Slowing growth – Russian Central Bank cuts key interest rate to 18 percent

Author: Klaus Dormann

On Friday, the Russian Central Bank lowered its key interest rate from 20 to 18 percent. Surveys had shown that the vast majority of analysts expected this decision.

Reuters notes that the Central Bank is under significant pressure from the business community to ease its monetary policy. Business representatives had complained that investments were no longer profitable given the high interest rates. Even Economy Minister Reshetnikov said at the St. Petersburg Economic Forum that the Russian economy was “on the brink of a recession.”

Growth in the Russian economy has indeed slowed sharply following last year’s strong increase of 4.3 percent. In the first quarter of 2025, seasonally and calendar-adjusted gross domestic product was even lower than in the preceding fourth quarter of 2024. Some observers expect it to have fallen in the second quarter of 2025 as well, compared to the previous quarter.

However, according to preliminary calculations by the statistics agency Rosstat, Russia’s industrial production in the second quarter was 0.6 percent higher than in the previous quarter on a seasonally and calendar-adjusted basis. There was therefore no “technical recession” in Russian industry involving a decline in production over two consecutive quarters. Rosstat will release further economic data for June on July 30. Initial estimates regarding the development of production across the entire Russian economy in the second quarter are also expected at that time.

Central Bank: Return to “moderate growth” of 1 to 2 percent

The Central Bank expects the economy to grow

“moderate” growth. It sees Russia on the path to a “balanced growth trajectory.” Its press release on the key interest rate cut on July 25 states:

“The Russian economy’s deviation from a balanced growth path is narrowing. High-frequency data, including figures for the second quarter of 2025, and survey indicators point to a further slowdown in domestic demand growth, while economic activity as a whole continues to grow moderately.”

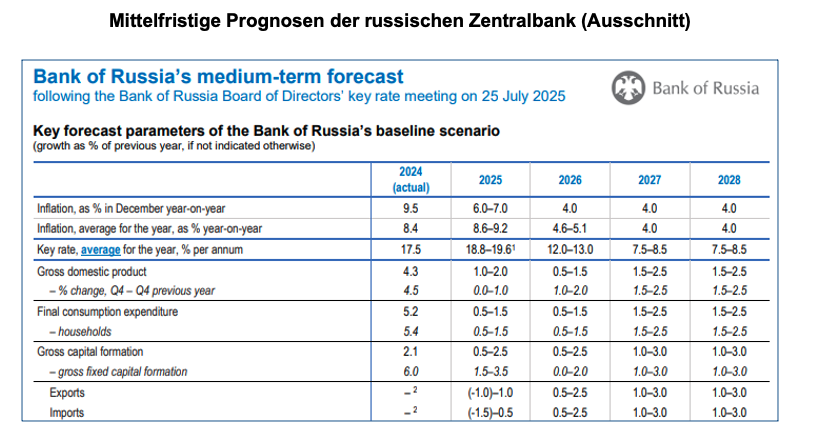

In its “Medium-Term Forecast,” updated on the occasion of the key interest rate decision, the Central Bank maintained its expectation that Russia’s gross domestic product will grow by 1.0 to 2.0 percent in 2025 (see the fourth row of the table below).

Inflationary pressures are easing faster than previously expected

The central bank primarily justifies the key interest rate cut by noting that price increases have eased in light of slower growth in domestic demand. It now expects the annual increase in consumer prices to reach only 6.0 to 7.0 percent by December 2025 (see the first row of the table below). Previously, it had anticipated an inflation rate of 7 to 8 percent by the end of 2025.

According to the central bank’s forecast, consumer prices will rise by an annual average of 8.6 to 9.2 percent in 2025, only slightly more than the 8.4 percent increase in 2024 (see second row).

The central bank stated that monetary policy conditions would be kept as tight as necessary to bring inflation back to its target level of 4 percent next year. It anticipates an average key interest rate of 18.8 to 19.6 percent in 2025 and 12.0 to 13.0 percent in 2026 (see third row). This means “that monetary policy will remain tight for an extended period,” the bank stated (dpa-AFX).

The annual inflation rate has since fallen from 10.3 percent in March to 9.4 percent in June (Trading Economics chart). The central bank expects to reach its inflation target of 4.0 percent by the end of 2026 (first row).

Russian Central Bank: Bank of Russia’s medium-term forecast, July 25, 2025; (excerpt)

Nabiullina: “Return to more balanced growth”

Elvira Nabiullina, President of the Russian Central Bank, noted in her statement on the key rate cut that the rise in consumer prices in Russia has slowed. Growth in consumer demand is gradually slowing. Lending is growing moderately. The central bank’s tight monetary policy is a key factor in the economy’s return to more balanced growth. Therefore, a further cut in the key interest rate is now possible.

