Russia's Slowing Economy: A Look Back and a Look Ahead

Author: Klaus Dormann

Discussions on the development of the Russian economy continue to focus on the Central Bank’s restrictive monetary policy, which has now led to a sharp economic slowdown. On October 24, however, the Central Bank lowered its high key interest rate by only 0.5 percentage points to 16.5 percent.

At the same time, it updated its “Medium-Term Forecast” for the development of the Russian economy through 2028. The Central Bank no longer expects “overheated” growth rates of over 4 percent, as seen in 2023 and 2024. It revised its growth forecast for 2025 down to just +0.5% to +1.0%. It considers it possible that real gross domestic product in the fourth quarter of 2025 will be up to 0.5 percent lower than a year ago. However, unlike some analysts, the Central Bank does not expect a recession in Russia. For 2026, it anticipates economic growth of +0.5% to +1.5%. According to the Central Bank, the Russian economy will return to its growth potential of +1.5% to +2.5% starting in 2027.

On November 6, the Central Bank released further information regarding its key interest rate decision and a detailed commentary on its “Medium-Term Forecast.” According to the Central Bank’s assessment, current data suggest that annual real GDP growth slowed to just +0.4% in the third quarter of 2025. In July, the Central Bank had still expected the Russian economy to grow by +1.6% year-over-year in the third quarter.

The Russian Ministry of Economic Development, however, estimated that Russia’s economic growth still reached +0.6% in the third quarter (Moscow Times). The BOFIT research institute of the Finnish Central Bank and Dr. Alexander Shirov, director of the Institute for Economic Forecasting at the Russian Academy of Sciences, were among those who commented on the current slowdown in the Russian economy.

IEF-RAS: Economic growth will slow to just +0.6% by 2025

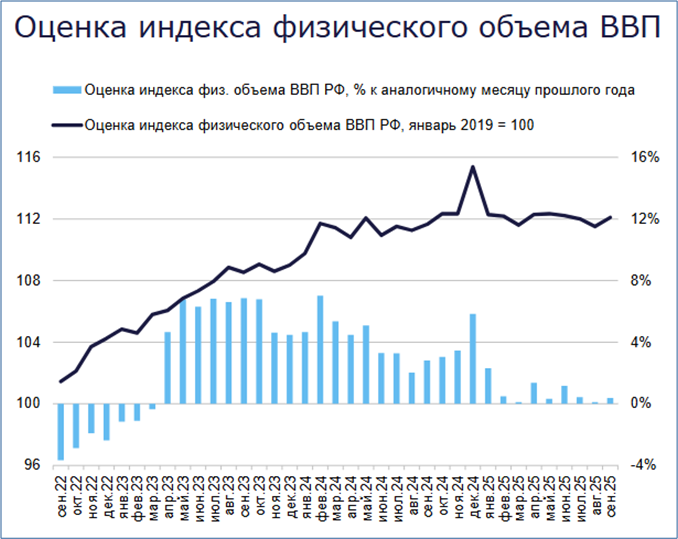

On November 10, the “Institute of Economic Forecasting of the Russian Academy of Sciences” published a new estimate of the seasonally adjusted trend in real gross domestic product in Russia. The following chart from the Institute shows that aggregate economic output has largely stagnated so far in 2025.

In September 2025, seasonally adjusted real GDP was 0.2 percent lower than in January 2025, according to preliminary calculations by the Institute of the Russian Academy of Sciences. It thus stood at the level already reached in May 2024.

Compared to the previous month of August, GDP grew by +0.5% in September 2025, according to the IEF. Compared to September 2024, it rose by +0.4% in September.

Estimate of seasonally adjusted real gross domestic product

Blue bars: Year-over-year changes in %

Black line: Real gross domestic product index, January 2019=100

Institute of Economic Forecasting of the Russian Academy of Sciences;

IEF-RAS: Short-term Forecast Russian GDP, 11/10/25

According to the IEF Institute’s estimate, the GDP level reached in December 2024 was undershot by 2.8 percent in September 2025. Due to the high comparative figure in the fourth quarter of 2024, the IEF now expects Russia’s aggregate economic output in the fourth quarter of 2025 to stagnate compared to the same quarter of the previous year (+0.0%). For 2025 as a whole, the institute estimates that GDP will be only 0.6 percent higher than in 2024.

BOFIT notes a “sluggish” development of the Russian economy

In its weekly report “BOFIT Weekly,” the BOFIT research institute of the Bank of Finland provides the following overview of Russia’s economic development in recent months and the deterioration of the operating environment for the Russian economy:

“The Russian economy has continued to grow only slowly in recent months. This picture of macroeconomic development remained unchanged in September. Even in light of slowing growth, there have been few signs so far of a reduction in structural economic imbalances. The situation in the labor market remains tight. Inflationary pressures are mounting. The sanctions recently imposed on Russia by Western countries are further worsening conditions for the Russian economy.”

