Russia: As growth slows sharply, problems are intensifying

Author: Klaus Dormann

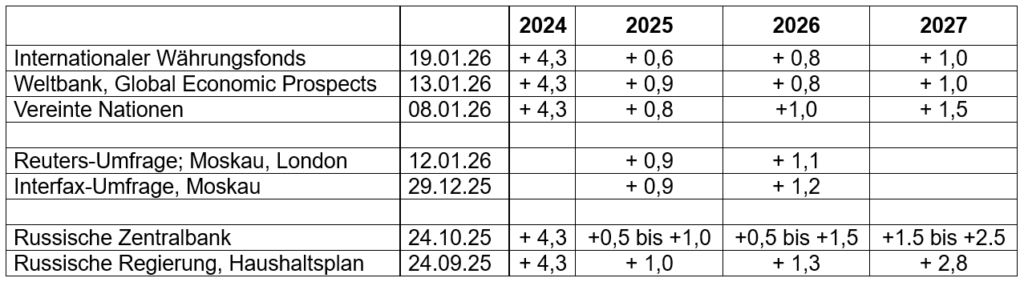

Following the United Nations Department of Economic and Social Affairs and the World Bank, the International Monetary Fund also updated its growth forecasts for the Russian economy a week ago. Looking back at 2025, the IMF is sticking to its relatively low forecast that the Russian economy is likely to have grown by only 0.6 percent. The estimates from the World Bank (+0.9 percent) and the United Nations (+0.8 percent) are slightly higher.

However, the forecasts from all three international economic organizations fall within the range that the Russian Central Bank had already published at the end of October for 2025 growth (+0.5 to +1.0 percent). They are also barely lower than the 1.0 percent growth forecast that the Russian government has been using as the basis for its budget planning since late September.

The IMF, World Bank, and UN’s expectations for Russia’s economic growth in 2026, which has just begun, are also consistent with the Central Bank’s estimates. The forecasts by international organizations range from 0.8 to 1.0 percent and thus fall almost exactly in the middle of the Central Bank’s broad forecast range for 2026 (+0.5 to +1.5 percent). However, compared to the government’s growth forecast (+1.3 percent), the IMF and World Bank’s forecasts for 2026, at +0.8 percent each, are noticeably lower.

GDP Forecasts 2024 to 2027

Year-over-year change in real gross domestic product, in percent

The forecasts for 2027 vary widely

A comparison of the forecasts for 2027 clearly shows that international economic organizations expect much less growth for the Russian economy in the long term than the government does. While the government expects the growth rate to more than double in 2027 and reach 2.8 percent, the IMF and the World Bank assume that GDP growth will remain stagnant at around one percent next year as well. The United Nations also expects only a slight acceleration in growth to 1.5 percent. However, the Russian government’s forecasts proved to be far too optimistic last year.

The Russian government had expected much higher growth for 2025

Estimates for the growth of the Russian economy achieved last year have since largely fallen to just under 1 percent. This is also reflected in analyst surveys conducted at the turn of the year, in which the increase in real gross domestic product in 2025 is now estimated at an average of just 0.9 percent.

A year ago, however, the Russian government had still expected growth of 2.5 percent for 2025. The Central Bank’s forecast proved to be much more realistic. As early as October 2024, it had already projected a growth range of just +0.5 to +1.5 percent for 2025.

The growth forecasts for 2025 published about a year ago by international economic organizations and participants in analyst surveys also proved to be quite accurate. On average, they were lowered to just around 1.5 percent by the end of 2024.

The problems of Russia’s “war economy” are intensifying

At the turn of the year, Yulia Starostina analyzed the current problems facing the Russian economy in “Meduza,” an online magazine published in Riga in Russian and English. She first emphasizes that Russia, “contrary to experts’ apocalyptic forecasts,” did indeed “weather” the sanctions shock of 2022. However, economic growth in the following years was primarily driven by sharply increased military spending. Other growth drivers included high energy prices and, in some cases, the successful restoration of disrupted supply chains.

By 2025, however, Starostina argues, the problems facing the Russian economy had “piled up to a critical point.” Growth had nearly come to a standstill. Oil prices had fallen. The Russian government increasingly lacked the funds to finance the war in Ukraine. It therefore resorted to unpopular measures, including higher taxes for businesses and households.

