Russia and China: More Tourists, Fewer Business Deals

The circumstances seemed favorable for “Power of Siberia 2,” the planned second gas pipeline from Russia to China, known internationally by its English name. One day before Russian President Vladimir Putin departed for Beijing on May 19, 2026, his advisor Yuri Ushakov had announced “very detailed” talks on the mammoth project, which both countries have been negotiating for eleven years. With a capacity of 50 billion cubic meters of gas, the pipeline is intended to connect the West Siberian gas fields to China. Russia has repeatedly pushed the project forward, especially since it has largely lost its European customers after 2022. But the Chinese doubt whether they would actually need that much additional Russian gas over a contract period spanning several decades.

Despite Hormuz: No Breakthrough on Pipeline Project

This time, however, Russian negotiators traveled to China with high hopes, the U.S. news agency Bloomberg learned from government sources. Given the war in Iran and the blockade of the Strait of Hormuz, the Chinese should be more interested in concluding the negotiations, the argument went. Yet even what the International Energy Agency (IEA) has called “the greatest threat to energy security in history” failed to yield a breakthrough for Power of Siberia 2. Putin and Xi Jinping signed a total of 40 documents or witnessed their signing; the gas pipeline is not mentioned in any of them.

In addition to unresolved economic issues, which we have already outlined in a background report, the project has now taken on a geopolitical dimension, according to an analysis by the Warsaw Center for Eastern Studies (OSW) from late 2025. According to the report, Beijing is also hesitating because signing a supply contract would mark China’s visible break with the West. This would allow Russian gas to enable Beijing to divert liquefied natural gas (LNG) from existing supply contracts to other markets, thereby competing with the world’s largest LNG supplier, the United States. So far, the authors conclude, China is not ready to take this step.

Power of Siberia 2 had already dominated the headlines during Putin’s last visit to Beijing last September. At that time, the Russian side reported that the state-owned companies Gazprom and its Chinese counterpart CNPC had signed a “legally binding memorandum” regarding the construction of the pipeline. Confirmation from China is still pending, and no details of this agreement have been made public.

Tourism Boom Thanks to Visa-Free Travel

Both meetings yielded concrete results in a completely different field: tourism. As early as September 2025, both sides had agreed on mutual visa-free travel. It was a historic first, as despite their geographical and ideological proximity, citizens of the two giant nations had never been able to visit the neighboring country without difficulty. For Russian tourists, visa-free travel took effect as early as September 15, 2025; in the opposite direction, this did not happen until December 1, 2025. The arrangement was originally intended to remain in effect until September 2026. In the context of Putin’s recent visit to Beijing, it was extended until the end of 2027.

Even before visa-free travel, Chinese tourists dominated travel to Russia. In 2025 as a whole, Russian border guards counted around 834,500 tourists from China—more than ten times the approximately 75,000 visitors from Saudi Arabia, which ranked second. In the first quarter of 2026, the visa-free regime caused numbers to rise sharply in both directions, as expected. 154,000 tourists from China represented an increase of more than 44% compared to the same quarter the previous year. This meant that more than half of the total 293,000 tourists in Russia came from China. If the trend continues, the number could rise to 1.2 million visitors for the full year. Before the pandemic, Russia welcomed a total of more than 5 million foreign tourists, 1.5 million of whom were from China.

Conversely, visa-free travel had already helped China rise to become the second-most important destination for Russian tourists by 2025. Just under 2.5 million visits represented a 30% increase over 2024 and placed China in second place, ahead of the United Arab Emirates with 2.4 million visits and behind Turkey with 6.9 million visits. In the first quarter of 2026, the number of Russian visitors to China actually rose by nearly 54% to 690,000. Only Thailand, with 726,000 visits during the winter months of January through March, ranked ahead of China. However, these outbound figures from the Russian Border Guard Service also include transit trips to other Asian countries. The tour operator Space Travel estimates the number of actual tourists to China in the first quarter of this year at 380,000, or slightly more than half of the recorded tourist departures to China. For 2025, this would translate to approximately 1.4 million actual tourist trips from Russia to China. Space Travel expects 150% growth for the full year 2026, which would drive the number to nearly 3.5 million tourists. Package tour operators are already reporting a 2- to 5-fold increase in bookings for China compared to the previous year, with simplified entry procedures being among the key factors driving demand for China, according to Pegas Touristik, one of Russia’s leading travel companies.

