Russia: 2 Percent Growth Despite Low Business Sentiment?

Author: Klaus Dormann

“Overall, we expect economic growth of around 1.5 to 2 percent this year.” According to RIA Novosti on July 6, Russian Finance Minister Anton Siluanov made this statement on the sidelines of the BRICS summit in Rio de Janeiro. Until now, the Russian government had assumed that economic growth of 2.5 percent would still be achieved by 2025.

The renowned “Vienna Institute for International Economic Comparisons (wiiw)” also expects the Russian economy to grow by 2 percent. It publishes forecasts four times a year for economic development in 23 countries in Central, Eastern, and Southeastern Europe. In its “Summer Forecast” of July 1, the wiiw maintained its forecast from late April that the Russian economy will grow by 2 percent in 2025. The “Eurasian Development Bank,” based in Almaty, Kazakhstan, also recently forecast 2 percent growth for Russia.

However, recent surveys of Russian companies have signaled a decline in economic activity. There are indications that, following the finance minister, the Russian Central Bank and the International Monetary Fund are also likely to lower their growth forecasts for the Russian economy.

The Central Bank and IMF are also likely to forecast lower growth soon

The Russian Central Bank currently still expects a 1 to 2 percent increase in output for this year. However, according to press reports, it intends to “adjust” its previous growth forecast. Growth will be lower than forecast, announced Deputy Central Bank President Alexey Zabotkin.

The IMF is also expected to lower its growth forecast for Russia.

In any case, “Moskovskij Komsomolets” reports on statements by the director of the IMF’s Communications Department, Julie Kozack, that the growth rate of the Russian economy will most likely decline given the current situation in numerous sectors. Kozack said at a press briefing on July 3 that, following last year’s overheating, a sharp slowdown in growth is currently evident in Russia. In April, the IMF had forecast that growth would slow to 1.5 percent by 2025. However, developments since April suggest that growth could be even lower. Kozack clarified, however, that she did not wish to preempt the update to the “World Economic Outlook” (expected in July).

Regarding the development of the Russian economy, she also noted that the downturn in production reflects the “tight policies” in Russia, by which she likely meant primarily the tight monetary policy. On the one hand, inflation in Russia remains high and unemployment very low. On the other hand, production is slowing rapidly and risks are rising. The central bank’s policy must “balance this out.”

Kozack also pointed to cyclical causes for the slowdown in growth. When a period of overheating comes to an end, a downturn is often observed. This is currently the case in Russia as well. Furthermore, the decline in oil prices is having an impact in Russia. The tightening of sanctions is also having some impact.

Reuters survey still expects 1.5 percent growth

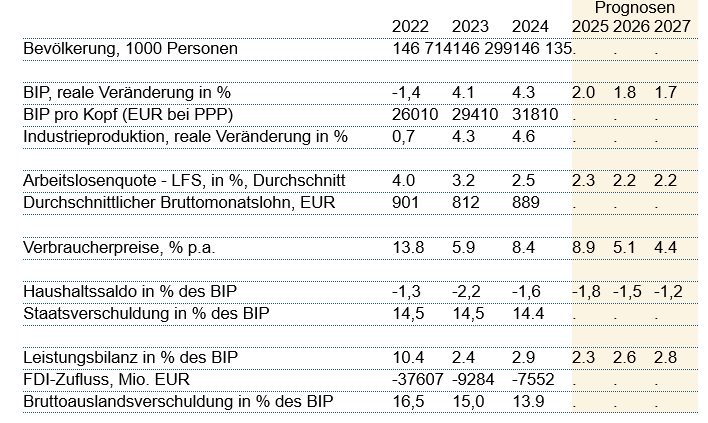

In the monthly analyst survey conducted by the Reuters news agency at the end of June, participants expected, as they did in May, that the Russian economy would grow by an average of only 1.5 percent this year. According to forecasts compiled by “Consensus Economics” from predominantly Western banks and institutions, even slightly weaker growth in the Russian economy is expected. The BOFIT research institute of the Finnish central bank reports that, according to the Consensus survey, Russia’s gross domestic product is expected to rise by 1.4 percent in 2025 and 1.3 percent in 2026. In 2024, Russia’s economy had still grown by 4.3 percent, slightly more than in 2023 (+4.1 percent).

