Russia and Eastern Europe: New Economic Data and Forecasts

Author: Klaus Dormann

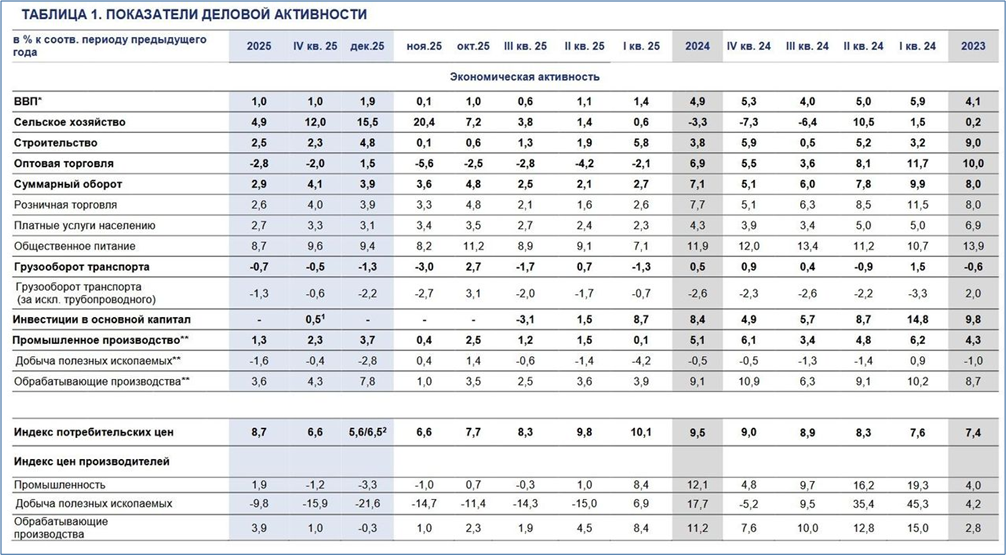

Russia’s annual economic growth has fallen from 4.9 percent in 2024 to just 1.0 percent in 2025. This is according to estimates published Friday by the Federal State Statistics Service (Rosstat). Previously, Rosstat had estimated growth in 2024 at 4.3 percent. In 2023, the Russian economy grew by 4.1 percent. Rosstat has now confirmed this figure once again.

Rosstat’s estimate for Russia’s GDP growth in 2025 matches exactly the Ministry of Economic Development’s September forecast of 1.0 percent. It falls at the upper end of the Central Bank’s forecast range of 0.5 to 1.0 percent, published in October.

The majority of analysts had previously expected Russia’s economic growth last year to be slightly below one percent. A survey conducted by the Russian Central Bank in late January/early February yielded an average forecast of 0.9 percent GDP growth for 2025. In its “Winter Forecast” released last week, the “Vienna Institute for International Economic Comparisons” (wiiw) estimated Russian economic growth at an even lower 0.7 percent.

Results of the Central Bank Survey on Inflation, Key Interest Rates, and Growth

Ahead of its next key interest rate decision on February 13, the Russian Central Bank once again conducted an analyst survey (Survey Calendar). The following table shows a selection of the results from this survey.

For the year 2026, the approximately 30 participants expect the following trends in consumer price inflation, the key interest rate, and real GDP growth:

The annual increase in the consumer price index will slow to 5.3 percent in December 2026. By December 2025, the annual inflation rate will have already fallen to 5.6 percent. At the end of 2024, it had reached 9.5 percent.

The annual average inflation rate for 2026 will fall to just 5.6 percent. The annual average for 2025 was 8.7 percent, slightly higher than in 2024 (+8.4 percent).

The average annual key interest rate for the current year will be 14.1 percent, a good 5 percentage points lower than in 2025 (19.2 percent).

Annual economic growth will pick up only slightly to 1.1 percent in 2026. In 2025, it is expected to slow to just 0.9 percent.

