Russia: Further interest rate cut amid weak growth prospects

Author: Klaus Dormann

Last Friday, the Russian Central Bank lowered its key interest rate from 16% to 15.5% (Interfax). Only 8 out of 24 analysts surveyed by Reuters had anticipated this move. Two-thirds believed the Central Bank would leave the key interest rate at 16%.

Alexander Shokhin, president of the Russian Union of Industrialists and Entrepreneurs (RSPP), argued in the run-up to the decision that the key interest rate should be cut by 0.5 percentage points at every rate-setting meeting this year. This would allow for the optimal scenario of lowering the key rate from 16% to 13% by the end of 2026. According to Interfax, Schochin expressed confidence regarding the prospects for an interest rate cut on February 13, stating that such a gradual approach at the Central Bank Council meeting would lead to a 0.5% reduction in the key interest rate.

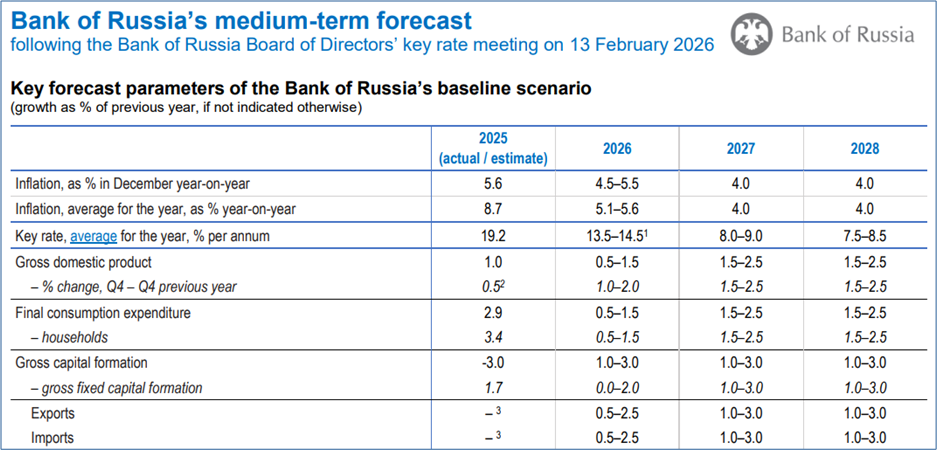

On the occasion of its key interest rate decision, the Central Bank updated its medium-term economic forecast. After raising the key interest rate to an annual average of 19.2% in 2025 amid an inflation rate of 8.7%, the Central Bank now expects it to be lowered to an annual average of 13.5% to 14.5% in 2026.

Last week, BOFIT, the research institute of the Finnish central bank, and DekaBank, the securities firm of the German Savings Banks Finance Group, were among those commenting on the development of the Russian economy over the past year and its outlook.

Central Bank’s Medium-Term Forecasts for Inflation and Growth

According to a preliminary estimate by the statistics agency Rosstat, the Russian economy grew by only 1.0% in 2025. Most forecasts suggest that growth will pick up only slightly in 2026. The government, too, has so far projected only a 1.3% increase in real gross domestic product this year. According to Economy Minister Reshetnikov, the government plans to present a new forecast in March (Interfax). In its updated medium-term forecast, the Central Bank continues to expect the real GDP growth rate in 2026 to range between 0.5% and 1.5% (see the fourth row of the table below).

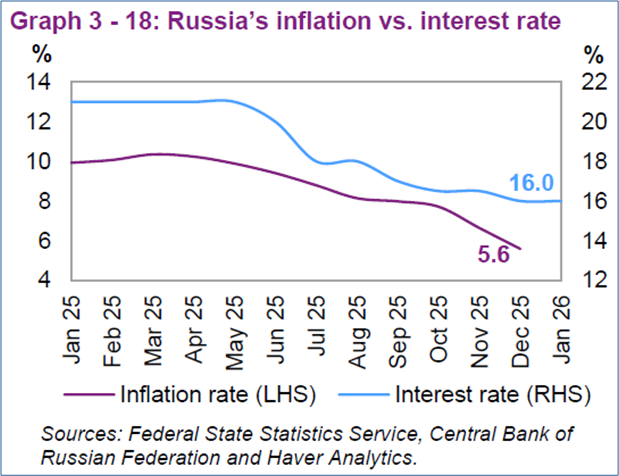

The annual increase in consumer prices, which unexpectedly fell sharply to 5.6% in December 2025, will still reach 4.5 to 5.5% in December 2026, according to the Central Bank (see first row of the table).

