Russia: Key interest rate cut slightly to support growth

Author: Klaus Dormann

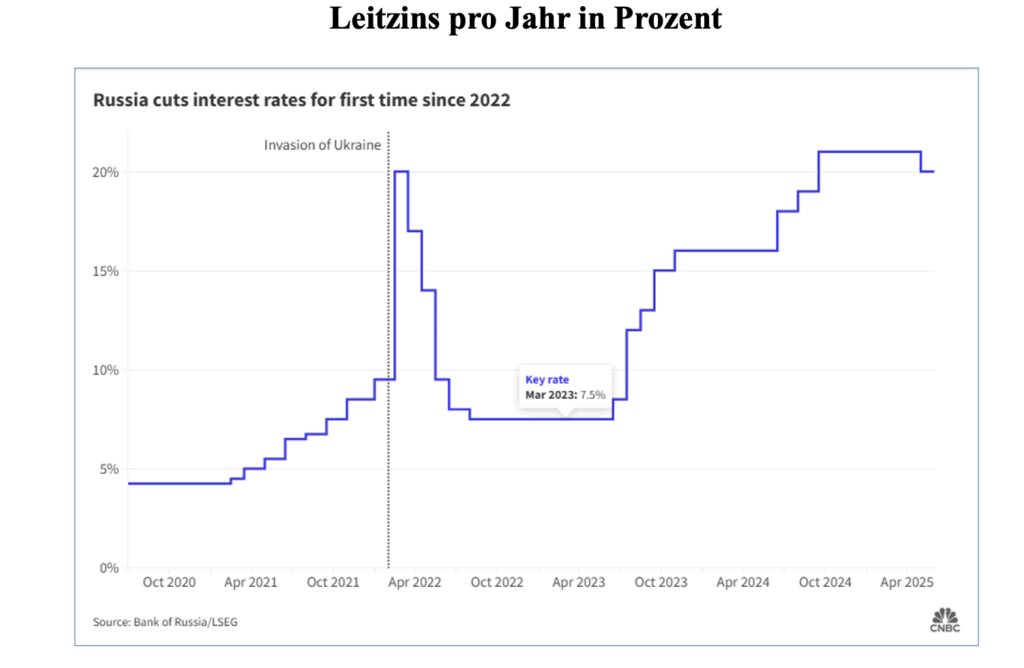

To curb inflation in Russia’s overheated wartime economy, the Russian Central Bank raised its key interest rate in October 2024 to a long-term high of 21 percent. Despite significant criticism from business leaders and politicians, it had maintained this rate until now. On June 6, however, to the surprise of many, it lowered the key interest rate to 20 percent (TradingEconomics). In a survey of analysts conducted by the business newspaper Vedomosti, just under two-thirds of participants had not expected a cut.

CNBC: Russia lowers interest rates to 20% in first cut since 2022 as inflation pressures ease, 06/06/25

Calls from politics and business for an interest rate cut

Economy Minister Maxim Reshetnikov had called on the Central Bank to cut interest rates ahead of the key rate decision: “We are counting on a timely easing of monetary policy.” This would allow the government to continue pursuing its 3% growth target in the future. The economy minister pointed out that an increasing number of industrial sectors are experiencing a decline in production. At the same time, the growth rate of consumer demand is also slowing.

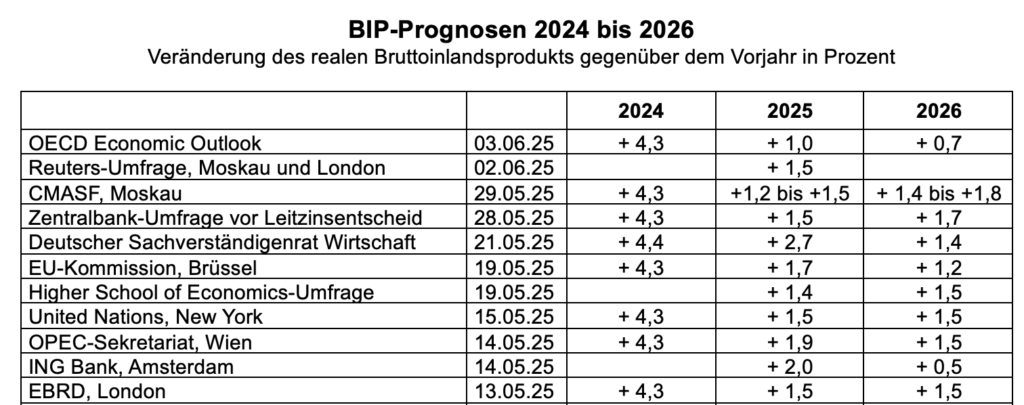

Analysts surveyed by Reuters in late May expect Russia’s economic growth to slow to 1.5 percent this year. In 2024, it had accelerated to 4.3 percent. The government expects economic growth of 2.5 percent in 2025 (FAZ, Reuters).

