Russia's government has cut its growth forecasts by a surprisingly large margin

Author: Klaus Dormann

The Russian government has drastically lowered its growth forecasts for 2025 and 2026. In its April budget plan, it had still projected a 2.5% increase in gross domestic product for the current year. As recently as late August, Finance Minister Anton Siluanov assured that the economy would grow by at least +1.5% in 2025.

However, in its recently published budget plan, the government now expects economic growth of only +1.0% this year. According to the new plan, growth in 2026 will be barely higher (+1.3%). Previously, however, sustained strong growth of +2.4% had been expected for next year. This means the government has nearly halved its economic growth expectations for 2025 and 2026 since the spring.

In their “Joint Economic Assessment” published on September 25, the five leading German economic research institutes now also expect economic growth in Russia to slow to just +1.0% this year. Unlike the Russian government, however, they do not forecast a slight recovery in growth to +1.3% for next year, but rather a further decline in output growth to just +0.8%.

The London-based development bank EBRD, on the other hand, expects the Russian economy to grow by +1.3 percent in 2026, as does the Russian government, according to its “Regional Economic Prospects” report, also published on September 25. This would mean it would grow at the same rate as in the current year.

Economy Minister: Growth is slowing but continuing

Economy Minister Maxim Reshetnikov presented the new socioeconomic forecast for 2026–2028 at a government meeting (government.ru/en; Monocle.ru):

“Following extremely high growth of over 4 percent in 2023 and 2024, GDP growth is expected to slow in 2025 and 2026. This is due to lower inflationary pressures, which are essential for balanced and sustainable growth rates in the coming years. Crucially, positive growth rates are expected to persist throughout the entire forecast period, with a gradual acceleration anticipated in 2027 and 2028.”

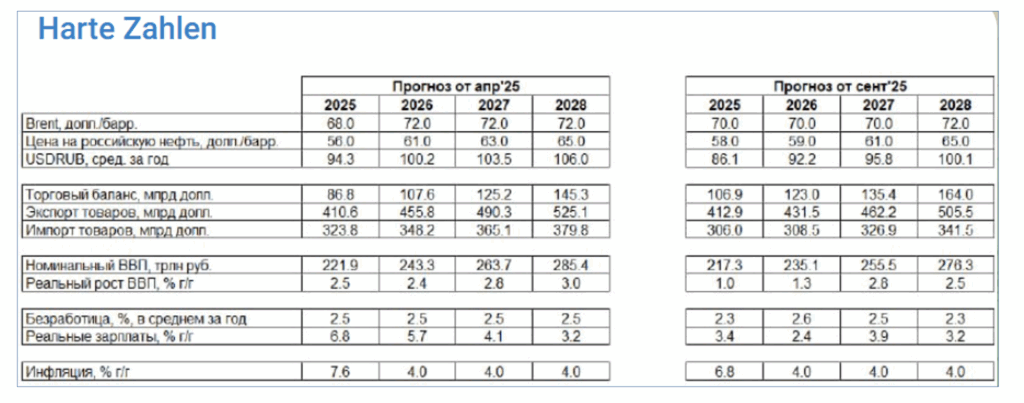

The following table from the Telegram channel “Harte Zahlen” compares the government’s April forecasts (left column) with its new September forecasts (right column).

The new oil price forecast assumes that the Brent oil price will stagnate at $70 per barrel from 2025 to 2027. At the same time, the Urals oil price is expected to rise gradually from $58 to $61 (see the first two rows of the table below).

The government expects a gradual weakening of the ruble (third row). The price of one dollar is expected to rise from 85.1 rubles per dollar in 2025 to around 100 rubles per dollar in 2028. The minister pointed out that in April, the government had still anticipated a significantly stronger depreciation of the ruble (see the left side of the table).

Comparison of the Ministry of Economic Development’s April and September Forecasts

“Hard Numbers”: Comparison of the Ministry of Economic Development’s April and September forecasts, 09/24/25

Unemployment remains very low, while incomes are rising much more slowly

According to the Minister of Economic Development, the unemployment rate will remain very low through 2028 (2025: 2.3 percent, third row from the bottom in the table above). In 2026, it could rise to 2.6% of the labor force due to slowing economic growth. The Ministry of Economy expects that by 2028, the unemployment rate will return to the 2025 level of 2.3% of the labor force (Finam.ru).