Results of the Central Bank survey from January 30 to February 3, 2026

(results of the December survey in parentheses)

Bank of Russia: Macroeconomic Survey of the Bank of Russia, February 4, 2026 (excerpt)

CBR Survey: Inflation Will Still Significantly Exceed the 4% Target at the End of 2026

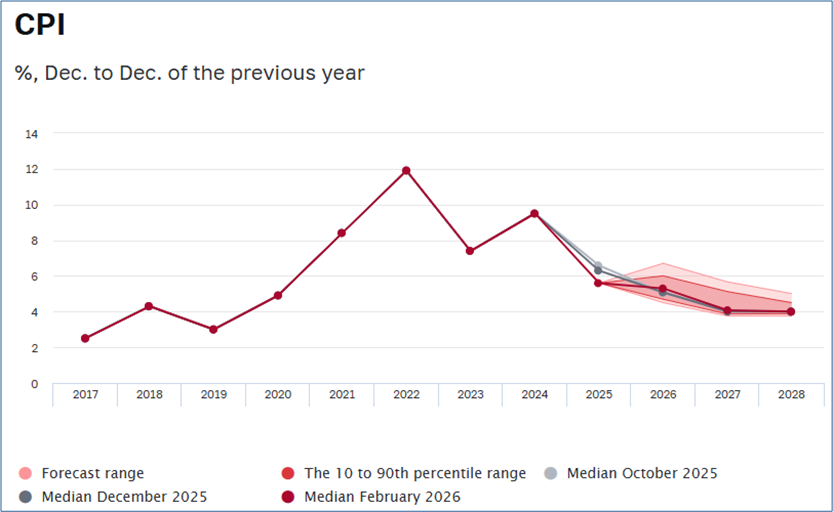

The following figure shows the projected development of the inflation rate according to the analyst survey. The Central Bank’s target inflation rate of 4.0 percent will not yet be reached by the end of 2026 based on the average of the survey participants’ estimates (black line). According to the survey, consumer prices will still rise by 5.3 percent in December 2026 (thus slightly exceeding the range of 4.0 to 5.0 percent cited in the central bank’s medium-term forecast). By the end of 2027, the survey indicates that the inflation target will be nearly met, with a price increase of 4.1 percent.

Consumer

Price Index: Year-over-year increase in December compared to December of the previous year (in %)

Bank of Russia: Macroeconomic Survey of the Bank of Russia, February 4, 2026

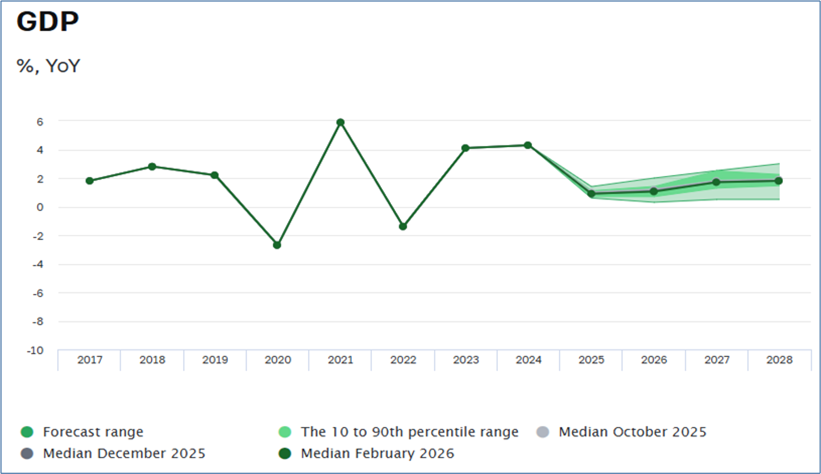

Skeptical growth forecast for 2026: GDP to rise by only about 1 percent

Survey participants’ expectations regarding economic growth have not changed since the December survey. Following a 0.9 percent increase in real gross domestic product in 2025, they continue to expect barely higher growth of 1.1 percent in 2026. In 2027, GDP growth is expected to accelerate to 1.7 percent and to 1.8 percent in 2028. However, this means that analysts’ growth forecasts from 2027 onward remain well below the government’s projections, which anticipate growth rates of 2.8 percent in 2027 and 2.5 percent in 2028.