Trade: First Decline Since the Pandemic

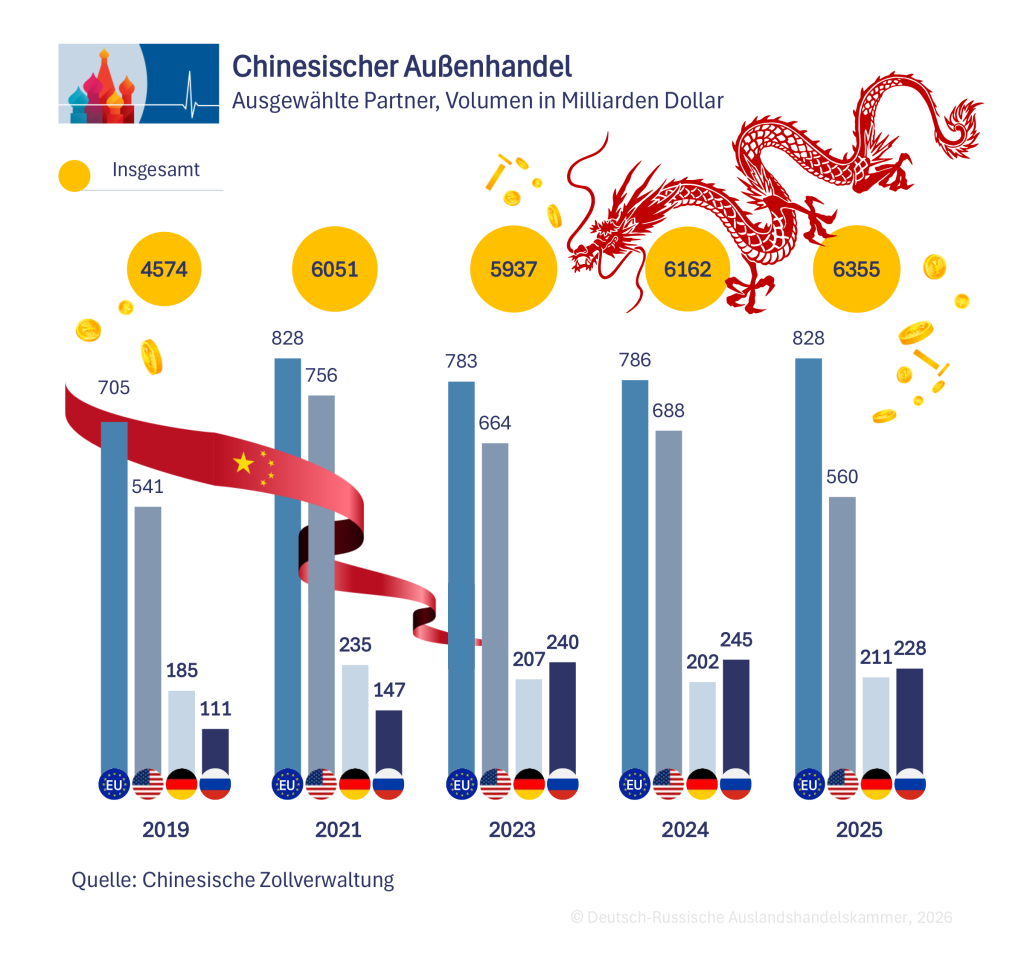

In contrast to tourism, Russian-Chinese trade has already passed its boom phase. Mutual trade volume surged from around $110 billion between 2018 and 2020 to more than $240 billion in 2023, according to statistics from the Chinese Customs Administration. After a modest increase of just 2% to $244.8 billion in 2024, 2025 saw the first decline since 2020. During the pandemic year, trade fell by 2.7% to $108 billion; in 2025, the decline amounted to nearly 7%, to $228 billion.