Regarding the current state of the Russian economy, Starostina notes, among other things:

- In 2025, the economy has returned from “overheating” to its “actual growth potential.”

- The inflation rate remains well above the target of 4 percent.

- The rapid growth of the military sector came at the expense of the civilian economy.

- The budget deficit is at a record high. Reserves are shrinking and government debt is rising.

- Energy revenues are falling as oil prices decline.

- The economy can survive another year of war—but at the expense of living standards.

Below are further notes on your analysis, supplemented with some figures and updated economic data.

Return from “overheating” to “true growth potential”

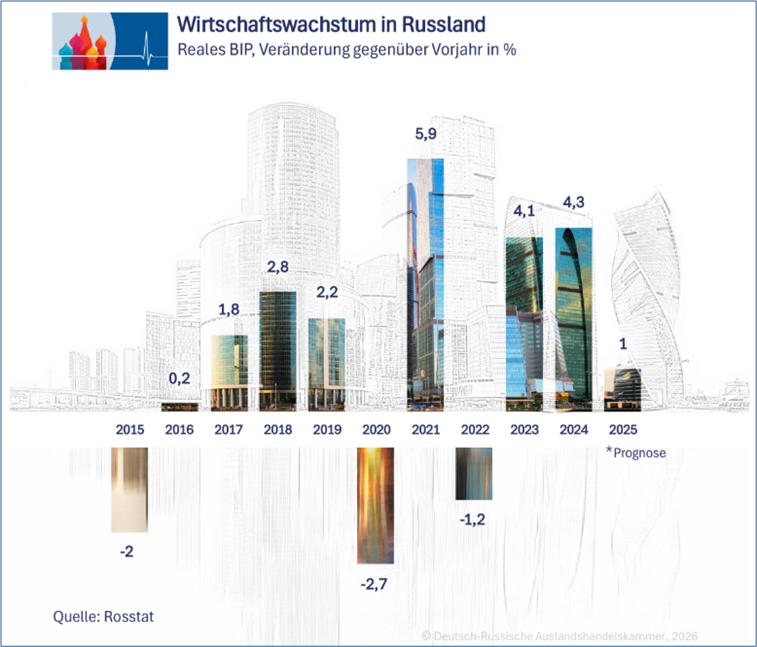

Starostina emphasizes: The slowdown in growth does not indicate a collapse of the Russian economy. Rather, it reflects the economy’s return to its “true growth potential” after two years of “overheating.” Fueled by military spending, growth exceeded four percent in both 2023 and 2024—a rate of growth that, with the exception of 2021, has not been achieved at any other time in the past ten years.

German-Russian Chamber of Foreign Trade: Focus Analysis: Review 2025 – Outlook 2026, Jan. 12, 2026

Since October, the Russian Central Bank has been forecasting GDP growth of 0.5 to 1 percent for 2025 and 0.5 to 1.5 percent for 2026. As economic growth slowed in 2025, the Central Bank began, according to Starostina, to lower its key interest rate “very cautiously.” At the last meeting of the Central Bank Council in December 2025, it reduced it from 16.5 to 16 percent.

