"Slowdown" rather than recession: Russia's GDP was likely higher in the second quarter than in the first

Author: Klaus Dormann

It is still quite uncertain how Russia’s gross domestic product performed in the second quarter. Leading Russian research institutes disagree on whether overall economic output in May was higher than in April. And the economic data for June will not be released by the Federal State Statistics Service (Rosstat) until July 30.

Nevertheless, the research and forecasting department of the Russian Central Bank issued an assessment last week of how gross domestic product developed in the second quarter of 2025 compared to the first quarter. The first sentence of the “Executive Summary” of the Central Bank’s “Talking Trends” economic report reads:

“Q2 macroeconomic statistics and surveys suggest the economy grew relative to the previous quarter.”

The Central Bank’s message: There was likely no recession

Based on statistics and surveys, the Central Bank therefore assumes that the economy grew in the second quarter compared to the preceding first quarter. This “message” is likely aimed primarily at those who already view Russia’s economy as being in a recession. For example, in a new study by Elina Ribakova and Benjamin Hilgenstock, the Washington-based “Peterson Institute for International Economics” points out that Russia’s real gross domestic product fell in the first quarter compared to the previous quarter.

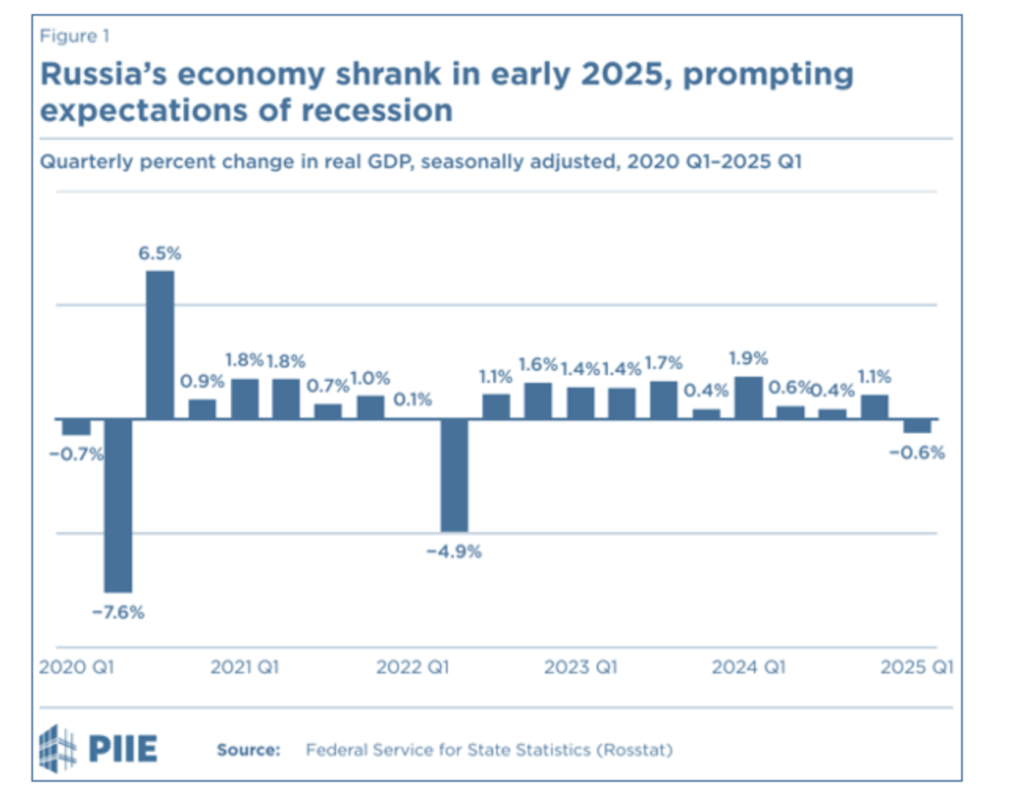

The Russian economy contracted in early 2025,

sparking expectations of a recession

Peterson Institute for International Economics; Benjamin Hilgenstock (KSE Institute) and Elina Ribakova (PIIE): Why Russia’s economic model no longer delivers, July 16, 2025; Chart URL

{kind=link}

The figure shows how Russia’s seasonally adjusted real gross domestic product changed from the first quarter of 2020 to the first quarter of 2025 compared to the respective previous quarter (see also FocusEconomics). The authors write about the development of aggregate economic output in the first quarter of 2025 compared to the same quarter of the previous year and compared to the previous quarter:

“In the first quarter of 2025, annual growth slowed to an estimated 1.4 percent compared to the previous year (after 4.5 percent in the last quarter of 2024).