The forecast indicates that the annual average inflation rate in 2026 will fall from 8.7% in 2025 to between 5.1% and 5.6%.

The Central Bank estimates that it will achieve its inflation target of 4.0% starting in 2027.

Bank of Russia’s medium-term forecasts through 2028

Bank of Russia: Medium-term forecast, Feb. 13, 2026 (excerpt)

Central Bank: There was a “shift in inflation” into 2026

The decline in the annual inflation rate to 5.6% in December 2025 was followed by an accelerated rise in consumer prices in January and February. This price surge had already been addressed by Economy Minister Reshetnikov on the eve of the key interest rate decision (Interfax.com). The Central Bank summarized the price trend in its press release, much like the minister, as follows:

At the end of 2025, prices for numerous goods, particularly fruits and vegetables, rose only slightly. At 5.6%, the overall inflation rate at the end of 2025 fell below the Central Bank’s October forecast (6.5 to 7.0%).

In January 2026, however, the rise in prices temporarily accelerated significantly. The main causes of this were, in addition to price increases for fruits and vegetables, the VAT hike from 20% to 22% as well as higher excise taxes. As of February 9, 2026, the annual inflation rate rose to 6.3%.

Thus, there was a “certain redistribution of inflation” between 2025 and 2026. Nevertheless, the overall rise in prices from November to January generally met the expectations of the Russian Central Bank.

Due to this “shift” in inflation from the end of 2025 into 2026, the Central Bank raised its forecast range for the annual inflation rate in December 2026 by 0.5 percentage points to 4.5–5.5% (Interfax.com).

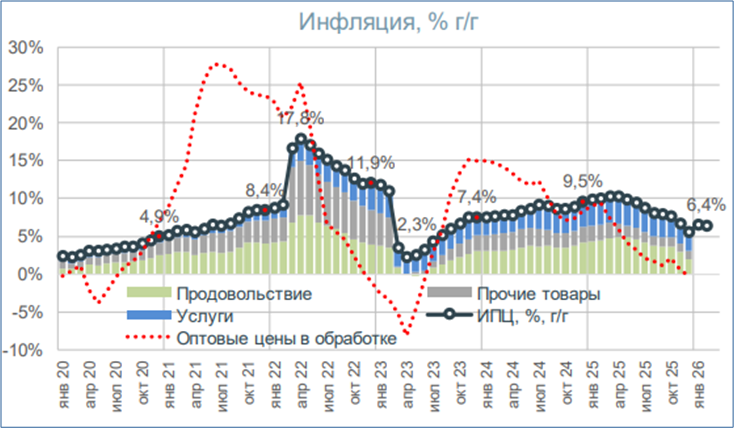

The research institute of the state development bank VEB estimates the rise in consumer prices in the week ending February 9 at 6.4%.

Year-over-year consumer price increase in % (black line); contributions to the inflation rate in percentage points:

green: food; gray: non-food; blue: services

; red line: annual rate of change in industrial producer prices

VEB Institute: Global Economic and Market Outlook; 02/13/26

GDP growth in 2025, at 1.0%, was at the upper end of the forecast range

Looking back at production trends in 2025, the central bank notes that while the annual growth rate of gross domestic product slowed overall, However, growth accelerated in the fourth quarter due to stronger consumer demand. Expectations of a value-added tax hike and the announcement of recycling fees on car purchases likely contributed to this. The Central Bank notes that economic growth in 2025, at 1.0% overall according to the first Rosstat estimate, was at the upper end of the Central Bank’s October 2025 forecast range (0.5 to 1.0%).