One reason for the decline is the drop in commodity prices, which in 2025 were below the levels of previous years. Russian exports to China, which consist largely of crude oil and other fossil fuels, fell by 3.9% to $124.8 billion. At the same time, imports from China—primarily industrial goods and machinery—plummeted by 10.4% to $103.3 billion. This is due not only to Western sanctions and restrictions on international payments, but also to domestic factors, notes renowned China and trade expert Sergei Zyplakov in a research report. These include Russia’s high key interest rate and labor shortages, as well as the limited Russian market for imports from China. These imports experienced a boom from 2021 to 2023 because they replaced imports from the EU and filled the niches vacated by Western companies following their withdrawal from Russia, explains Zyplakov.

Last summer, Russia’s Trade Minister Anton Alikhanov also noted a partial saturation of the Russian market with Chinese goods. While the “expansion of goods” is reaching its limits, the minister hopes that the share of high-tech products in imports will increase in the future. In the long term, a “technological-industrial partnership” between the two countries is more promising than mere trade in goods, Alikhanov explained.

Two Unequal Trading Partners

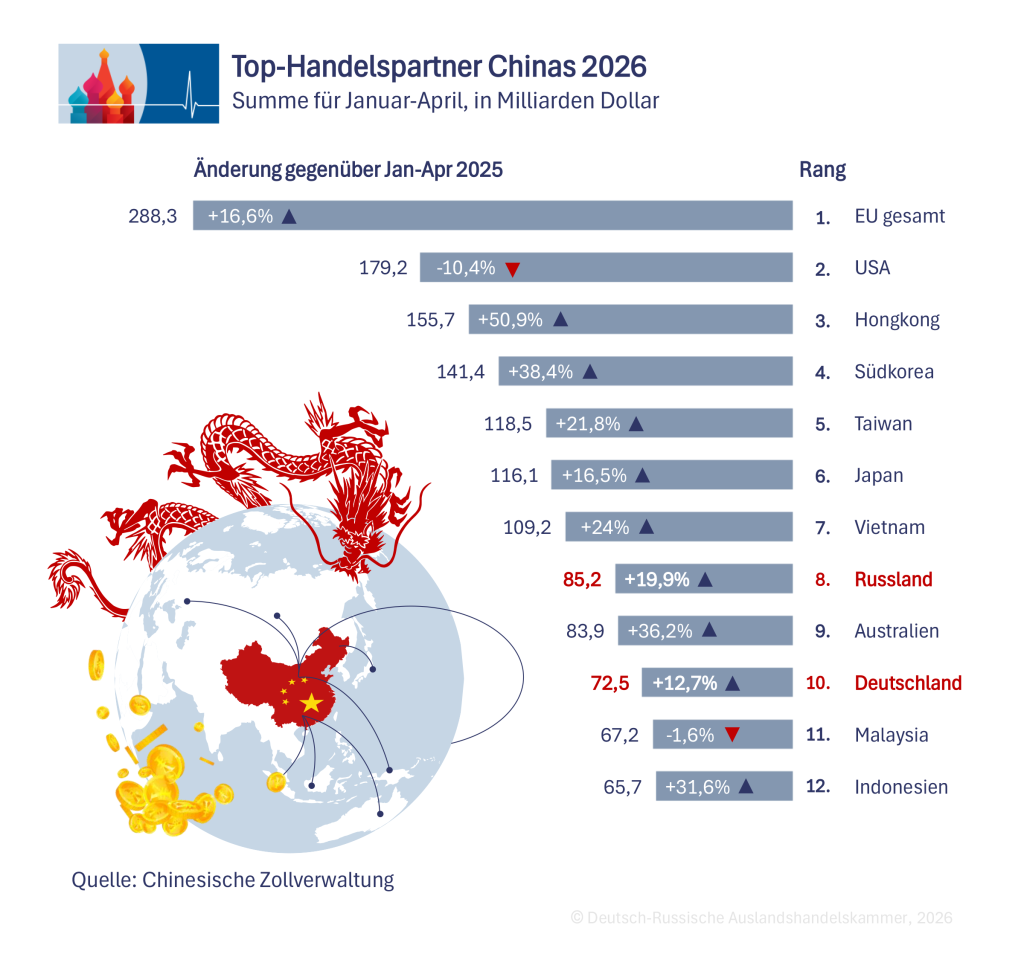

So far, economic relations between the two countries have been characterized by a twofold imbalance. For Russia, China is by far the most important trading partner, while for China, Russia is just one partner among many. Last year, for example, Russia ranked tenth among China’s export destinations, accounting for 2.7% of Chinese exports. In terms of Chinese imports, Russia’s 4.8% share placed it sixth. The second asymmetry lies in the structure of the mutual exchange of goods. While Russia primarily supplies raw materials such as oil, gas, and coal, it imports industrial goods and other finished products from China.

According to Industry and Trade Minister Alikhanov, the path to greater balance lies in a portfolio of 63 joint investment projects worth approximately $130 billion. Russian officials sometimes put the number at more than 80 bilateral projects worth $200 billion. This refers to a list compiled by the Russian-Chinese Commission on Investment Cooperation. As of July 2024, it contains 63 “important” and another 23 “promising” projects. According to an analysis by German economist Janis Kluge, most of these projects “have not progressed beyond the announcement stage even after many years,” and new projects were predominantly added between 2014 and 2019.

