Russia's Economic Outlook

Author: Klaus Dormann

For about a year now, Russia’s overall economic output has been virtually stagnant. In November 2025, according to a preliminary estimate by the Institute for Economic Forecasting at the Russian Academy of Sciences, real gross domestic product fell back to the level reached a year earlier.

However, high inflation did cool significantly over the course of 2025. By March 2025, the annual increase in consumer prices had accelerated to 10.3 percent. It then declined month by month. In December 2025, the year-over-year price increase was projected to be just under 6 percent (December 2024: +9.5%). However, the annual average inflation rate for 2025 is likely to have been slightly higher than in 2024. In early December, analysts surveyed by the central bank expected consumer prices to rise by 8.8 percent year-over-year in 2025/2024 (2024/2023: +8.4 percent).

Sergey Aleksachenko (born 1959), Deputy Finance Minister of Russia from 1993 to 1995 and subsequently Deputy President of the Russian Central Bank until 1998, calls the reduction in the inflation rate the “most important achievement” of the Russian government in 2025. “This was the result of coordinated measures by the Ministry of Finance and the Central Bank of Russia,” says Aleksachenko, who emigrated to the U.S. in 2014 for political reasons, praising his successors at the Ministry of Finance and the Central Bank in an analysis for the London-based “New Eurasian Strategies Centre.”

Ministry of Economic Development: In 2025, the economy grew by only 1.0 percent

On December 26, Russia’s statistics agency Rosstat published economic data for November. The Ministry of Economic Development estimated that real gross domestic product grew by only 1.0 percent in the first 11 months of 2025 compared to the previous year. Since late September, the Ministry has also expected a slowdown in the growth of aggregate economic output from 4.3 percent in 2024 to just 1.0 percent for the full year 2025. The Federal State Statistics Service (Rosstat) will present an initial estimate of Russia’s economic growth in 2025 in February, following the release of economic data for December.

IEF-RAS: In November, GDP fell by 1.3 percent compared to October

Most analysts expect that the Russian economy’s output growth last year likely fell to between 0.5 percent and 1.0 percent. Among them is the Institute of Economic Forecasting of the Russian Academy of Sciences (IEF-RAS). In mid-December, it had already lowered its forecast for real GDP growth in 2025 to 0.7 percent in its “Quarterly Economic Forecast.”

To supplement this quarterly economic outlook, the IEF also publishes a monthly “Analysis of Short-Term GDP Trends” with growth estimates. In November, due to the sharp rise in production in October, it had raised its estimate for year-over-year real GDP growth in 2025 compared to 2024 to +1.1 percent. However, in light of the weak economic performance in November, it revised this estimate down to +0.9 percent at the end of December.

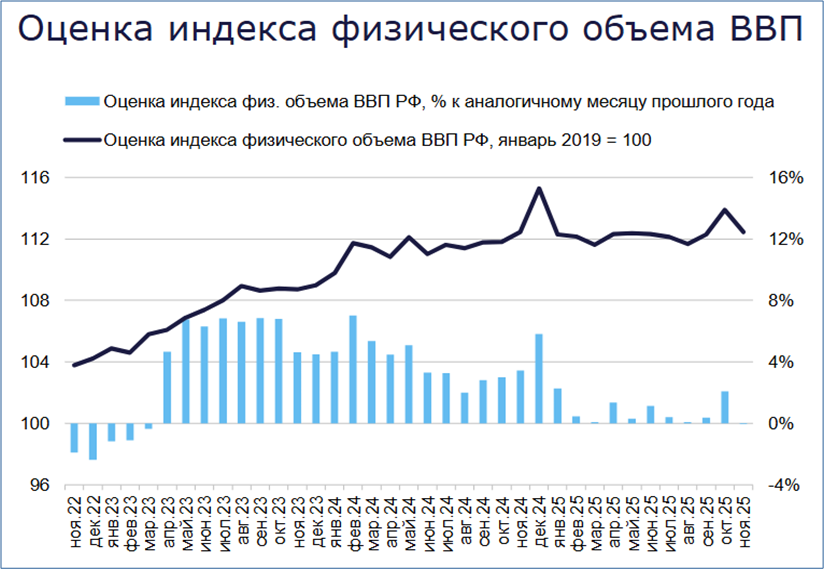

In its monthly “Analysis of Short-Term GDP Trends,” the IEF also publishes an estimate of the seasonally adjusted trend in aggregate economic output. The black line in the following figure shows that the seasonally adjusted index of real gross domestic product rose sharply in October compared to September (+1.4%). In November, however, total economic output fell again by 1.3 percent compared to October, according to the institute’s estimate. Apart from the strong increase in October, seasonally adjusted GDP remained virtually stagnant over the course of 2025.

