Slump in Russian economic growth

Author: Klaus Dormann

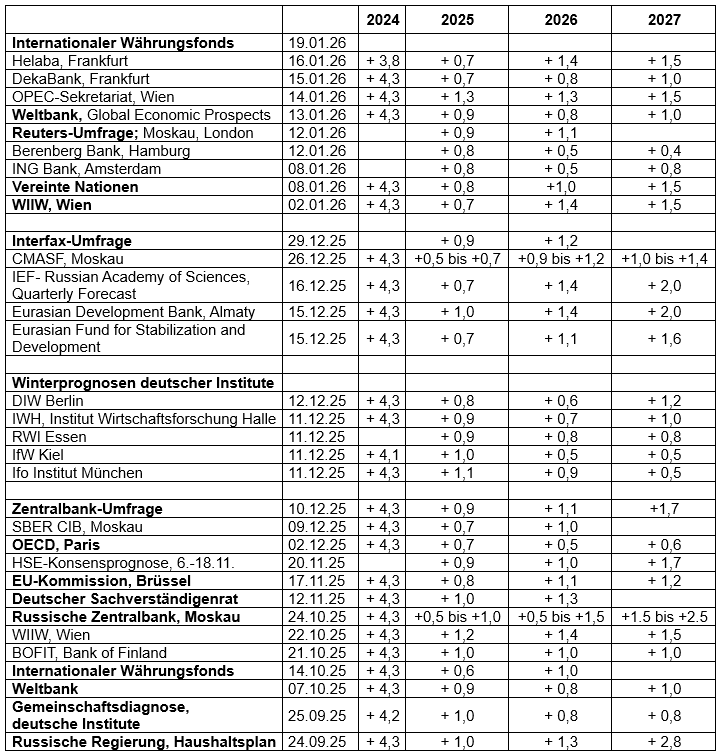

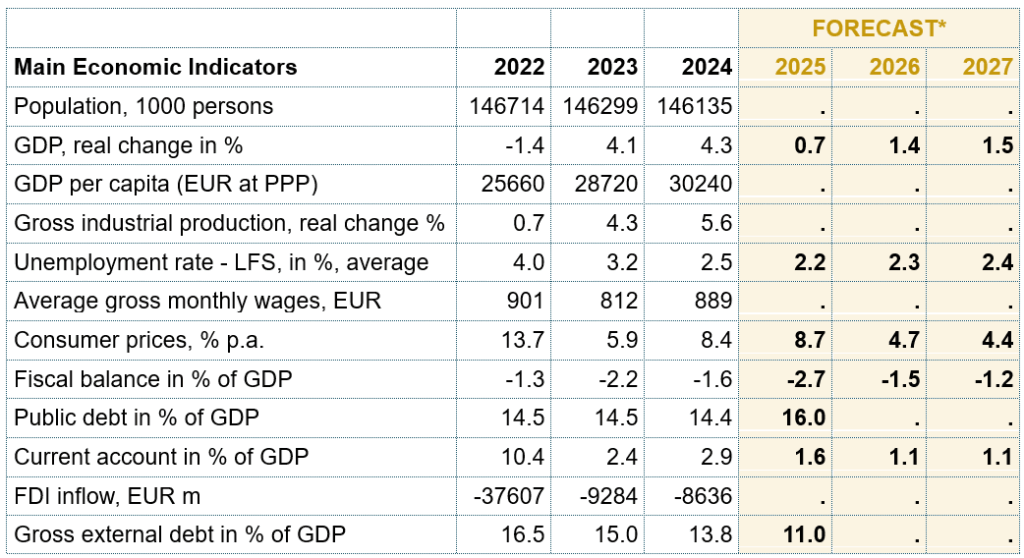

On January 19, the International Monetary Fund will publish an update to its “World Economic Outlook.” In mid-October, in the “Autumn Edition” of the World Economic Outlook, it had lowered its forecast for Russian economic growth in 2025 to just 0.6 percent. At the time, few observers expected Russia’s growth rate to fall quite that low. The World Bank’s slightly higher forecast had already found more support in the fall. In early October, in its “Country Report on Russia” within the “Macro Poverty Outlook,” the World Bank estimated real gross domestic product growth in Russia in 2025 at 0.9 percent—following a much stronger increase of 4.3 percent in 2024.

Nothing has changed in this regard over the past three months. Last week, in its “Global Economic Prospects,” the World Bank again forecast that the Russian economy is likely to have grown by 0.9 percent in 2025. Most analysts continue to expect the same. In surveys published by the news agencies Reuters and Interfax at the turn of the year, they also anticipated an average economic growth rate of 0.9 percent in Russia for 2025.