However, the main driver of private consumption growth—the rise in real wages—will already decline to +3.4 percent in the current year 2025 (second-to-last row of the table above). In April of this year, the government had still expected a rise in real wages twice as strong, at +6.8 percent. According to the new forecast, the rise in real wages next year will also be only about half as high as previously expected, at +2.4 percent (Finam.ru). Along with real wages, total real household income will also rise much more slowly than previously expected: in 2025, it will increase by only +3.8% (instead of +6.2%) and in 2026 by +2.1% (instead of +4.8%).

The government assumes that the rise in consumer prices will drop to 6.8 percent by the end of 2025 and that the Central Bank’s inflation target of 4.0 percent will be reached in the following years (last row of the table).

Private consumption will grow much more slowly as early as 2025, and investment will even decline slightly in 2026

The lower growth in real incomes is reflected in the decline in growth in the retail and services sectors.

Real retail sales still rose by 7.7% in 2024. In the current year, 2025, they will grow by only 2.5% (April forecast: +6.6%). For 2026, the Ministry forecasts growth of just 1.1%.

According to the forecast, the volume of fee-based services for the population will grow by 2.6% in 2025 (after +4.3% in the previous year). In 2026, growth in the services sector is expected to more than halve, reaching just 1%.

According to the minister, the volume of investment will decline slightly next year. However, the government expects investment to rise again starting in 2027. briefly-news.com reports: According to the 2025 forecast, growth in fixed investment will slow to +1.7%. In 2026, the volume of investment is expected to decline by 0.5%.

Speaking before the Federation Council’s Economic Policy Committee, the minister stated that the more moderate trend in GDP growth rates amounts to a “controlled soft landing.” The slowdown in inflation opens up room for monetary policy easing, which is important for long-term economic growth.

Continued high growth potential: “The economy can grow by 3%”

According to Finmarket.ru, a spokesperson for the Ministry of Economic Development commented on the significant slowdown in economic growth, noting that the ministry had not previously anticipated such a rapid economic cooling. However, he emphasized:

“So far, we see no reason to revise our assessments of the Russian economy’s growth potential. The economy can grow by 3%; it has reserves.”

The government now expects economic growth to accelerate to +2.8% in 2027, as previously planned. For 2028, it had expected growth to rise to +3.0%. According to the spokesperson, however, this forecast has now been lowered to +2.5% “in light of various factors, including a prolonged period of restrictive monetary policy.”

The forecasts from the government and the central bank are now more aligned

The Russian Central Bank has so far been noticeably more skeptical about the Russian economy’s growth prospects than the government. In its July medium-term forecast, the bank expects GDP growth in Russia of only 1.0 to 2.0% this year and 0.5 to 1.5% in 2026. These wide ranges have so far remained below the government’s growth forecasts (2025: +2.5%, 2026: +2.4%).

Now, the government’s new growth forecast for 2025, at +1.0%, has slipped to the lower end of the central bank’s forecast range. The government’s forecast for next year, at +1.3%, is, however, quite close to the upper end of the central bank’s forecast range (see the second row of the table below).

According to the government’s forecast, the rise in consumer prices will fall to 6.8% in December 2025. This expectation falls within the central bank’s forecast range, which anticipates an inflation rate between 6.0 and 7.0 percent. Starting at the end of 2026, both the government and the central bank expect the central bank’s target inflation rate of 4.0 percent to be reached (first row of the table below).

Comparison of forecasts by the Ministry of Economy and the Central Bank

“Hard Numbers”: Comparison of forecasts by the Ministry of Economy and the Central Bank, 09/24/25

The Telegram channel “Hard Numbers” has compared the forecasts of the Ministry of Economy and the Central Bank for the following indicators in the table above: Inflation rate, % year-on-year; Gross domestic product, % year-on-year; Urals oil price, dollars per barrel; Trade surplus, billion dollars

BOFIT: Fiscal and monetary policy requirements must be balanced

The weekly report from the BOFIT research institute of the Bank of Finland, dated September 26, outlines the Russian government’s current economic policy challenges as follows:

“Russia’s economic policy continues to balance between war-driven loose fiscal policy and the tight monetary policy necessary to stabilize the economy. Government spending and state-backed loans have expanded drastically in recent years.

