Russia: Will there be a "soft landing," or is a recession still on the horizon?

Author: Klaus Dormann

According to the Federal State Statistics Service (Rosstat), Russia’s real gross domestic product grew by only 1.1% year-over-year in the second quarter of 2025, much weaker than the Central Bank had estimated on August 6 (+1.8%, see Ostwirtschaft.de). In the first quarter of 2025, Russia’s annual GDP growth had still reached 1.4%. In the first half of 2025, total economic output was thus only 1.2% higher than a year ago, according to estimates by the Ministry of Economic Development.

In 2023 and 2024, Russia’s economy had still grown by a solid 4 percent year-over-year. There was frequent talk of “overheating.” The annual inflation rate rose to around 10 percent in early 2025. The central bank and the government set a goal of “cooling down” the economy. In fact, the current price surge has since subsided significantly amid a marked slowdown in production growth. The annual inflation rate fell to 8.8 percent in July.

For the full year 2025, analysts surveyed by Interfax in early August expect GDP to rise by an average of 1.4 percent, and by 1.7 percent for 2026. Sergey Aleksashenko, who served as Deputy President of the Russian Central Bank and Deputy Finance Minister in the 1990s, does not, however, believe in a “soft landing” for the Russian economy with a renewed uptick in growth in the near future. His detailed analysis, published by the London-based “New Eurasian Strategy Centre,” paints a bleak picture:

“The Russian economy is moving slowly but steadily toward a recession and runs the risk of slipping into a prolonged period of stagnation.”

Further insights on this topic can be found at the end of this article. First, a comparison of current comments from financial institutions and think tanks on the development of aggregate economic output in Russia (MMI, Raiffeisenbank, Capital Economics, Alfa Bank, Oxford Economics, BOFIT), with references to the economic assessments of the government and the central bank.

MMI sees a “technical recession” in the first half of the year—with reservations

According to a report in The Moscow Times on August 14, only a small minority of analysts believe that a so-called “technical recession” has already occurred in Russia in the first half of the year. They assume that aggregate economic output declined not only in the first quarter of 2025 compared to the previous quarter, but also in the second quarter. Rosstat has not yet published data on this. However, the vast majority of analysts apparently believe that GDP rose slightly in the second quarter compared to the first quarter, and thus there was no “technical recession” in Russia.

Based on initial estimates, the Telegram channel MMI concluded that there was a “technical recession” (t.me/russian macro). The MMI channel, founded by Kirill Tremasov, an advisor to the President of the Russian Central Bank, published the following two charts on the quarterly development of real gross domestic product:

Quarterly trends in real gross domestic product

https://t.me/russianmacro/21649

The left figure shows the slowdown in the annual growth rate of real gross domestic product, as calculated by Rosstat, from 1.4 percent in the first quarter of 2025 to 1.1 percent in the second quarter of 2025.

The right-hand figure shows the development of the real gross domestic product index (2014 = 100) according to MMI estimates. It is evident that the GDP index peaked in the fourth quarter of 2024. It declined in the first and second quarters of 2025. MMI therefore assumes a “technical recession,” in which GDP declines for two consecutive quarters.

In the table below the figures, the first row shows Rosstat data on the quarterly development of gross domestic product compared to the same quarter of the previous year.

The second row shows how seasonally adjusted real gross domestic product developed compared to the previous quarter, according to Rosstat. In the first quarter of 2025, real gross domestic product fell by 0.6 percent compared to the fourth quarter of 2024, according to Rosstat. Rosstat has not yet provided any data on the development of aggregate economic output in the second quarter compared to the first quarter.

The third row shows MMI’s estimates of GDP growth compared to the previous quarter. In some quarters, these estimates differ significantly from Rosstat’s figures. According to MMI’s initial estimate, Russia experienced a “technical recession” in the first half of the year. MMI estimates that real gross domestic product fell by 0.5 percent on a seasonally adjusted basis in the second quarter compared to the first quarter, after having been 1.2 percent lower in the first quarter than in the fourth quarter of 2024.

