The Druzhba Pipeline – once a symbol of friendship, now a source of contention

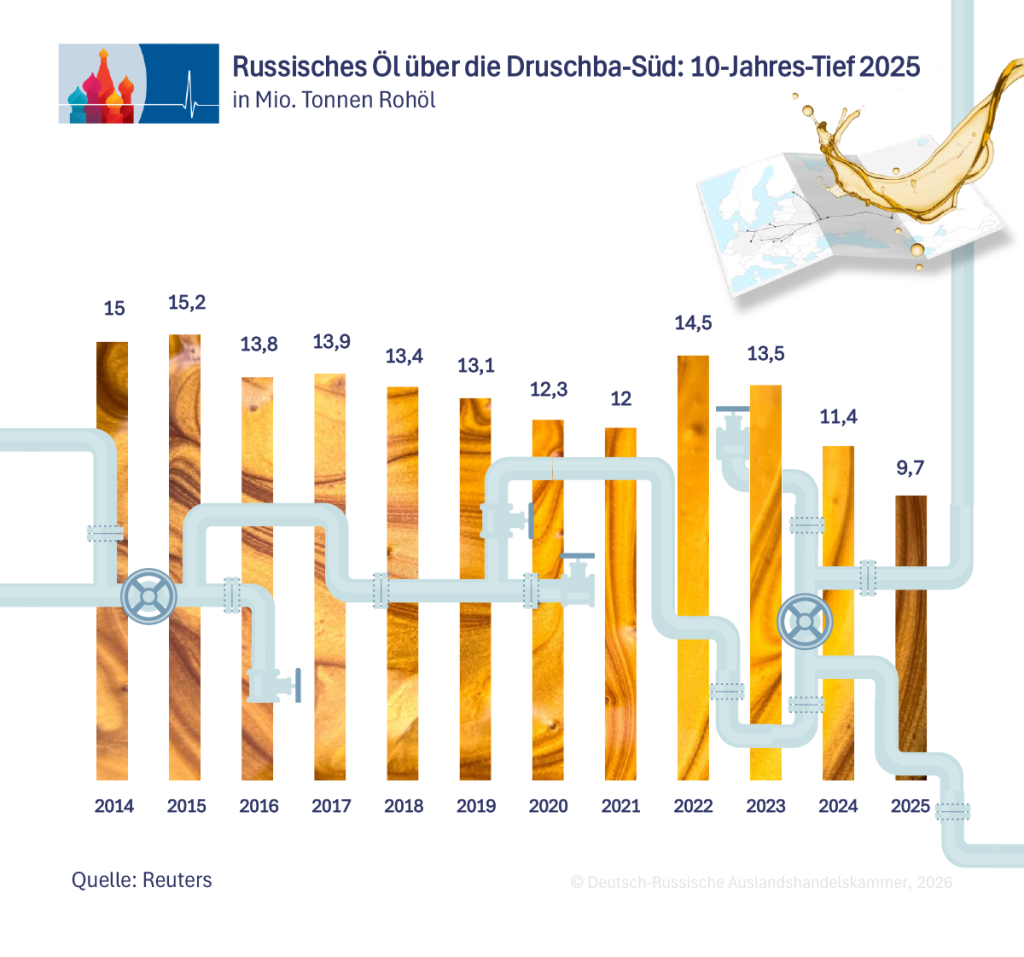

Sixty-two years after it went into operation, the Druzhba pipeline is at a turning point—and may be on the verge of closure. The suspension of Kazakh oil transit to the Petrochemisches Kombinat (PCK) Schwedt refinery in the eastern German state of Brandenburg as of May 1, the Ukrainian drone attacks on the Druzhba pipeline in 2025 and 2026, and the EU phase-out legislation planned for late 2027 have reduced what was once the most important export system for Russian crude oil to Europe to a skeleton operation. Deliveries to Hungary and Slovakia totaled 9.25 million tons in 2025, with a market value of over 3.5 billion euros. This represents a drop of about two-thirds, reports the Qatari news channel Al Jazeera. A calculation by the Finnish Centre for Research on Energy and Clean Air (CREA) shows that the southern Druzhba pipeline now accounts for only 2 to 3% of Russia’s oil revenues.

