Russia's growth is likely to remain at just under 1 percent

Author: Klaus Dormann

This year, there has been much speculation as to whether the Russian economy entered a “technical recession” in the first half of the year, defined as a decline in real gross domestic product for two consecutive quarters compared to the previous quarter. On September 12, the Russian Federal State Statistics Service (Rosstat) gave the “all-clear.” In a preliminary estimate, it announced that Russian economic output in the second quarter of 2025 rose by 0.4 percent on a seasonally adjusted basis compared to the first quarter of 2025, following a 0.6 percent decline in the first quarter (Interfax).

Nevertheless, the “recession debate” has by no means died down. Several institutes and analysts did not adopt Rosstat’s estimates but are sticking to their own estimates regarding the development of aggregate economic output. For example, the research institute of the state-owned “Vnesheconombank” ("Bank for Foreign Economic Relations," VEB) states in a table in its "September GDP Index" published on November 11 that real GDP fell by 0.4 percent quarter-on-quarter in both the first and second quarters. This would mean that Russia experienced a “technical recession” in the first half of the year. The VEB Institute estimates that aggregate economic output stagnated at a depressed level (0.0%) in the third quarter.

Kommersant: The debate over the economic situation is likely to intensify

In Kommersant, Artem Chugunov cites the following examples, among others, regarding the controversial assessment of the Russian economy’s output performance:

The Telegram channel “Hard Numbers” expects seasonally and calendar-adjusted growth of “around 1%” for the third quarter.

Dmitry Polevoy (JSC Astra Asset Management), however, estimates seasonally adjusted growth at just +0.15% compared to the previous quarter.

In its “Analysis of Short-Term GDP Trends,” based on data from early November (prior to the release of Rosstat’s GDP data) that the seasonally adjusted monthly GDP in September 2025 had returned to the level of May 2024. The high level reached in December 2024 was 2.8% below that level in September.

Chugunov summarizes the current economic trend as follows: The economy is growing sluggishly. There are still no sectors in sight that are driving a new growth cycle. Growth in the third quarter was “minimal.” It is driven by consumption, which is not expected to grow sustainably. Industrial production and investment have slowed significantly more than the overall figures suggest.

Chugunov says: “Against this backdrop, the debate over the economic situation is likely to intensify further.”

CMASF: A recession is “highly likely” in 2026

The Moscow-based economic research institute “Center for Macroeconomic Analysis and Short-term Forecasting (CMASF)” is adding fuel to the recession forecasts. It predicts that the Russian economy will “most likely” enter a recession by July of next year. According to the institute’s “Analysis of Macroeconomic Trends” published on November 17, this is signaled by one of the institute’s “leading indicators.”

According to the institute, the likelihood of a recession has increased, among other things, because a “systemic banking crisis” has become more probable. The Institute cites a decline in the current account surplus and a steady decline in the real gross domestic product growth rate as further reasons for its recession forecast.

Currently, however, the institute sees no signs that the impending recession will last for more than four consecutive quarters.

Unlike Rosstat, the CMASF estimates that Russia’s seasonally adjusted real gross domestic product fell by 0.3 percent in the first quarter of 2025 compared to the previous quarter (Rosstat: -0.6%). In the second quarter, GDP stagnated completely (0.0%; Rosstat: +0.4%). In the third quarter, it rose minimally by 0.1 percent.

The institute notes that key sectors on the demand side have shrunk significantly, particularly investment. Production in key industries has also fallen rapidly. The institute expects that it will soon become clear which trend will prevail—slow growth or a decline in production.

The “prolonged, extremely restrictive monetary policy” is weighing on investment

Regarding investment trends, the CMASF notes that investment peaked in mid-2024. Since then, it has been declining. Investment has already covered three-quarters of the distance back to its last low point in 2022. If the current trend continues, investment levels in a few months would be even lower than in 2022, when investment was severely depressed by sanctions. Now, however, the slowdown in investment is not caused by sanctions, but by the “prolonged, extremely restrictive monetary policy.”

The CMASF points out that industrial profitability continued to decline in the second quarter. The difference between the key interest rate and the industrial profitability rate has reached a historic high. This clearly hinders investment activity and the expansion of supply.

Growth in real disposable income continued at a slower pace

According to the CMASF, seasonally adjusted real disposable income rose by an average of 1.7 percent per month in the third quarter (2nd quarter: +3.0%).

The rise in real wages also continued (2nd quarter: +0.7% on a monthly average). In July, real wages rose by 0.9 percent. In August, however, they fell by 0.9%.