Estimate of the real gross domestic product

index: blue bars: change from the same month of the previous year in %

; black line: real GDP index, January 2018=100; seasonally adjusted

IEF-RAS: Analysis of short-term GDP dynamics: December 2025, Dec. 30, 2025

As shown by the blue column series in the figure, real gross domestic product stagnated in November 2025 at the level reached in the same month of the previous year due to the sharp decline compared to October. In October 2025, however, it had still risen by around 2 percent year-on-year.

IEF-RAS: Industrial production fell in November compared to the same month last year

The Institute for Economic Research of the Russian Academy of Sciences highlights the following regarding industrial development in November: Overall, industrial production fell by 0.7% in November compared to the same month of the previous year (following a 3.1% increase in October 2025).

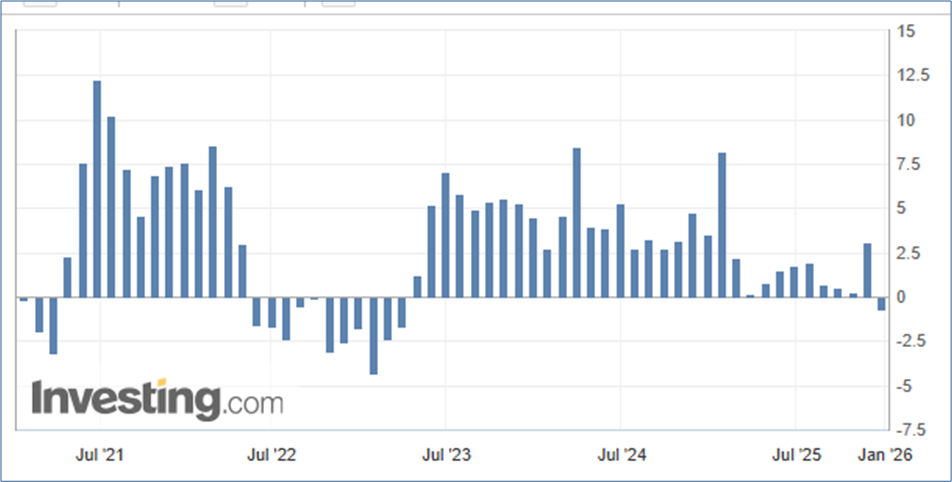

Industrial production (January 2021 to November 2025)

Year-over-year change in percent

Investing.com: Russia Industrial Production YoY, Dec. 26, 2025

In November 2025, production in the “manufacturing sector” fell by 1.0% year-over-year. The industrial sector “mining and extraction of raw materials,” however, recorded a 0.7% increase in production.

In the first eleven months of 2025, however, the “Mining and Raw Materials Extraction” sector saw a 1.5% year-over-year decline in production. At the same time, production in the “Manufacturing” sector rose by 2.6%. Including other industrial sectors, annual growth in total industrial production for the period from January to November 2025 reached only 0.8 percent. In 2024, industrial production had still risen by 5.1 percent in the first eleven months.

Industrial

Production Trends: Year-over-Year Changes in %

Source: Rosstat, Finam calculations

Defense production has continued to grow strongly

Annual production growth in the “manufacturing sector” was driven in the first eleven months by production in defense-related industries. Olga Belenkaya, chief economist at the brokerage firm FINAM, notes in a detailed analysis that, when comparing the first eleven months of 2025 and 2024, industrial production continued to rise sharply in the following three “defense-related” sectors:

- “Other transport equipment”; including aircraft, ships; excluding motor vehicles: +29.5%

- Metal products; excluding machinery and equipment: +13.9%

- Computers, electronic, and optical products: +13.0%

Production of pharmaceuticals and materials for medical purposes grew by 15.6 percent.

At the same time, however, Belenkaya points to significant fluctuations in the production of the “military-industrial complex” in recent months. Following a sharp increase in defense production in October, which boosted total industrial production by 3.1 percent year-over-year, its annual growth slowed in November. Production of metal products (excluding machinery and equipment) actually fell by 1.3% year-over-year in November, after rising by 19.4% in October. Growth in the production of “other transportation equipment” (including shipbuilding, aerospace, and aviation) slowed to 6.4% after a 41% increase in October.

