Russia: As growth slows, inflation is falling rapidly

Author: Klaus Dormann

“Stagflation”—this is the buzzword some analysts use to describe the current economic situation in Russia. In fact, real gross domestic product actually declined in the first quarter of 2025 compared to the fourth quarter of 2024. And in the second quarter, it likely rose only slightly compared to the previous quarter. This is indicated by data on industrial production trends published at the end of July. The Federal State Statistics Service (Rosstat) will publish a preliminary estimate of overall economic output for the second quarter on August 13.

For 2025 as a whole, however, the Russian Central Bank does not expect aggregate economic output to stagnate at the previous year’s level. It forecasts a return of the “overheated” economy to “balanced growth” with a GDP increase of 1 to 2 percent. At the same time, it expects the annual inflation rate in the fourth quarter of 2025 to be significantly lower at 6.0 to 7.0 percent than it was a year earlier in the fourth quarter of 2024 (+9.5 percent).

The central bank’s forecasts are discussed in detail at the end of this article. First, here are some insights into how renowned Russia experts Vasily Astrov and Anders Aslund view the current state of the Russian economy.

Vasily Astrov: Above all, the “very restrictive monetary policy” is causing problems

At the end of April, the Vienna Institute for International Economic Studies (wiiw) raised its forecast for this year’s Russian economic growth to +2.0 percent, placing it at the upper end of the central bank’s forecast range. In its spring forecast, the wiiw even expects GDP growth to accelerate to 2.5 percent in 2026. However, there was no mention of this in the latest episode of the podcast “Russia, Gas, Sanctions, Oligarchs” by the Austrian newspaper “Die Presse” featuring Vasily Astrov on July 30. In a conversation with longtime Russia correspondent Eduard Steiner, the wiiw’s Russia expert primarily criticized the Russian Central Bank’s policy.

Astrov cites “the very restrictive monetary policy” as the main reason for the slowdown in the Russian economy’s growth. The extremely high interest rates made borrowing practically impossible while simultaneously providing strong incentives to save. A second reason for the weaker growth, he said, is the sharp drop in oil prices.

According to Astrov, following the economic boom and high inflation of the past two years, the Central Bank now faces an unfamiliar, new situation. In his view, the Central Bank “has not handled this in the best way.”

Astrov points to the loss of growth caused by restrictive monetary policy: An annual inflation rate of 10 percent or even slightly higher was, of course, an argument for the Central Bank—which aims for an inflation rate of 4 percent—to make its monetary policy as restrictive as possible. In recent months, inflation in Russia has also “slowed dramatically.” The Central Bank has thus certainly been successful with its “policy of extremely high interest rates,” but at the cost of a slowdown in growth. From his perspective, Astrov emphasizes, it would therefore have been wise to accept slightly higher inflation. The question is whether an inflation rate of 8 or 10 percent is really so bad that it must be fought at all costs. Astrov cites studies by the IMF and other international economic organizations indicating that inflation rates of 8 to 10 percent do not hinder economic growth.

High interest rates are holding back private consumption

Astrov points out that, according to the latest figures, the rise in household consumption has slowed to the point of near stagnation. However, private consumption has been the main driver of economic growth over the past two or two and a half years (Author: According to the Russian Central Bank’s “Medium-Term Forecast” of July 25, the growth in household consumption will decline from +5.4 percent in 2024 to between +0.5 percent and +1.5 percent in 2025).

The wiiw expert does not believe that the slowdown in wage growth was the main reason for the weakening of private consumption growth. The main reason is the decline in lending. This is because demand for durable consumer goods, cars, and real estate—which is often financed by credit—has declined in particular.

Astrov expects at least two further key interest rate cuts in 2025

Astrov considers the central bank’s previous cut of the key interest rate to 18 percent insufficient. Many companies have stated in surveys that the key interest rate should be no higher than 15 percent for them to seriously consider investing. Many observers now also expect the key interest rate to be cut to 15 or 14 percent by the end of the year. He himself anticipates at least two further key interest rate cuts this year. However, they would only take effect after a time lag. The central bank assumes that the full effect of key rate cuts will only be felt after 6 to 9 months.