Real Gross Domestic Product

Year-over-year change in percent

Bank of Russia: Macroeconomic Survey of the Bank of Russia, February 4, 2026

What President Putin Says About Low Growth and Inflation

“The slowdown in economic growth in 2025 was not only to be expected; one could even say it was man-made,” President Putin commented on the current GDP trend in his opening remarks at this year’s first government conference on economic policy on February 3 (see the Presidential Administration’s website). The lower growth, according to the President, is linked to targeted measures to reduce inflation.

Three days before the release of Rosstat’s data for 2025, Putin noted that Russia’s growth rate in 2025, at 1 percent, was below the high growth rates of the previous two years. Russia’s inflation rate had fallen to 5.6 percent by the end of 2025, down from 9.5 percent a year earlier.

The president noted that inflation had accelerated to 6.4 percent at the beginning of 2026. He emphasized: “This, too, was to be expected and is partly attributable to the restructuring of the tax system, including the VAT increase” (Kommersant.ru).

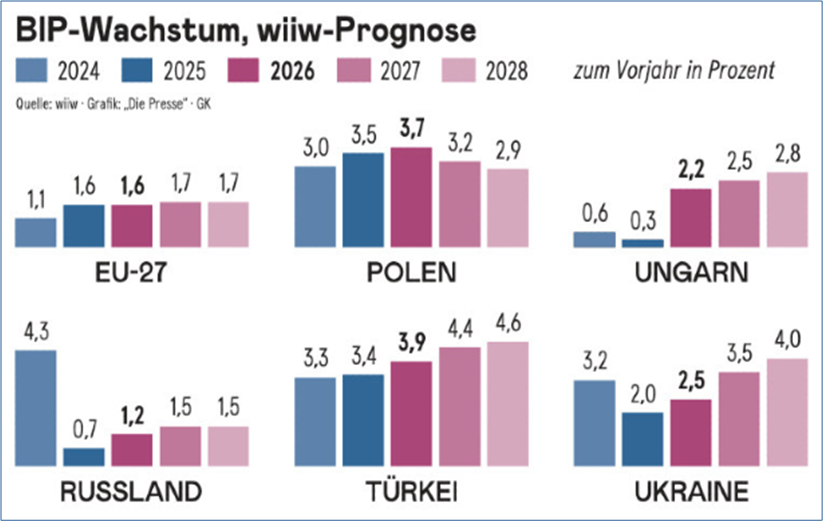

wiiw Growth Forecasts for Central and Eastern Europe and Turkey

The “Vienna Institute for International Economic Comparisons” updated its quarterly forecast last week for economic developments in Central, Eastern, and Southeastern Europe, including Turkey.

The following figure from a report in the Austrian newspaper “Die Presse” shows the wiiw’s forecasts for economic growth in Poland, Hungary, Russia, Turkey, and Ukraine compared with the growth forecast for the 27 EU member states.

Of the selected countries, Turkey will experience the strongest growth in 2026 (3.9 percent).

Poland will achieve the highest growth in the group of 11 EU member states in Central and Eastern Europe, at 3.7 percent, followed by Lithuania (3.0 percent) and Croatia (2.8 percent)

In Hungary, which in 2025 will be the slowest-growing country in the EU-CEE 11 group with a gross domestic product increase of just 0.3 percent, growth will pick up to 2.2 percent in 2026.

The entire group of 11 EU member states in Central and Eastern Europe will continue to grow at nearly twice the rate (2.6 percent) of the eurozone countries (+1.4 percent) and the EU-27 (1.6 percent) in 2026.

Die Presse; David Freudenthaler:

wiiw Forecast. Growth from the Ruins: Ukraine’s Economy Continues to Grow Despite Attacks, 02/04/26

wiiw forecasts for Russia and Ukraine

In Russia, the previously strong economic growth has slumped to just 0.7 percent in 2025, according to wiiw estimates. In 2026, the institute says, it will recover to 1.2 percent. Ukraine’s economy will grow by 2.5 percent in 2026—just as it did in 2025—more than twice as fast as the Russian economy.

These wiiw forecasts for Russia and Ukraine are based on the assumption that the war against Ukraine continues and there is no easing of U.S. sanctions. The wiiw press release assesses the consequences of an end to the war for Russia as follows:

“In the short term, the elimination of spending on soldiers’ wages and compensation for their families—which accounts for roughly 2% of GDP—could lead to a demand shock. In the medium term, however, the economy is likely to benefit from the easing or partial lifting of U.S. sanctions.”