Private consumption fell for the first time in September

After seasonally adjusted household consumption rose by 0.5% in July and 0.6% in August, it fell by 0.1% in September, according to the CMASF. The institute notes that it is not entirely clear whether this actually represents a decline (exacerbated by high interest rates on consumer loans) or merely a statistically unrecorded shift from traditional grocery purchases toward meals from restaurants.

According to the CMASF, developments in the food sector have proven to be the “main problem area.” Seasonally adjusted real growth in the second and third quarters averaged only 0.1% per month here. For other goods and services, the trend over the past two quarters has not been as weak.

Central Bank Advisor in Video: There Was No “Technical Recession”

The Russian Central Bank has since responded to the widespread criticism of its restrictive monetary policy with, among other things, a video explanation. Kirill Tremasov, an advisor to the Central Bank president, noted on November 11 in his blog “What Does It Cost?” that growth in the Russian economy had resumed in the second quarter of 2025. According to Rosstat, GDP in the first quarter of this year

fell by 0.6% compared to the previous quarter. However, the economy had already returned to growth in the second quarter, rising by 0.4%. Therefore, one could say that there was “formally” no technical recession in Russia (Lenta.ru).

Tremasov presented the following chart showing the seasonally adjusted trend in Russia’s real gross domestic product. On the far right of the chart, the decline in aggregate economic output in the first quarter of 2025 and the subsequent increase in the second quarter are visible. Rosstat is expected to publish a preliminary estimate of seasonally adjusted GDP growth for the third quarter on December 12.

Index of seasonally adjusted real gross domestic product

https://www.youtube.com/watch?v=rRC-1xIKXEE&t=369s

Russian Central Bank: What Is a Recession? // “What Does It Cost?” with Kirill Tremasov

How will annual growth develop in the fourth quarter and for the full year 2025?

Regarding the expected trend in the fourth quarter of 2025, Tremasov noted a few days later at an economic conference in Yekaterinburg that there had been a sudden surge in growth in the fourth quarter of last year. The basis for comparison for this year’s output growth is therefore very high in the fourth quarter. Consequently, a slight decline in gross domestic product in the fourth quarter of 2025 compared to the previous year cannot be ruled out. However, a small increase is also possible (Interfax.ru). In its latest medium-term economic forecast, the Central Bank already estimated that the annual rate of change in aggregate economic output in the fourth quarter of 2025 is likely to range between -0.5% and +0.5%.

Russian analysts expect growth of only 0.5 to 1.0 percent in 2025

Igor Nikolaev, a senior researcher at the Institute of Economics of the Russian Academy of Sciences, also commented on the expected development of the annual growth rate in the fourth quarter in MK.ru. The annual increase in gross domestic product in the third quarter, calculated by Rosstat, of just 0.6% came as no surprise to Nikolaev. He commented on the development as follows:

“The economic slowdown began as early as last year, as the quarterly data shows, even though we achieved overall growth of 4.3% in 2024.

The downward trend is unmistakable and will continue to intensify, primarily due to recent decisions to increase the tax burden (in particular, the VAT rate hike from 20% to 22%) and the expected 0.5% decline in fixed investment in the baseline scenario through 2026.”

Igor Nikolaev concludes that Russia’s GDP will grow by no more than 0.7 to 0.8 percent in 2025. He assumes that high government spending will prevent the economy from slipping into the “red.”

Andrey Glushkin, a board member of the Moscow branch of the business association “Delovaya Rossiya,” offers a similar assessment of the situation. Commenting on the slowdown in annual growth to just 0.6 percent in the third quarter, he says:

“Some of the previous growth drivers have weakened. The economy is under pressure from sanctions. However, it remains stable and is restructuring logistics, domestic investment, and technological development. By the end of the year, we can expect moderate growth in the range of about 0.5 to 1%. While these are modest figures, they form a solid foundation for a gradual recovery.”

Gluschkin expects the growth rate to remain low in 2026. He considers a transition to stronger economic growth possible if “external conditions” improve, investment rises, and measures to support domestic demand continue.

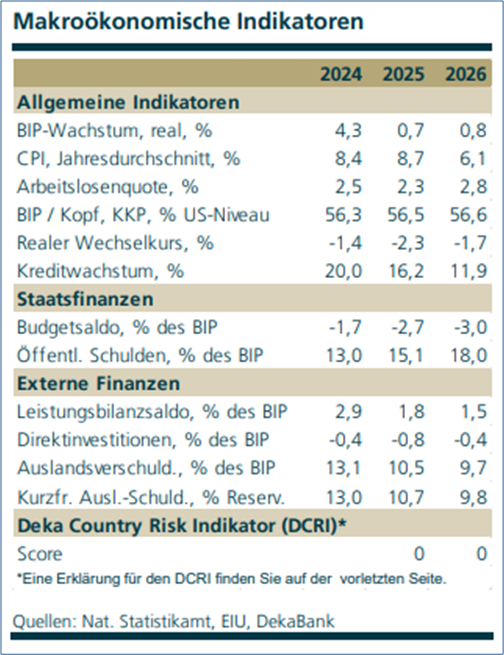

DekaBank also expects growth of just under one percent in 2025 and 2026

Frankfurt-based DekaBank, the securities firm of the German savings banks, also emphasizes in the November issue of its publication “Emerging Markets Trends” that the Russian economy is not “on the verge of collapse.” However, the Russian government’s financing options are being hampered by low oil prices, tightened sanctions, and the discounts demanded by buyers of Russian oil.