According to Reuters, the ruble was trading at 78.45 per U.S. dollar on July 1 (data from LSEG based on over-the-counter quotes). Since the start of the year, its exchange rate against the dollar has risen by around 45 percent, according to Reuters. This appreciation helped combat inflation in Russia by making imported goods cheaper. On average, however, participants in the Reuters survey still expect the ruble to depreciate significantly over the next twelve months. In twelve months, an exchange rate of 98.25 rubles per U.S. dollar is expected. In the short term, however, the ruble is expected to remain strong.

Regarding monetary policy, survey participants expect, on average, that the Russian Central Bank will likely cut its key interest rate by another percentage point to 19% at its board meeting on July 25. They anticipate that the year-over-year increase in consumer prices will decline from 9.9 percent in May to 7 percent in December 2025.

Vasily Astrov: Monetary policy will very likely be further eased in July

Vasily Astrov, the wiiw’s Russia expert, also expects a rate cut soon. Speaking to Newsweek, he said he was “almost certain” that Central Bank Governor Nabiullina would further ease monetary policy at the next meeting in late July, citing lower inflation, rather than risking economic stagnation and recession.

Regarding the controversial discussion between Economy Minister Reshetnikov, Finance Minister Siluanov, and Central Bank Governor Nabiullina at the St. Petersburg Economic Forum, Vasily Astrov noted that there is still “a great deal of freedom in economic policy debates” in Russia. Since high interest rates would dampen economic activity, Economy Minister Reshetnikov is advocating for an interest rate cut and painting a negative picture of the economic situation (Reshetnikov stated at SPIEF that Russia is “on the brink of a recession”). Central Bank President Nabiullina, on the other hand, downplays the economic risks, as openly acknowledging these risks would amount to self-criticism for her. Her tight monetary policy is the most important factor behind the economic slowdown. That is why she speaks of a “planned cooling” of the overheated economy, according to Astrov.

Business sentiment has deteriorated significantly

In the Reuters survey, some analysts pointed to a significant deterioration in business sentiment across large parts of the Russian economy.

Natalya Orlova, chief economist at Alfa-Bank, drew attention to a serious deterioration in the business climate in consumer-oriented sectors. Combined with the slowdown in consumer price inflation that has already occurred in recent months, this points to a further interest rate cut in July (see also: Natalya Orlova, alfabank.ru: Growth model exhausted: indicators point to economic slowdown, June 26, 2025).

Some survey participants also noted that, according to S&P Global’s Purchasing Managers’ Index, sentiment among companies in the “manufacturing sector” recorded its sharpest decline in more than three years in June.

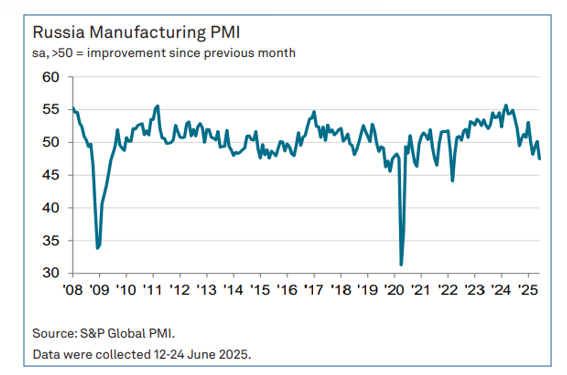

Purchasing Managers’ Index Falls Below “Growth Threshold”

The “Russia Manufacturing Purchasing Managers’ Index” from the global research firm S&P Global fell by 2.7 percentage points to just 47.5 points on a seasonally adjusted basis, based on surveys of Russian companies conducted in mid-June. Falling below the 50-point mark signals a decline in business activity compared to the previous month of May. This was the sharpest decline since March 2022 (the start of the war in Ukraine) and the third decline in the last four months.