Above all, the renewed access to Western high-tech that would then become possible would be of great significance for the Russian economy, according to Vasily Astrov, a Russia expert at wiiw.

Downside risks to the wiiw forecasts:

Further U.S. tariffs, budget deficits in Central and Eastern Europe, an “imposed peace” in Ukraine

The wiiw identifies the following “downside risks” for its forecasts:

The greatest downside risk is posed by further U.S. tariffs on imports from the EU: “Although direct trade flows between the U.S. and Central and Eastern Europe are negligible, lower U.S. demand for European industrial products due to further tariffs on imports from the EU could indirectly weigh on the Central and Eastern European region, as it is closely intertwined with Western European industry,” explained Richard Grieveson, deputy director of the wiiw and lead author of the winter forecast.

According to Grieveson, another risk is the high budget deficits in some Central and Eastern European countries, particularly those of Romania, Hungary, Poland, and Slovakia. In the event of turbulence in the bond markets, these deficits could force governments to implement austerity measures that hinder growth. Romania is already pursuing such a policy.

“A peace in Ukraine dictated by Russia” could also have a negative impact on the region. “The lack of credible security guarantees for Ukraine is likely to deter investors and lead to significant uncertainty, as Moscow is expected to destabilize the entire region in such a scenario,” warns Grieveson.

wiiw: Very high interest rates have pushed Russia’s economy into a “slump”

The wiiw currently views the Russian economy as being in an “economic slump.” Regarding the causes, the wiiw press release states:

“The main cause of the current economic slump in Russia is the Russian Central Bank’s still very high key interest rates, currently at 16%, which make loans expensive and thus stifle the economy.”

“Compounding the problem are low oil prices combined with U.S. sanctions against the energy sector and far too little investment, which is likely to decline further.”

In its “Country Overview Russia,” the wiiw comments on the consequences of the “extremely restrictive monetary policy”:

“Thanks to an extremely restrictive monetary policy, inflation has largely been brought under control. However, this success was accompanied by a weakening of domestic demand and a slowdown in GDP growth.

Stagnation, moderate oil prices, and a strong ruble put pressure on government revenues, leading to further tax increases, including on the value-added tax.”

For 2026, the wiiw, like the government, expects slightly more growth than in 2025

The wiiw estimates real gross domestic product growth in 2025 at 0.7 percent, slightly lower than the 1.0 percent reported by Rosstat on February 4.

In 2026, the wiiw expects a slight acceleration in GDP growth to 1.2 percent. The Russian government expects only slightly stronger growth this year (1.3 percent).

However, the government anticipates a sharp acceleration in growth to 2.8 percent in 2027. In contrast, the wiiw considers growth of only 1.5 percent—just over half that level—to be possible next year.