Whether growth will pick up somewhat as early as 2026 is a matter of debate

The analysts surveyed by the agencies expect a slight pickup in Russian economic growth in the new year, averaging 1.1 percent (Reuters) and 1.2 percent (Interfax). The World Bank, on the other hand, continues to expect Russia’s economy to slow slightly further to 0.8 percent in 2026. In contrast, the United Nations Department of Economic and Social Affairs anticipates that Russia’s economic growth will pick up this year from 0.8 percent to 1.0 percent.

GDP Forecasts 2024–2027

Year-over-year change in real gross domestic product, in percent

World Bank: Economic growth stabilizes at just 0.9 percent

In its “Global Economic Prospects” report, the World Bank provides only a few brief references to economic developments in Russia.

According to the World Bank, the expected sharp decline in economic growth to just 0.9 percent in 2025 is attributable to “restrictive monetary policy” and high inflation. The downward revision of its growth forecast from 1.4 percent in its June forecast to 0.9 percent reflects the fact that households and businesses took out fewer loans than expected due to high interest rates.

According to the World Bank, private consumption and investment in Russia are expected to weaken due to the tight financial situation and reduced government support. However, the World Bank expects economic growth to stabilize over the next two years and reach an average of 0.9 percent in 2026/27, as in 2025.

The World Bank assumes that lower oil prices, new sanctions, and a stronger ruble will have further constrained Russia’s exports and government revenues in 2025. It also points to the decision by some EU countries to reduce energy imports from Russia. According to the World Bank’s assessment, Russia’s current account surplus is likely to remain small due to lower oil prices and the reduction in oil production under OPEC+ quotas. The Russian budget deficit is expected to remain high due to lower export revenues.

UN Economic Department: Growth will not pick up to 1.5 percent until 2027

The United Nations Economic Department expects Russia to see

and 2026, similar to the World Bank’s forecast, with economic growth of just under one percent. In 2027, it anticipates a slight uptick in growth to 1.5 percent, though it does not provide further justification for this assessment. The UN Department summarizes the economic outlook for 2025 and 2026 as follows:

The economy of the Russian Federation is projected to have grown by 0.8 percent in 2025. Economic activity gradually lost momentum over the course of the year. The impact of previous growth drivers—including extensive investments in the military sector, import substitution programs, and substantial payments to military personnel and their families—waned.

The Central Bank, which has pursued an extremely restrictive monetary policy since mid-2024, began easing monetary policy in June 2025. Further interest rate cuts are likely. In doing so, the central bank faces the challenge of balancing efforts to curb persistent inflationary pressures with the need to support the economy.

Despite a moderate easing of monetary policy, the Russian economy is forecast to grow by only 1.0 percent in 2026. On the one hand, production growth is likely to be hampered by an acute labor shortage. Private consumption is being held back by high household debt. In addition, fiscal measures such as the increase in the value-added tax from 20 to 22 percent and higher corporate taxes are weighing on business activity.

The labor shortage in the Russian economy was mainly caused by conscription into military service and the outflow of workers from Russia. The unemployment rate fell to a record low of 2.1 percent in the second half of 2025. However, there are now initial signs of an easing in parts of the labor market.

The development of Russian state budget revenues in 2025 was weighed down by lower-than-expected oil prices. In addition, the ruble was stronger than expected. The stronger exchange rate reduced the ruble value of oil and natural gas revenues denominated in U.S. dollars. To reduce the budget deficit, the government has announced tax increases.

Although Russia remains subject to extensive sanctions, which are primarily directed against its oil exports and restrict the import of high-tech goods, Russian energy exports remained relatively stable. Russia was largely able to maintain its access to imports. Constant adjustments to Russia’s trade relations and financing channels helped limit the macroeconomic impact of the sanctions. Following the imposition of additional sanctions by the European Union and the United States in 2025, the outlook for Russian energy exports depends on whether the country can continue to sell oil to markets outside the European Union.

Vasily Astrov on current developments in the Russian economy

The Vienna Institute for International Economic Studies (wiiw) is expected to publish new forecasts for the countries of Central, Eastern, and Southeastern Europe in early February. In its “Country Overview Russia,” updated in early January 2026, the institute further lowered its forecast for Russian economic growth in 2025 to just 0.7 percent.

wiiw: Country Overview Russia

Basic data are continuously updated; wiiw: Country Overview Russia

In its “Autumn Forecast” in October 2025, wiiw had still expected GDP growth of 1.2 percent in Russia for 2025. In its “Spring Forecast” published at the end of April, the institute had even anticipated that growth would reach 2.0 percent in 2025.

Vasily Astrov, a Russia expert at wiiw, commented in detail on the current state of the Russian economy in a conversation with Eduard Steiner on the Russia podcast of the Austrian newspaper “Die Presse” on January 9. He criticizes not only the central bank’s very high key interest rates but also the Russian government’s “restrictive” fiscal policy.

