025

- Russia.capital: Trade volume between Russia and China continues to decline, Aug. 20, 2025

- Kommersant, Artem Chugunov: Economists analyze GDP trends, 08/18/25

- Deutschlandfunk, Katja Scherer: The Russian economy is more resilient than expected, audio, 3 min., Aug. 18, 2025

- CNN; Lauren Kent: The US and Europe are still doing billions of dollars’ worth of business with Russia despite years of war, 08/15/25

- DW.com/ru; Oleg Loginov: Russia’s economy: From war euphoria to the threat of recession, Aug. 15, 2025

- Vedomosti: CNN: New sanctions against Russia will “hit the American economy with a sledgehammer,” Aug. 6, 2025

- The Conversation; Keith A. Preble (East Carolina University), Charmaine N. Willis (Old Dominion University): Sanctioning ghosts: Why US plans to hit Russia with fresh economic penalties will have little effect, July 29, 2025

- DW.com/ru.; Olga Lebedeva: The Kremlin has “taken note” of Trump’s ultimatum, July 29, 2025

- New York Post; Gregory W. Slayton, Opinion: Trump can apply real pressure on Russia’s collapsing economy, July 28, 2025

- Finam.ru; Olga Belenkaya: Trump’s new tariffs will slow global economic growth, July 28, 2025

- Harvard Kennedy School, Belfer Center: Russia Matters; Robin Brooks and Ben Harris, Brookings: Secondary Tariffs or Tighter Sanctions? Strategies to End Russia’s War in Ukraine, July 25, 2025

- Infosperber; Markus Mugglin: Why the Russia Sanctions Won’t Stop the War, The sanctions do cause damage. But they also stimulate Russia’s economy, July 24, 2025