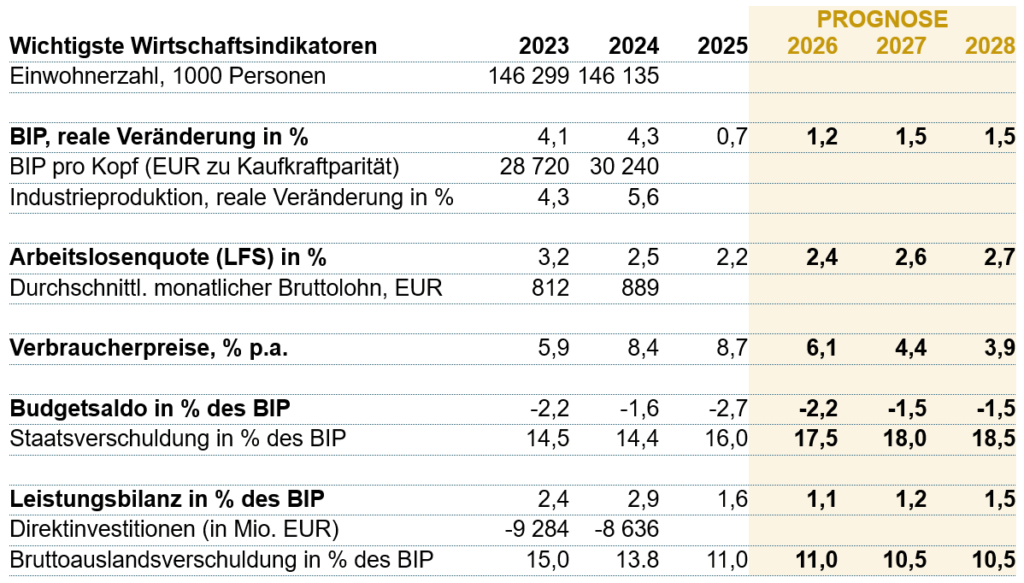

wiiw Country Overview: Russia

wiiw: Country Overview Russia, 02/04/26

Rosstat Data for 2025: How Key Sectors Performed Differently

In its overview above, the wiiw was not yet able to take into account the Rosstat reports from February 6 on economic data for the year 2025. However, it apparently did take into account that the year-over-year increase in consumer prices accelerated to 8.7 percent in 2025 compared to 2024 (see also the table above showing the results of the Central Bank’s survey).

According to Rosstat, industrial production rose by 1.3% year-over-year in 2025. In 2024, the increase in industrial production had reached 5.1%. In December 2025, year-over-year growth in industrial production accelerated to 3.7%, following a 0.4% increase in November. Compared to the previous month of November, seasonally adjusted industrial production rose by 2.3% in December (Finam.ru).

Within the industrial sector, production in the “manufacturing industry” grew by 3.6% year-over-year from 2024 to 2025. At the same time, however, production in the “mining and extraction of raw materials” sector fell by 1.6% (Finmarket.ru).

In 2025, production in agriculture (+4.9%) and the construction sector (+2.5%) grew more strongly than in industry.

While production in wholesale trade fell by 2.8 percent, retail trade recorded growth of 2.9%.

Freight traffic declined by 0.7% in 2025 (Finmarket.ru).

The annual average unemployment rate fell to 2.2 percent for the first time in 2025 (RT).

Average real disposable income rose by 7.4 percent in 2025 (Interfax).

Table from the Russian Ministry of Economic

Development’s report “On the Current State of the Economy,

” including data on GDP and production by sector

Source: Finam.ru: Industrial production in Russia grew by 1.3% in 2025, 02/06/26

wiiw expert Astrov: The population’s standard of living is beginning to stagnate,

but Russia’s government can still afford the war financially

Regarding current developments in the Russian economy, wiiw Russia expert Vasily Astrov also commented in a podcast by the Austrian newspaper “Die Presse” on January 21 in a conversation with Eduard Steiner. In summary, Astrov stated (from min. 12):

The standard of living of the Russian population is beginning to stagnate. While unemployment is still very low, wage growth is no longer as high as it used to be.

I believe President Putin is already aware that the Russian economy is stagnating, that domestic demand is being held back by very high interest rates, and that sanctions are certainly having an impact in certain areas. For example, in recent months we have seen that the price discount on Russian oil has risen sharply due to the sanctions imposed by U.S. President Trump against the two leading Russian oil companies, Rosneft and Lukoil.

This is not good news for the Russian budget. A quarter of the federal budget’s total revenue comes from the energy sector—in other words, essentially from oil and gas sales. On the other hand, from a purely financial standpoint, the Russian government can still afford to continue the war. The government can finance budget deficits by taking on debt from domestic banks.