Chinese Investments: Slump Since 2022

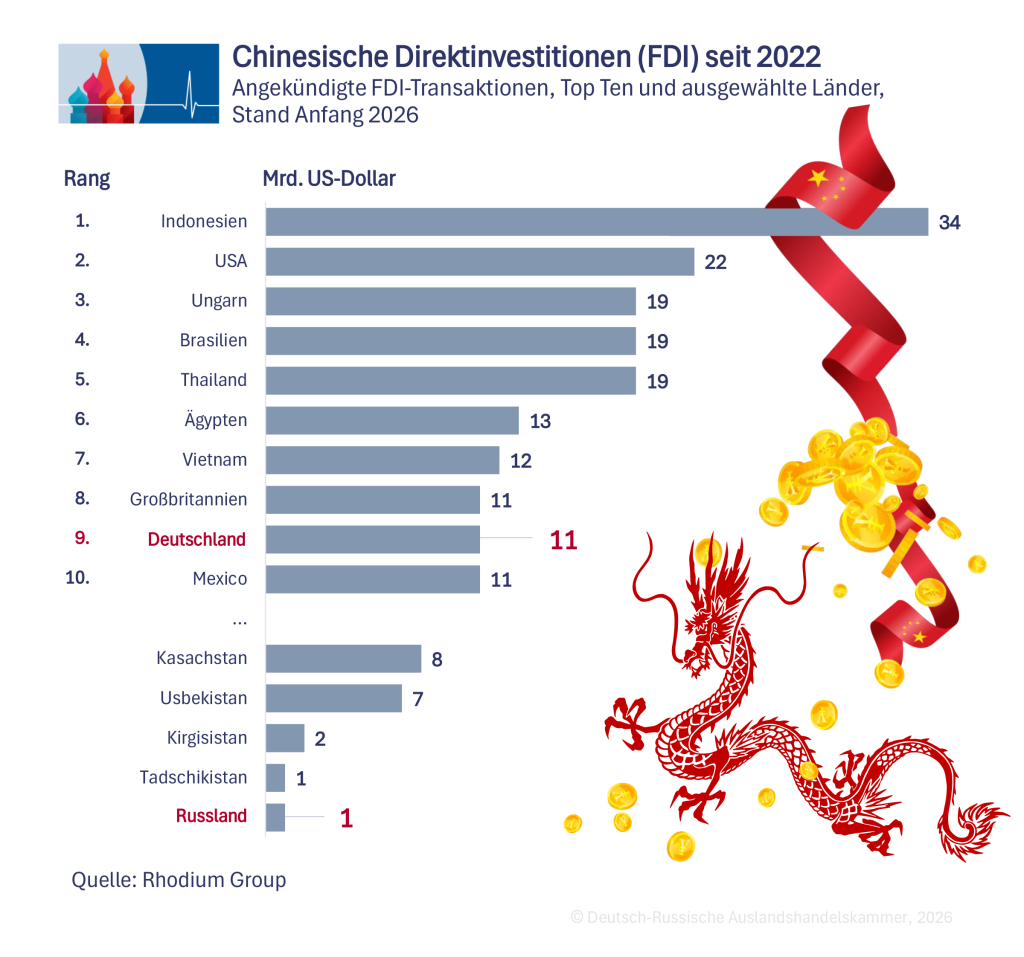

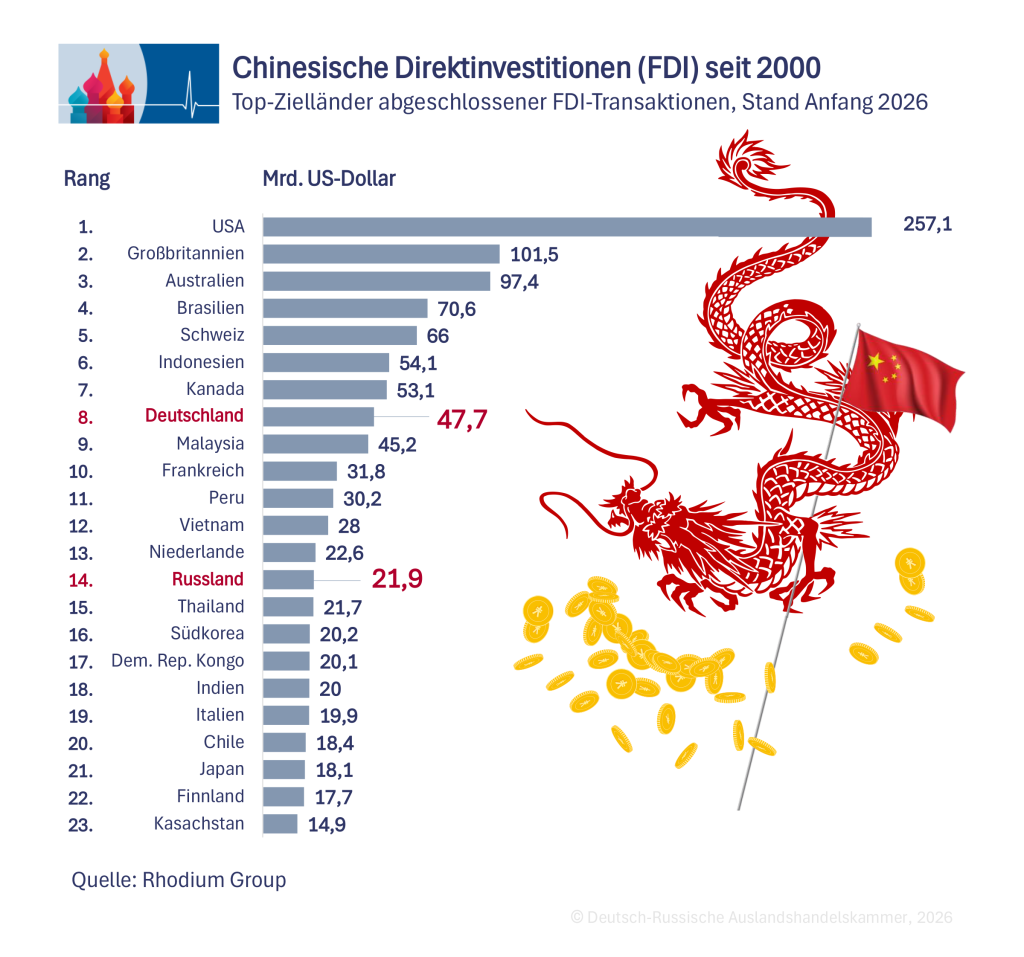

The volume of actual Russian-Chinese investments is more modest. The American Enterprise Institute (AEI) has recorded no Chinese investments in Russia at all since 2021. The Washington-based think tank estimates the volume of investments recorded since 2005 at $34 billion. By comparison, AEI puts investments in Germany at $56 billion, of which nearly $5.3 billion has been made since 2022. According to the investment tracker of the U.S. think tank Rhodium Group, Chinese investment transactions in Russia since 2000 total around $22 billion, practically the same amount as in neighboring Thailand. However, according to Rhodium, Chinese foreign direct investment (FDI) also originated almost entirely from the period before 2022. Since then, there have been announcements of Chinese direct investment in Russia totaling just $1 billion.

The figures only include inflows of direct investment, not outflows or changes in the stock of FDI. The total stock of foreign FDI in Russia decreased from around $500 billion in 2021 to about $220 billion by the end of 2024, according to a study by BOFIT, the research institute of the Bank of Finland, citing Russian statistics. Foreign