Origins as a Soviet Prestige Project

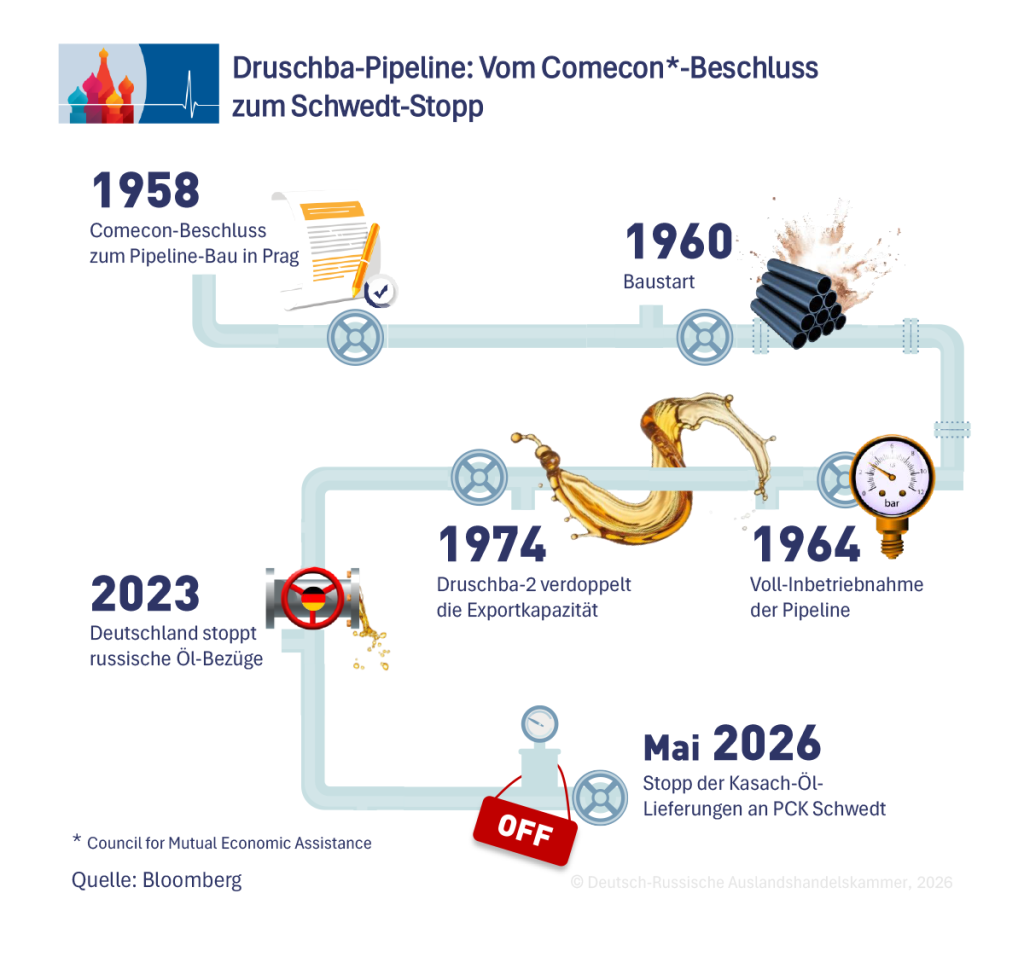

The political origins of the pipeline lay in Prague. On December 18, 1958, the Council for Mutual Economic Assistance (COMECON) of the socialist states in Europe decided to build an international crude oil pipeline because rail transport could no longer meet Eastern Europe’s rising oil demand. Construction began on December 10, 1960, in the Carpathian Mountains. Pipes were manufactured in the Soviet Union and Poland, fittings came from Czechoslovakia, pumps from the GDR, and automation technology from Hungary.