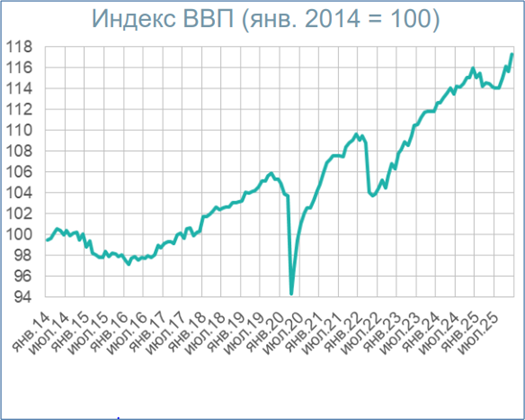

The following figure from the VEB Institute shows that, according to the Institute’s estimates, seasonally and calendar-adjusted aggregate economic output rose sharply during the third and fourth quarters of 2025. According to the institute’s estimate, real gross domestic product in December 2025 was significantly higher than a year earlier. Unlike in the past, however, the institute has not yet published any figures on this.

Real Gross Domestic Product Index (Jan. 2014=100)

VEB Institute: Global Economic and Market Outlook; Feb. 13, 2026

The BOFIT research institute of the Bank of Finland reported in BOFIT Weekly on Friday on the development of aggregate economic output since July:

“Preliminary data suggest that the Russian economy recovered slightly toward the end of last year. In the July–September period, year-over-year GDP growth was only 0.6%, but the latest data suggest that GDP grew by around 1% year-over-year in the October–December period. More detailed GDP data for the last quarter have not yet been released. According to a preliminary estimate by the Russian Ministry of Economic Development, GDP grew by nearly 2% year-over-year in December.”

The labor market is gradually easing

Regarding developments in the labor market, the Central Bank states in its press release:

“Tensions in the labor market are gradually easing. According to surveys, the share of companies reporting labor shortages has reached its lowest level since mid-2023. Companies are planning more moderate wage adjustments for 2026 than in the 2023–2025 period. At the same time, unemployment remains at a historic low. Wage growth continues to outpace labor productivity growth.”

Growth in domestic demand will slow in 2026

With regard to economic developments in 2026, the central bank assumes in its medium-term forecast that growth in domestic demand will slow in the coming months.

According to the central bank’s medium-term forecast, growth in household consumption (“final consumption expenditure households”) will more than halve in 2026. It is expected to decline from 3.4% in 2025 to just 0.5% to 1.5%.

According to the central bank’s estimates, gross fixed capital formation rose by 1.7% in 2025. In 2026, its growth is expected to range between 0.0% and 2.0%. For total gross investment (“gross capital formation”), the Central Bank expects an increase of 1.0 to 3.0% in 2026 (following an unexpectedly sharp decline of an estimated 3% last year).

Central Bank President Nabiullina commented on the development of capital investments during the press conference:

“As for investment, companies have expanded it at a record pace over the past three years. This has led to new projects that are now coming online. They will support the economy’s growth potential, even if the pace of investment slows somewhat.

Investment trends remain highly varied across sectors. In particular, the export- and transport-oriented sectors are expected to see a decline in investment compared to the high levels of previous years. At the same time, however, there are also sectors that plan to increase their investments. We have revised our investment forecast for 2026 slightly downward, but we still expect a positive trend.”

According to the forecast table, the Central Bank now expects growth in fixed capital formation to range between 0.0% and 2.0% in 2026.

Nabiullina: Oil price forecast lowered, ruble remains “attractive”

The Central Bank President also commented on external economic developments. Regarding the trend in oil prices and the ruble, she said:

“Last year, oil supply surged, leading to a surplus on the global market and now putting pressure on prices. The situation for Russian exporters is further complicated by sanctions. In light of global market developments, we have lowered our oil price forecast for the next three years. Accordingly, we have also adjusted our forecast for the value of Russian exports.

The ruble exchange rate remained stable. The decline in export revenues for oil producers was partially offset by revenues from other exports. Overall, the ruble remains attractive, supported by fiscal rules and sound monetary policy.”