This represents a 0.6 percent decline in economic activity compared to the previous quarter—the first quarterly decline since the second quarter of 2022 (Figure 1).”

Ribakova and Hilgenstock highlight the following conclusion from their analysis:

“A shrinking economy and low oil prices are signs that Russia’s ability to maintain its military capabilities may be limited.”

As things stand, the Russian economy has so far contracted only in the first quarter of 2025 compared to the sharply increased GDP level in the fourth quarter. In “Talking Trends,” the Russian Central Bank assumes that Russia’s real gross domestic product rose again in the second quarter of 2025 compared to the first quarter of 2025. If this assessment is confirmed, there has been no so-called “technical recession” in Russia—defined as a decline in real gross domestic product compared to the previous quarter for two consecutive quarters.

The Central Bank can also use this to counter critics who accuse it of having dampened the growth of the Russian economy too severely with its key interest rate, which was raised to 21 percent in October 2024.

The trend in gross domestic product in May is controversial

According to the Russian Ministry of Economic Development, Russia’s real gross domestic product in May was 1.2% higher than a year ago. From January through May, it grew by 1.5% year-over-year, according to the ministry (Finmarket.ru).

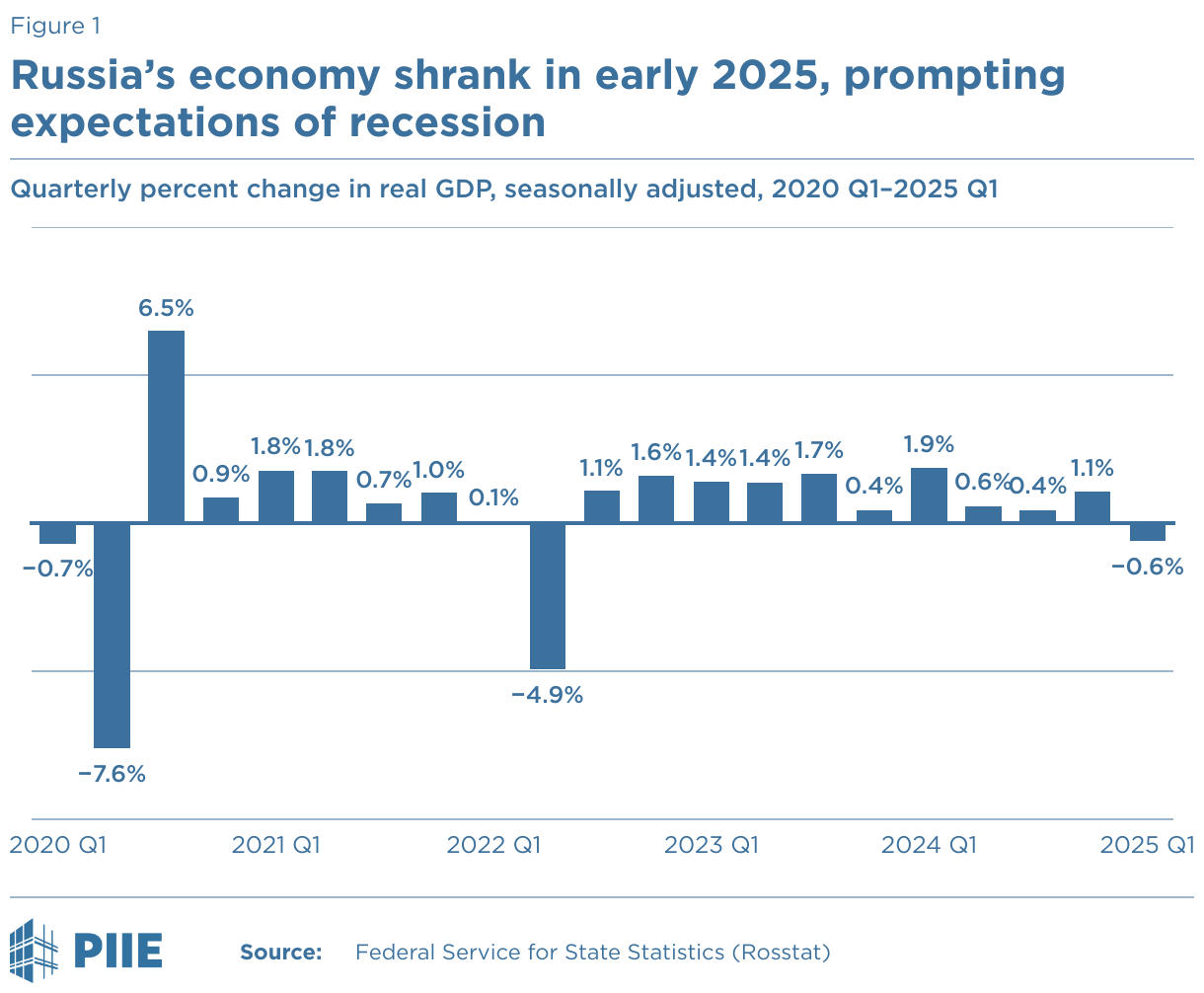

However, leading Russian economic research institutes have not yet reached a consensus on how aggregate economic output developed in May compared to the previous month of April. In its “Short-Term Analysis of GDP Development,” the Institute of Economic Forecasting of the Russian Academy of Sciences (IEF-RAS) states that real gross domestic product rose by 0.5% in May compared to April, seasonally adjusted. However, the research institute of the state-owned Bank for Foreign Economic Affairs (Vnesheconombank, VEB) estimates in its “GDP Index May 2025” that real GDP stagnated in May at the April level. Andrey Klepach, chief economist at Vnesheconombank, had recently stated in interviews that Russia’s growth was “currently taking a break” (see Ostwirtschaft.de).

In the following figure from the Research Institute of the Russian Academy of Sciences, the black line shows that the real gross domestic product index fell significantly during the first quarter of 2025. It is evident that roughly half of this decline was offset in April and May 2025. According to estimates by the RAS Institute, real GDP grew by 0.5 percent in May compared to April on a seasonally adjusted basis. The blue bars show the year-over-year changes in gross domestic product as a percentage.

Index of seasonally adjusted real gross domestic product;