Lower interest rates are likely to weaken the ruble—but support the budget

Astrov believes that the easing of monetary policy could lead to a weakening of the ruble exchange rate. A weaker ruble could have benefits for the development of the Russian national budget. While the drop in global oil prices is a problem for Russia, a weaker ruble could lead to an increase in government revenue from the energy sector in rubles (Author: Because Russia’s energy exports are paid for in foreign currency).

Astrov expects, however, that the Russian government will most likely be unable to meet its budget deficit target of 1.7 percent of GDP for 2025. The deficit ratio will almost certainly rise above 2 percent.

Sanctions have not yet caused Russia’s economy to “suffer massively”

Regarding the effectiveness of the sanctions against Russia, Astrov explains that he has always said the sanctions will increasingly harm the Russian economy in the long term. However, he does not believe it is possible to say at this point that the Russian economy is “suffering massively” from the effects of the sanctions.

Regarding the “secondary sanctions” against China and India announced by U.S. President Trump over oil imports from Russia, Astrov says he does not believe Trump will really be willing to pick a fight with India and, above all, China over this. Otherwise, Trump would effectively have to restart the entire negotiation process with China from scratch. In his view, China is in a very strong position to withstand pressure from the U.S. It is fairly certain that Russian oil deliveries will continue, at least to China.

However, according to Astrov, further oil deliveries to India are uncertain. The consequences of halting the very extensive deliveries to India would be difficult to predict. World market prices would then be driven up. In the medium term, however, Russia will naturally try to find other buyers for its oil (see: NDR Info interview with Astrov following the EU’s decision on the 18th sanctions package on July 18 and the ZDF heute report on tariffs imposed on India).

China’s support makes Russia “resilient”

In a radio interview with the Austrian broadcaster Ö1, Astrov also commented on the effectiveness of Western sanctions. In particular, support from China and the “Global South” makes Russia “resilient.” The West has no effective leverage over Russia. Russia is the world’s fourth-largest economy and has the support of China, the world’s largest economy (IMF ranking in international dollars at purchasing power parity). Russia cannot be compared to smaller economies such as Iran.

Anders Aslund: Russia’s economy is stagnating and suffering from high inflation

In an article for “Project Syndicate,” Swedish Russia expert Anders Aslund discusses the development of the Russian national budget in greater detail. On August 7, under the headline “Stagflation Is Hitting Russia’s War Economy,” he outlines the current state of the Russian economy as follows:

“While the Russian economy is not collapsing, it is stagnating and suffering from high inflation.” … “In any case, official growth has fallen this year, likely to 1.4% in the first half of 2025.” …

“An improvement is unlikely. The country’s financial reserves are running low, energy revenues are falling, and there is a growing shortage of labor and imported technology.”

The decline in energy exports is reducing government revenues

Aslund reports on the critical importance of energy exports for financing the national budget:

“Traditionally, half of Russia’s government revenue comes from energy exports; in the past, these accounted for two-thirds of total exports. However, in the face of Western sanctions, Russia’s total exports have plummeted, falling by 27% between 2022 and 2024, from $592 billion to $433 billion.”

Regarding the imminent depletion of government funding sources, Aslund reports:

“Due to Western financial sanctions, Russia has had virtually no access to international financing since 2014. For fear of secondary sanctions, not even China dares to openly finance the Russian state. In fact, two small Chinese banks have just been sanctioned by the European Union for such violations.”

“Russia must therefore make do with the liquid funds in its National Wealth Fund. These have fallen from $135 billion in January 2022 to $35 billion in May 2025 and are expected to be depleted in the second half of the year.”

“The 2025 state budget was based on an oil price of $70 per barrel, but the oil price is now approaching the West’s price cap of $60 per barrel, and the EU has just set a cap of $47.6 per barrel on the Russian oil it still purchases.

Furthermore, the West has sanctioned nearly 600 tankers in Russia’s “shadow fleet,” which will reduce Russian government revenues by at least 1% of GDP.”

“Against this backdrop, the Kremlin has announced that this year

it plans to spend 37 percent of its federal budget—$195 billion (7.2 percent of GDP)—on national defense and security, but will have to cut federal spending from 20 percent of GDP to around 17 percent.”

“However, since the government has already reduced its non-military spending to a minimum, it says it intends to cut its military spending by an unspecified amount in 2026.”