In the Central Bank’s medium-term forecast, the oil price calculated by the Russian government for tax purposes is now expected to fall from $56 per barrel in 2025 to $45 in 2026. In 2026 and 2027, it anticipates a price increase of approximately $5 in each year.

According to the central bank’s forecast, with this oil price trend, the Russian current account surplus will decline from $41 billion in 2025 to just $10 billion in 2026. In 2027, the Central Bank expects the current account surplus to rise to $25 billion.

By comparison: Here’s how Finland’s BOFIT Institute views Russia’s economy

In its latest weekly report, “BOFIT Weekly,” the BOFIT research institute of the Finnish central bank points out in its analysis “Russian economy lost steam in 2025,” that Russia’s economic growth slowed significantly in 2025, reaching only 1%, even though government spending continued to rise sharply and the budget deficit grew. A labor shortage and high capacity utilization are said to have slowed production growth while simultaneously increasing inflationary pressure.

BOFIT: Restrictive monetary policy curbed inflation

According to BOFIT, Russia’s inflation has been curbed by restrictive monetary policy. The central bank did gradually lower its key interest rate in the second half of the year. However, the key interest rate was still “very high” at 16% at the end of 2025.

The Vienna-based OPEC Secretariat published the following chart on this topic:

Russian Central Bank’s key interest rate in % per year

and year-over-year consumer price inflation in %

OPEC Secretariat: Monthly Oil Market Report, February 11, 2026

On an annual average for 2025, consumer prices rose by 8.7%

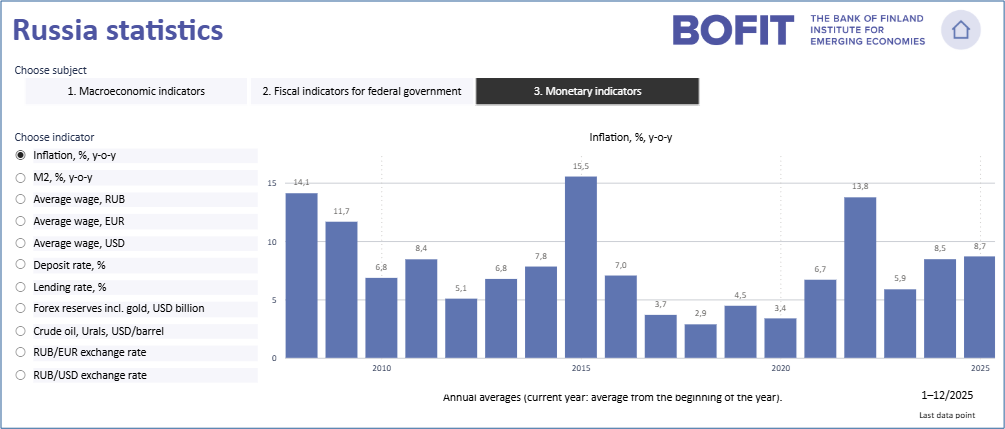

Unlike most other observers, BOFIT does not emphasize in its analysis of inflation trends in Russia that the annual inflation rate fell to 5.6% in December 2025. BOFIT points out that consumer prices rose by around 9% on average over the past year. At the same time, the inflation rate “gradually declined toward the end of 2025.”

The following chart from the BOFIT database “Russia statistics” shows that the year-over-year inflation rate rose to 8.7% in 2025 compared to 2024

Inflation in Russia

as a percentage compared to the previous year

Data sources: Russian Federal State Statistics Service (Rosstat), Central Bank of Russia, Ministry of Finance, OECD, and CEIC. The data are updated once a month.

BOFIT, Bank of Finland: Russia statistics, Jan. 31, 2026

Regarding the expected further development of inflation in 2026, BOFIT states:

Inflationary pressure this year is driven, among other factors, by the increase in the value-added tax. In particular, companies’ inflation expectations have risen significantly. According to the latest international and Russian forecasts, inflation is expected to decline further to around 5% by December 2026.

Fiscal policy boosted demand last year

According to BOFIT, government fiscal policy was “expansionary” last year—in contrast to “restrictive” monetary policy. BOFIT reports:

Government spending continued to rise rapidly last year, while revenue growth remained subdued due to the decline in oil and gas revenues. At the same time, the budget deficit reached its highest level since the start of the war of aggression.