2019=100, blue bars: year-over-year changes in %

IEF-RAS: Short-term forecast of Russia’s GDP dynamics; 07/14/25

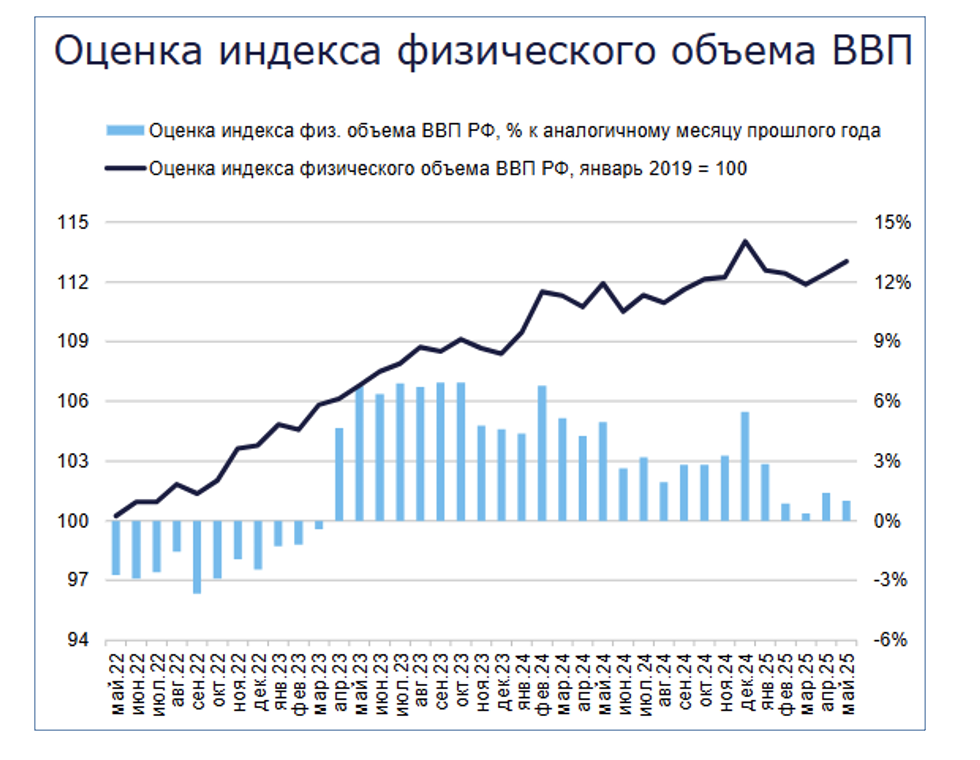

The Vnesheconombank Research Institute, however, estimates that real gross domestic product stagnated in May at the level reached in April.

Index of seasonally adjusted real gross domestic product,

January 2008=100

VEB Institute: GDP Index May 2025, June 17, 2025

Olga Belenkaya, chief economist at the brokerage firm FG Finam, published a detailed overview of current developments in the Russian economy on July 18 as background analysis for considerations regarding a further key interest rate cut: Economic data allows the Central Bank to reduce the key rate with more confidence.