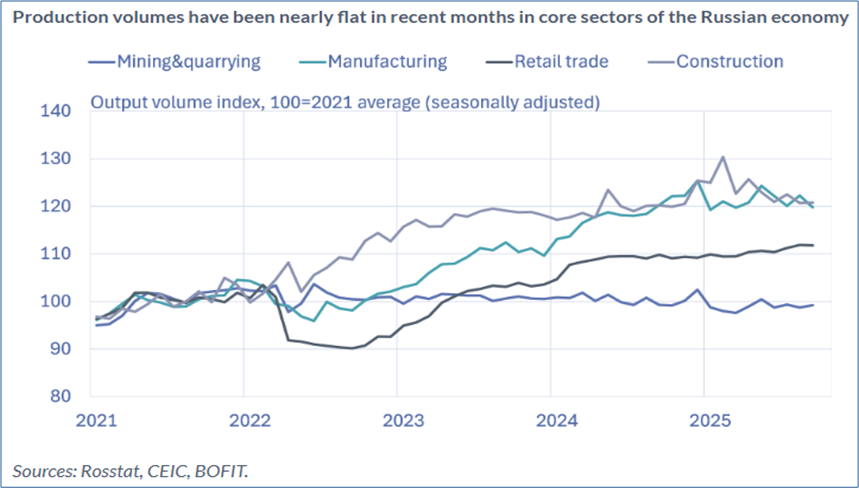

The Finnish Central Bank’s Institute refers to data already published by the Federal State Statistics Service (Rosstat) on the development of the “core sectors” of the Russian economy. The index, which covers the production volume of Russia’s five most important economic sectors, grew by +0.8% year-on-year in September, according to BOFIT. While growth was slightly higher than in previous months, there are no signs of a broad economic recovery. From January to September, year-over-year growth in the core sectors index stood at +0.9%.

Regarding the development of total output in the Russian economy—that is, real gross domestic product—BOFIT cites an estimate from the Russian Ministry of Economic Development. According to this estimate, GDP rose by +0.9% year-on-year in September. From January to September, annual growth reached +1.0%.

BOFIT illustrates the production trend in four “key sectors” of the Russian economy with the following figure:

Production Indices in Core Sectors of the Russian Economy

: Mining/Extraction of Raw Materials, Manufacturing, Retail, Construction

(seasonally adjusted, 2021=100)

BOFIT Weekly: Russia’s economic development remains sluggish and continues to suffer from imbalances, 11/07/25

Regarding production trends in the selected sectors, BOFIT notes:

The decline in production in the raw materials sector (“Mining & Quarrying”) came to a halt in September. However, in the period from January to September 2025, production fell by around 2% year-on-year (lower blue line).

In the “manufacturing” sector, growth this year was virtually limited to the defense and pharmaceutical industries. In nearly all other sectors of “manufacturing,” production from January to September was below the previous year’s level (green line).

Construction output stagnated in September (upper gray line). Residential construction, in particular, has performed weakly in recent months. It declined by 12% in the third quarter compared to the previous year.

Growth in retail sales slowed in September after peaking in August, but was still about 2% above the previous year’s level (middle dark gray line). Private household consumption continues to be supported by rising wages amid high employment levels. The average monthly wage rose by 4% in real terms in August compared to the previous year. The unemployment rate has long remained at a historically low level of around 2%.

Alexander Shirov: The economy has cooled significantly

Dr. Alexander Shirov, director of the Institute for Economic Forecasting at the Russian Academy of Sciences (IEF-RAS), also sees the Russian economy entering a “cooling-off phase” in 2025. He analyzed the overall development of the Russian economy since the start of the war in Ukraine in October in an article for “Stimul Magazine,” which has now also been published on his institute’s website.