The GDP estimates are still highly uncertain

MMI itself points out the high uncertainty of these estimates:

“The negative GDP momentum in the first half of 2025 is largely a consequence of the abnormal and unexplained rise in GDP in the fourth quarter of 2024. According to our estimates, even after two quarters of decline, seasonally adjusted GDP in the second quarter of 2025 was 0.5% higher than in the third quarter of 2024.

Our smoothing (adjustment) differs from that of Rosstat. Many fellow analysts are providing different estimates. And the data itself is still subject to revision. Therefore, we are refraining for now from asserting that a technical recession has occurred.”

Capital Economics: Russia narrowly avoided a recession

Liam Peach (“Senior Emerging Markets Economist” at Capital Economics) estimates that Russia’s economy narrowly avoided a technical recession. He puts second-quarter growth at 0.3 percent compared to the previous quarter.

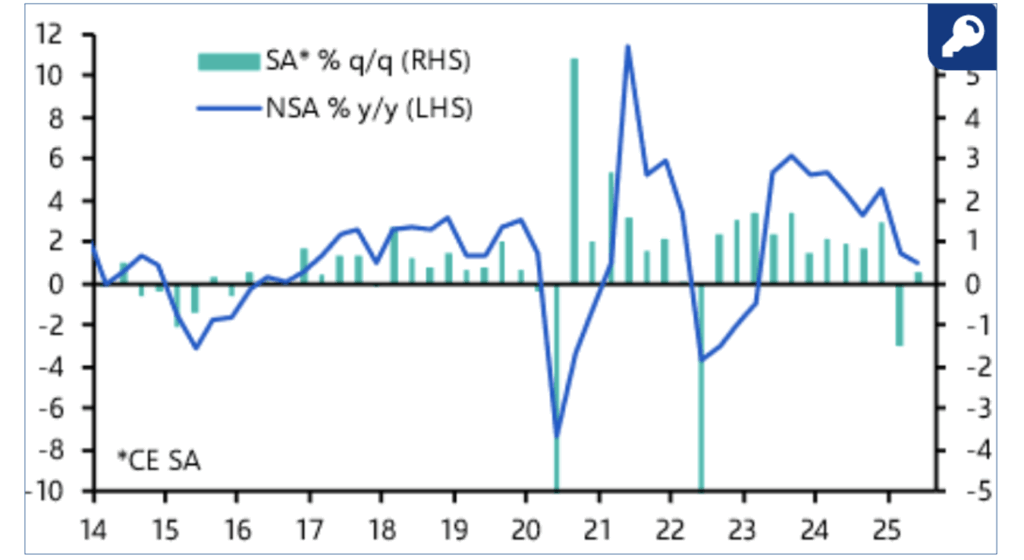

In the following chart from Capital Economics, the right-hand green bar shows the weak increase in seasonally adjusted gross domestic product in the second quarter compared to the previous quarter of 0.3 percent (right-hand scale). The blue line shows the year-over-year percentage changes in aggregate economic output (left scale).

Quarterly trend in real gross domestic product

Source: https://www.capitaleconomics.com/about-us/our-team/liam-peach

Raiffeisenbank Russia: The “soft landing” scenario is coming true

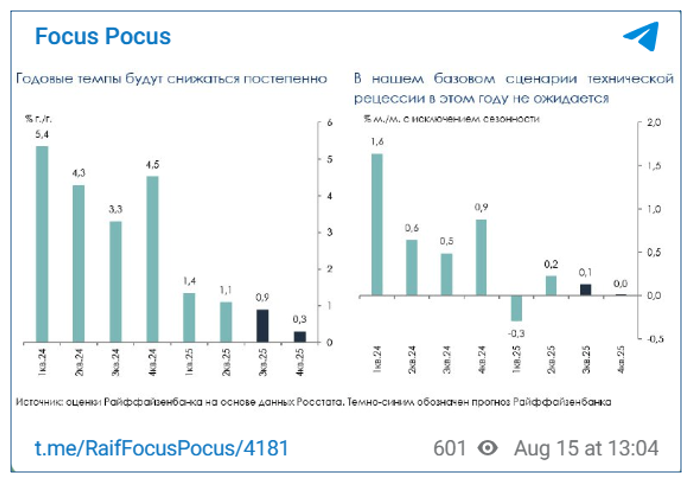

In its Telegram channel “Focus Pocus,” Raiffeisenbank Russia states that the development of aggregate economic output in Russia “fully corresponds to the soft landing scenario” (see also RAIF Daily Focus). Chief Economist: Stanislav Murashov also ventures forecasts for the further development of gross domestic product in the third and fourth quarters of 2025 using the following chart.