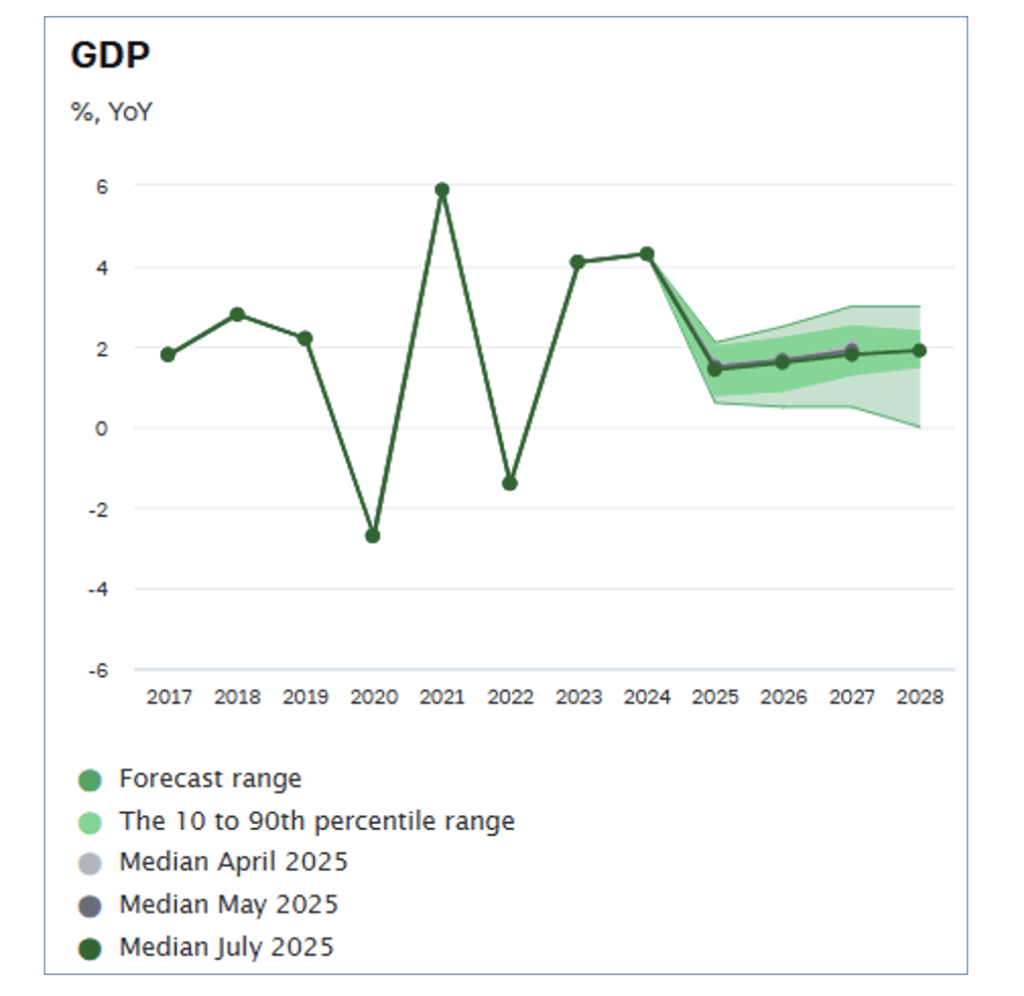

Analyst Survey: Economy to Grow by 1.4 Percent in 2025

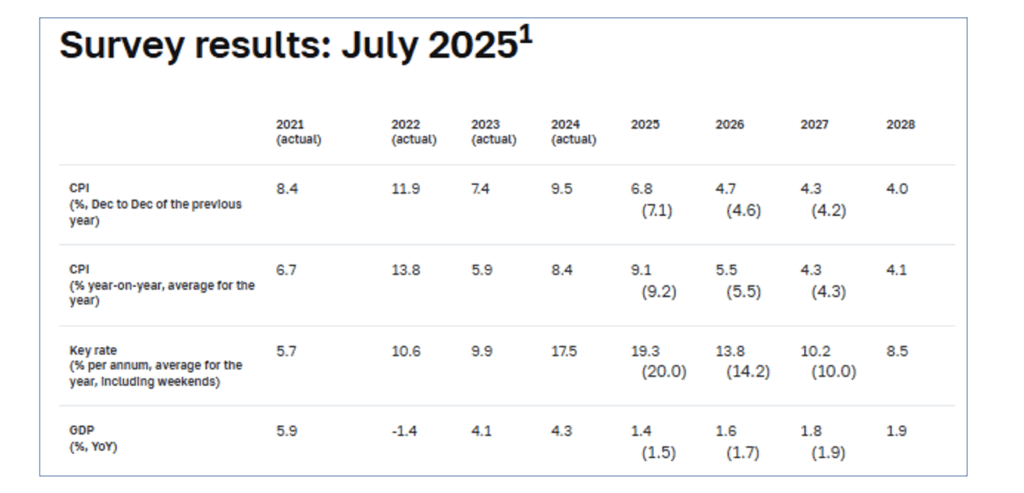

Ahead of its next key interest rate decision on July 25, the Central Bank once again surveyed analysts from banks, research institutes, and the media on economic developments in Russia. The results were published on July 16 (Macroeconomic survey of the Bank of Russia).

According to the 33 survey participants—including only a few foreign ones—annual growth in the Russian economy is expected to average 1.4 percent in 2025. In the last survey at the end of May, they had anticipated slightly higher growth (+1.5 percent). Their growth forecasts for 2025 now range from +0.5 percent to +2.1 percent. None of the participants expects a recession in the next three years.

Real Gross Domestic Product,

year-over-year change in percent

Bank of Russia: Macroeconomic survey, July 16, 2025

However, in an interview with the Polish international broadcaster “TVP World” at the end of June, Swedish Russia expert Anders Aslund stated that Russia would enter a crisis in the second half of 2025, with aggregate economic output barely rising. He expects “stagflation.”

The average growth forecasts in the Central Bank survey for 2026 and 2027 fell by only 0.1 percentage points each compared to the May survey. Unlike many foreign experts, the analysts do not expect a further slowdown in the growth of the Russian economy over the next three years, but rather a slight pickup in growth. They now anticipate real gross domestic product growth of +1.6 percent in 2026, +1.8 percent in 2027, and +1.9 percent in 2028 (see the last row of the table below).

According to analysts’ estimates, the year-over-year increase in consumer prices in Russia will accelerate to 9.1 percent in 2025 compared to 2024 (2024/2023: +8.4 percent; see second row). In December 2025, however, the annual inflation rate will reach only 6.8 percent on average according to their forecasts (December 2024/December 2023: +9.5 percent, see first row).