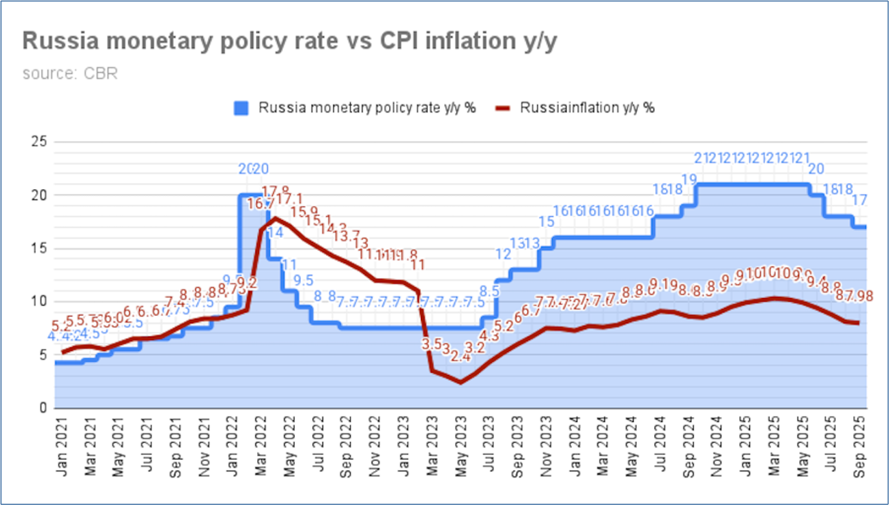

In the article, Shirov notes that by the fall of 2025, a trend had developed in the Russian economy toward a split between a growing military-industrial sector and a shrinking civilian sector. An analysis of developments in 2024 and 2025 shows that the main reason for the slowdown in economic activity was not the central bank’s high key interest rate “in itself,” but rather the prolonged period during which the key interest rate remained at a record high. From August 2024 to June 2025, the key interest rate stood at over 10 percent in real terms.

Russia’s key interest rate in percent per year (blue line)

and the annual increase in consumer prices in percent per year

bne IntelliNews: Russia’s central bank cuts rates by 50bp to 16.5%, 10/29/25

According to Shirov, the decline in production had spread to more and more sectors of the economy. While initially companies in the automotive, building materials, and railway industries were primarily affected, the decline in production had spread to the entire civilian industrial sector by the fall of 2025 (see Finmarket.ru for industrial production in September). Industry suffered the most from the persistently extremely high key interest rate. However, negative trends were also emerging in the service sector. The economy had cooled significantly.

However, Shirov considers a decline in real gross domestic product in the fourth quarter of 2025 compared to the fourth quarter of 2024 to be “unlikely.” He stated this in late October in an interview with Expert.ru. Shirov expects that, due to the increase in the value-added tax starting in 2026, there will be a slight but still noticeable recovery in consumer demand in the fourth quarter. Together with the growth contribution from the defense sector, this will be sufficient to keep the annual GDP growth rate above zero in the fourth quarter.

More growth requires lower interest rates and an “economic stimulus package”

In his article for Stimul magazine, Shirov highlights that a “balance” must be found between fiscal and monetary policy decisions as a challenge for Russian economic policy:

“A cut in the key interest rate is inevitable. The question is how quickly this will happen. Much will depend on fiscal policy. The smaller the fiscal stimulus, the more the key interest rate will have to be cut.”

In his article, Shirov emphasizes that lowering the key interest rate alone is not enough to revive the economy. The current situation in the second half of 2025 requires the development of an additional package of measures to support certain companies and economic sectors.

At the same time, he points out that, given the low unemployment rate, such economic stimulus carries the risk of renewed wage increases and accelerating inflation. For this reason, spending on the “economic stimulus package” should not exceed approximately 1 percent of gross domestic product. That would be sufficient to ensure low but positive economic growth through the end of 2026.

According to Shirov’s assessment, financing such a program is possible through a redistribution of budget expenditures within the framework of budget execution in 2026. In the short term, an increase in the budget deficit may be necessary.