According to preliminary data from the Ministry of Finance, Russian federal budget revenues rose by about 2% to 37 trillion rubles in 2025. Revenues from the oil and gas sector fell by 24%, while other revenues rose by 13%.

Federal budget expenditures increased by 7% to a total of 43 trillion rubles. The growth in expenditures was concentrated at the beginning of the year, while expenditures at the end of the year declined significantly compared to the previous year.

The federal budget deficit rose to 5.6 trillion rubles, or 2.6% of GDP.

Growth in domestic demand slowed in Russia

Regarding the development of consumption and investment, BOFIT notes:

Private consumption rose by only about 3% in 2025. Growth in government consumption also declined.

Although public spending, which rose rapidly last year, appears to have been largely channeled into investment, overall investment growth slowed significantly in 2025, reaching only about 2%. This suggests that private investment performed very weakly.

The decline in oil prices weighed on export revenues

BOFIT notes that the Russian government no longer publishes data on the volume of foreign trade.

Regarding the decline in the value of foreign trade, BOFIT reports: The value of exports of goods and services fell by 14% in 2025, while the value of imports of goods and services fell by 9%.

The decline in export revenues was primarily due to lower oil prices. According to the International Energy Agency (IEA), the average export price for Russian crude oil last year was around $56 per barrel, a decline of 18% compared to 2024. The IEA estimates that the volume of oil exports declined by about one percent.

According to data from the Russian Customs Service, the decline in Russian imports was due to lower imports of machinery, equipment, and transportation vehicles. In particular, car imports to Russia fell sharply last year following an increase in recycling fees for imported vehicles.

The defense industry drove growth on the production side

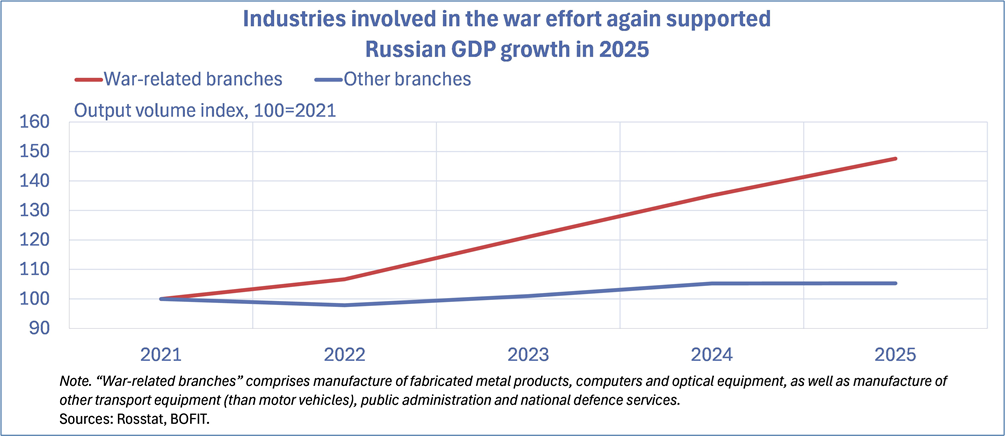

BOFIT emphasizes that growth in the Russian economy last year was once again driven by sectors with a high share of products for military purposes (“war-related branches”).

The following BOFIT chart shows that production in these sectors continued to rise sharply in 2025. Compared to 2021, the year before the start of the war in Ukraine, it increased by nearly 50%. According to BOFIT, production in other sectors stagnated last year.

BOFIT Weekly 7/2026: Russian Economy Lost Steam in 2025, 02/13/26

The Moscow-based “Center for Macroeconomic Analysis and Short-Term Forecasting” (CMASF) also noted in its latest monthly analysis of industrial production trends:

“All positive developments in industrial production in recent months are primarily attributable to increased production in sectors with a high share of defense goods. Civilian industrial production has been stagnating since the second quarter of 2025 (following a decline in the first quarter).”