The right-hand figure of the two below shows how seasonally adjusted gross domestic product is likely to develop compared to the previous quarter. Following a weak increase of 0.2 percent in the second quarter of 2025, Raiffeisenbank expects the growth rate to halve to just 0.1 percent in the third quarter. In the fourth quarter, GDP is expected to stagnate at the level reached.

Quarterly GDP changes compared to the previous year and the previous quarter

Raiffeisenbank, Focus Pocus: GDP for Q2 2025: Recession Not Confirmed, 08/15/25

The chart on the left shows the slowdown in the annual growth rate to 1.1 percent in the second quarter of 2025, as calculated by Rosstat. According to “Focus Pocus,” year-over-year growth in the current third quarter will reach only 0.9 percent. In the fourth quarter, real gross domestic product will exceed its previous year’s level by only 0.3 percent. Raiffeisenbank estimates year-over-year growth for 2025/2024 at 0.9 percent.

Oxford Economics: Russia is on the Brink of a Recession

Analysts surveyed by Bloomberg had estimated the annual growth rate of the Russian economy in the second quarter at 1.5 percent prior to the Rosstat announcement. Bloomberg concluded that the government had apparently succeeded in achieving a “soft landing,” despite growing concerns about unsustainably high borrowing costs and a sharp decline in demand due to the central bank’s restrictive monetary policy. At the same time, Bloomberg noted that much of the growth momentum came from government spending on the defense sector. Otherwise, the economy would continue to weaken (see also regarding the Bloomberg article: Financial Post; Inosmi.ru with Russian translation).

According to Bloomberg, whether Russia can maintain at least moderate economic growth currently depends on both geopolitical factors and the easing of Russian monetary policy. Tatiana Orlova, Lead Economist for Emerging Markets at Oxford Economics, spoke to Bloomberg about the implications of negotiations to end the war in Ukraine for the Russian economy. If Russia were to decide to continue the war, Orlova believes that additional harsh sanctions—which would likely target the energy sector—could lead to an economic downturn. According to Orlova’s assessment, deposit and lending rates will remain high. This would have a negative impact on lending and private consumption.

The economist’s assessment of growth trends appears to be quite similar to that of Raiffeisenbank. However, she does not speak of a “soft landing,” but emphasizes that the Russian economy is “on the brink of a recession.” Orlova told Bloomberg:

“The economy returned to weak growth in the second quarter, but this growth is losing momentum. We expect the economy to be on the brink of a recession in the coming quarters.”

BOFIT: Production growth has stagnated this year

BOFIT, the research institute of the Finnish central bank, also does not believe that the Russian economy has entered a “technical recession.” In its weekly report released on Friday, the institute noted that preliminary data suggests that output in the Russian economy grew slightly in the second quarter compared to the previous quarter. BOFIT provides the following overview of economic developments:

“The rise in Russian production has stagnated this year, although the economy did not fall into a recession. Growing economic imbalances, high interest rates dampening demand, and falling oil prices have slowed growth.

Despite falling export revenues and lower budget revenues due to lower oil prices, budget spending has been significantly increased in recent months to boost war-critical production. Inflation remains high.”