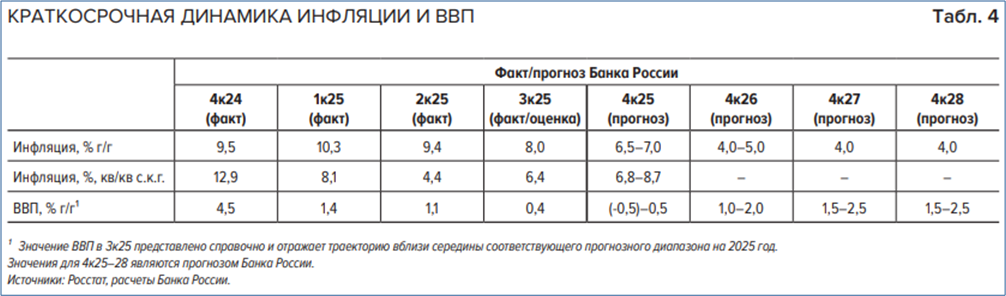

Russian Central Bank: Inflation rate fell to +8.0 percent in the third quarter

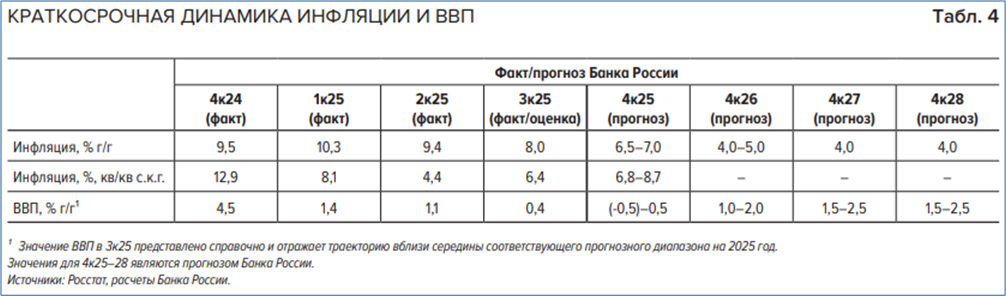

In its commentary on its “Medium-Term Forecast,” the Russian Central Bank first analyzes quarterly inflation trends. It examines, on the one hand, the rise in the consumer price index compared to the same quarter of the previous year (annual inflation rate; first row of the following table). However, the Central Bank also analyzes how the Consumer Price Index has developed on a seasonally adjusted basis compared to the previous quarter (SAAR = Seasonally Adjusted Annual Rate; second row of the table below; see also the Central Bank’s monthly report “Inflation in Russia”).

Quarterly trends in inflation and gross domestic product

1) The GDP figure for the third quarter of 2025 serves as a reference value and reflects a trend close to the midpoint of the corresponding forecast range for 2025. The figures for the fourth quarter of the years 2025 through 2028 are based on the Russian Central Bank’s forecast; sources: Rosstat; calculations by the Russian Central Bank;

Russian Central Bank: Commentary on the Russian Central Bank’s Medium-Term Forecast, Nov. 6, 2025

Regarding the rise in the consumer price index in the third quarter of 2025, the Central Bank notes:

- The annual inflation rate was +8.0% in the third quarter (first row of the table above). It was thus lower than the Central Bank had forecast in July (+8.5%). This was due to a decline in fruit and vegetable prices in July and August that exceeded the seasonal average.

- Compared to the second quarter of 2025, however, inflation accelerated in the third quarter of 2025 as expected, primarily due to the indexation of energy tariffs in July. The seasonally adjusted annualized inflation rate compared to the second quarter rose to +6.4% in the third quarter (second row of the table above).

The central bank notes that its baseline scenario takes into account one-time inflationary factors effective in October, including the situation in the fuel market, the VAT increase from 20% to 22% in 2026, the increase in the recycling fee for imported vehicles, higher indexation rates for energy costs in the coming years, and other announced tax and tariff changes.

The central bank estimates that the upcoming increase in the value-added tax from 20% to 22% in 2026 will contribute 0.8 percentage points to the annual inflation rate. The price-driving effect of the tax increase is expected to be most noticeable primarily between December 2025 and January 2026.

The central bank’s inflation target of 4 percent will be reached no earlier than the end of 2026

In the fourth quarter of 2025, the Central Bank estimates that the seasonally adjusted inflation rate will likely range from +6.8% to +8.7% year-over-year (second row of the table below). At the same time, the annual inflation rate in the fourth quarter is expected to be between +6.5% and +7.0% (first row).

By the end of 2026, annual inflation is projected to fall to +4.0% to +5.0%, according to the central bank’s forecast. It will then stabilize near the central bank’s target annual inflation rate of +4.0%.

Annual GDP growth fell to just +0.4% in the third quarter of 2025

According to the Central Bank, current data indicate that annual real GDP growth slowed to just +0.4% in the third quarter of 2025 (see the third row of the table below). In July, the Central Bank had expected a much smaller slowdown in growth to +1.6% for the third quarter. The Russian Ministry of Economic Development, however, estimated that Russia’s economic growth still reached +0.6% in the third quarter (Moscow Times).

Quarterly trends in inflation and gross domestic product

1) The GDP figure for the third quarter of 2025 serves as a reference value and reflects a trend close to the midpoint of the corresponding forecast range for 2025. The figures for the fourth quarter of the years 2025 through 2028 are based on the Russian Central Bank’s forecast; sources: Rosstat; calculations by the Russian Central Bank;

Russian Central Bank: Commentary on the Russian Central Bank’s Medium-Term Forecast, Nov. 6, 2025

In the fourth quarter of 2025, annual GDP growth is expected to range between -0.5% and +0.5%, according to the Central Bank’s assessment. It therefore also considers a decline in aggregate economic output compared to the previous year to be possible. It cites the so-called “base effect” as the reason: in the fourth quarter of 2024, there was a temporary GDP increase of +4.5%.