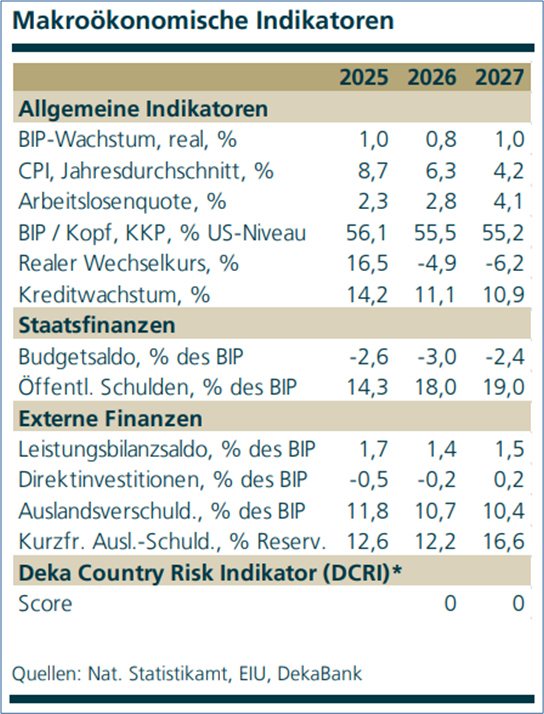

DekaBank: The economic boost from war spending has subsided

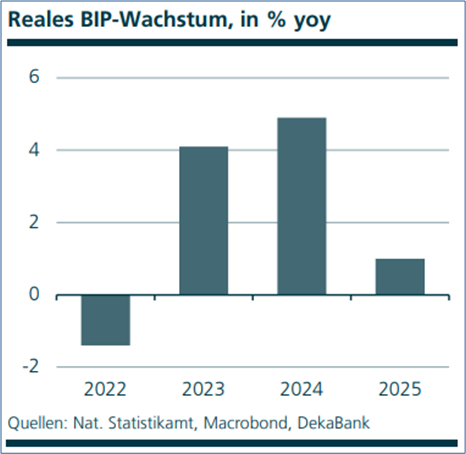

Frankfurt-based DekaBank, the securities firm of the German savings banks, summarized the development of the Russian economy in its “Emerging Markets Trends” immediately following the release of the first Rosstat estimates for 2025 as follows:

“The economic boost from war spending, which gave Russia’s economy growth rates above 4% in 2023 and 2024 (with potential growth of around 1.0%), has finally subsided in 2025. According to the statistics agency’s initial estimate, real GDP grew by 1%.”

DekaBank: Emerging Markets Trends, 02/09/26

Monetary policy is likely to be eased only cautiously in the first half of the year

DekaBank points out that the key interest rate had already been cut by 500 basis points from 21% to 16% prior to the most recent reduction. Regarding the future course of monetary policy, DekaBank states:

“However, the extent to which the central bank can further ease monetary policy remains unclear, as several taxes and levies were raised in 2026 to finance the growing budget deficit. In particular, the 2-percentage-point increase in the value-added tax to 22% is driving up inflation and could trigger second-round effects given the unstable inflation expectations. In the first half of the year, the central bank is likely to remain cautious, and the private sector of the economy is expected to remain under pressure.”

“Russia’s national budget is a major work in progress”

This is how DekaBank views the problems of Russian fiscal policy:

“Revenues from the oil and gas industry fell by 23.8% year-over-year in 2025 due to sanctions and low oil prices, now accounting for just under 23% of total government revenues—the lowest level in over 20 years.

Other revenue sources were unable to compensate for the loss of oil revenues, so the budget deficit is likely to have stood at 2.6%.

The 2026 budget plan calls for a reduction in the budget deficit, though this appears unrealistic given the current macroeconomic environment.”

DekaBank points out that the price of Russian oil is below the $59 per barrel level on which Russia’s budget planning is based. Furthermore, in light of the sanctions imposed on Rosneft and Lukoil in November, Russia’s oil exports appear to have declined. In particular, India—an important market for Russian oil—is likely to become more cautious regarding its oil imports from Russia, according to DekaBank’s assessment, in light of the recent trade deal between the U.S. and India.