Production in many major “civilian” industrial sectors, however, declined

For numerous consumer goods, however, there were year-over-year declines in production from January through November (including food, beverages, clothing, leather goods, and furniture).

Production in the chemical industry also declined, as did production in the machinery sector (excluding the defense industry). Fewer materials were produced for the construction industry. The sharpest decline continued to be recorded in the production of motor vehicles and trailers (-23.6%).

Very mixed trends in other “core sectors” of the economy

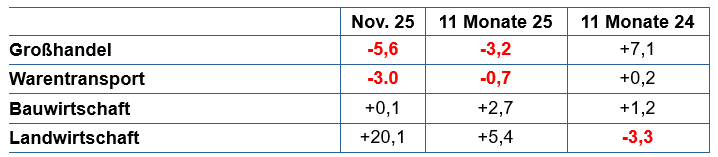

In wholesale trade, the decline in production intensified in November (-5.6% year-on-year; following -2.5% in October and +2% in September 2025). Belenkaya points to falling gas exports and weak import momentum.

In the freight transport sector, the year-over-year decline in production accelerated to 3.0 percent in November. In the first eleven months, transport volume was 0.7 percent lower than in the previous year.

In the construction sector, production still grew by 2.7 percent in the first eleven months of 2025. In November, however, it was only 0.1 percent higher than a year ago. The sharp decline in the production of key construction materials points to the beginning of a downward trend in construction output.

Agriculture recorded well above-average growth rates in 2025 (November: +20% year-over-year, October: +7%). In the first eleven months, its production rose by 5.4 percent. This more than offset the 3.3 percent decline in agricultural production in the previous year.

Production trends by sector

: Year-over-year changes in %

Source: Rosstat, Finam calculations

Consumer demand supported economic growth in 2025

The IEF-RAS notes that economic growth in November 2025 was supported by rising consumer demand. Purchasing impulses stemmed from the increase in the value-added tax effective January and also from the change in the calculation of recycling fees for car purchases effective December 1.

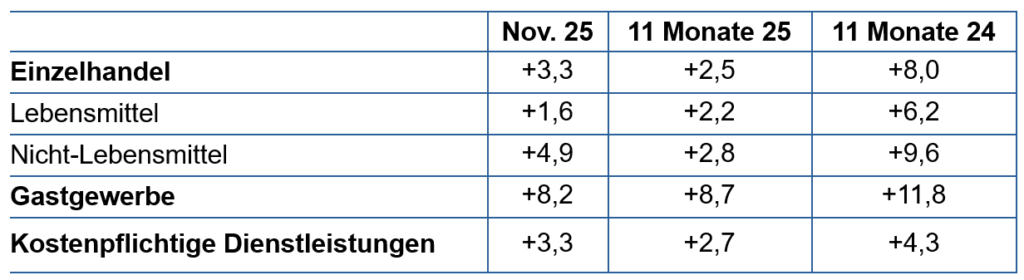

Real retail sales rose by 3.3% year-over-year in November 2025, real sales in the hospitality sector by 8.2%, and real sales of services to the public by 3.3%.

Production trends by sector

: Year-over-year changes in %

Source: Rosstat, Finam calculations

The IEF-RAS observed that over the course of 2025, the “gaps” between the development of consumer demand and production in the core sectors of the economy widened. For example, retail sales of food rose by 2.2% year-over-year in the first eleven months of 2025, while food production in Russia fell by 0.7% over the same period. In the hospitality sector, sales rose by 8.7% in the first eleven months, while beverage production fell by 3.6%. According to the IEF’s assessment, these gaps were offset by higher imports due to the relatively strong ruble exchange rate.

Real incomes and real wages have continued to rise significantly so far

According to the IEF, growth in consumer demand in the current situation is primarily determined by income trends and the propensity to save.

According to Rosstat, real disposable income rose by 9.2% year-over-year in the period from January to September 2025. Real wages grew by 4.7% year-over-year in the period from January to October 2025 (by 6.1% year-over-year in October 2025). In the coming months, the IEF expects slower real wage growth. Competition among job seekers has intensified.

The IEF cites a slowdown in income growth due to the “normalization” of the labor market situation as a “risk” to economic development in 2026. With slower income growth, growth in consumer demand will also decline. According to the IEF, other risks include a real decline in government spending and lower investment.