Central Bank’s commentary on its “Medium-Term Forecast”

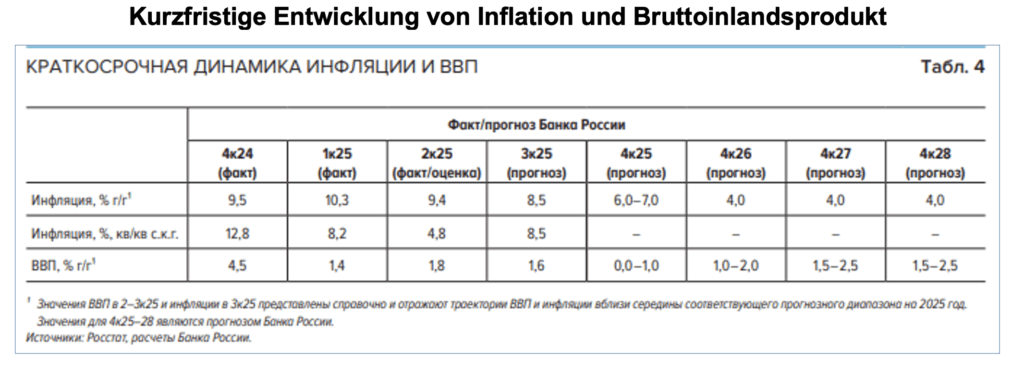

The Russian Central Bank provided further details on its “Medium-Term Forecast,” published alongside the key interest rate decision on July 25, in a detailed “Commentary” on August 6. In the following table from this “commentary,” it forecasts the quarterly development of consumer prices and real gross domestic product

¹ The GDP figures for Q2–Q3x25 and inflation for Q3x25 are for reference purposes and reflect the development of GDP and inflation in the middle of the corresponding forecast range for 2025. The figures for Q4x25–28 represent the Bank of Russia’s forecast. Sources: Rosstat, calculations by the Bank of Russia.

Central Bank of Russia: Commentary on the Bank of Russia’s Medium-term Forecast, August 6, 2025