Results of the Central Bank’s July 2025

analyst survey on the development of inflation, the key interest rate, and gross domestic product

(May survey results in parentheses)

Bank of Russia: Macroeconomic survey, July 16, 2025

The key interest rate is expected to fall slightly faster than previously anticipated

Survey participants now expect the Central Bank’s key interest rate to fall to an annual average of 19.3 percent in 2025. Previously, they had anticipated a decline to 20 percent. In 2026, the key interest rate is expected to average 13.8 percent, 5.5 percentage points lower than in 2025.

According to an Izvestia survey published on July 18, all participants expect the central bank’s key interest rate—which was lowered from 21 to 20 percent in June—to be cut further at the central bank’s next rate-setting meeting on July 25. Eleven out of 15 survey participants expect the key interest rate to be lowered to 18 percent. A Vedomosti survey yielded a similar result.

“Talking Trends”: Resumption of GDP Growth in the Second Quarter

The Central Bank’s “Talking Trends” report from July 15 notes that Russia’s real gross domestic product declined in the first quarter of 2025 compared to its peak in the fourth quarter of 2024. The economy was “less overheated” in the first quarter, the Central Bank writes. Growth in private consumption slowed significantly as the effects of monetary tightening at the end of last year began to take hold. While growth in investment spending was high, it was concentrated in only a few sectors.

However, according to the central bank’s assessment, indicators for April and May now signal a resumption of growth in the second quarter. It cites data on trends in production and consumption, lending, the labor market, and corporate insolvencies.

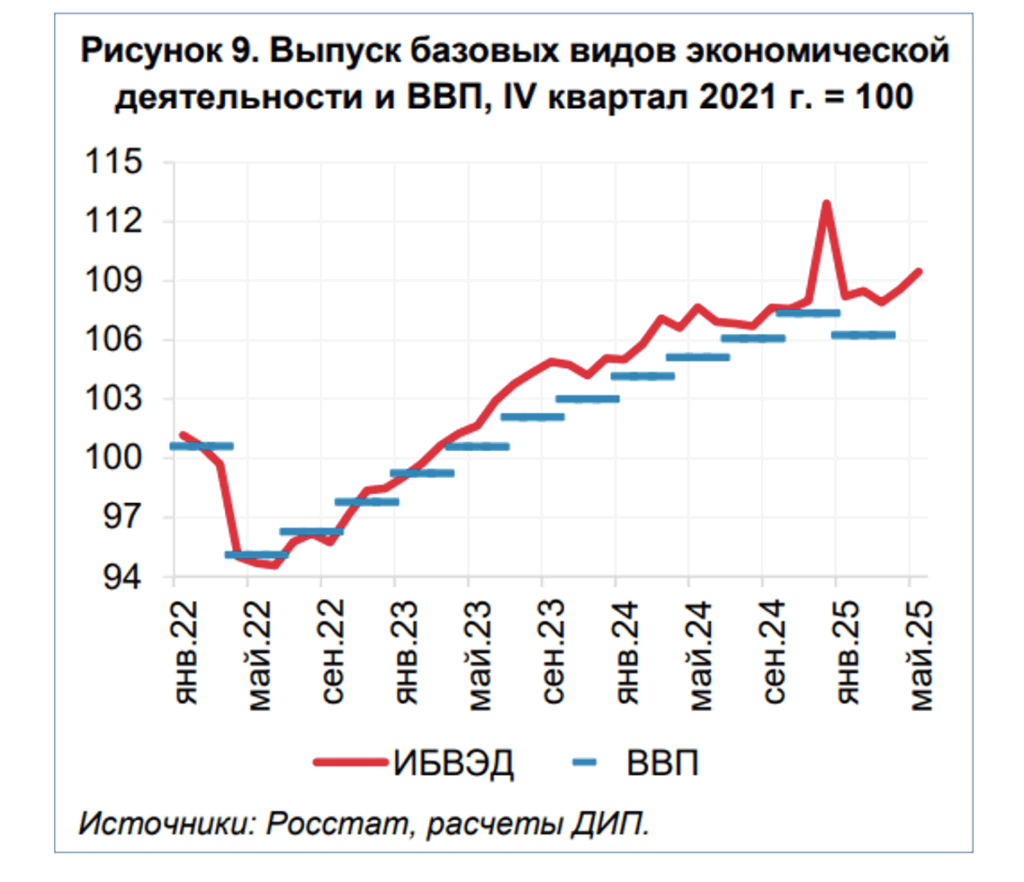

The following figure from the central bank’s report shows the trend in production in the “core sectors” of the Russian economy (red line) as an indicator of overall economic production. After a sharp rise at the end of 2024, production in the core sectors declined through March 2025. It recovered significantly in April and May. The blue lines show that real gross domestic product in the first quarter was lower than in the last quarter of 2024.