companies have generally refrained from making new investments in Russia in recent years. The study attributes this primarily to concerns about secondary sanctions and the “capriciousness” of Russian economic policy. An example of the latter is the seizure of foreign companies, which so far, however, has targeted only owners from so-called “unfriendly” Western countries. According to the study, the fact that companies from friendly China are also following this trend is evidence of the “superficiality” of Russian-Chinese economic relations.

Automotive Manufacturing as an Investment Destination

A large portion of Chinese investment since 2022 has gone to the automotive industry. For instance, the automaker Great Wall Motor expanded its factory in Tula—built back in 2019—with an engine plant in 2024. In 2026, the parent company of the Haval brand also plans to open a factory for auto parts there, for which the Chinese are investing a total of 30 billion rubles, equivalent to around 360 million euros.

Since 2022, Chinese manufacturers have conquered the Russian auto market. According to industry service Awtostat, the Chinese share of imported new cars in the first half of 2025 stood at 77%. In April 2026, it was similarly high at 72%. Over the entire year of 2025, Russia imported 396,000 new cars, nearly 60% fewer than in the previous year. The overall car market shrank by 16% to 1.33 million vehicles. Including cars manufactured by Haval, Geely, and others in Russian factories, 685,200 Chinese cars were sold, causing their share of the Russian passenger car market to decline from around 59% to 52%.

The slump in imports in 2025 is due to a drastic increase of up to 85% in the vehicle disposal fee at the beginning of last year. The fee is effectively a tax on imported cars and increases their cost by $7,000 to $20,000, depending on the vehicle class, according to calculations by the Rhodium Group. This also increases pressure on Chinese manufacturers to shift production to Russia, which aligns with the government’s goal of not merely being a consumer of Chinese finished products. In the meantime, car imports from China have recovered. The Chinese industry service Gasgoo reports that for the first quarter of 2026, imports nearly doubled compared to the weak same quarter of the previous year, reaching 187,000 vehicles. Russia is thus once again the world’s largest export market for Chinese automakers, ahead of Brazil (167,000 passenger cars) and the United Kingdom (109,000 passenger cars). This article was prepared for the German-Russian Chamber of Foreign Trade.