The PMI index for the “manufacturing sector” thus recovered only briefly above the “growth threshold” of 50 index points in May. A year ago, in June 2024, the index stood at 54.4 points, nearly at a long-term high. Since then, however, it has trended steadily downward—albeit with significant fluctuations.

Purchasing Managers’ Index for Russia’s Manufacturing Sector

S&P Global: Russia Manufacturing PMI: Contraction in Russian manufacturing output quickens amid renewed drop in new orders in June, 07/01/25

The index for the services sector (“S&P Global Russia Services PMI Business Activity Index”) also fell below the growth threshold in June. It dropped from 52.2 points in May to 49.2 points in June.

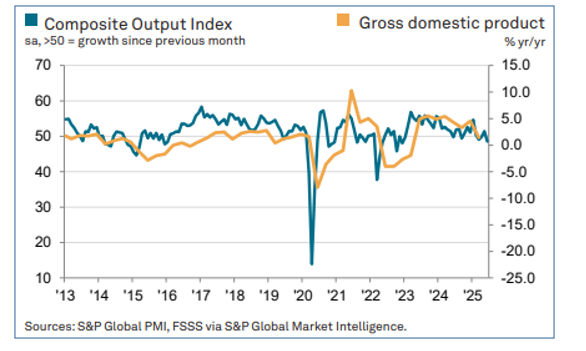

The composite index for the “manufacturing” and services sectors, the “S&P Global Russia Composite PMI Output Index,” fell from 51.4 points in May to 48.5 points in June. According to S&P Global, this signals a decline in business activity. Both the “manufacturing sector” and service providers reported declines in production.

The following figure compares the trend of the “Composite Output Index” with the quarterly trend of real gross domestic product. It is evident that the combined PMI Output Index (blue line) rose by the end of 2024. At the same time, annual growth in real gross domestic product (orange line) also accelerated in the fourth quarter of 2024.

In contrast, the “Composite Output Index” fell sharply during the first quarter of 2025. At the same time, annual growth in real gross domestic product also slowed significantly.

Combined Purchasing Managers’ Index and quarterly change in gross domestic product compared to the previous year in percent

S&P Global Russia Services PMI, Russia Composite PMI, July 4, 2025

Further signs of the economic downturn

Based on the survey results, S&P Global cites the following additional signs of an economic downturn:

Employment continued to decline. Companies reported the sharpest drop in staffing levels since December 2022.

New orders in the private sector declined. While the overall decline was only slight, it was the sharpest since March. However, the order backlog in the private sector rose overall. A faster increase in the order backlog in the services sector outweighed a significant decline in the order backlog in the “manufacturing sector.”

At the same time, inflationary pressure eased in the “manufacturing sector” and in the services sector. Both purchase prices and selling prices rose at their slowest pace since November 2019 and July 2020, respectively.

BOFIT: Alarming Slowdown in Russia’s Growth

The BOFIT research institute of the Bank of Finland also analyzes the current economic slowdown in Russia in its latest weekly report (title: “Concerns emerge over Russia’s slowing growth”)

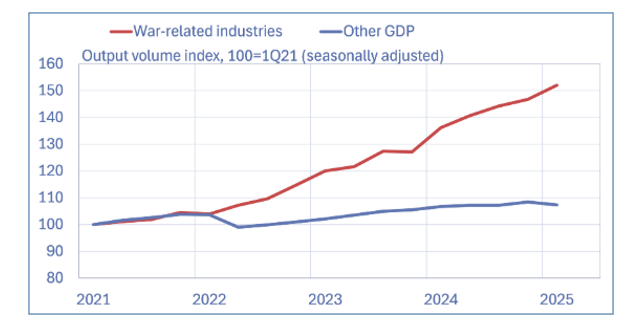

The institute notes that Russia’s annual economic growth slowed to 1.4 percent in the first quarter of 2025. Growth continued to be driven by war-related industries and services. In contrast, for example, production in mining and other raw material extraction shrank significantly from January to March compared to the previous year. Wholesale and retail sales also fell slightly in real terms.