The inflation rate remains well above the target of 4 percent

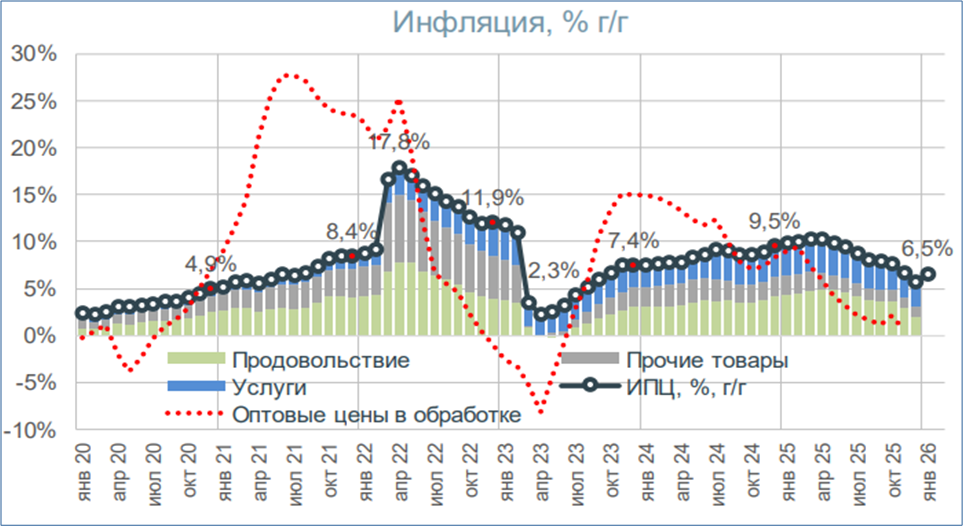

The rise in consumer prices remains well above the Russian Central Bank’s target of 4 percent. Regarding current inflation trends, the statistics agency Rosstat reported that the annual inflation rate fell to 5.6 percent in December 2025 (Finmarket.ru). With the increase in the value-added tax from 20 to 22 percent at the beginning of 2026, the annual rise in consumer prices accelerated. According to data from the research institute of the state-owned VEB Development Bank, consumer prices in the week ending January 19 were 6.5 percent higher than a year earlier (see black line in the figure below).

Year-over-year increase in consumer prices, in percent

Green bars: Food; Gray bars: Other goods;

Blue bars: Services; Red line: Wholesale prices in production

VEB Institute: Global Economy and Markets, January 16–22, 01/23/26

According to Raiffeisen Capital, the annual inflation rate had accelerated to 6.26 percent in the first ten days of January. In its weekly report dated January 19, the financial institution notes that the effect of the VAT increase has so far been “rather minor.” The acceleration in the annual inflation rate is also attributed to other factors. It is expected to take about two to three months for the new tax rate to be fully reflected in prices. The slowing economy will make it difficult for producers and sellers to pass on their increased costs to consumers. This would mitigate the impact of the tax hike on the rise in consumer prices. The Central Bank estimated that the tax hike would increase the annual inflation rate by 0.5 to 0.7 percentage points in 2026.

By December 2026, the Russian Central Bank expects the annual inflation rate to decline to 4.0 to 5.0 percent.

The rapid growth of the military sector came at the expense of the civilian economy

According to Starostina, growth disparities within Russian industry intensified in 2025. The “military economy,” which is a priority in government budget spending, is growing. Production in the “civilian economy,” on the other hand, is stagnating because the high key interest rates set by the Central Bank severely restrict access to credit.

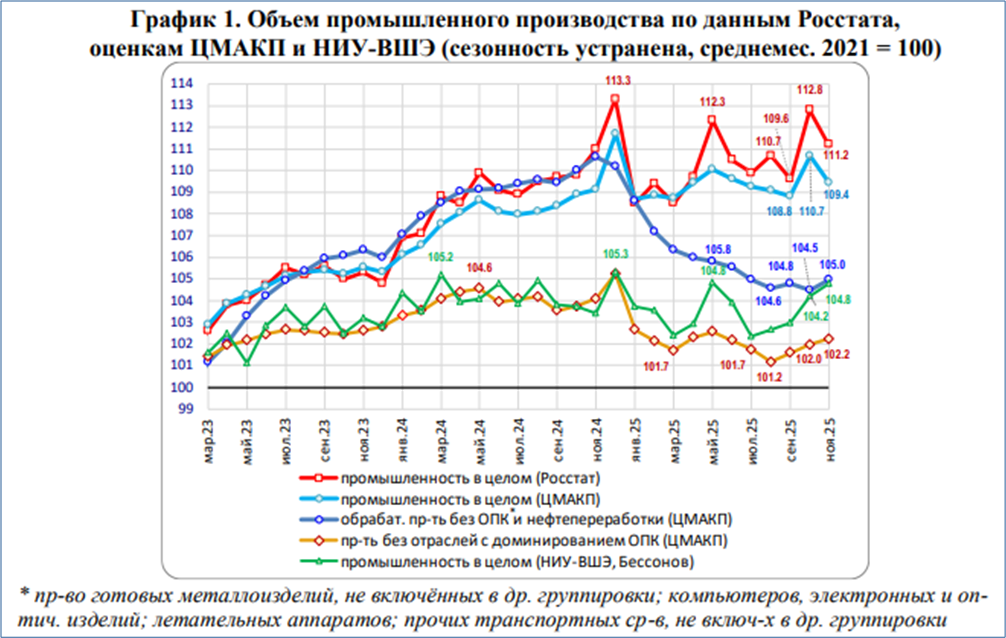

In some sectors, production is already declining sharply. Starostina cites estimates from the “Center for Macroeconomic Analysis and Short-Term Forecasting” (CMASF). The trend of the dark blue line in the following figure shows that the index value for production “in the core civilian sector of the manufacturing industry” has fallen by about 5 percent from just under 111 points in November 2024 to 105 points in November 2025, according to CMASF.