Alexander Shokhin, president of the Russian Union of Industrialists and Entrepreneurs (RSPP), stated in a TASS interview prior to the key interest rate decision that business leaders hoped the interest rate would be lowered. He noted that even a “symbolic cut” of one percentage point to 20 percent was important because it would signal a “return to normalcy.” Regarding the benefits of a cut to 19 percent, he said:

“A cut in the key interest rate to 19 percent would … create the conditions for maintaining economic growth rates at an acceptable level and minimizing the risks of increasing defaults and even bankruptcies due to the high cost of working capital and increased loan payments” (Russia.capital).

Central Bank: Monetary policy will remain “tight” for a long time

In a press release regarding the cut in its key interest rate, the Central Bank stated that the Russian economy is gradually returning to a balanced growth path. However, domestic demand continues to exceed the economy’s capacity to expand the supply of goods and services. The Central Bank still aims to reach its inflation target of 4 percent by 2026. This means monetary policy will remain tight for a long time to come.

Central Bank President Elvira Nabiullina also emphasized this in her statement. Given that the current pace of inflation in the Russian economy has slowed, the reduction of the nominal key interest rate from 21 to 20 percent does not represent a significant real easing of monetary policy conditions.

Current price inflation has already fallen significantly since the end of 2024

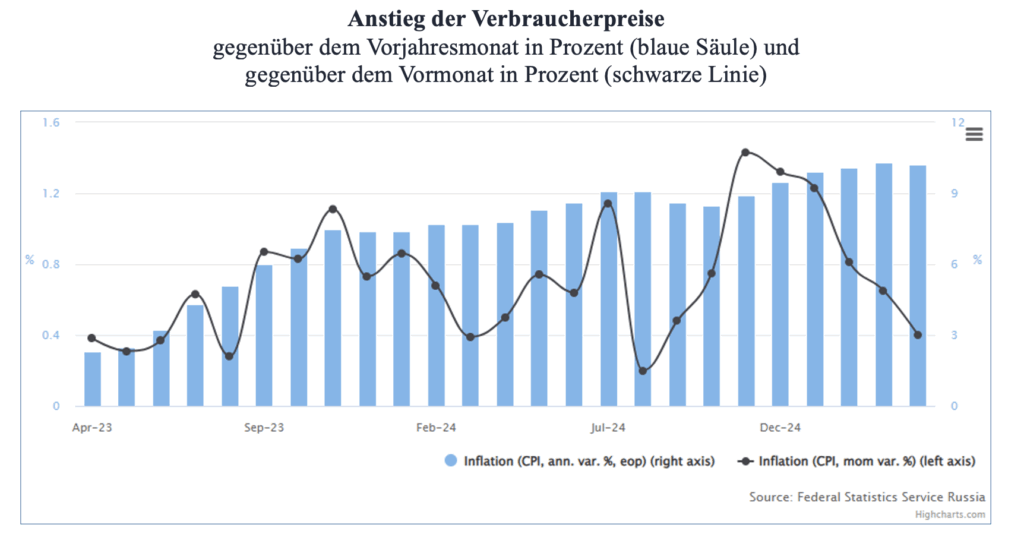

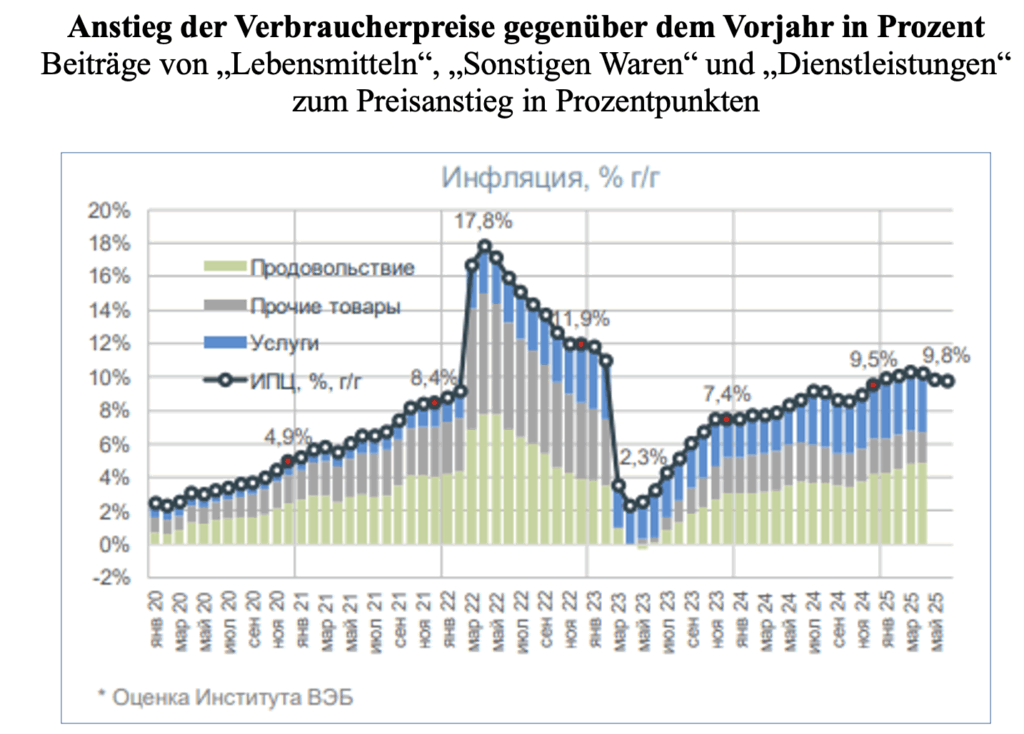

In its press release on the key rate cut, the Central Bank noted that the current rise in consumer prices in April 2025, extrapolated to an annual rate and seasonally adjusted, had fallen to 6.2 percent, after averaging 8.2 percent in the first quarter. In the fourth quarter of 2024, this “seasonally adjusted annualized rate (SAAR) of price growth” had even risen to 12.9 percent (Bank of Russia: Consumer Price Dynamics, April 2025; May 21, 2025).

The Barcelona-based research firm FocusEconomics shows in the following figure that the month-over-month increase in consumer prices in April 2025 (black line) had fallen to just 0.4 percent (left scale). However, the annual inflation rate (blue bar) was still 10.2 percent in April.