Nabiullina also noted the following regarding the development of consumption and investment:

Demand growth is gradually slowing down. It is increasingly in line with the economy’s capacity to increase production. This is a key factor in the decline in price increases. Companies are scaling back their expectations regarding demand growth, particularly in the consumer sector. The Central Bank expects investment to increase this year, partly due to government support in priority sectors, though at a lower growth rate than in the previous two years.

According to the central bank’s updated forecast, the growth in gross fixed capital formation will slow from +6.0 percent in 2024 to just +1.5 percent to +3.5 percent this year.

Labor shortages remain a “risk factor” for inflation

According to Nabiullina, the situation on the labor market has eased somewhat recently. The number of companies reporting labor shortages has declined. At the same time, however, the unemployment rate remains at a record low.

According to the central bank’s assessment, companies are planning a more moderate wage adjustment for this year. However, the current rate of wage growth in the overall economy still exceeds the growth in labor productivity.

According to Nabiullina, the labor shortage remains a risk factor for inflation:

“Should domestic demand growth accelerate again without a corresponding increase in productivity, this will soon run into a labor shortage and would largely translate into price increases.”

No “technical recession” in Russia’s industry in the first half of the year

On July 23, the Russian Federal State Statistics Service (Rosstat) reported on the development of industrial production in June. The Moscow-based “Center for Macroeconomic Analysis and Short-term Forecasts (CMASF)” has illustrated in the following figure (red line) how the seasonally adjusted industrial production index developed according to Rosstat.

The red line shows that industrial production in April, May, and June 2025 was higher than in January, February, and March 2025. According to CMASF, Russia’s seasonally adjusted industrial production, as reported by Rosstat, was 0.6 percent higher in the second quarter than in the first quarter. In the preceding first quarter, industrial production had fallen by 1.2 percent compared to the fourth quarter of 2024, according to Rosstat. This means that Russia’s industrial production did not decline in two consecutive quarters. Thus, there was no so-called technical recession in Russian industry in the first half of 2025.

Industrial production according to estimates by Rosstat, CMASF, and HSE (seasonally adjusted, monthly average 2021 = 100)

Red line: Total industry (Rosstat)

Brown line: Industry excluding military-industrial complexes (CMASF)

Blue line: Manufacturing excluding military-industrial complexes and oil refineries (CMASF) green line: Total industry (HSE, Bessonov)

* Production of finished metal products not included in other categories; computers, electronic, and optical products; aircraft; other transport vehicles not included in other categories

Center for Macroeconomic Analysis and Short-term Forecasting, CMASF: Industrial Production in June, July 25, 2025

Recommended reading:

- bne IntelliNews Comment: Why Russia’s economic model no longer delivers, July 25, 2025

- Debug Lies: Russia’s Economic Crossroads in 2025: Militarization, Sanctions and the Limits of Resilience, July 24, 2025

- ntv.de: No new business deals. Eastern Committee: Normal trade with Russia “not foreseeable,” July 24, 2025; ntv.de: Numerous trips to Moscow. SPD historian appalled by Platzeck’s “hubris” and “stupidity,” 07/22/25

- t-online, jaf.: Crisis feared. This is how bad the Russian economy is, July 24, 2025

- Newsweek; Brendan Cole: Russia’s Economy Wobbles Under Strain of Ukraine War, 07/23/25

- National Security Journal; Georgia Gilholy: Russia’s Economy Is a Ticking Time Bomb, July 23, 2025, Stephen Silver. Russia’s Economy Looks Like a ‘House of Cards’ About to Collapse, July 23, 2025

- The Moscow Times; Jason Corcoran: Russian Banks Will Fall. The Question Is How Hard, July 22, 2025

- russland.capital. Bloomberg: Russian Banks May Need Government Support Next Year, 07/21/25

- TLDR News EU Video: Does Russia’s Economy Have a Debt Problem? With high interest rates and a slowing economy, Russia’s economy is showing increasing signs of near-collapse, 10 min., July 17, 2025

- Moscow Times: Does Russia’s Economy Have a Debt Problem? Record-high interest rates have led to warnings of a systemic banking crisis in the next 12 months. How realistic is that possibility? July 10, 2025

- thebell.io; Alexandra Prokopenko, Carnegie Berlin Center; Alexander Kolyandr, Center for European Policy Analysis (CEPA): Interest rates on banks. Is Russia facing a banking crisis? July 9, 2025

- Anders Aslund in Times Radio Interview: Putin faces an ‘existential’ threat as Russian economic growth collapses due to the war in Ukraine. Stagnation in the Russian economy has left Putin with no realistic option to end the war in Ukraine, says Anders Åslund on The Putin Files, July 21, 2025

- t-online, Simon Cleven: Russia in crisis. Putin’s economy is running out of steam, July 20, 2025

- Olga Belenkaya, Chief Economist at FG Finam: Economic data allows the Central Bank to reduce the key rate with more confidence; July 18, 2025

- Focus.de; Christian Massengarb: War economy becomes a problem. Banks fear financial crisis: A money problem is slowly creeping up on Putin, July 18, 2025