The preliminary budget plan for 2026–2028 forecasts a continued budget deficit, although at the same time efforts are being made to increase government revenue through tax hikes.

In recent months, the central bank has begun to gradually lower its historically high key interest rate as inflationary pressures have eased due to slowing demand growth. However, the slowdown in growth has also raised concerns in Russia that the economy is sliding into a recession, prompting calls for a faster shift toward a more accommodative monetary policy.”

The budget deficit was much higher than planned in the first eight months of 2025

BOFIT reports on the federal budget’s performance so far in 2025:

According to the budget revised in June, federal budget expenditures were expected to rise by 5% this year. However, from January through August, expenditure growth already stood at +21% compared to the previous year.

Revenues, on the other hand, grew more slowly than expected.

The federal budget deficit widened. The budget deficit originally planned for this year was 1.2 trillion rubles, but in January–August it had already reached 4.2 trillion rubles (about 2% of GDP).

Finance Minister Siluanov has already announced that the government will take on more debt this year than expected.

The federal budget will remain in deficit in the coming years as well

BOFIT reports on the current status of the budget deliberations:

The Ministry of Finance presented its proposals for this year’s budget and the budget framework for the next three years to the government this week. The budget proposals are scheduled to be debated in the State Duma next week.

The budget framework for the coming three-year period calls for an increase in federal budget spending of 4% per year from 2026 to 2027 and 7% in 2028. Revenues are also expected to rise, but the federal budget will run a deficit throughout the entire three-year period. The deficit for 2026 is estimated at 3.8 trillion rubles (1.6% of GDP) (see also finmarket.ru).

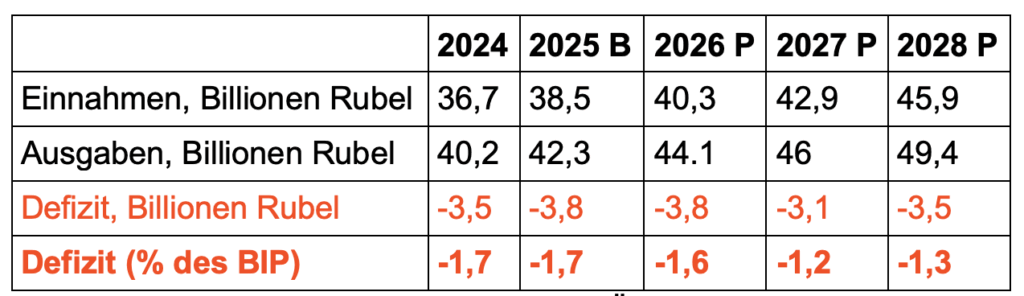

Federal Budget Development from 2024 to 2028

B) Figures for 2025 based on the approval of amendments to the 2025 Budget Law on June 24, 2025 P) Figures for 2026–2028 based on the Ministry of Finance’s preliminary budget of September 24, 2025 Sources: Russian Ministry of Finance, BOFIT