Slight easing in the labor market despite record-low unemployment rate

The unemployment rate reached a historic low of 2.1% in November, down from 2.2% in October. The number of unemployed remained near its lowest level at 1.6 million.

However, according to Olga Belenkaya, some indicators point to a slight easing in the labor market (due to slowing economic growth). For instance, the number of job openings has fallen. The average duration of job searches increased in November from 5.5 to 5.7 months (the highest level since May 2024).

Labor market studies indicate increased competition for jobs. The number of applications per job opening rose to 8.1 in November. This was nearly double the figure from a year ago, which was 4.2 applicants per job.

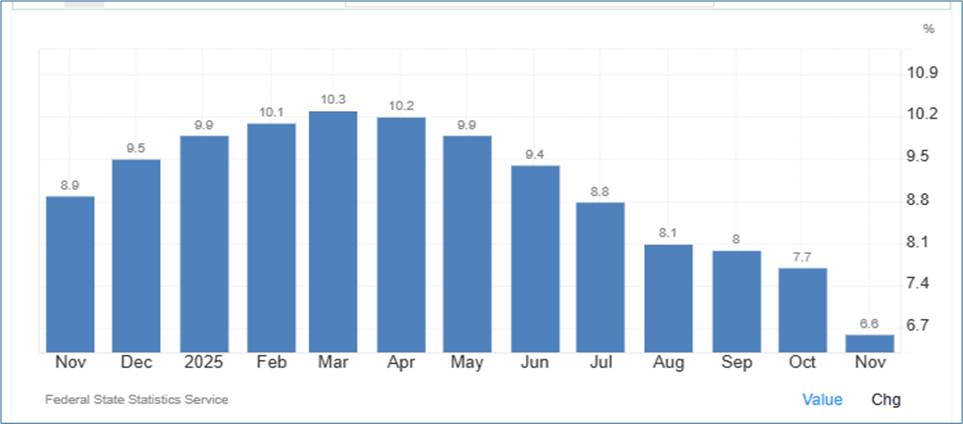

The annual inflation rate is expected to have fallen to just under 6 percent in December

Regarding current consumer price trends, Olga Belenkaya also considers it very likely that the annual inflation rate fell below 6 percent in December. This would be the lowest level in the past five years. The price increase would be below the Central Bank’s October forecast (6.5 to 7 percent). According to Belenkaya, the decline in the inflation rate gives the Central Bank room to further lower the key interest rate.

Year-over-year increase in consumer prices in %

Trading Economics: Russia Annual Inflation Rate

Belenkaya points to the “side effects” of maintaining a very restrictive monetary policy for an extended period: production in most sectors is stagnating or declining, companies’ financial situations are deteriorating, and investment is falling.

At the same time, however, Belenkaya cites a whole range of factors driving up prices that could force the Central Bank to exercise caution when cutting the key interest rate:

- The value-added tax was raised from 20% to 22% at the beginning of the year (with the scope of taxpayers expanded to include small businesses).

- The recycling fee on new car purchases has been raised.

- The cost of housing is rising.

Aleksachenko: The most important achievement in 2025 was the reduction of inflation

Sergey Aleksachenko, a Russian economist who emigrated to the U.S. and served as Deputy Finance Minister and Deputy President of the Central Bank in the 1990s, offers the following assessment of Russia’s monetary and fiscal policy over the past year in an article for the London-based “New Eurasian Strategies Centre”:

“The Russian government’s most significant achievement in 2025 was reducing inflation from 9.5 percent to below 6 percent. This was the result of coordinated measures by the Ministry of Finance and the Central Bank.

In the first eleven months of 2025, the Ministry of Finance adhered to strict budgetary discipline and limited spending. The increase in the federal budget deficit compared to the previous year’s forecasts was mainly due to a decline in oil and gas revenues resulting from the ruble’s appreciation.

In addition, the Ministry of Finance made the highly unpopular decision to raise the VAT rate effective January 1, 2026. This measure will increase government revenue, reduce private demand, and have an additional disinflationary effect.

For its part, the Russian Central Bank kept its key interest rate at an extremely high level until June 2025. It subsequently cut it five times, but the cumulative reduction from 21 percent to 16 percent led only to a very moderate easing of monetary policy.”