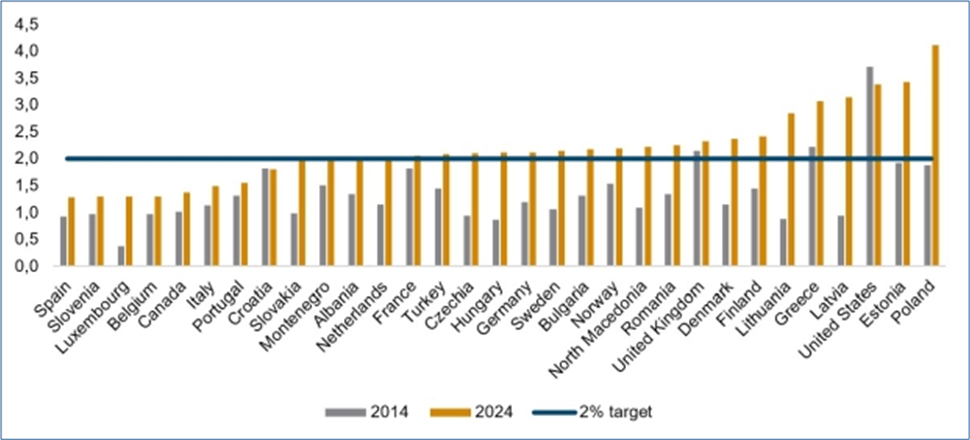

At 7 or 8 percent, the share of war spending in Russia’s gross domestic product is actually not particularly high. The Baltic states and Poland spend about 5 percent of GDP on the military—not much less—even though they are not at war (see GTAI: Baltic States: Pioneers in Defense Spending, 09/05/25).

The following figure from a wiiw study published a year ago shows the increase in defense spending in NATO countries from 2014 to 2024.

Defense spending by NATO members, % of GDP

wiiw; Richard Grieveson, Olga Pindyuk, Vasily Astrov:

Three years of full-scale war in Ukraine: What would a dictated peace mean? 02/24/25

Russia and the EU are actually “ideal trading partners”

In response to a question from Eduard Steiner regarding the development of economic relations between Russia and the EU, Astrov emphasized that the EU and Russia are “actually ideal trading partners.” Trade between the EU and Russia offers advantages to both sides. Astrov argues as follows:

Europe “actually” needs Russian energy and Russian raw materials. And Russia “actually” needs European technologies to modernize.

At the moment, however, there is a risk that Russia will fall further and further behind technologically in the medium to long term due to the sanctions, particularly the export bans on high-tech goods. An easing or, ideally, even a lifting of the sanctions would greatly help the Russian economy.

Energy has become much more expensive in Europe due to the decoupling from Russia

On the other hand, it would be a great help to the European economy if Russian energy were to return to the European market. In the gas market, Europe’s current dependence on U.S. liquefied natural gas (LNG) would decrease. This would provide the EU with more alternative gas suppliers. LNG from the U.S. has become significantly more important in Europe since the war broke out and sanctions were imposed on Russia.

Energy has become much more expensive in Europe due to the decoupling from Russia. We have seen what has happened in energy-intensive industries in many European countries, and especially in Germany. They have shrunk massively because they are no longer internationally competitive at current energy prices.

Recommended reading:

- Vienna Institute for International Economic Studies (wiiw): Winter forecast for Eastern Europe: Solid growth despite uncertainties; Press Releases: English, German; Forecast Report, Executive Summary; 02/04/26; Country Overview Russia; wiiw in the press

- wiiw, Doris Hanzl-Weiss: Eastern Europe is Austria’s most important trading partner and provides strong growth momentum, 02/04/26

- wiiw: New Podcast – CEE Outlook 2026: Making Decisions Amid Uncertainty; Executive Director Mario Holzner and Deputy Director Richard Grieveson discuss the geopolitical and economic outlook for Central and Eastern Europe in 2026; 02/03/26

- RT.ru; Vladimir Zegoyev: Rosstat forecasts record economic growth for Russia of 213 trillion rubles in 2025. In 2025, the Russian economy will grow by 1%; 02/07/26

- The Bell.io; Denis Kasyanchuk: Rosstat estimates Russia’s economic growth in 2025 at 1%, 02/06/26

- Finmarket.ru: Russia’s GDP grew by 1.0% in 2025, 02/06/26

- Kommersant.ru: Russia’s GDP grew by 1% in 2025, 02/06/26

- Finam.ru: Russia’s GDP growth in 2025 was 1%, 02/06/26

- Interfax.ru: The Ministry of Economic Development reported a rise in GDP growth to 1.9% for December, 02/06/26

- Finmarket.ru: Output in the Russian Federation’s core sectors rose by 1.4% in 2025, 02/06/26