Commissioning took place in stages. In 1962, the oil reached Bratislava in what was then Czechoslovakia; in September 1963, Hungary; in November 1963, Poland; and in December 1963, the GDR. On October 15, 1964, the Soviet leadership inaugurated the entire system; on November 4, 1964, regular oil transport from the Volga region began. According to contemporary estimates, construction cost around 400 million rubles. At the official Soviet exchange rate of 0.90 rubles per U.S. dollar, 400 million rubles equaled approximately 444 million U.S. dollars. The exchange rate was set politically by the State Bank; the ruble was not convertible and was worth considerably less on black markets. Estimates by the U.S. Central Intelligence Agency (CIA) put the Soviet gross domestic product in 1964 at about 250 billion rubles—meaning the pipeline cost 0.16% of annual economic output. A total of 730,000 tons of steel pipe were laid. The total length of the pipeline system is 8,900 km. The hydraulic capacity is 1.2 to 1.4 million barrels per day, or 60 to 70 million tons per year. On the Belarusian-Polish section, up to 80 million tons were transported. The Russian news agency TASS cites a maximum annual volume of around 100 million tons for the entire branched network.

The mega-pipeline begins in Almetyevsk in the Muslim republic of Tatarstan. From there, crude oil is collected from Western Siberia, the Volga-Ural region, and the Caspian region. The pipeline first runs to Mosyr in Belarus, where it splits. The northern branch runs through Poland to Schwedt: the total length to Germany is 5,327 km. The southern branch runs via Brody and Uzhhorod in Ukraine to Hungary, Slovakia, and the Czech Republic.

Seven national operators

With the collapse of the Soviet Union in 1991, centralized control also came to an end. Afterward, seven national operators were responsible for the pipeline system: Transneft Druzhba in Russia, Gomeltransneft Druzhba in Belarus, Ukrtransnafta in Ukraine, PERN in Poland, Transpetrol in Slovakia, Mero ČR in the Czech Republic, and MOL in Hungary.

Within the 67,000-km-long Transneft network, Druzhba is now just one route among many. Transneft is the Russian state-owned monopoly for crude oil and petroleum product pipelines. It was founded in 1993 from the Soviet Ministry of Oil Pipeline Construction. Nikolai Tokarev has been the CEO since 2007. According to Transneft’s latest figures from late March 2025, revenue rose by 1.2% to 1.44 trillion rubles, equivalent to 16.3 billion euros. Net profit, however, plummeted by 19.6% to 226 billion rubles, or approximately 2.6 billion euros.

The main reason for the drop in profits is the rising tax burden. Since January 1, 2025, Transneft has been paying a 40% profit tax, effective until the end of 2030. Added to this are the consequences of sanctions, declining cargo throughput, and the Central Bank’s high key interest rate, according to an analysis by the Russian business newspaper Kommersant.

Operationally, the group remained close to the previous year’s levels. In 2024, Transneft transported 447 million tons of crude oil, of which 435 million tons were Russian and 12 million tons were Kazakh. For 2025, CEO Nikolai Tokarev expected a slight decline in pumping volume; for the KTK pipeline (Caspian Pipeline Consortium), he projected 74.4 million tons of export oil (TASS). The 1,510-km-long pipeline runs from the major Kazakh fields of Tengiz and Karachaganak through southern Russia to the Black Sea terminal near Novorossiysk and is the most important export route for Kazakh oil to the world market. In 2026, the volume is expected to remain at the 2025 level.

Druzhba after the embargo: From mainline to special case

With Regulation 2022/879 amending Regulation 833/2014, in force since June 4, 2022, the European Union imposed an embargo on Russian crude oil transported by sea effective December 5, 2022. Pipeline deliveries via Druzhba were permitted in Article 3 as an indefinite exception for the landlocked countries Hungary, Slovakia, and the Czech Republic—until the Council “decides otherwise.” The 11th sanctions package later explicitly blocked the legal possibility of importing Russian pipeline oil to Germany and Poland.

In April 2025, the Czech Republic became the third country to end supplies via Druzhba after the Transalpine Pipeline Plus project was completed. With an investment of 1.6 billion Czech korunas, approximately 65 million euros, fully financed by the state-owned pipeline operator Mero ČR, the country doubled the capacity of the Transalpine Pipeline from Trieste through Bavaria to 8 million tons per year. Prime Minister Petr Fiala stated on April 17, 2025: “We have taken another step toward our energy independence.” The first shipment was Norwegian Johan Sverdrup crude oil, according to a report by the energy analysis platform Grosswald.