Industrial production (seasonally adjusted, monthly average 2021=100);

Rosstat data on industrial production (red line) compared with estimates

by the CMASF (light blue line) and the Higher School of Economics (green line);

dark blue line: CMASF

estimate of production in the core civilian sector of the manufacturing industry

CMASF: On the Development of Industrial Production in November 2025, Dec. 26, 2025

High interest rates are squeezing corporate profits

Starostina points out the negative consequences of sharply increased defense spending for Russian companies: The rise in defense spending has widened the federal budget deficit and fueled inflation. As a result, the Russian Central Bank cannot lower interest rates quickly. Loans remain extremely expensive—a burden that primarily affects the civilian economy. Interest payments are consuming an ever-increasing share of corporate profits. In the third quarter of 2025, companies were already spending 38 percent of their profits on debt service, according to Starostina.

Labor is in very short supply

The labor shortage in the Russian economy has worsened. The labor force has shrunk due to war-related losses, emigration abroad, and a sharp decline in immigration from Central Asia.

The extremely low official unemployment rate fell to 2.1 percent in November (Trading Economics). However, according to Starostina, analysts at the “Center for Macroeconomic Analysis and Short-Term Forecasting” (CMASF) believe there is “hidden unemployment” within companies in the form of reduced working hours.

The budget deficit rose to 2.6 percent of GDP in 2025

Yulia Starostina also cites the rise in the budget deficit as a symptom of the crisis in the Russian economy. She notes that the state’s financial reserves are shrinking while public debt is rising.

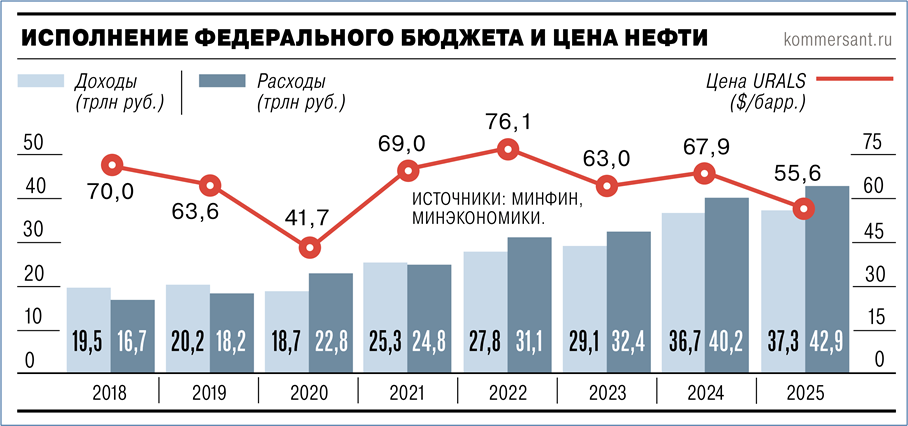

According to a statement from the Ministry of Finance on January 19, the deficit in the Russian federal budget reached 5.6 trillion rubles, or 2.6 percent of GDP, in 2025. The original plan for 2025 was to reduce the deficit to 0.5 percent of GDP.

Federal budget revenues rose to 37.3 trillion rubles in 2025, while expenditures rose to 42.9 trillion rubles, Kommersant reports. Meanwhile, the price of Urals crude oil fell from $67.9 per barrel in 2024 to $55.6 per barrel in 2025.

Federal budget revenues and expenditures in trillions of rubles

and Urals oil price in US dollars per barrel

Kommersant; Vadim Visloguzov: The Budget Is Excellent, 01/19/26

Kommersant notes that the government had planned for a deficit of 2.6% of GDP since a budget amendment in November. The gap between revenue and expenditure in 2025 was primarily covered by domestic debt. Unlike in the previous three years, the “National Welfare Fund” was not used to cover the deficit in 2025. The government decided to preserve this reserve.