Aleksachenko expects that the Central Bank will proceed with extreme caution when cutting interest rates in early 2026. However, he does not rule out further cuts to the key interest rate. A cut in the key interest rate to 12 to 13 percent could be seen, given the current inflation level, as a partial offset for the inflation slowdown already achieved.

Aleksachenko is skeptical about the Central Bank’s forecast that it will reach its inflation target of 4 percent by mid-2026. On the one hand, there is uncertainty regarding the future course of fiscal policy. It remains unclear how potential future declines in oil and gas revenues would be offset. On the other hand, a devaluation of the overvalued ruble is increasingly expected, followed by a renewed acceleration of inflation. An additional risk to price developments is the slight rise in inflation expectations among consumers and businesses in recent months.

The government sacrificed growth for more stable prices

Looking back at 2025, Aleksachenko notes that Russia’s economy is stagnating. However, he argues that the Russian government acted “rationally” in 2025. It “sacrificed” growth in order to curb inflation.

Aleksachenko cites the following causes for the economic slowdown in 2025:

- The increased tax burden

- Cuts to non-military budget spending

- High interest rates, which made borrowing significantly more expensive for businesses

Regarding the development of the national budget, Aleksachenko notes:

The appreciation of the ruble and the sanctions have led to a decline in oil and gas revenues of more than 25 percent and a decline in import tax revenues, which could continue to weigh on the revenue side of the budget in 2026 as well. Due to rising military spending and falling oil and gas revenues, the Russian state budget is “vulnerable” to the emergence of high budget deficits.

Outlook: “Sustainable growth” is unlikely

At the start of the new year, Aleksachenko sees the Russian economy under pressure from three factors.

“First, the war continues to tie up financial, material, and human resources.

Second, efforts to maintain macroeconomic stability require the continuation of a restrictive monetary policy and further cuts in civilian budget spending.

Third, sanctions are accelerating the technological obsolescence of capital goods.”

Aleksachenko therefore considers “sustainable growth” of the Russian economy unlikely.

In his view, a potential end to hostilities in Ukraine could also increase the risk of recession in the short term. Defense industry production could then decline, and household incomes could fall.

Recommended reading:

- Sergey Aleksachenko, New Eurasian Strategies Centre. London: The Price of Stability: What Awaits Russia’s Economy in 2026? Jan. 6, 2026; see also Aleksachenko: “Behind the Iron Curtain”

- Sergey Aleksachenko in an interview with Bogdan Bakaleyko: 2026; the hardest part is yet to come, review and forecasts; video, 46 min., Dec. 28, 2025

- Das Parlament: Economist Sergey Aleksachenko in an interview with Moritz Gathmann, freelance journalist: “Western politicians like to deceive themselves.” Former Russian Deputy Central Bank Chief Aleksachenko is skeptical about new EU sanctions against Moscow, 09/26/25

- German-Russian Chamber of Foreign Trade: Podcast “Tsars. Data. Facts” by Thomas Baier: 2026: Forecasts for Russia’s economy from German institutes and Russian analysts, Jan. 7, 2026

- The Guardian; Phillip Inman: Why Russia’s economy is unlikely to collapse even as oil prices fall, 01/10/26

- Profile.ru; Vladislav Grinkevich: We’re holding steady, we’re not falling: Russia’s economy is slowing down, but it turns out that’s how it’s supposed to be, Jan. 7, 2025

- Finam.ru; Evgeny Kogan: Investment Banker: Three Key Economic Trends at the Start of the Year, 01/07/25

- Information portal “Volkswahl” (www.vybor-naroda.org); Sergei Grechishnikov, political consultant: Russia 2026: A dialectical forecast of the country’s development, 01/06/26

- ukrinform.net: Further weakening of Russia’s economy to force it into peace talks – Sikorski. 01/06/25

- Interfax.ru: Primakov National Research Institute for World Economy and International Relations of the Russian Academy of Sciences: Russia and the World: Economic Trends 2026, Jan. 5, 2026 The Primakov National Research Institute for World Economy and International Relations of the Russian Academy of Sciences published its annual forecast “Russia and the World: 2026. Economy and Foreign Policy,” Jan. 5, 2026; IMEMO: Russia and the World: 2026. Economy and Foreign Policy. Annual Forecast / Project Directors: A. A. Dynkin, V. G. Baranovsky; Editors: G. I. Machavariani, I. Ya. – Moscow: IMEMO RAS, September 2025. – 202 pp., PDF