Ministry: Continued Slowdown Amid Restrictive Monetary Policy

Russia’s Ministry of Economic Development, however, emphasizes in its “Report on the Current State of the Economy” that the rise in prices has slowed significantly. The ministry cites the central bank’s restrictive monetary policy as one reason for the economic slowdown. According to Finmarket.ru, it notes that

“the maintenance of restrictive monetary conditions in the second quarter was accompanied by a continued economic slowdown: According to a preliminary estimate by Rosstat, the economy’s growth rate in the second quarter of 2025 was 1.1% year-over-year, down from 1.4% in the first quarter. The main reason for the slowdown was weaker domestic demand, which was reflected in a significant deceleration of inflation from a peak of 10.3% year-over-year in March to 8.55% year-over-year on August 11.”(For more on price trends, see also: Interfax.ru and: Oktagon.media; Olga Belenkaya; Chief Economist at FG Finam: Is the Central Bank Taking the Lead and Winning? 08/15/25)

Year-over-year in 2025/2024, the Russian economy continues to grow

However, analysts surveyed by Interfax in early August still expect GDP to rise by an average of 1.4 percent for the full year 2025 and by 1.7 percent for 2026. BOFIT reports that, according to the July report from “Consensus Economics,” analysts surveyed worldwide expected the Russian economy to grow by 1.4 percent in 2025 and 1.3 percent in 2026.

In its medium-term forecast for 2025, updated at the end of July, the Russian Central Bank continues to expect the Russian economy to grow by 1.0 to 2.0 percent. At 1.2 percent, the growth achieved in the first half of the year is thus just above the lower end of the Central Bank’s annual forecast.

Russia’s Ministry of Economic Development has so far forecast significantly stronger growth in Russia’s gross domestic product: 2.5% in 2025 and 2.4% in 2026. According to Interfax, the ministry will present a revised forecast in late August or early September.

Alfa Bank, Russia’s largest private bank, stated in a report dated August 14 that annual economic growth this year could be around 1 percent, placing it at the lower end of the Central Bank’s forecast range of 1.0 to 2.0 percent.

However, the bank notes that there have been signs of a recovery since July thanks to lower interest rates: new car sales rose by 33% compared to the previous month, and real estate sales in Moscow increased by 17%.

Rising household incomes, according to Alfa Bank, could support demand: In the first half of the year, real disposable income rose by 7.8 percent compared to the previous year, and in the second quarter by as much as 7.0 percent.

Alfa Bank continues to expect the Central Bank to cut its key interest rate by another 2 percentage points to 16% in September. It anticipates a key interest rate of 15% by year-end.

However, unlike the government, the central bank, and the majority of analysts, some experts expect a recession in 2026. On August 6, the Moscow-based “Center for Macroeconomic Analysis and Short-term Forecasts” (CMASF), often described as “pro-government,” published an analysis of leading economic indicators. In it, the CMASF concludes that a recession in Russia is inevitable next year, even if the central bank continues to ease its monetary policy (Frank Media.ru). In its economic forecast published at the end of July, however, the CMASF expects economic growth of 1.5 to 1.8 percent next year.

Putin: The Central Bank currently sees “no major risks”

Presumably to reassure the public, President Putin also addressed the growing fears of a recession on August 12 during economic consultations with government officials and Central Bank Governor Nabiullina. He noted that the Russian Central Bank currently sees “no major risks.” According to Finam.ru, Putin said:

“Many experts are talking about the emergence of risks of an excessive economic slowdown and even a recession. … We are in constant communication with the President of the Bank of Russia about this. The Bank is monitoring the situation, working directly with companies, and assessing the situation. As I understand it, the Bank does not see any major risks at this time.”

The President highlights progress toward “balanced growth”

Putin emphasized that the government and the Central Bank face the joint task this year of returning the Russian economy to a “balanced growth path.” This means reducing inflation while simultaneously stabilizing unemployment at a low level.

The president cited the decline in the inflation rate as an “important success.” The annual inflation rate had fallen to 8.8 percent by the end of July. In March, it had still stood at 10.3 percent. According to the Central Bank’s latest forecast, the rate of price increases could drop to 6 to 7 percent by the end of the year, lower than the Central Bank had previously expected.

Regarding labor market trends, Putin highlighted signs of a reduction in labor shortages. According to surveys, including those conducted by the Bank of Russia, the proportion of companies facing labor shortages is declining. The number of officially registered unemployed and the number of estimated “hidden” unemployed is rising. However, the unemployment rate remains at a historic low of 2.2 percent.