- Finam.ru: Industrial production in Russia grew by 1.3% in 2025, 02/06/26

- Finmarket.ru: Industrial production in Russia will grow by 1.3% in 2025, 02/06/26

- Finam.ru: The unemployment rate in Russia rose to 2.2% in December 2025, 02/06/26

- Interfax.ru: Real disposable income of the Russian population rose by 7.4% in 2025, 02/06/2

- Finam.ru: Real wages in Russia rose by 4.8% in the first eleven months of 2025, 02/06/26

- Finam.ru; Olga Belenkaya: More reasons for a pause ahead of the Bank of Russia meeting on February 13, 02/06/26

- Finam.ru; Yuri Kozlov: What lies ahead for the ruble in 2026? 02/06/26

- Finam.ru: Russia’s budget deficit amounted to 1.7 trillion rubles in January, 02/06/26

- Politcom.ru; Marina Voitenco: January “Stalemate” in Macro Trends 2026; 02/05/26

- Finam.ru; Maria Babanova: Oil prices have let us down. Is the Russian budget on the brink of collapse? 02/05/26

- Alfa Bank: Economy and Trends: Central Bank Macroeconomic Survey: What Experts Expect, 02/04/26

- Finmarket.ru: Analysts have raised their inflation forecast for Russia in 2026 to 5.3%, 02/04/26

- Finmarket.ru: The inflation situation in November, December, and January is largely developing in line with the Central Bank of the Russian Federation’s October forecast. 02/04/26

- The Bell.io; Alexandra Prokopenko; Alexander Kolyandr: All eyes back on inflation, 02/04/26

- The Overshoot; Matthew C. Klein; Russia’s war spending may be running out of steam, 02/03/26

- Finmarket.ru: Putin: The impact of the VAT increase on price growth will be short-lived, 02/04/26

- Kommersant.ru: Putin described the slowdown in GDP growth in 2025 as man-made. 02/03/26

- en.kremlin.ru: Meeting on economic issues. The President held a meeting on economic issues, 02/03/26

- Joe Blogs: Russia crumbles; I look at inflation, interest rates, employment, and growth prospects to explain why the slowdown is not temporary, but structural, Video, 18 min., 02/04/26; Russia Breaking: This video breaks down what the latest PMI data is showing — including falling employment, weakening exports, inventory drawdowns, and persistently soft demand conditions, 02/02/26

- Finmarket.ru: According to Central Bank analysts, the knock-on effects of January’s inflation require maintaining a restrictive monetary policy and cautious interest rate decisions, 02/03/26

- Central Bank Report “Talking Trends” from the Economics Department: What are the trends saying? Archive (RU); + Archive (EN); Central Bank Press Release: What are the trends saying? No. 1 (84) / February 2026; 02/03/26

- Euromaidan; Peeter Helme: Russia’s oil revenues collapse 24% as global prices slide further (INFOGRAPHICS); Deficit hits $72 billion—highest since 2009—as war spending peaks, 02/02/26

- Merkur.de; Nils Thomas Hinsberger: A severe blow to Putin’s economy: According to Trump, India wants to stop buying Russian oil, 02/02/26

- Merkur.de; Vasily Astrov, wiiw, in an interview with Matthias Schneider: “Shock” for Russia’s economy: Expert shows which sanctions are effective. Are the sanctions not yet tough enough?, 02/02/26.

- bne IntelliNews: Russian manufacturing PMI contracts at a slower pace but VAT hike fuels sharp rise in inflation, 02/02/26

- ACRA Ratings: Macroeconomic Forecast for Russia: Where Is the Gas, Where Is the Brake: Russia and the World in Search of Balance, 02/02/26

- Realnoevremya, Digital Economist Ravil Akhtyamova: What Will Become of the National Welfare Fund? Infrastructure, Industry, and Banks Are the Fund’s New Priorities, 02/02/2026

- The Riddle; Andras Toth-Czifra: Russia’s Industrial Winter; Andras Toth-Czifra on the political economy of industrial decline in the Russian automotive industry and metallurgy, 02/02/26

- Inosmi.ru; Berliner Zeitung, Michael Maier: Russian Gas Import Ban: Has the EU Left a Loophole for U.S. Supplies? 02/01/26