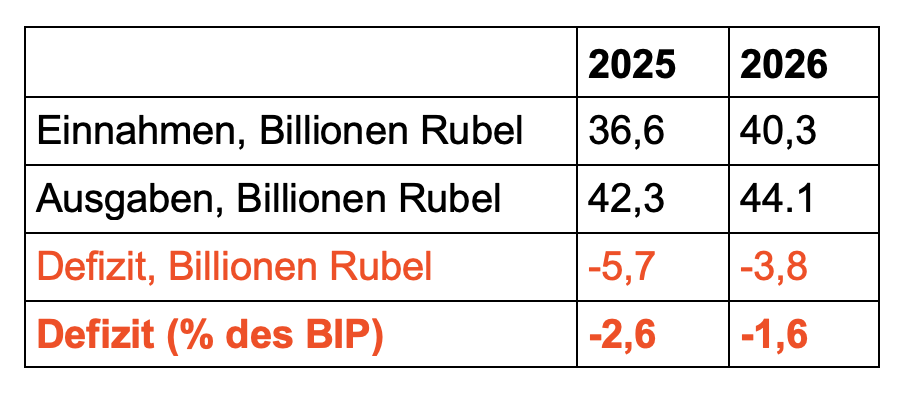

New estimate: In 2025, the deficit will rise to 2.6 percent of GDP

In its weekly report on the table above, BOFIT notes that, according to media reports, there is a new estimate regarding the development of the federal budget in 2025. According to this, the budget deficit in 2025 will not, as indicated in the table above as of June 24, reach 1.7 percent of GDP again, but is expected to rise to 2.6 percent of GDP. According to Interfax.com, this is provided for in changes to the 2025 budget prepared by the Ministry of Finance. Interfax reported on this on September 24:

This year’s increase in the deficit of 3.8 trillion rubles by 1.9 trillion rubles to 5.7 trillion rubles corresponds to a reduction in estimated budget revenues for the current year by 1.9 trillion rubles, from 38.5 trillion rubles to 36.6 trillion rubles. Budget expenditures for the current year are still estimated at 42.3 trillion rubles (see also: Moscow Times; Reuters: Key Parameters of the Draft Federal Budget of the Russian Federation for 2026–28, 09/25/25)

Budget trends for 2025 and 2026 according to Interfax and BOFIT

Interfax.com: Russian budget deficit will increase to 2.6% from 1.7% of GDP in 2025 – Finance Ministry amendments, September 24, 2025; BOFIT, Bank of Finland: Russia struggles to balance fiscal and monetary policy demands, September 26, 2025

VAT will be raised by about 10 percentage points to reduce the deficit

To reduce the budget deficit, the Ministry of Finance has proposed, among other measures,

increase the VAT rate by 2 percentage points to 22 percent starting in January 2026. The standard VAT rate was last raised in 2019 from 18 percent to 20 percent. A reduced rate of 10 percent will continue to apply to socially essential goods (including basic foodstuffs and medications).

According to Russland.capital, the additional tax revenue from the VAT increase is estimated at 1.3 trillion rubles. Total VAT revenue is projected to reach 15.7 trillion rubles, accounting for about 40 percent of all budget revenue. On the expenditure side, according to the “Moscow Times/Reuters,” spending allocated for the military, police, and intelligence services in the 2026 budget will account for 38% of total spending, compared to the 41% planned for this year.

Alfa Bank: Budget deficit and higher VAT fuel inflation

Analysts at Alfa-Bank expect that the fiscal policy planned for 2025 and 2026, with the planned VAT increase from 20 to 22 percent, will drive up prices. They explain this as follows:

“Spending in 2025 will amount to 42.3 trillion rubles, compared to the originally projected 45 trillion rubles. This is better than expected and a sign that the Ministry of Finance is attempting to control spending trends.

However, this has not reduced inflation risks: The deficit for 2025 is projected at 5.7 trillion rubles, which is higher than originally planned. Consequently, the government will need to borrow 2.6 trillion rubles on the market in the fourth quarter of 2025.

In 2026, the deficit will be lower at 3.8 trillion rubles, but will still be higher than the average for 2022–2024 (3.3 trillion rubles).

Budget revenues are expected to increase by 3.7 trillion rubles in 2026 compared to 2025. The main contribution will come from raising the VAT rate to 22%. The increase will generate additional revenue of 1.2 trillion rubles. …

Ultimately, the budget has two sides: a cautious reduction in spending and a simultaneous increase in the tax burden. … The VAT increase and the high budget deficit will drive prices up.”

Central Bank Governor Elvira Nabiullina sees things differently.

Nabiullina: “We currently view the draft budget as disinflationary”

Central Bank President Elvira Nabiullina also commented on the consequences of the planned VAT increase. At the 22nd International Banking Forum in Moscow, she said, according to Finam.ru:

“We currently view the draft budget as disinflationary.”

There will likely be a short-term price reaction to the VAT increase. The one-time effect could “to some extent influence the pace of the decline in inflation expectations.” However, she noted that VAT was also raised by two percentage points in 2019 and that the reaction to that, in her view, had been “moderate.”