Production in core sectors and real gross domestic product

(Q4 2021=100)

Red line: Core sector production index, blue line: Gross domestic product, Sources: Rosstat, DIP calculations

Central Bank of Russia: What the trends say, July 15, 2025

At the same time, however, “Talking Trends” points out that the initial economic data for June indicated “more moderate momentum” compared to the data for April and May.

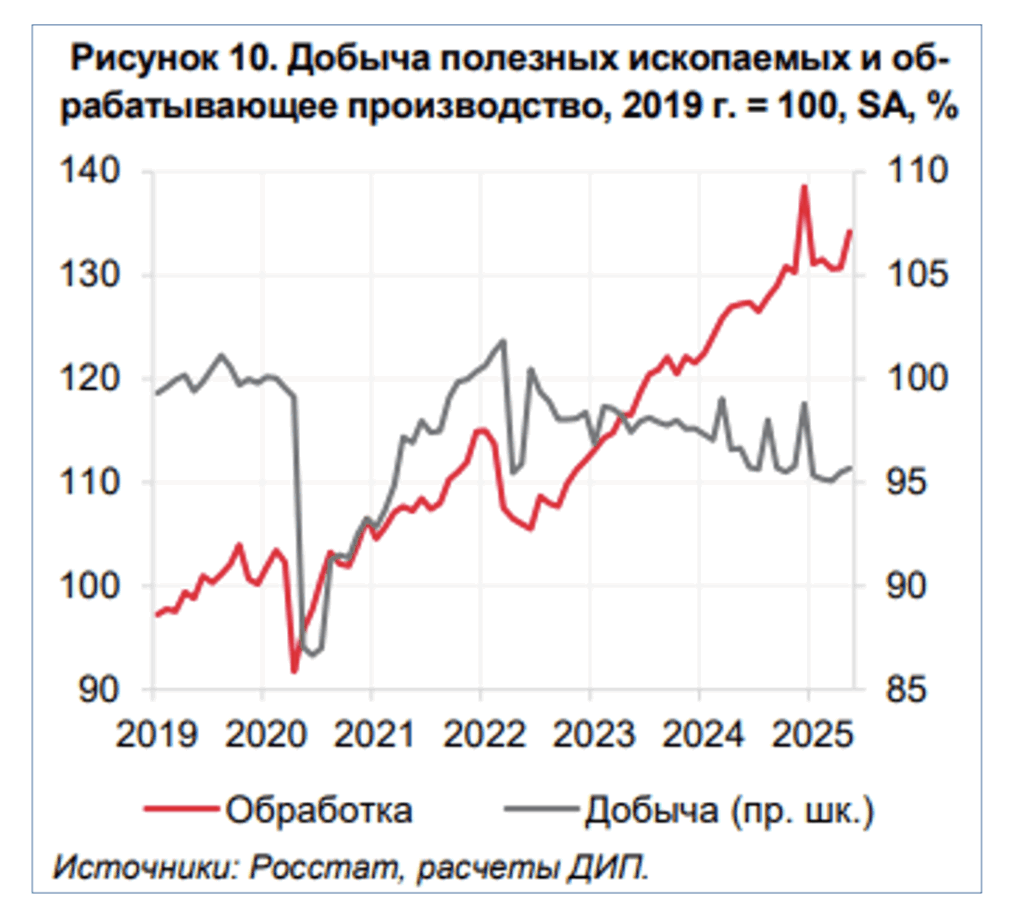

Industrial production rose in April and May

The Central Bank department calculated that Russia’s industrial production rose by 1.0 percent in April and May compared to the first quarter, on a seasonally adjusted basis.

This growth was driven primarily by an accelerated rise in production in the “manufacturing sector” (red line in the figure below). Sectors focused on meeting government demand and import substitution continued to grow at an above-average rate.