The bank expects public debt to rise and the tax and levy burden on the economy to increase. The liquid portion of the sovereign wealth fund, which is used to plug budget gaps, has fallen below 2% of GDP. As a result, it can no longer single-handedly offset the additional spending or revenue shortfalls.

As a result, the bank expects that in 2026, with Russian economic growth at 0.8%, the federal budget deficit will rise from 2.6% to 3.0%. The annual average increase in consumer prices is expected to slow to just 6.3% (while the Russian Central Bank anticipates a sharper decline to 5.1–5.6%).

DekaBank: Emerging Markets Trends, 02/09/26

Recommended reading:

- fr.de: Disaster on the oil market in Russia – War financing wobbles, 02/15/26

- Vladimir Milov in an interview with Michael Nucky; YouTube video, Russian: Nabiullina freaks out/There is no growth and there won’t be any/Catastrophic decline in income/Cucumbers are more expensive than meat, 02/15/25

- BOFIT, Bank of Finland: Russian Economy Lost Steam in 2025, 02/13/26

- Yahoo Finance; Reuters: Russian central bank cuts key rate by 50 basis points to 15.5%, February 13, 2026

- Interfax.com: Central Bank again lowers key rate by 50 bps to 15.5%, 02/13/26

- Interfax.com: Central Bank of Russia raises 2026 inflation forecast to 4.5%-5.5%, 02/13/26

- Finam.ru; Olga Belenkaya: For the first time in a long time, the Central Bank sent a cautious signal regarding future measures, 02/13/26

- Bank of Russia: Statement by Bank of Russia Governor Elvira Nabiullina following the Board of Directors meeting on February 13, 2026, February 13, 2026

- Bank of Russia: Bank of Russia cuts the key rate by 50 basis points to 15.50% p.a., 02/13/26

- Interfax.com: Russia is now seeing a decline in annual inflation and still has sufficient reserves to ease monetary policy – Reshetnikov, 02/12/26

- Interfax.com: The Russian economy will slow down in the first half of the year; a recovery is expected by the end of 2026 or, more likely, in 2027 – Reshetnikov, 02/12/26

- Yahoo Finance; Reuters; Darya Korsunskaya: Russia’s economy minister delays recovery outlook, Interfax reports, 02/12/26

- Interfax: The head of the RSPP expects the Central Bank to cut the key interest rate in “small steps” of at least 50 basis points by April, reaching 13% by year-end, 02/05/26

- ZDF Auslandsjournal, Felix Klauser: How Russians are feeling the effects of the war, video, 6 min., 02/12/26; ZDF, Felix Klauser: Inflation in Russia. Why a Putin poster is causing a stir, 01/28/26

- RBC Radio: Alfa Bank assessed the Ministry of Economic Development’s forecast regarding an economic slowdown. Orlova: The economic recovery will begin in the summer with a cut in the key interest rate, 02/12/26

- Lenta.ru; Anatoly Akulov (Editor): Pessimistic Forecast for the Russian Economy. Reshetnikov: Russia’s GDP Growth Rate Will Not Recover Until 2027, 02/12/26

- OPEC Secretariat: Monthly Oil Market Report, 02/11/26

- Business-gazeta.ru; Pavel Riabov: Ahead of the Central Bank meeting: Inflation hits record high in January, interest rate decision is set, 02/11/26

- Mr. East; Søren Riishøj, Associate Professor of Political Science: Russian Gas Continues to Flow to Europe – Pressure for Direct Negotiations Grows, 02/09/26

- Vladislav Inozemtzev; IFRI Paper: Deathonomics: The Social, Political, and Economic Costs of War in Russia, 02/09/26

- inbusiness.kz; Ardak Zhanat: A total collapse. Russia has never experienced a crisis like this before. February 9, 2026,

- Bankiros.ru; Victoria Tyupina: “The Russian economy is on the brink of a recession”: What decision will the Central Bank make on February 13? February 9, 2026

- Fortune, Jason Ma: Russian officials are warning Putin that a financial crisis could arrive this summer, report says, while his war on Ukraine becomes too big to fail