In the first quarter, seasonally adjusted GDP fell by a total of 0.6 percent

Compared to the fourth quarter of 2024, Russia’s GDP fell by 0.6% on a seasonally adjusted basis in the first quarter of 2025, according to BOFIT. This was the first decline since spring 2022 following the invasion of Ukraine, BOFIT noted.

In the following figure, BOFIT shows that, according to its calculations, only production in “war-related industries” continued to rise on a seasonally adjusted basis in the first quarter (red line). Production in the remaining sectors of the economy fell considerably (blue line).

Indices of production in “war-related industries”

and production in the rest of the gross domestic product (first quarter of 2021=100)

Note. The development of war-related industries is an estimate that covers three manufacturing industries most closely related to the war industry, as well as services related to public administration and national defense. Sources: Rosstat, BOFIT.

BOFIT Weekly Review 27/2025: Concerns emerge over Russia’s slowing growth, July 4, 2025

The Russian Federal State Statistics Service (Rosstat) also reports a 0.6 percent decline in seasonally adjusted real gross domestic product in the first quarter of 2025 compared to the previous quarter (see detailed analysis by Marina Voitenco for the online magazine Politcom.ru: Supply and demand – risks of balancing, July 2, 2025)

Growth also fell significantly in a 5-month comparison

Regarding the economic data for May published by Rosstat on Thursday, BOFIT notes:

Growth in aggregate economic output has also slowed significantly when comparing the first five months of 2025 and 2024. The indicator, which reflects output in the five “core sectors” of the economy and is therefore used as a measure of total economic output, grew by 1.4% year-over-year from January to May (see also: Finmarket.ru: Output growth in basic activities in Russia slowed to 0.7% in May – Rosstat, July 2, 2025)

Production in mining and the extraction of other raw materials declined again in May compared to the same period last year, while production in the “manufacturing sector” continued to grow. The construction sector stagnated in May at the previous year’s level.

Retail sales grew moderately in May, as in previous months.

Consumer prices continued to rise by around 10% in May compared to the previous year.

The CMASF warns of a “debt recession”

The Moscow-based “Center for Macroeconomic Analysis and Short-Term Forecasts” (CMASF) continues to see only a low probability of an economic recession and a protracted banking crisis based on its “early warning system for macrofinancial risks.” However, in an analysis published on July 4, the center notes that leading indicators for a recession and a banking crisis have risen steadily in recent months. If their future development is extrapolated, they would most likely signal both an economic recession and a protracted banking crisis in the coming months. According to the CMASF, this deterioration in the outlook for the Russian economy is attributable to a prolongation of the phase of extremely high interest rates coupled with low overall economic growth rates.

The CMASF argues as follows: During the credit boom in 2024, companies took out loans at higher interest rates because they expected to continue achieving high production growth rates and high profits in the future. The current general slowdown in production growth amid persistently high interest rates means that the balance between rising interest payments and rising borrower incomes has been disrupted. In such a situation, the erosion of borrowers’ financial capacity is merely “a matter of time.” Once that resilience is exhausted, a “debt recession” could ensue. In this scenario, the deterioration of borrowers’ financial stability and the decline in production would be mutually reinforcing.

According to the CMASF, a “debt recession” could be avoided by “strong positive macroeconomic shocks.” However, the CMASF does not yet see any corresponding economic policy measures or improvements in the framework conditions for the Russian economy.

Russia’s economic growth has slowed significantly so far in 2025

In the first five months of 2025, real gross domestic product was 1.5 percent higher than in the same period of the previous year, according to preliminary calculations by the Ministry of Economy. In May, however, it was only 1.2 percent higher than a year ago. In April, it had still risen by 1.9 percent year-over-year.