DekaBank estimates that government spending on the military and security sectors is likely to account for around 40% of total central government spending by 2025. However, the growth momentum for the Russian economy driven by the military sector has lost steam.

DekaBank also believes that Russia’s private companies are being “held back by restrictive monetary policy.” As a result, economic activity has slowed significantly. It is expected to stagnate in the coming quarters. In 2025, the Russian economy is likely to grow by only 0.7%, and in 2026 by barely more—0.8%.

Nevertheless, DekaBank believes the Russian Central Bank will only “cautiously” lower the key interest rate—currently at 16.5 percent—in the coming months. The Central Bank does not want to reignite inflationary pressures. On an annual average for 2025, the rise in consumer prices will still be slightly higher at +8.7 percent than in 2024 (+8.4%). DekaBank does not expect the annual inflation rate to fall to +6.1 percent until 2026.

DekaBank also addresses Russia’s demographic challenges. These are exacerbated by the high number of war casualties (which the government does not disclose) and the wave of emigration. The supply of available labor remains tight. The annual average unemployment rate is projected to fall to 2.3 percent in 2025. An increase to 2.8 percent is not expected until 2026.

DekaBank Forecasts

DekaBank: Emerging Markets Trends:

Russia: No Concessions in Negotiations Despite New Oil Sanctions, 11/06/25

The budget deficit will rise to 2.7 percent of GDP in 2025

In 2024, Russia’s budget deficit had still been limited to 1.7 percent of GDP. This year, DekaBank expects an increase to 2.7 percent of GDP.

According to DekaBank, the liquid portion of the sovereign wealth fund, which is used to plug budget gaps, has shrunk by about half since 2022. It currently stands at around $48 billion (approx. 2% of GDP). If the current pace of spending growth continues, the fund will be depleted within the next two years.

New Western sanctions are driving the budget deficit even higher

DekaBank also analyzes how the new sanctions against Russia’s two largest oil exporters, Rosneft and Lukoil—imposed by the U.S. government and the EU at the end of October—are likely to impact the situation. The two companies account for about half of Russia’s total crude oil exports. At the same time, the U.S. held talks with the main buyers of Russian crude oil (China, India, Turkey) to encourage them to reduce their imports from Russia.

DekaBank expects that the new sanctions will place additional burdens on the Russian federal budget. To date, approximately 23% of total budget revenue has come from the oil and gas sector. According to DekaBank’s assessment, the revenue shortfall now expected due to the new sanctions is likely to cause Russia’s budget deficit to rise to 3.0 percent of GDP in 2026, even though increases in value-added tax and other levies were approved in the 2026 budget.

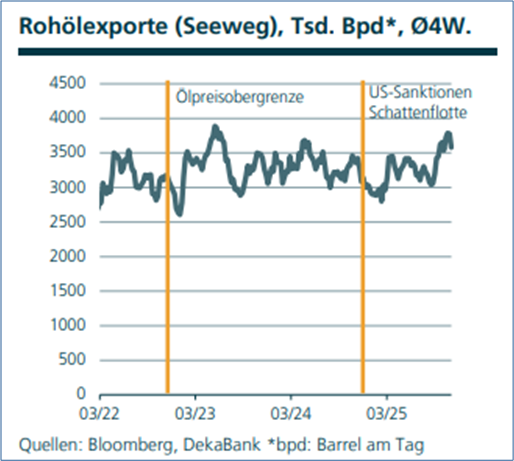

DekaBank questions whether a sustained decline in Russian oil exports is likely

DekaBank points out that the following chart showing the trend in Russian crude oil exports by sea indicates an initial decline in Russian exports.

However, from DekaBank’s perspective, the sustainability of this decline remains an open question. The two major “rounds of sanctions” against Russian oil exports to date—the introduction of the oil price cap in 2022 and the U.S. sanctions against the Russian “shadow fleet” in 2025— only had an effect on Russian oil export volumes until Russia developed “circumvention measures.”