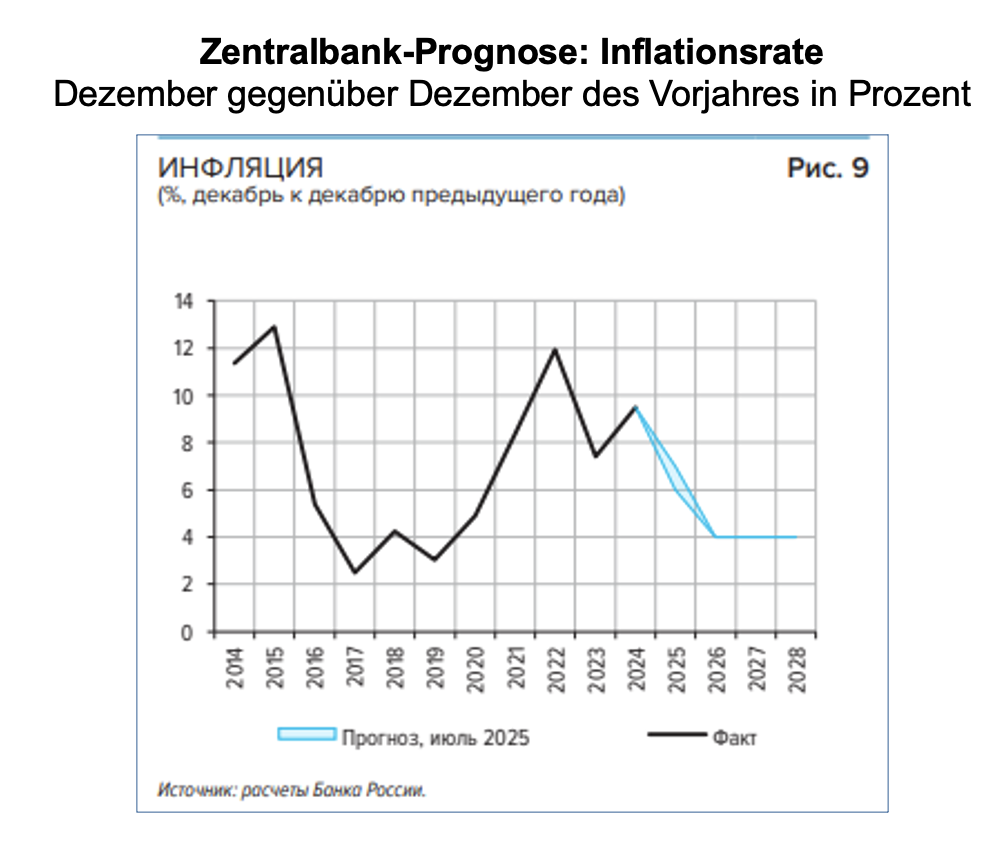

The annual inflation rate will fall to 6–7 percent by the end of 2025

According to the first row of the table above, the year-over-year increase in the consumer price index accelerated to 10.3 percent in the first quarter of 2025. In the second quarter, this annual increase in consumer prices was only slightly lower at 9.4 percent. In the third quarter, the Central Bank expects a further decline in the annual inflation rate to 8.5 percent and to 6.0 to 7.0 percent in the fourth quarter.

The Central Bank’s target annual inflation rate of 4 percent is expected to be reached in the fourth quarter of 2026. In its “Commentary,” the Central Bank cites current monetary policy and the economy’s return to a “balanced growth path” as the rationale:

“The Bank of Russia’s baseline forecast assumes that, given the current monetary policy and the economy’s return to a balanced growth path, annual inflation will reach the target level of 4% again in 2026 and stabilize there thereafter.”

Central Bank of Russia: Commentary on the Bank of Russia’s Medium-term Forecast, August 6, 2025

Inflation has already fallen sharply compared to the previous quarter

The second row of the table above shows the seasonally adjusted increase in consumer prices compared to the previous quarter (extrapolated to an annual rate).

In the first quarter of 2025, this “current” inflation rate still stood at 8.2 percent.

In the second quarter, it fell to 4.8 percent.

In the third quarter, however, the Central Bank expects a sharp acceleration to 8.5 percent. This is due to the increase in public utility rates on July 1, 2025 (see Olga Belenkaya, Finam).

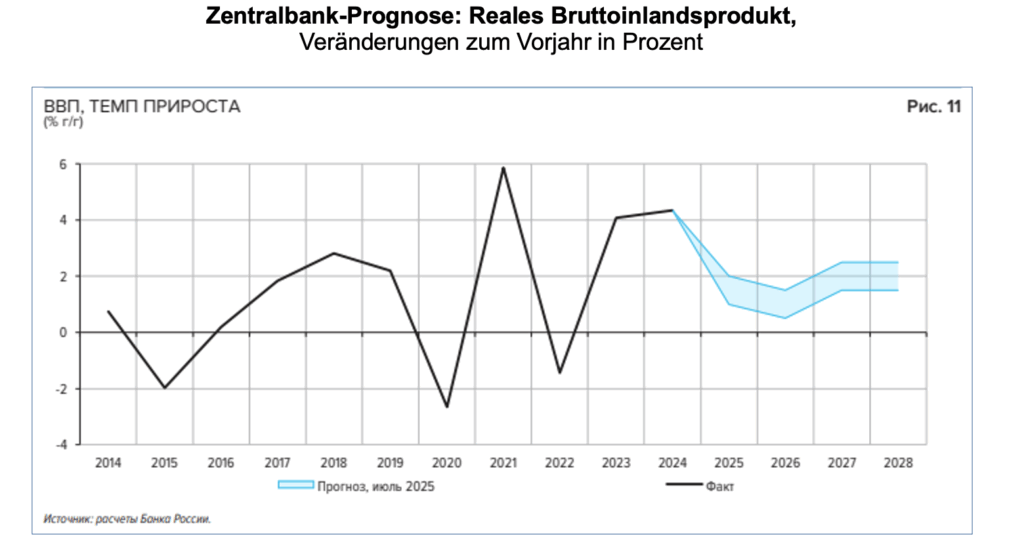

GDP growth falls to 0 to 1 percent in the fourth quarter of 2025

The third row of the table above shows the Central Bank’s forecasts for the annual increase in aggregate economic output. In the first quarter of 2025, Russia’s real gross domestic product was only 1.4 percent higher than in the same quarter of the previous year, according to preliminary Rosstat calculations. The Russian Central Bank assumes that GDP in the second quarter—for which Rosstat has not yet published data—was 1.8 percent higher than a year ago.