Moderate growth in the “mining and raw materials extraction” sector also contributed to the rise in industrial production, as voluntary production restrictions under the OPEC+ agreements were eased (gray line).

Production in Mining and “Manufacturing,

” 2019=100, seasonally adjusted

Central Bank of Russia: What the trends say, July 15, 2025

The Moscow “Center for Macroeconomic Analysis and Short-Term Forecasting (CMASF)” notes in its “Analysis of Macroeconomic Trends” published on July 16 that overall industrial production recorded a seasonally adjusted increase of 2.6% in May compared to the previous month. Production volume thus returned to the record level of December 2024.

However, according to CMASF estimates, about two-thirds of the May increase in industrial production is attributable to the sharp rise in output in sectors that primarily manufacture products for the defense sector. The remaining portion of the growth resulted from an increase in production in the non-ferrous metallurgy sector. In other industrial sectors, seasonally adjusted production stagnated in May at the April level.

Signs of “more moderate momentum” in June

According to the central bank’s “Talking Trends” report, business surveys from June showed that companies are planning to reduce their production.

Preliminary data suggests that growth in private spending slowed further in the second quarter. The central bank report states that domestic private demand has “aligned more closely with a balanced growth trend.” This development is reflected in slower growth in production costs and industrial producer prices.

Labor market remains tight with prospects for “stabilization”

Central bank analysts point out that the unemployment rate fell to a new all-time low of 2.2% in May and that employment reached another record high. Real wages rose by 0.5 percent in April compared to May on a seasonally adjusted basis. Consumers’ propensity to make major purchases remained high. Central bank analysts view this as a “development that continues to fuel inflation.”

However, there are signs that the labor market situation is gradually stabilizing. Some surveys and data suggest a decline in new hires and a shift in expectations toward staff reductions.

Recommended reading:

- Dr. Simon Gerards Iglesias, German Economic Institute, in conversation with Thomas Baier; podcast by the German-Russian Chamber of Foreign Trade “Zaren.Daten.Fakten”: “Between Growth, Stagnation, and Recession: Perspectives on the Russian Economy,” July 17, 2025

- German Economic Institute: Dr. Simon Gerards Iglesias in an interview with the Münchner Merkur: “Russia is financing its war largely through debt,” July 15, 2025

- DW.com,ru; Oleg Loginov: Has the Central Bank of the Russian Federation defeated inflation? What is the status of the key interest rate? July 18, 2025

- KSE Institute; Borys Dodonov, Benjamin Hilgenstock, Anatoliy Kravtsev, Yuliia Pavytska, Nataliia Shapoval; Russian Oil Tracker: Low prices push oil revenues down to the second-lowest level since the start of the full-scale invasion; July 17, 2025

- Bruegel, Brussels; Benjamin Hilgenstock, Elina Ribakova: Why Russia’s economic model no longer delivers. A contracting economy and low oil prices are signs of potential constraints on Russia’s ability to maintain its military capabilities, July 16, 2025;

- Peterson Institute for International Economics; Benjamin Hilgenstock (KSE Institute) and Elina Ribakova (PIIE): Why Russia’s economic model no longer delivers, July 16, 2025

- Interfax.com: Russian GDP may have grown slightly in Q2 – Central Bank analysts, July 15, 2025

- David O’Sullivan, EU Sanctions Envoy, in an interview: Groupe d’études géopolitiques, École normale supérieure, Paris: A conversation with David O’Sullivan, EU Sanctions Envoy, July 15, 2025

- Yahoo; dpa international: Russians struggle to pay for potatoes as war eats up state funds, July 14, 2025

- The Moscow Times: Russia-China Trade Falls 9% in First Half of 2025, July 14, 2025

- Joe Blogs: Russian revenues crash: … 4:08 Urals oil, 8:43 Military spending, 11:52 LNG,.. July 14, 2025

- Kommersant, Artem Chugunov: Investing is becoming increasingly difficult. The Institute of Economic Forecasting (IEF) of the RAS conducted another survey of enterprises, July 11, 2025

- Sergey Aleksashenko, Senior Research Fellow, New Eurasian Strategies Centre: Economic constraints of the Russian war machine, July 10, 2025