Druzhba’s Last EU Customers

Originally, Druzhba supplied six countries directly: Belarus via the Mosyr refinery, Poland via Płock and the connection to Schwedt, Germany via Schwedt and historically Leuna, the Czech Republic via the Litvínov and Kralupy refineries, Slovakia via Bratislava, and Hungary via Százhalombatta.

Germany has not processed Russian oil since January 2023, but continued to receive Kazakh crude oil via the Druzhba system until April 2026.

The Polish state-owned company Orlen terminated the last relevant Druzhba contract in February 2023. Since then, Warsaw has stopped using Russian pipeline oil. The Polish section of the Druzhba pipeline remains technically operational but is now used only for the transit of Kazakh oil to the Schwedt region and for reverse logistics from the port of Gdansk.

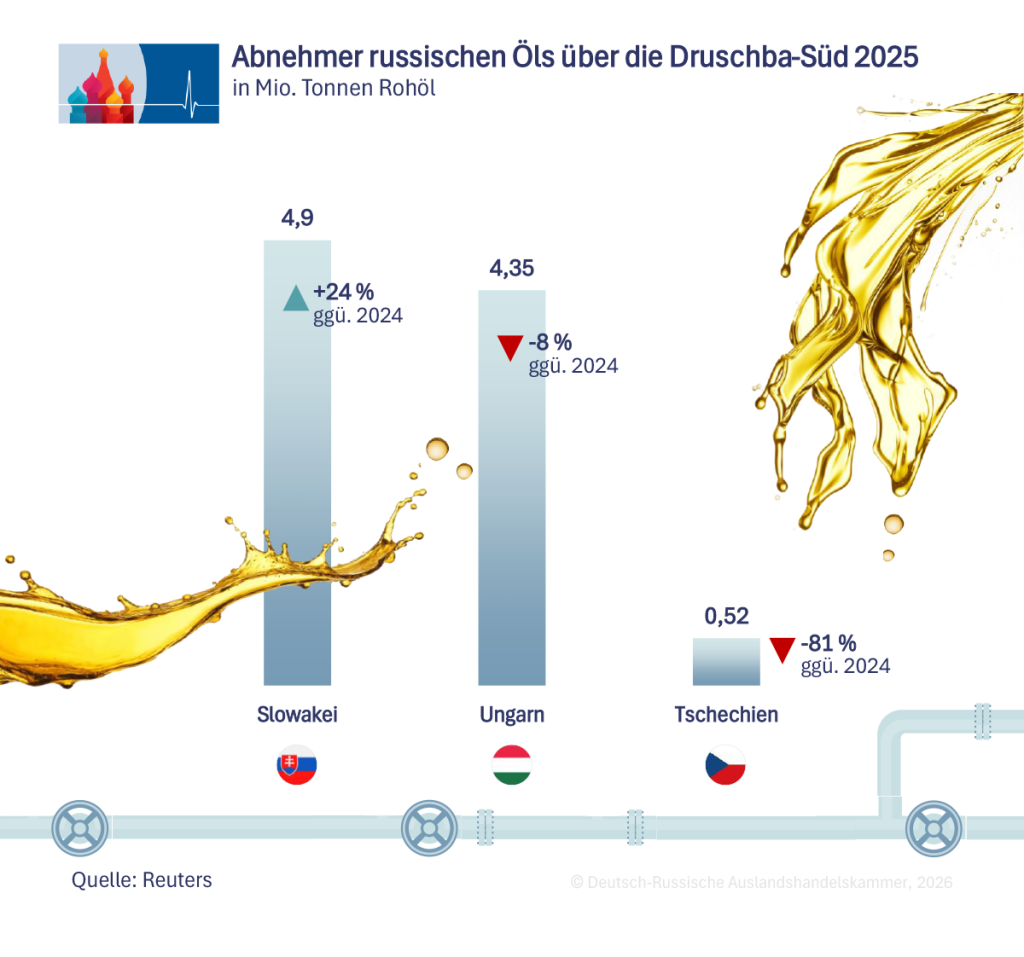

According to calculations by the Finnish institute CREA, Druzhba deliveries to Hungary and Slovakia generated oil sales worth 13 billion euros for Russia between February 2022 and December 2024. Of this amount, approximately 5.4 billion euros flowed directly into the state budget as tax revenue. In August 2025, the five largest EU importers of Russian fossil fuels paid a total of 979 million euros to Russia—Hungary 416 million euros (of which 176 million euros was crude oil), Slovakia 276 million euros (of which 204 million euros was crude oil).