According to Kommersant’s assessment, the deficit of 2.6% of GDP is “quite high” compared to previous years. The year 2024 ended with a deficit of 1.7% of GDP, and 2023 with 1.8%.

Domestic government debt is set to rise sharply

Starostina points out that the liquid portion of the “National Welfare Fund” had fallen to 4.1 trillion rubles (1.9 percent of GDP) as of December 1. This is lower than the federal budget deficit forecast for 2025 (5.6 trillion rubles).

To prevent the fund from being completely depleted, the government increased domestic debt by 2.2 trillion rubles (28.3 billion U.S. dollars) in the fall, bringing the total to nearly seven trillion rubles (90 billion U.S. dollars).

According to Starostina, the government plans to borrow an additional 5.5 trillion rubles on the domestic market in 2026. Just under four trillion rubles of this amount is to be used to finance the budget deficit, with the remainder going toward servicing existing debt.

This means that in 2026, around 8 percent of all federal spending is expected to go toward debt service. Thirty-eight percent of spending is earmarked for the “military” and “security” sectors.

Starostina considers the planned deficit reduction for 2026 to be overly optimistic

The 2026 federal budget calls for a reduction in the deficit to 1.6 percent of GDP (3.8 trillion rubles). However, given current oil price trends, Yulia Starostina considers this forecast overly optimistic. She believes that all signs point to government revenues from the oil and gas sector falling even more sharply in 2026 than in 2025.

The main reason for this is not so much a decline in export volumes due to U.S. sanctions against Rosneft and Lukoil, which together account for about half of Russia’s oil production. More significant is the fact that Russian crude oil has become even cheaper—due to the sanctions and a global decline in prices.

Taxes, energy costs, and household expenses are rising

Yulia Starostina points to various tax increases. For instance, the corporate income tax was raised from 20 to 25 percent. In 2025, a progressive income tax with a top rate of 22 percent was introduced. Starting in January 2026, the value-added tax was raised from 20 to 22 percent. At the same time, electricity and energy costs for households continue to rise. In addition, a new tax on imported electronic products is being introduced.

Starostina quotes an unnamed “senior economist at a Russian research center” regarding the consequences of the higher tax burden. He states:

“Higher taxes hamper civilian industry, reduce investment and consumption, and ultimately lower the average standard of living compared to what would otherwise be possible.”

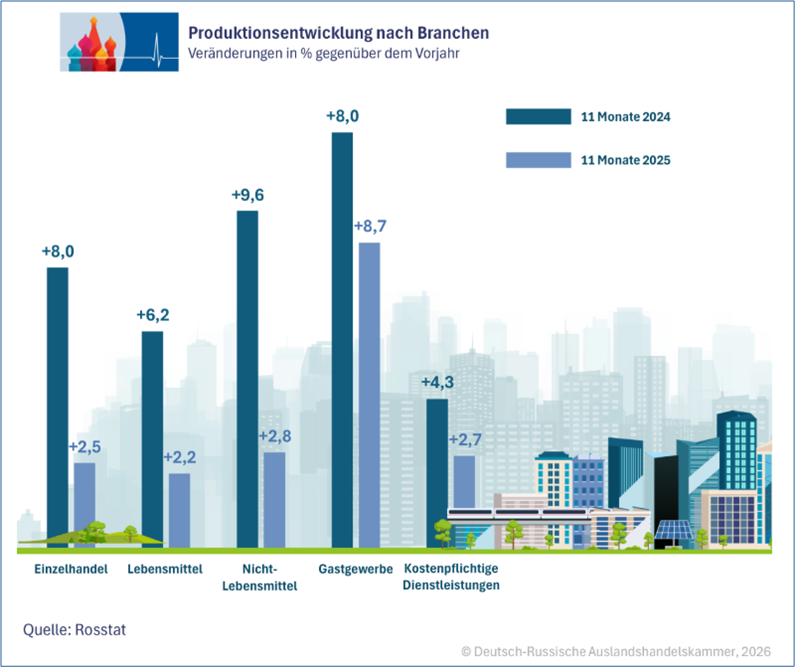

However, household consumption still grew in 2025

In the first eleven months of 2025, however, real sales in the Russian retail, hospitality, and service sectors still grew significantly year-over-year, according to Rosstat, as shown in the following figure from an analysis by the German-Russian Chamber of Foreign Trade. However, the growth in consumer spending was much weaker than in 2024.