FocusEconomics: Russia Inflation April 2025, May 16, 2025

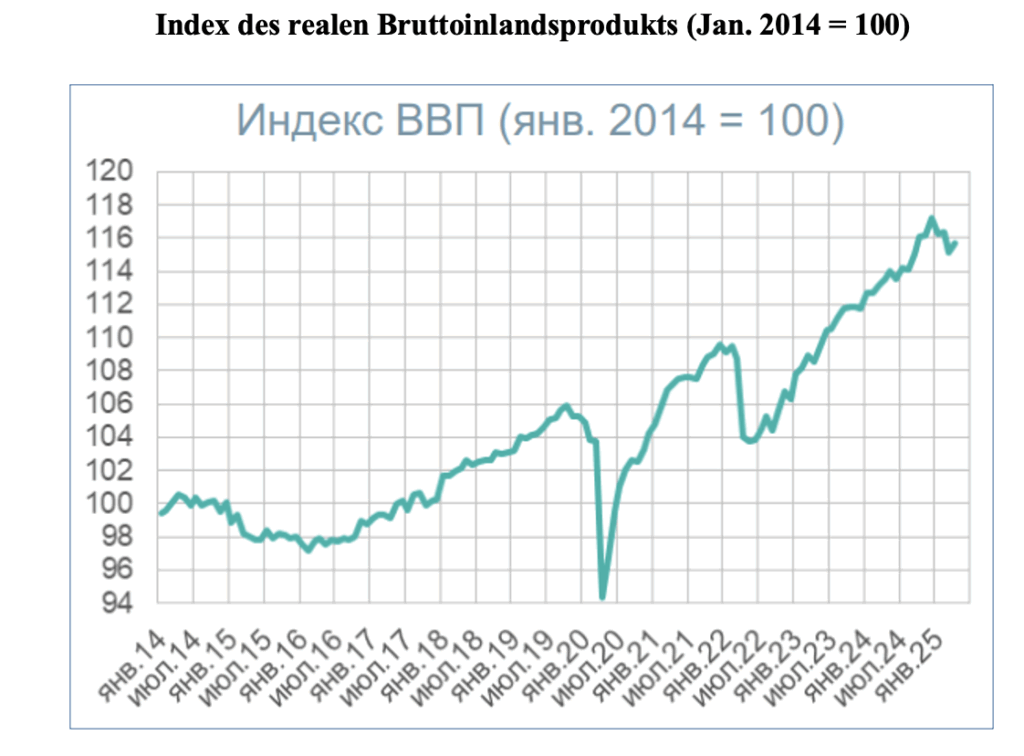

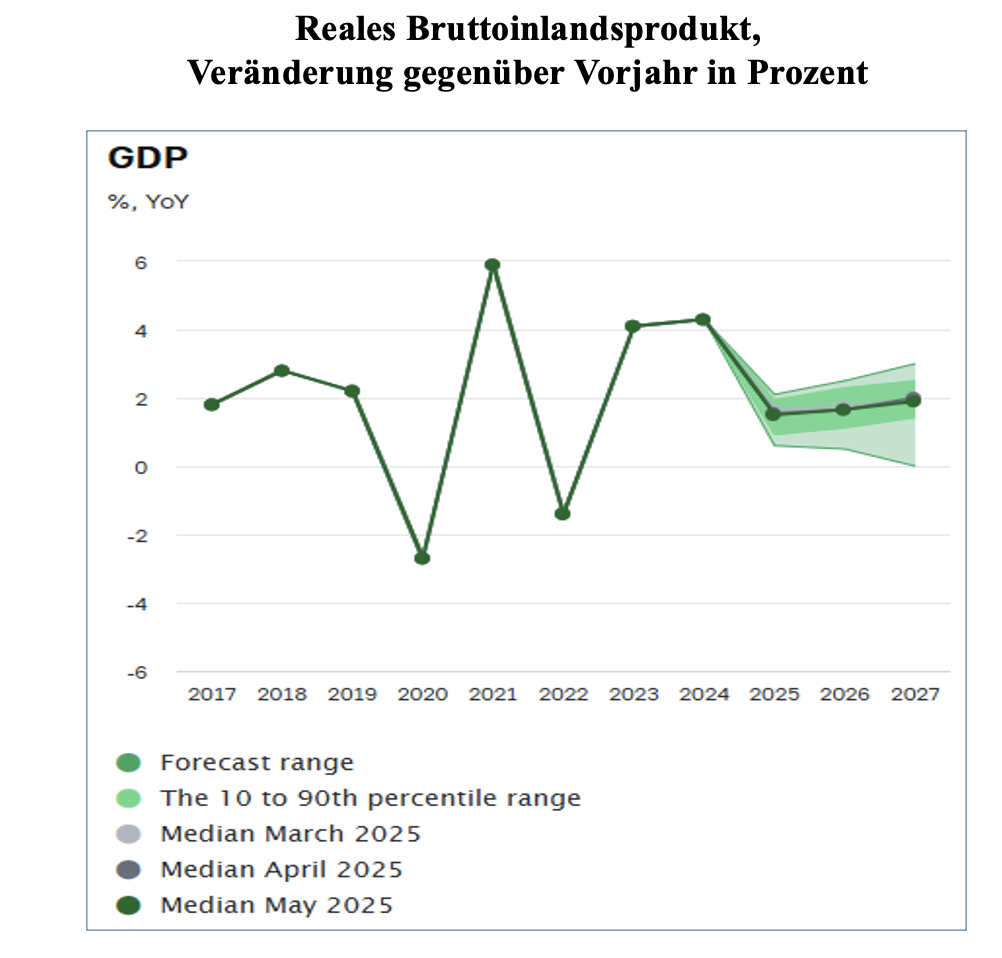

Economic growth has cooled significantly

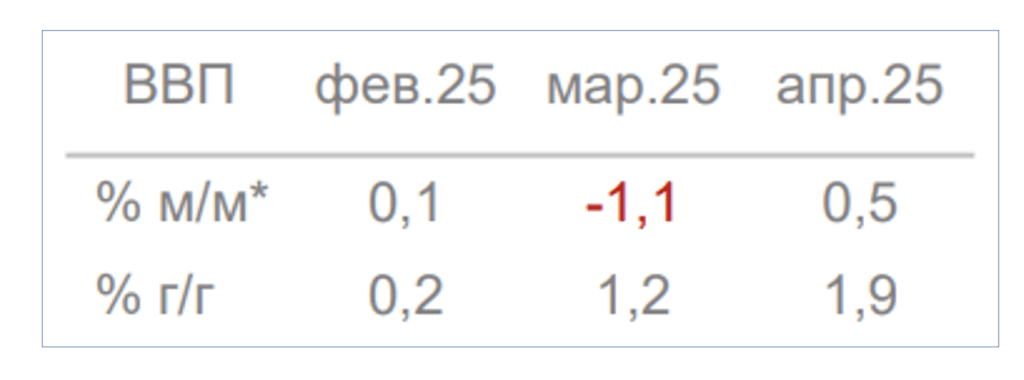

In 2023 and 2024, high defense spending in particular fueled the rise in aggregate economic output to 4.1 and 4.3 percent. In the fourth quarter of 2024, annual real GDP growth accelerated to 4.5 percent. However, according to Rosstat, it reached only 1.4 percent in the first quarter of 2025.

In April 2025, however, the annual increase in the Russian economy’s real gross domestic product accelerated again to 1.9 percent, according to initial calculations. According to estimates by the research institute of the state-owned Bank for Foreign Economic Affairs (Vnesheconombank), real gross domestic product rose by 0.5 percent in April compared to the previous month of March, after seasonal and calendar adjustments.