DekaBank: Emerging Markets Trends:

Russia: No Concessions in Negotiations Despite New Oil Sanctions, 11/06/25

However, DekaBank assumes that it will become increasingly difficult and costly for Russia to find “loopholes” to circumvent the sanctions. It expects India and Turkey to become “significantly more cautious” regarding the conclusion of supply contracts with Russia. China, however, will largely maintain its imports from Russia.

Recommended reading:

- MK.ru; Igor Bokov: On the Brink of Stagnation and Recession: What Awaits the Russian Economy Next Year? 11/21/25

- Joe Blogs Videos: Russia’s $20 Billion Disaster, Nov. 20, 2025; Russian oil glut disaster, The International Energy Agency warns that global supply is rising far faster than demand, Nov. 18, 2025

- MarketMinute: Russian Stock Market Navigates Sanctions and Geopolitical Headwinds in Late 2025, 11/20/25

- Kommersant, Artem Chugunov: Persistent Components of Inflation Are Rising, 11/20/25

- Prime.ru; Alexey Leron, independent financial and economic expert, Doctor of Economics: The economic trap: Why there is money but no growth. Economist Leron: Economy enters a phase of low growth amid high spending, Nov. 20, 2025

- Deutsche Welle, Olga Lebedeva: The Russian State Duma has passed the budget for 2026–2028 in its third reading, Nov. 20, 2025; Vedomosti.ru; Ksenia Kotchenko: The State Duma has approved the draft budget for the next three years in its second reading, Nov. 18, 2025

- RIAMO, Oksana Dyachenko: From “growth on steroids” to a moderate slowdown: How the Russian economy will end 2025, Nov. 18, 2025

- Raiffeisenbank Focus Pocus: Oil and gas exports remain stable in September and October; 11/18/25.

- Raiffeisenbank; Focus Pocus: Inflation in October: A positive surprise. 11/17/25

- MK.ru; Igor Bokov: “Exports Stalled”: Due to U.S. sanctions, tankers carrying Russian oil cannot be unloaded. Analysts have assessed the risks to the market posed by Russian oil stuck in tankers. 11/17/25

- Interfax.ru: The European Commission has lowered its forecast for Russian GDP growth to 0.8% in 2025 and 1.1% in 2026, 11/17/25.

- CMASF: Analysis of Macroeconomic Trends; Nov. 17, 2025; D.R. Belousov (CMASF): “On the State of the Russian Economy and Some Forecast Parameters” (with video, starting at 8:04); Presentation at the Annual Conference of the Presidential Management Training Program 2025, Nov. 14, 2025

- Kommersant, Artem Chugunov: Russia’s economy is slowing down. Analysts continue to discuss its current state, Nov. 16, 2025

- Crisis Watch, Video: Putin’s $207 Billion GAMBLE: Why Russia’s Economy is Headed for Disaster, 17 min., Nov. 16, 2025

- Olga Belenkaya: Inflation in Russia was significantly lower than expected in October, Nov. 16, 2025

- AP; David McHugh: A slowing wartime economy pushes the Kremlin to tap consumers for revenue. Russia’s economy has slowed after two years of robust growth fueled by the war in Ukraine, Nov. 15, 2025

- Dmitry Polevoy, Astra Asset Management JSC; Finam.ru: Russia’s inflation data provided a pleasant surprise, Nov. 14, 2025

- Finmarket.ru: According to the Ministry of Economic Development, slowing inflation in Russia expands the scope for further monetary policy easing, Nov. 15, 2025

- Finmarket.ru: The Central Bank of the Russian Federation estimates the structural deficit of the 2025 budget following the amendments to be significant, 11/14/25

- Finmarket.ru: Inflation in Russia stood at 0.5% in October, 11/14/25; Finam.ru: Inflation in Russia accelerated to 0.5% in October, 11/14/25

- Interfax.com: VAT hike in Russia expected to have main impact in Jan, 11/14/25

- Vedomosti.ru: Nabiullina identified the Central Bank’s main mistakes. These include a delayed increase in the key interest rate in 2023 and a communication error in 2024, 11/14/25; russland.capital: Nabiullina: Interest rate should have been raised sooner in 2023, 11/16/25

- Frankfurter Rundschau; Florian Neumann: “They wanted those billions in black money”: Author explains Germany’s Russia mistake; Interview with Birgit Jennen, author of the book “Putin’s Puppets,” Deutscher Wirtschaftsbuchverlag; 11/20/25

- Michael Thumann, Die Zeit, on “Der Standard Podcast”: What happens if Putin dies? Thumann (author of the books “Revanche” and “Eisiges Schweigen flussabwärts”) explains how firmly Putin remains in power despite heavy losses in the war and a faltering economy, 11/18/25