The Central Bank President explained her support for a balanced budget as follows:

“For the central bank, a balanced budget is much better than a rising deficit. It is better for fiscal stability, inflation, and interest rates. Why? Because the more the government increases its debt, the higher we have to keep interest rates, and the less room there is for lending to the private sector.”

Recommended reading:

- Deutsche Welle.com/en; Arthur Sullivan: How Russia’s mounting economic woes could force Putin’s hand, 09/25/25

- bne Intellinews, Ben Aris: Russia’s 2026 budget draft cuts military spending for the first time, introduces new taxes, 09/25/25

- Russland.capital: Ministry of Economy has lowered its forecast for GDP growth in 2025, 09/25/25; Russland.capital: Three-year budget draft presented: VAT hike to counter spending pressure, 09/25/25

- Alfa Investor: The Ministry of Finance has presented the draft budget: Revenues are rising, but risks remain, 09/26/25

- briefly-news.com: Moscow signals “mild stagflation” as growth forecasts are drastically cut, 09/25/25

- briefly-news.com: Russia’s 2026–2028 draft budget: Higher VAT, stricter rules for SMEs, and a political stalemate, 09/25/25

- Moscow Times; Reuters: Key parameters of the draft federal budget of the Russian Federation for 2026–28, 09/25/25

- Moscow Times; Reuters: How has the structure of Russian federal budget spending changed? 09/25/25

- Yahoo Finance; Reuters: Russia’s state debt-servicing costs will rise by 23% in 2026, 09/25/25

- Finmarket.ru: Russia’s budget deficit will amount to 1.6%, 1.2%, and 1.3% of GDP in 2026, 2027, and 2028, respectively. Revenue, Expenditures, Public Debt; September 25, 2025

- Finmarket.ru: According to the Russian Ministry of Finance, the budget deficit will rise to 2.6% of GDP in 2025, September 24, 2025

- Interfax.com: Russian budget deficit will increase to 2.6% from 1.7% of GDP in 2025 – Finance Ministry amendments, 09/24/25

- Kommersant, Vadim Visloguzov: The VAT rate will be raised to 22%, 09/24/25.

- Moscow Times: Russia Moves to Raise VAT by 2% as Budget Deficit Swells, 09/24/25

- Vedomosti, Ksenia Kotchenko: The Ministry of Economic Development has lowered its forecast for Russian economic growth in 2025 to 1%. The slowdown in GDP comes against a backdrop of falling inflation and demand, 09/24/25

- Finmarket.ru: The Ministry of Economic Development has lowered its forecast for Russian GDP growth in 2025 to 1%, September 24, 2025

- Finmarket.ru: The inflation forecast for Russia in 2025 has been lowered to 6.8%, 09/24/25

- Vedomosti: The government approved the draft budget for three years, 09/24/25

- Kommersant, Vadim Visloguzov: VAT rate to be raised to 22%, 09/24/25

- Government.ru/en: Government meeting; The agenda: draft federal budget and allocations for state extra-budgetary funds, socio-economic development forecast, and draft guidelines for the integrated state monetary and credit policy for 2026–2028…, September 24, 2025

- Alfa Investor: Central Bank summary: Why the regulator lowered the interest rate to 17%, 09/24/25.

- Finmarket.ru: Industrial production growth in Russia slowed to 0.5% in August, 09/24/25

- Vladimir Milov, Free Russia Foundation: What’s Happening to the Russian Economy? PDF, 25 pages, 09/24/25; Vladimir Milov video: Is the Russian economy in recession or not yet? 09/19/25

- Deutsche Welle.ru; Oleg Loginov: German Companies in Russia: No Rush to Leave? 09/23/25; Deutsche Welle, Russian Service: Oil, Gas, and Sanctions: What Awaits Russia and Germany After the Failure of the Partnership; Talk show “Auf den Punkt” with Elena Barysheva: Guests: Michael Harms – Managing Director of the German Committee on Eastern European Economic Relations; Anastasia Tikhomirova – DIE ZEIT; Sergey Vakulenko – Senior Fellow at the Carnegie Berlin Center for Russian and Eurasian Studies, 44 min., 09/18/25