Year-over-year in 2025/2024, GDP will grow by only 0.5 to 1.0 percent

Given this quarterly GDP trend, the central bank expects year-over-year GDP growth for 2025/2024 to reach only +0.5% to +1.0%.

The so-called “positive output gap”—the excess of aggregate demand over aggregate supply resulting from the pressure of restrictive monetary policy on aggregate supply—is expected by the central bank to close in the first half of 2026.

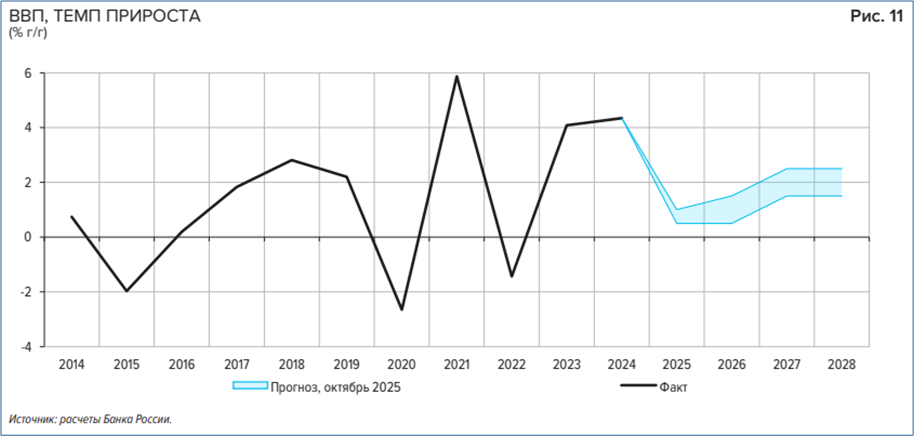

According to its medium-term forecast, the Central Bank expects GDP growth of between +0.5% and +1.5% for the full year 2026. It anticipates that the Russian economy will reach its growth potential of +1.5% to +2.5% in 2027. Economic growth is expected to remain within this range in 2028.

Real Gross Domestic Product; from 2025, Central

Bank forecast, year-over-year change in percent

According to Alexander Shokhin, president of the Russian Union of Industrialists and Entrepreneurs (RSPP), “2 to 2.5 percent is the optimal growth rate for an economy that is not overheating.” With this level of growth, it would be possible to solve a truly wide range of problems, Shokhin said in a TV interview in late September (Finmarket.ru).

Recommended reading:

- The Moscow Times: Russia’s Economy Could Slip Into Recession by Year-End, Central Bank Warns, 11/07/25

- Finam.ru; Dmitry Nikitin: Post-Mortem: The Russian Economy Has Slowed Down. How Can We Revive It? 11/06/25

- Joe Blogs: Russian Disaster; 11/09/25; Russia Failing: Chapters:0:00 Intro 0:59 Fabricated metal 2:09 Military transport 2:59 Manufacturing output 4:06 Industrial output 4:48 Civilian industry 5:41 Total output 6:38 Workforce 8:35 Technology 9:32 Civilian sector 10:30 Investment 11:49 Summary; 11/04/25

- fr.de, Lars-Eric Nievelstein: Putin’s Plan Backfires – Russia’s Economy Expected to Slide into Recession Faster; 11/09/25; Warning for Putin – Russia’s Economy Shows Significant Weakness, 11/03/25

- Finance.rambler.ru; Irina Agaltsova: How will the Russian economy perform in November? 11/04/25

- MK.ru; Igor Bokov: Experts discuss Elvira Nabiullina’s views on the signs of a recession, 11/02/25

- CMASF: Trends of the Russian Economy, 11/01/25

- Gaidar Institute: Yevgeny Goryunov on the risks of a drastic cut in Russia’s key interest rate, 10/31/25

- russland.capital: Nabiullina sees no signs of a recession in the Russian economy, 10/31/25

- russland.capital: Russia’s GDP rose by 1 percent in nine months, 10/30/25

- The Moscow Times: Russia’s Economic Growth Slows for Third Straight Quarter – Ministry Data, 10/30/25

- Alfa Investor: Economy and Trends: Slowdown in Retail: Declining Demand or Just a Temporary Effect?, 10/30/25

- t-online: Trump’s Sanctions. The Consequences Are Already Visible, 10/30/25

- Interfax.com: Russian GDP grows 0.9% in Sept, 1.0% in 9M – Econ Ministry, 10/29/25