According to the wiiw press release (English, German), Vasily Astrov, the Vienna Institute’s Russia expert, believes that the Russian Central Bank’s “monetary policy emergency brake” is primarily responsible for the slump in growth in Russia.

Over the course of 2024, the central bank had raised its key interest rate to 21 percent. In early June, the key interest rate was lowered by one percentage point as a first step. At 20 percent, however, the wiiw considers it still exorbitant: “High interest rates are stifling the economy because they make loans unaffordable and also create a strong incentive to hoard money in bank accounts,” Astrov argues, according to the press release. He warns that a “wave of bankruptcies” is looming. In some cases, it could also affect large corporations and “key enterprises.”

In the “Country Overview Russia,” the wiiw comments on the central bank’s monetary policy, noting that the policy of double-digit real interest rates—motivated by the “supposed necessity” of bringing inflation closer to the 4 percent target— has likely significantly exacerbated the slowdown in the Russian economy that was already expected.

With an easing of monetary policy, the economy will grow by 2.0 percent in 2025

In its “Country Overview Russia,” the wiiw notes that growth in the Russian economy has slowed significantly after two years of a boom. It points out that the annual growth rate of the overall economy reached only 1.6 percent in the first four months of 2025, with industrial production rising by 1.2 percent. Even this result was due exclusively to defense production. However, a slowdown in growth was to be expected given the phasing out of “war-related fiscal stimulus” and import substitution driven by sanctions.

In its “base scenario,” however, the Vienna Institute maintains its forecast of 2 percent GDP growth for 2025. It assumes that the reduction of the key interest rate to 20 percent will likely be followed by further cuts. At the same time, the wiiw warns: “However, should monetary easing be delayed or proceed too slowly, growth this year could well be closer to 1–1.5%.”

The wiiw notes that overall credit growth in Russia has effectively stalled. Growth in private lending has even turned negative, which is hampering demand for durable consumer goods and housing. With the cooling of demand, inflation had fallen to around 6% on an annualized basis by April.

The institute expects that monetary easing, in addition to supporting lending activity, is likely to exert “much-needed depreciation pressure” on the ruble. The ruble has appreciated by around 20 percent against the U.S. dollar since the start of the year. Combined with falling oil prices, this is weighing on Russia’s government revenues.

Wiiw Country Overview – Key Economic Indicators

The wiiw is lowering its growth forecast for 2026 from +2.5% to +1.8%

At the end of April, the wiiw had still expected the Russian economy to pick up again next year and grow to 2.5 percent. In the spring, according to the wiiw’s assessment, it had still appeared as though U.S. sanctions might soon be eased or lifted in light of a convergence in the positions of Presidents Trump and Putin regarding the war in Ukraine.

However, according to the wiiw’s press release, this hope has “vanished into thin air for the time being.” In its “Country Overview Russia,” the wiiw now states that it is increasingly unlikely that the easing of Russia’s relations with the U.S.—and the associated prospect of sanctions being eased—will go beyond the current stage. Astrov explains: “This is another key reason why Russia is likely to grow more slowly in 2026 than was assumed just a short time ago.” For 2026, the wiiw now expects economic growth to slow further to 1.8 percent.

This forecast is almost in line with that of the Eurasian Development Bank, which expects Russia’s growth to decline from +2.0 percent to +1.7 percent in 2026.

Russia’s budget deficit will rise to 1.8 percent of GDP in 2025

As another reason for the slowdown in Russia’s economic growth, the wiiw points out that Russia’s oil revenues have fallen due to lower prices. Furthermore, the substitution of imports from the West with domestic products is increasingly reaching its limits.

However, Vasily Astrov does not consider the decline in energy and tax revenues to be “threatening” for Russia’s fiscal outlook. The Russian government still has sufficient financial leeway, he notes. It still has fiscal reserves and the ability to borrow from domestic banks. According to the wiiw forecast, however, Russia’s budget deficit in 2025 will not be limited to 0.5 percent of GDP as planned by the government, but will rise to 1.8 percent of GDP.