Below is a summary of Astrov’s assessments in the podcast:

The very high interest rates are slowing down consumption growth

Very high interest rates are the primary problem for economic development in Russia. The auto market, for example, is suffering massively from this because a large portion of car purchases is or was financed through loans. Considering that the annual inflation rate currently stands at around 6 percent, real interest rates are still in the double digits.

All purchases that are financed entirely or largely through loans are affected by the high real interest rates. This also applies to the purchase of durable consumer goods and real estate. When it comes to purchasing basic foodstuffs, for example, we see only minor effects from high interest rates because these purchases are financed by wages and other income. While their growth has also leveled off, it remains in positive territory.

Overall, consumption is still growing, but not as strongly as before.

The inflation rate has been successfully reduced

The Russian Central Bank’s policy is geared toward doing everything possible to bring the inflation rate close to its target of four percent. The European Central Bank’s inflation target is two percent, but “by Russian standards,” 4 percent is a fairly low figure. The Russian Central Bank has also achieved “considerable success” in this regard by 2025. It should not be forgotten that inflation stood at ten percent at the beginning of 2025 (minute 37).

Central Bank President Nabiullina expected a slump in growth

Central Bank Governor Nabiullina likely already anticipated that the very restrictive monetary policy would lead to a massive slump in economic growth. The Russian economy will probably end up in stagnation. That was likely factored in.

When the Central Bank chief or even President Putin himself speak of a “controlled soft landing,” they likely mean it. It was rather surprising that it took so long for this landing to occur. After all, interest rates had been in the double digits—or close to twenty percent—for some time. Yet it still took quite a while before demand actually cooled significantly.

High interest rates have hurt the economy more than the sanctions

A “pro-government” economic research institute—which, incidentally, is headed by the brother of the current Defense Minister Belousov—has issued a statement that is quite well-known in Russia, claiming that the Russian Central Bank’s high-interest-rate policy has harmed the Russian economy more than the sanctions. “And if you ask me, I do believe that’s true, at least in the short term” (minute 42).

The sanctions act like a “slow-acting poison.” The full impact of the sanctions, especially the effect of limited access to Western technologies, will only unfold gradually, over the long term. But in the short term—if we’re talking about a period of one or one and a half years—it is primarily the high interest rates that are to blame for the current economic slump.

Russia’s budget deficit is low by international standards

On the one hand, there are now a whole series of tax hikes in Russia. For example, the VAT rate was raised from 20 percent to 22 percent.

On the other hand, however, one must not forget that Russia’s current budget deficits are not particularly high by international standards. The deficit of 2.6 percent of GDP projected by the finance minister for 2025 is indeed a high budget deficit “by Russian standards.” It was higher only during the COVID-19 pandemic. In 2020, the budget deficit exceeded three percent of GDP. But by international standards, for example compared to the eurozone, it is not particularly high.

Economic policymakers in Russia have always strived to keep budget deficits as low as possible, partly due to historical experience (the 1998 sovereign default). Another reason for the relatively restrictive fiscal policy is that the cost of issuing government bonds is very high due to generally very high interest rates. Debt service expenditures have risen sharply, to around eight percent of federal budget expenditures, which amount to just under 20 percent of Russia’s gross domestic product.

The policy of low deficits—and even the generation of surpluses in many years—has naturally had positive consequences. Public debt has been brought down to a very low level. Fiscal reserves have been built up.

However, this restrictive fiscal policy came at the cost of lost growth

On the other hand, this overly cautious fiscal policy meant that much of the spending actually needed for infrastructure, education, and healthcare was either entirely or largely neglected. This largely explains why the Russian economy grew so sluggishly for years. In the ten years before the war, the Russian economy grew by only about one percent—or even less than one percent—per year. In effect, it stagnated. This means there is, or at least there was, the potential for the economy to grow somewhat faster than that one percent.

The decline in investment is a cause for concern

Until 2024, there was still fairly strong growth in gross fixed capital formation. Currently, however, we are seeing virtually no year-over-year growth when we look at the first three quarters. In the third quarter, investment declined slightly.

The fact that investment is declining is, of course, not good news for growth.

If companies aren’t investing, where is growth supposed to come from? Labor is rather scarce. Unemployment remains very, very low. The unemployment rate is around two percent.

Russia must invest above all in labor-saving technologies, in technologies that enable higher labor productivity. But we haven’t seen such investments, not even during the boom years. Those were not investments in machinery and equipment. They were other kinds of investments, such as investments in military infrastructure. None of that has much to do with creating higher labor productivity. But growth without rising labor productivity will not be possible.

The risk of corporate bankruptcies is growing

Due to high interest rates, Russian companies now have to spend nearly forty percent of their profits on debt service. The longer interest rates remain this high, the greater the likelihood that the number of bankruptcies will increase.