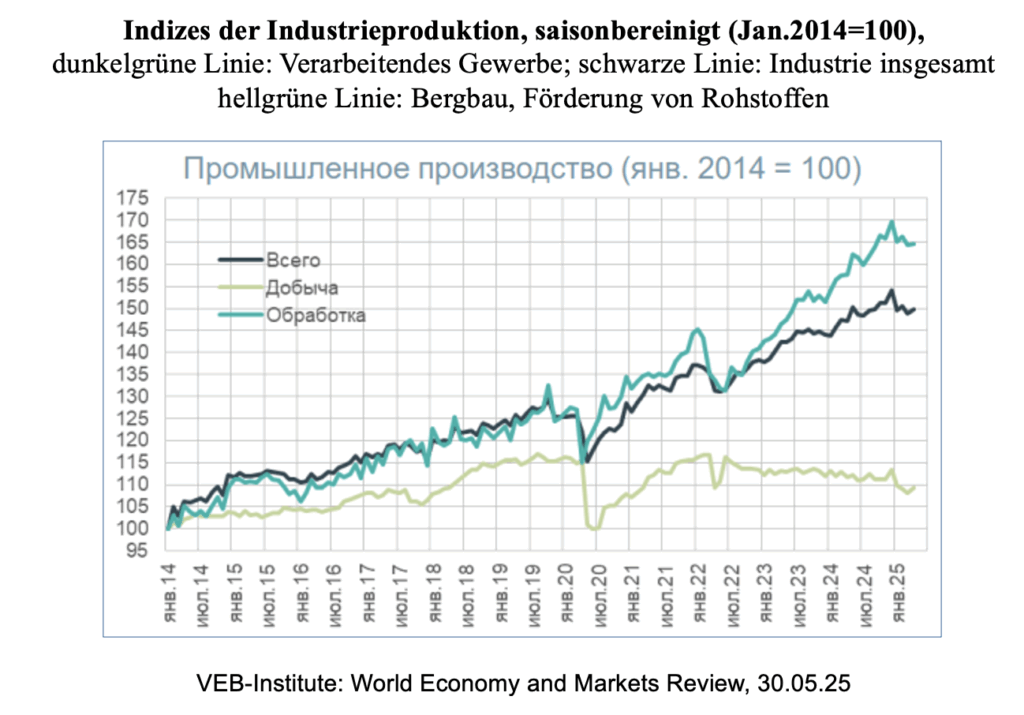

The following figure shows that aggregate economic output in April was thus barely lower than it had been about six months earlier, in October and November 2024.

VEB Institutes: “World Economy and Markets Review,” June 6, 2025

Analysts’ forecasts in the Central Bank’s economic survey

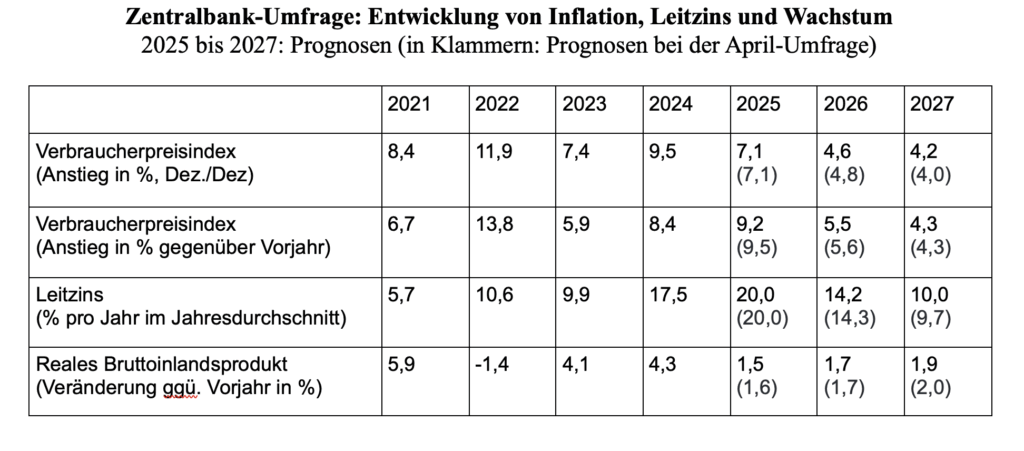

Ahead of its key interest rate decision from May 23 to 27, the Russian Central Bank surveyed analysts at banks, research institutes, and media outlets regarding further economic developments.

Survey participants, including some Western analysts, expect—as in the April survey—that the year-over-year increase in Russian consumer prices will fall to 7.1 percent by December 2025, after reaching 9.5 percent in December 2024 (TradingEconomics chart).

In the week ending June 2, the inflation rate fell to 9.8 percent, according to preliminary calculations by the research institute of the State Bank for Foreign Economic Affairs.