Putin described the current state of public finances as “stable.” The government has begun drafting the federal budget for the years 2026 to 2028.

Sergey Aleksachenko: High interest rates have serious side effects

Sergey Aleksachenko, Senior Research Fellow at the “New Eurasian Strategy Centre” in London, acknowledges in a detailed analysis of the Russian economy in the second quarter of 2025 that the Russian Central Bank was able to prevent runaway inflation through a significant interest rate hike. The high interest rates led to a decline in prices for non-food items and a significant strengthening of the ruble. At the same time, however, the Central Bank’s crisis-response measures and the ruble’s appreciation had serious side effects:

“Sectors of the real economy not involved in defense production came under pressure due to excessively high interest rates. These interest rates directly restricted companies’ access to financing and indirectly weakened demand, which was reflected, among other things, in lower leasing activity and a decline in mortgage lending.

Furthermore, the state budget lost a significant portion of its exchange-rate-dependent revenues (due to the ruble’s appreciation), including revenues from oil and gas production as well as value-added tax on imports.”

Aleksachenko draws the following conclusions from his analysis, among others:

“The non-military sector of the Russian economy continues to experience a slow but steady decline in output. The recession is deepening and could lead to a prolonged period of stagnation.

The previous increase in the key interest rate enabled the Bank of Russia to control inflation and strengthen the ruble. However, this led to higher borrowing costs and a decline in credit demand.

The interest rate cut that began in May has not altered the overall negative trend. Real interest rates remain high (with a key interest rate of 18 percent and a current inflation rate of 4 percent on an annualized basis), which continues to slow economic activity.”

What an end to the war in Ukraine would mean for the Russian economy

Aleksachenko, who emigrated to the U.S. in 2014 for political reasons, highlights in his analysis the importance of the defense industry for the development of the Russian economy and comments on the consequences of a ceasefire in Ukraine as follows:

“Arms production remains the engine of the economy. A potential halt to military operations in Ukraine carries the risk of a decline in economic activity. Until demand for credit recovers, this could lead to an even deeper recession.”

Aleksachenko describes a potential cessation of hostilities in Ukraine as “a major external risk to the Russian economy.” Regarding the economic consequences of a ceasefire, he states:

“In the short term, this would slow the growth of military spending and, in the longer term, lead to its reduction. Since defense production is currently the only significant driver of economic activity, any weakening of this factor before a recovery in credit demand from households and businesses could deepen the recession and entrench it as the new normal.”

Recommended reading:

- Bank of Finland; BOFIT Weekly: Economic conditions in Russia continue to weaken, 08/15/25

- Moscow Times.ru: Rosstat estimates that the Russian economy is growing again following Putin’s demand to “under no circumstances allow a decline,” August 14, 2025

- The Bell.ru: Bloomberg describes Russia’s economic risks ahead of the meeting between Putin and Trump, Aug. 14, 2025

- Alfa Bank: Russia’s GDP grew by 1.1% in the second quarter of 2025—worse than forecast. Economic slowdown fuels debate over interest rate cuts, August 14, 2025

- Interfax.ru: The Ministry of Economic Development reported an acceleration in Russian GDP growth to 1.1% in June, up from 0.8% in May, 08/13/25

- Interfax.ru: Rosstat reported that Russian GDP growth slowed to 1.1% in the second quarter from 1.4% in the first quarter, August 13, 2025

- Institute for Economic Research of the Russian Academy of Sciences (RAS): Short-term analysis of GDP dynamics, 08/13/25

- TASS.com: IN BRIEF: Putin’s key statements at meeting on economic issues, 08/12/25

- Sergey Aleksashenko, Senior Research Fellow at the New Eurasian Strategy Centre, London: Russian economy update: Q2 2025, August 10, 2025; YouTube: Videos featuring Sergey Aleksashenko

- German-Russian Chamber of Foreign Trade: Podcast “Zaren.Daten.Fakten”: Sanctions and Their Limits (Guest: Prof. Christian von Soest), August 9, 2025