While large companies like Gazprom, Rosneft, and the railways, for example, can always count on a bailout from the state, smaller medium-sized companies, of course, cannot.

Recommended reading:

- Finam.ru; Alexander Abramov: Head of the Laboratory at the Institute for Applied Economic Research of the Russian Presidential Academy of National Economy and Public Administration: Rosstat has caused problems for the Central Bank with record-low inflation in 2025, 01/18/26

- russianlife.com: Poor economic indicators. The Bell highlighted ten factors that could push the Russian economy to the brink of collapse in 2026, Jan. 17, 2026

- Finmarket.ru: Inflation in Russia stood at 5.59% in 2025, 01/16/26

- The Bell.ru; Denis Kasyanchuk: Inflation in 2025 slowed to 5.6%, which is below analysts’ forecasts, Jan. 16, 2026

- Expert.ru: Anton Siluanov: The budget deficit for the year amounted to 2.6% of GDP, Jan. 16, 2026

- Bank of Finland; BOFIT Weekly: Russia’s economic performance has weakened in many areas, Jan. 15, 2026

- Politcom Economic Report; Marina Voitenko: Macroeconomic Dynamics in Russia in 2026: Expectations and Risks, Jan. 15, 2026

- Ura.news; Artur Yakushko: Belousov warned of a recession: What will happen to prices and wages? Most Russian industries are stagnating or have incurred losses, Jan. 15, 2026

- Ura.news: Economist Belousov assessed the likelihood of wage cuts in 2026. Companies will not carry out mass layoffs in 2026, Jan. 15, 2026

- Nezavisimaya Gazeta; Anastasia Bashkatova: Russian consumers have begun to replenish their wallets. The New Year holidays ended with a sharp rise in inflation, 01/15/26.

- Nezavisimaya Gazeta; Anastasia Bashkatova: Short-term forecasts predict that Russian GDP will grow by only 0.9% per year, Jan. 14, 2026

- Actual News; Olga Pavlova: Expert Kogan stated that the year 2026 will bring changes in macroeconomic trends, Jan. 14, 2026.

- CMASF: Trends in the Russian Economy; Monthly Report, November Data; 01/14/26

- FR.de, Bona Hyun: Money for Putin’s war chest: Gazprom sets a new record—and becomes China’s largest supplier, 01/13/26

- Alexander Shirov; Institute for Economic Forecasting of the Russian Academy of Sciences: “We’re delivering the weather forecast.” How and why economists look to the future, 01/13/26

- World Bank: Global Economic Prospects, Press Release; GDP Forecasts; Regional Overview: Europe and Central Asia, Jan. 13, 2026

- Kommersant, Artem Chugunov: Roughly Zero: Economic Activity Approached Stagnation by the End of 2025, 01/12/26

- Lenta.ru; Alena Shevchenko: Russia has declared the problem of zero economic growth. Professor Abramov spoke about the problem of zero economic growth in Russia. 01/12/26

- Gazeta.ru; Anastasia Alekseevskikh: “Under current conditions, it’s already good”: Economist on stagnation in Russia. BCS: Demographic trends slow GDP growth by 1%. 01/12/26

- Rosa Luxemburg Foundation, IIlya Matveev: The Limits of the Russian War Economy, 01/12/26; Testing the Limits of State-Directed Mobilization. The Russian economy appears resilient for now, but long-term stagnation is nearly unavoidable; 12/15/25

- Focus online, Christian Gehrke: $150,000 for a death: Putin is deliberately sacrificing indigenous peoples. Mortality rate 27 times higher than in Moscow, 01/11/26

- Nezavisimaya Gazeta, Mikhail Sergeev: The decline in investment in Russia has become the sharpest in the last 20 years, 01/11/26

- FR.de; Max Schäfer: Russia’s economy suffers heavy losses: Putin’s “shadow economy” collapses massively, 01/11/26

- The Guardian; Phillip Inman: Why Russia’s economy is unlikely to collapse even as oil prices fall, Jan. 10, 2026

- “Die Presse”: Podcast by Eduard Steiner and Vasily Astrov (wiiw): Will Putin finally kill Russia’s economy in 2026? Podcast guest: international oil and energy consultant Johannes Benigni, audio 54 min., 01/09/26

- United Nations; Department of Economic and Social Affairs: World Economic Situation and Prospects 2026, January 8, 2026

- Inosmi.ru, Anadolu Agency Turkey; Gürkan Abay: The Russian economy, which is in a phase of cooling, will continue to face difficulties in 2026, Jan. 8, 2026

- FR.de; Lennart Niklas, Johansson Schwenck: Putin’s oil power is collapsing: Expert explains Russia’s energy decline, 01/08/26: .