For the full year 2025, the Central Bank expects, according to its “medium-term forecast,” that annual economic growth will slow to 1.0 to 2.0 percent—following two years of growth rates of just over 4 percent (2023: +4.1%; 2024: +4.3%).

In 2026, the Central Bank estimates that GDP growth will slow to 0.5 to 1.5 percent year-over-year, but will reach 1.0 to 2.0 percent in the fourth quarter compared to the same quarter of the previous year.

Central Bank of Russia: Commentary on the Bank of Russia’s Medium-term Forecast, August 6, 2025

According to the Russian Ministry of Economic Development, real gross domestic product in the first five months of 2025 was 1.5 percent higher than in the same period of the previous year (TASS). In a survey of analysts conducted by the Reuters news agency at the end of July, participants also expected economic growth of 1.5 percent for the full year 2025.

Further perspectives on the Russian economy

The online magazine “International Investment” has compiled the following additional news and opinions on current economic developments in Russia:

In July, S&P Global reported the sharpest decline in Russia’s manufacturing purchasing managers’ index in three years, driven by weak demand and customer solvency issues. Business confidence is at its lowest level since 2022.

The IMF forecasts growth of just 0.9% for 2025. High interest rates are curbing inflation but also reducing credit availability, which harms consumption and investment.

Alex Kokcharov of Bloomberg Economics says: “There is growing evidence that many sectors are facing serious problems.” The consequences of the war, sanctions, labor shortages, falling oil prices, a stronger ruble, and high interest rates are taking their toll.

Demand in the steel and construction sectors is falling. The CEO of Severstal forecasts a 10% decline in domestic demand for steel.

Car sales fell by 30% in June compared to the previous year.

The coal sector is struggling with sanctions, equipment shortages, and long logistics delays.

Banks are concerned about credit quality. According to Bloomberg, major banks could apply for government aid if the number of defaults rises. Internal borrower ratings are far worse than the official data.

Alexander Kolyandr (CEPA) described the “balanced growth curve” as a euphemism for economic anemia and warned of long-term recession risks (Alexander Kolyandr: Russia’s Bankers Fight Inflation and the Kremlin’s War Addiction, July 31, 2025).

Further reading:

- Business Petersburg; Victoria Grushevskaya: A Natural Outcome: Why the Russian Economy Is Heading for a Recession. CMASF: Russia’s Economy Will Inevitably Slip into a Recession, Aug. 7, 2025

- Finmarket.ru: Russia’s budget deficit stood at 2.2% of GDP in January–July, higher than planned, Aug. 7, 2025

- fr.de; Bona Hyun: The bill and “anemic growth” for Russia’s economy: Key sectors are collapsing, 08/07/25

- Finam.ru; Olga Belenkaya: What was discussed at the Central Bank’s latest meeting, 08/06/25

- dw.com/ru, Oleg Loginov: Russia wants to cap food prices: Should we expect shortages? 08/05/25

- The Spectator, Alexander Kolyandr: Putin’s economic alchemy cannot last forever, 08/04/25

- German-Russian Chamber of Foreign Trade: Focus Analyses, German; also Russian; Russian-Indian Economic Relations Against the Backdrop of Trump’s Tariff Threat, 08/04/25

- Business Insider; Huileng Tan: Inflation under control, growth at risk: Russia’s economy at a turning point, 08/04/25

- The Observer; Kim Willsher and Nina Kuryata, Ukraine and Defense Editor: Putin unfazed as his economy holds up; in Russian at Inosmi.ru; 08/03/25

- moscowtimes.ru: Rosstat began hiding key economic data after Putin demanded that a recession not be allowed, August 1, 2025

- PSB; Denis Popov: Rosstat published only an abridged collection of macroeconomic statistics for June and the first half of the year, August 1, 2025

- PSB Analytics: The risk of an economic slowdown remains; the leading indicator for manufacturing activity reached its lowest level since March 2022 in July, August 1, 2025