VEB Institute: World Economy and Markets Review, June 6, 2025

Despite the expected further decline in the inflation rate over the course of 2025, the year-over-year increase in consumer prices for 2025/2024 will still be slightly higher than in 2024 at 9.2 percent, according to the central bank survey (+8.4 percent).

Survey participants do not expect a rapid cut in the central bank’s key interest rate. The key interest rate, which was raised to 21 percent at the end of October 2024 (TradingEconomics chart), is projected by the survey to average 20.0 percent in 2025—2.5 percentage points higher than the average key interest rate in 2024 (17.5 percent).

Bank of Russia: Macroeconomic survey of the Bank of Russia, excerpt, May 28, 2025

Analysts: Russia’s economy will grow by 1.5 percent in 2025

Survey participants now expect, on average, that Russia’s economic growth will decline from 4.3 percent in 2024 to just 1.5 percent in 2025. They have thus again revised their forecast for this year’s growth downward by 0.1 percentage points. In the April survey, they had forecast growth of +1.6 percent, and in the March survey, +1.7 percent. None of the participants expect stagnation or a recession year-over-year

Bank of Russia: Macroeconomic survey of the Bank of Russia, May 28, 2025

Growth forecasts for 2026 range from +0.5 to +2.5 percent

However, uncertainty regarding growth trends remains high. The range of growth forecasts provided by survey participants for 2025 still extends from +0.7 to +2.1 percent. This means that even particularly optimistic participants fall well short of the forecast published on May 21 by Germany’s “German Council of Economic Experts.” The “Economic Experts” anticipate economic growth of +2.7 percent in Russia this year. The Russian government expects a slightly weaker GDP increase of +2.5 percent in 2026 (Interfax.com).

For 2026, survey participants expect growth of between +0.5 percent and +2.5 percent. On average, they anticipate that the rise in aggregate economic output will accelerate slightly next year, reaching +1.7 percent. No participant expects a recession next year—unlike the Munich-based ifo Institute in its spring forecast of March 17 (2026/2025: –0.8%).

For 2027, the central bank survey forecasts an average further acceleration of growth to 1.9 percent. The range of forecasts for annual GDP change then widens to +0.0 percent to +3.0 percent (see central bank chart).

Industrial production has fallen significantly since the end of 2024

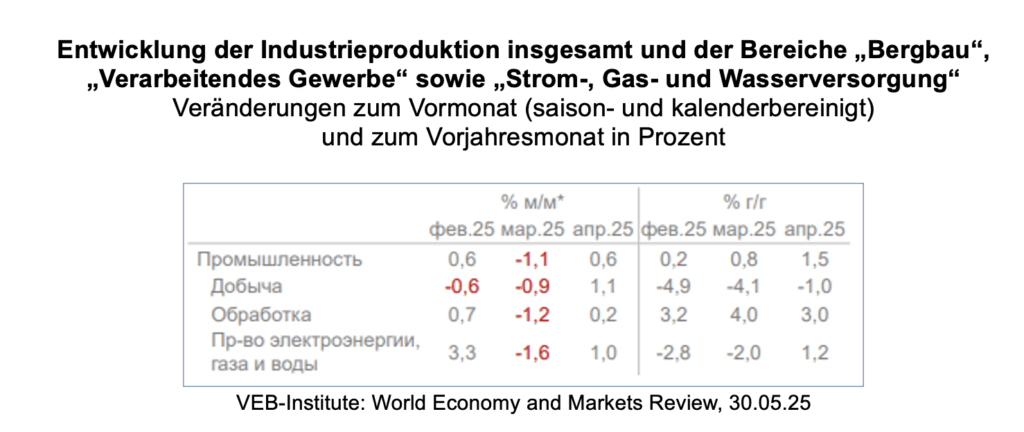

Regarding the development of industrial production, the Federal State Statistics Service (Rosstat) published the April data at the end of May. Compared to the previous month of March, industrial production grew by 0.6 percent on a seasonally and calendar-adjusted basis, according to estimates by the Research Institute of the State Bank for Foreign Economic Affairs (Vnesheconombank) (black line in the following figure in the VEB Institute’s weekly report).

However, over the course of the first four months of 2025, the production gains that the industry had achieved during the second half of 2024 were largely lost. In addition to the decline in production in the “Mining and Extraction of Raw Materials” sector (lower light green line), the decline in production in the “Manufacturing” sector (upper dark green line) also contributed to this.

In April 2025, however, according to the VEB Institute’s estimate, seasonally and calendar-adjusted production in the manufacturing sector rose by 0.2 percent compared to the previous month. Unlike overall industrial production, it was still significantly higher in April than in mid-2024.