Schwedt after May 1

Germany’s special position in the Druzhba system hinges on a single location: the Schwedt Petrochemical Complex (PCK). The refinery, with a capacity of around 12 million tons per year, supplies approximately 90% of the Berlin-Brandenburg fuel market. Since January 2023, Schwedt has no longer processed Russian oil. Supplies will then come via the Port of Rostock, with an annual capacity of 7 million tons, the Polish port of Gdansk, and via Kazakh oil, which the pipeline company KazTransOil transported to Germany through the Druzhba system. In 2025, Astana supplied 2.15 million tons—44% more than in 2024 and about 17% of the total volume.

About 1,200 people work directly at the refinery, with thousands more employed in regional petrochemical logistics. On December 23, 2025, the Federal Ministry of Finance and the Federal Ministry of Economics extended the job security program for PCK employees until June 30, 2026—part of the “Future Package” for East German refinery sites launched in September 2022. Federal Finance Minister Lars Klingbeil assured: “The people of the Uckermark can rely on the federal government.” Economy Minister Reiche will visit the site on May 11, 2026; until then, State Secretary for Energy Frank Wetzel will negotiate with Warsaw regarding additional supplies from Gdansk.

The majority shares of Rosneft Deutschland GmbH and RN Refining & Marketing GmbH have been under the trusteeship of the Federal Network Agency since September 2022. On April 22, 2026, Russian Deputy Prime Minister Alexander Novak announced that Russia would halt the transit of Kazakh crude oil via Druzhba to Germany as of May 1, 2026—officially citing “technical capacities.” Brandenburg’s Minister-President Dietmar Woidke stated that PCK could weather May with reserves and an operating capacity of around 80%. Federal Minister of Economics Katherina Reiche is quoted in the Handelsblatt. She “assumes that production in Schwedt will continue.”

Expiration of the EU exemption by 2027

The political end of the Druschba special regulation has begun. The European Commission had initially announced the submission of legislation to phase out Russian oil imports for April 15, 2026—three days after the Hungarian elections. Due to the Iran crisis and the drone dispute, the deadline was postponed to March 2026; no new date has been set.

EU Energy Commissioner Dan Jørgensen stated on December 3, 2025: “We must end the purchase of Russian oil as soon as possible, by the end of 2027 at the latest.”

Three scenarios are plausible for the future of Druzhba oil deliveries.

First, the orderly phase-out of Russian oil supplies by the end of 2027. A key factor for this is the Adriatic Pipeline. It runs from the Croatian deep-sea port of Omišalj on the island of Krk through Croatia to Hungary and Slovakia, reaching the same refineries there (Százhalombatta near Budapest, Slovnaft in Bratislava) that currently process Russian Druzhba oil. The Hungarian state-owned oil company MOL and the Croatian oil supplier Janaf began another ten-month series of stress tests on March 11, 2026, after tests in September 2025 had failed, reported the industry service Ceenenergynews. JANAF cites an annual capacity of 11 to 15 million tons; MOL has never transported more than 2.2 million tons to date. According to the company, 14 million tons per year (40,000 tons per day) would be required to fully supply both MOL refineries. If JANAF can demonstrate the required 14 million tons per year in the ongoing stress tests, a faster Hungarian phase-out of Russian oil supplies under newly elected Prime Minister Peter Magyar is to be expected. Hungary could do without Russian oil as early as 2026 or early 2027, rather than waiting until the end of 2027.

Second, the Druzhba pipeline could be damaged by drone attacks to such an extent that operations come to a standstill before the end of 2027.

Third, a peace scenario involving a political solution for the pipeline. Theoretically, the Druzhba pipeline could be used to reactivate the Schwedt facility with Russian oil. The likelihood of this is considered low.

This article first appeared in the exclusive newsletter of the German-Russian Chamber of Foreign Trade