- Business newspaper VZGLYAD: The Russian economy has achieved ten record-breaking feats. Jan. 3, 2026

- FR.de; Bona Hyun: After massive losses: Russia’s economy could lose out on oil in 2026, 01/03/26

- TAZ; Mathias Brüggmann: Russian Oil Revenues. Prices Fall Below the Pain Threshold, Jan. 2, 2026

- Finam.ru: The Russian economy is in a cooling-off phase. What are the risks? Experts from the New Economic School on the economic outlook for 2026. 01/02/26

- MK.RU, Mikhail Smalzev: A wise Frenchman spoke about a hypothetical conflict between Russia and NATO. Economist Jacques Sapir: The Russian economy is performing well and is not preparing for a war with NATO. In an exclusive interview with the Hungarian newspaper “Hungarian Conservative” (translation: Inosmi), French economist and leading Russia expert Jacques Sapir analyzed the current economic situation in Russia and the prospects for a resolution to the Ukraine conflict, 01/01/26

- Anton Gerashenko, threads.com: In November, industrial output turned negative across the economy as a whole, Dec. 31, 2025

- Reuters, Nika Khutsieva: Russians curb New Year spending despite falling inflation, Dec. 31, 2025

- Reuters; The Bell: Russian pipeline gas deliveries to Europe have fallen to a half-century low, 12/30/255

- Focus online, Russian press review at the turn of the year by Christian Dobber: They affectionately call him “Donald.” Putin’s newspapers celebrate Trump as an ally in the fight against Europe, 12/30/25

- Russian Central Bank: Following its December 19 meeting, the Russian Central Bank publishes a summary of the key interest rate discussion, including: Summary of the discussion on key interest rates during the “quiet week” and during the meeting of the Bank of Russia’s Board of Directors on December 19, 2025; Dec. 29, 2025

- Vedomosti; The Central Bank noted the Russian economy’s return to balanced growth, Dec. 29, 2025

2025 Review, 2026 Outlook

- Prime.ru: Siluanov estimated Russia’s economic growth in 2025. 12/30/25

- Finmarket.ru: Siluanov expects the Russian federal budget deficit to amount to 2.6% of GDP by year-end. 12/30/25

- 1Prime.ru: Siluanov: The Russian economy will grow by 1% in 2025, and the budget deficit will reach 2.6% of GDP, 12/30/25

- MK.RU; Dmitry Dokuchaev, Georgi Stepanov: Economists forecast how GDP, inflation, and the ruble exchange rate will develop in 2026, 12/31/25

- Elitetrader; T-Investments, Mikhail Boldov: Will the economy fall into a recession or recover? Forecasts for the Russian economy in 2026, Dec. 30, 2025

- Russian Central Bank: New Year’s edition of the podcast #KudasmotritCB (Where the Central Bank Is Looking): What awaits us in 2026? How will inflation, the key interest rate, and the economy in general develop? Guests: Andrey Gangan, Director of the Central Bank’s Monetary Policy Department, and financial analyst Nikita Mitrofanov. Host: Alexey Antonov; video, 63 min., Dec. 29, 2025

- Kommersant: 2025 Year in Review; Dec. 29, 2025

- Kommersant: A Sea of “Black Swans.” Artem Chugunov on the dwindling room for “anti-shock” maneuvers in the Russian economy, Dec. 29, 2025; see: CMASF: Analysis of Macroeconomic Trends, Dec. 23, 2025

- Kyiv School of Economics: Russia Chartbook by KSE Institute — Rosneft-Lukoil Sanctions Bite; Budget Deficit Will Soar in December, Dec. 29, 2025

- Finam.ru; Natalia Asedova: From Slowdown to Recovery: What Awaits the Russian Economy in 2026? Results of the Current Year and Forecasts for 2026; Dec. 26, 2025

- globalmsk.ru: Experts Summarized Economic Results for 2025, Dec. 24, 2025

- MK.ru; Igor Nikolaev, Institute of Economics of the Russian Academy of Sciences: A Year of Unfulfilled Expectations: Economic Results for 2025, Dec. 24, 2025

- MK.ru; Lyudmila Alexandrova; Low growth, deceptive inflation, a strong ruble: The economic results for 2025 can be summarized. Experts discussed the main risks, the ruble outlook, the reality of inflation, and scenarios for 2026, Dec. 23, 2025