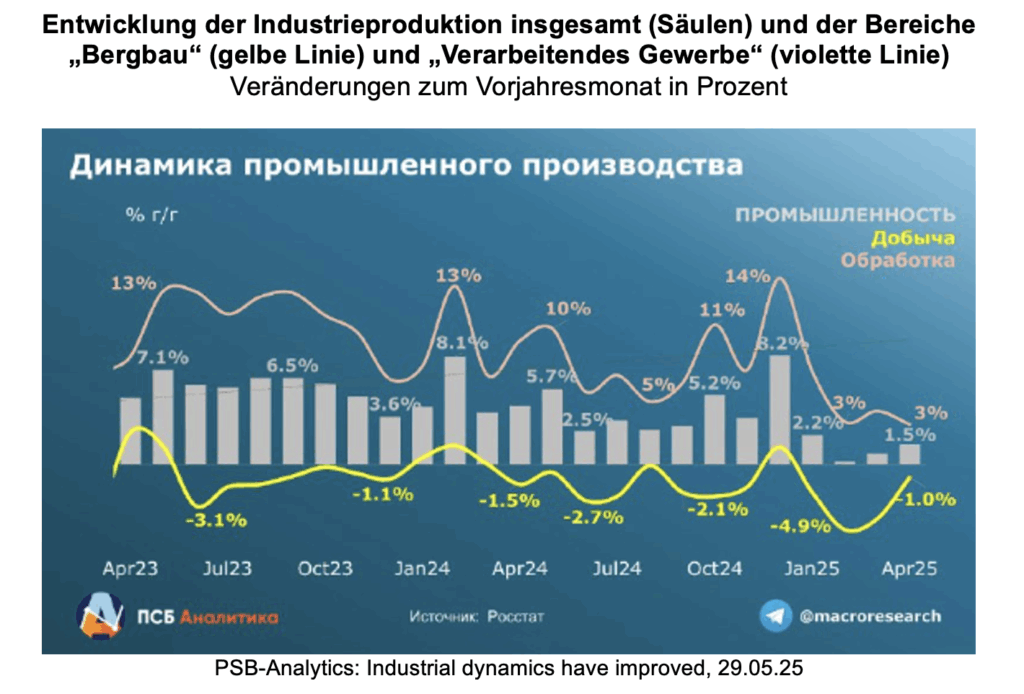

Annual industrial production growth rose to 1.5 percent in April

Overall, according to Rosstat, industrial production in April was 1.5 percent higher than in the same month of the previous year (Finmarket.ru), as shown by the right-hand column in the following figure from PSB Analytics. The decline in production in the “Mining” sector eased to -1.0 percent in April (yellow line). In the “Manufacturing” sector, annual production growth fell to +3.0 percent in April (purple line).

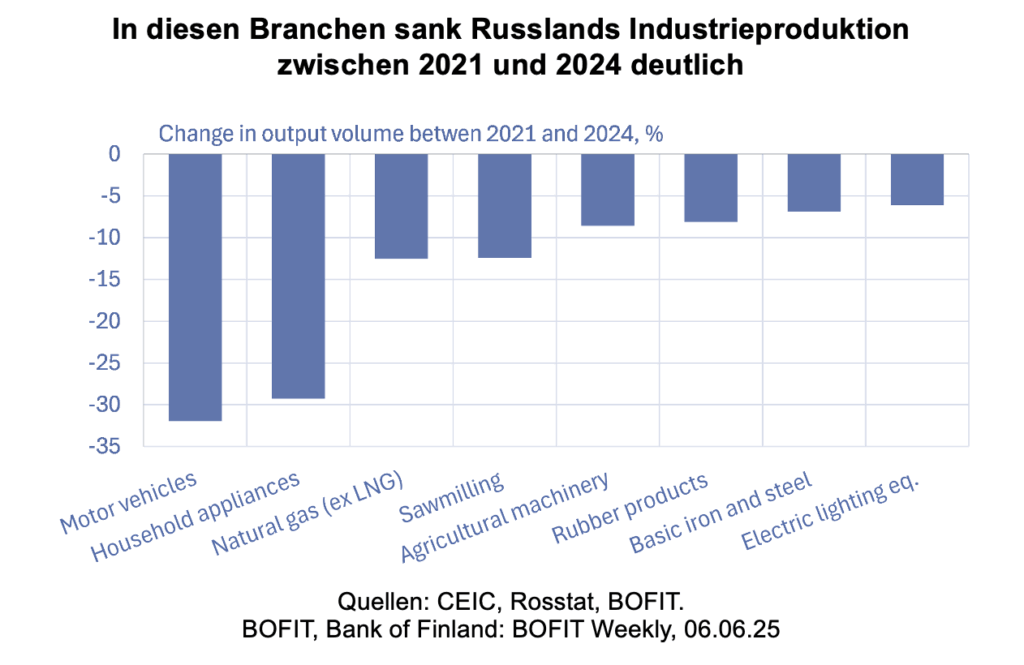

Which industrial sectors have seen a significant decline in production since 2021

The BOFIT research institute of the Bank of Finland analyzed in its weekly report how differently Russia’s industrial sectors have developed over the past three years of the war in Ukraine. It draws the following interim conclusions:

Comparing 2024 and 2021, sectors of the defense industry recorded particularly high production growth (production of metal products, computers and electronics, and military transport vehicles). Construction output also grew strongly.