German-Russian Chamber of Foreign Trade: Focus Analysis: Will Russia Go Bankrupt in 2026? 01/14/26

On its Telegram page “Focus-Pocus,” Raiffeisenbank cites the following factors that have supported consumer demand in recent months:

- The increase in the recycling fee for car purchases on December 1, 2025

- Discounts and special offers from retailers looking to sell off goods at the old VAT rate.

However, the bank expects a gradual slowdown in consumer activity in the coming months. It points to rising taxes and fees, as well as high interest rates on consumer loans amid a persistently restrictive monetary policy.

Recommended reading:

German-Russian Chamber of Foreign Trade:

- Focus analyses, in German; also in Russian:

- Will Russia Go Bankrupt in 2026? 01/14/2026

- Review 2025 – Outlook 2026, Jan. 12, 2026

- Tax Reform 2026: Higher VAT, Higher Social Security Contributions, Small and Medium-Sized Businesses Hit Hardest, Jan. 12, 2026

Other:

- Russian Central Bank: Useful links for anyone who wants to better understand the economy and monetary policy. Jan. 23, 2026

- Interfax.com: Central Bank of Russia emphasizes the importance of monthly data amid a surge in inflation in the first half of January, 01/23/26

- Finam.ru: Egor Susin, author of the Telegram channel TruEcon: Annual inflation could accelerate to 6.4–6.5% in January, 01/22/26

- Carnegie Politika video, Russian: Alexandra Prokopenko: How will the Russian economy develop in 2026? Alexandra Prokopenko, Carnegie Berlin Center, spoke with Vladislav Gorin and others about the impact of low oil prices on the Russian state budget and which indicators are particularly important for understanding the Russian economic situation; video, 56 min, Jan. 21, 2026.

- RBC.ru: The IMF has lowered its forecast for Russian GDP growth, Jan. 19, 2026

- Reuters; Global Banking and Finance Review: Russia’s oil and gas budget revenue set to sink 46% in January, Reuters calculations show, Jan. 19, 2026

- NEWS.ru: Will Russian economic growth slow down in 2026? The IMF has updated its forecast, 01/19/26

- Monocle.ru; Alexander Ivanter: Don’t lose your spoils! Is it beneficial for Russia to remain a member of OPEC+? How much oil should be exported? How can Russian energy companies be encouraged to cooperate? Valery Semikashev, Institute for Economic Forecasting of the Russian Academy of Sciences, on the development of the Russian fuel and energy sector, Jan. 19, 2026

- Kommersant; Vadim Visloguzov: The budget is excellent, 01/19/26

- Nezavisimaya Gazeta, Anastasia Bashkatova: Russian science is currently turning into an “entertainment device.” Dmitry Belousov (CMASF) warns. Research findings must be translated into real business practice, Jan. 18, 2026.

- Expert.ru: Anton Siluanov: The budget deficit for the year amounted to 2.6% of GDP. 01/16/26

Inflation in December and in 2025

- Bank of Russia: Inflation in Russia; December Monthly Report; PDF, Jan. 21, 2026; in English

- Raiffeisen Capital: Weekly Review, 01/19/26

- Alfa Investments; Economy and Trends: Inflation slowed to 5.6% at the end of 2025. However, inflation picked up again at the beginning of this year, Jan. 19, 2026.

- Finam.ru; Alexander Abramov: Head of the Laboratory at the Institute for Applied Economic Research of the Russian Presidential Academy of National Economy and Public Administration: Rosstat has caused problems for the Central Bank with record-low inflation in 2025, 01/18/26

- Finmarket.ru: Inflation in Russia stood at 5.59% in 2025, Jan. 16, 2026

- The Bell.ru; Denis Kasyanchuk: Inflation in 2025 slowed to 5.6%, which is below analysts’ forecasts, Jan. 16, 2026

- AFP: Russian inflation drops significantly in 2025, Jan. 16, 2026