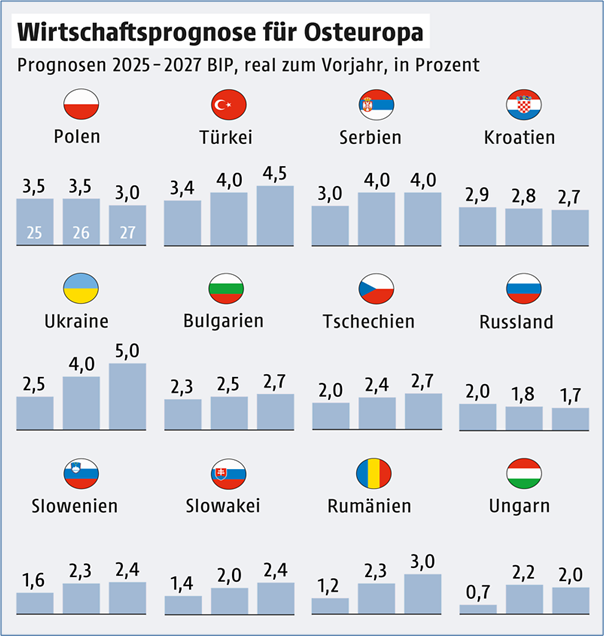

In a comparison of Eastern European countries, Russia will fall to the bottom of the growth scale in 2026

Even if the wiiw’s comparatively high growth forecast for the Russian economy this year (+2.0 percent) is confirmed, Russia is already growing significantly more slowly this year than Poland (+3.5 percent), Turkey (+3.4 percent), Serbia (+3.0 percent), and Croatia (+2.9 percent).

Next year, the wiiw even sees Russia at the bottom of the growth rankings: even with a real GDP increase of +1.8 percent, Russia will grow more slowly than all other countries in Central, Eastern, and Southeastern Europe included in the figure above.

According to the wiiw, the main drivers of the economy in Central and Eastern Europe are private consumption and strong real wage increases. In Poland, the region’s largest market, the wiiw expects economic growth of 3.5 percent this year and next.

For Turkey, wiiw expects GDP growth of 3.4 percent in 2025 and 4 percent in 2026.

Recommended reading:

- fr.de; Stefan Scholl: Debt Crisis in Russia, July 5, 2025

- Südtirol News: Economy Becoming Increasingly Fragile. Russian Economic Experts Warn – and Disagree with Putin, July 3, 2025

- FOCUS-online, dpa: Kremlin under pressure. Putin paints a rosy picture of Russia’s economy – ally sees a “perfect storm” brewing, July 2, 2025

- Newsweek; Brendan Cole: Russia’s Officials Keep Contradicting Putin on War Economy, July 1, 2025

- Radio Free Europe Radio Liberty; Mike Eckel: Russia’s War Economy Is Heading Toward Recession. It Probably Won’t Slow Down the War, July 1, 2025

- Finam.ru; Dmitry Polevoy, Investment Director of JSC Astra Asset Management: Is Russia’s economy in a state of controlled cooling or recession? July 1, 2025

- The Spectator, Mark Galeotti: Will Putin really rein in Russia’s defense spending? June 30, 2025

- realnoevremya.com; Yulia Garaeva: ‘Winter’ in the economy: recession, risks of ruble devaluation, and a new round of inflation; June 30, 2025

- Interfax.com: Russia’s economy is on track for a soft landing – Central Bank Deputy Governor Zabotkin, June 30, 2025

- MSN.com. Bohdan Babaiev: Putin says Russia will cut military spending as economy is ‘on the brink of going into a recession,’ June 28, 2025

- Forbes.ru; Natalia Orlova: Russian Economy: Crisis Braking or Premature Panic, June 27, 2025