On the other hand, production in many other key sectors has fallen drastically due to sanctions and the deterioration of Russia’s international trade relations.

Russia’s automotive industry suffered from the withdrawal of foreign manufacturers from the Russian market. Last year, 32% fewer motor vehicles were produced than in 2021.

The production of machinery and equipment for domestic use in Russia was hampered by limited import opportunities and the prioritization of the defense industry. For example, the production of household appliances also declined by about 30% last year compared to 2021.

The export ban to the EU has particularly affected the timber, coal, natural gas, and automotive tire industries. Production at sawmills, as well as the production of basic iron and steel products and rubber goods, declined by about 10% compared to the pre-war year of 2021. Production of agricultural equipment fell by a similarly sharp margin.

Coal production also declined. In recent months in particular, coal producers have struggled with a lack of profitable export opportunities. In light of falling export prices and rising transportation costs, the government recently approved a special support package for the coal industry.

New Growth Forecasts for Russia

In early June, the OECD lowered its forecast for this year’s growth of the Russian economy from 1.3% to 1.0%. In contrast, participants in the latest Reuters survey, as well as those in the Central Bank survey, expect economic growth of 1.5% for 2025.

The Moscow-based “Center for Macroeconomic Analysis and Short-term Forecasts” (CMASF) updates its growth forecasts for Russia’s economy roughly once a month. At the end of April, it expected economic growth in Russia for 2025 to be between +1.0 and +1.3 percent. The CMASF raised this forecast to between +1.2 and +1.5 percent at the end of May.

Sources and recommended reading:

- The Moscow Times.ru: “Calendar of a Possible Crisis”: Pro-Kremlin Economists Warn of Stagflation Risk, June 7, 2025

- Carnegie Endowment for International Peace: “Carnegie Politika” podcast by Alexander Gabuev and Alexandra Prokopenko: How Stable Is the Russian War Economy? June 5, 2025

- Center for Strategic and International Studies (CSIS); Maria Snegovaya, Nicholas Fenton, Tina Dolbaia, Max Bergmann: The Russian Wartime Economy. From Sugar High to Hangover, June 5, 2025

- TradingView; Invezz: Putin’s War Economy Gamble: How Long Can Russia Sustain the Cost? June 4, 2025

- Vedomosti: CMASF expert warns of risks of technical recession in coming months, June 4, 2025

- Vedomosti Interview: Anastasia Boyko, Ksenia Kotchenko: Dmitry Belousov: “Everyone is participating in the technology race, but few will win,” June 4, 2025

- The Moscow Times.ru: “More and more industries are showing decline.” The government asks the Central Bank to support the economy, June 4, 2025

- Bloomberg, TheEdgeMalaysia: Putin’s war economy roars ahead but the rest of Russia struggles, June 4,

- The Riddle; Nick Trickett: Hydraulic Putinism: Misusing and abusing “stability,” June 4, 2025

- Investing.com; Reuters: Russia’s economy minister calls for ’timely’ rate cut to boost growth, June 3, 2025

- YahooFinance; Reuters; Gleb Bryanski and Elena Fabrichnaya: Russian central bank seen keeping key rate on hold at 21%: Reuters poll, June 2, 2025

- n-tv.de; Lea Verstl: Moscow’s budget deficit is growing. Putin is plundering Russians’ pension funds for the war, article from June 1, 2025, for the ntv podcast “Wieder was gelernt” with Alexandra Prokopenko, Carnegie Endowment for International Peace: Putin is plundering Russians’ pension funds for the war, May 30, 2025

- Newsweek; Brendan Cole: Russia’s Economy Facing Triple Threat, May 31, 2025

- Institute for Economics and Peace (IEP); Amir Najafi, IEP Research Fellow: Russia’s War Economy: Growth Built on Unsustainable Foundations, May 30, 2025

- Finam.ru; Olga Belenkaya: The Central Bank Faces a Difficult Choice Between Maintaining and Reducing the Key Rate, May 30, 2025

- Handelsblatt+: Interview with Janis Kluge (German Institute for International and Security Affairs); Mareike Müller, Judith Henke: Looming Recession. On the Brink of Collapse? The State of Russia’s Economy, May 29, 2025