“Positive Outlook for Russia Thanks to Trump”

Author: Klaus Dormann

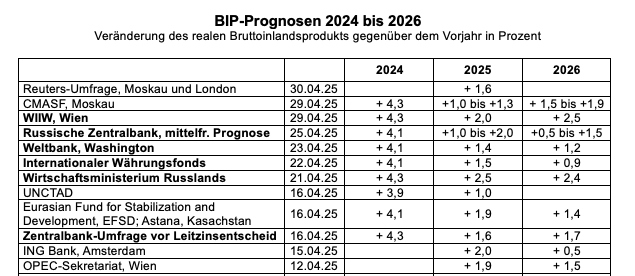

This is the optimistic headline used by the “Vienna Institute for International Economic Studies” (wiiw) for the “Russia chapter” in its press release on its spring forecast for economic developments in the countries of Central, Eastern, and Southeastern Europe (MOSOEL). Particularly surprising in comparison with the Russia forecasts of the IMF, the World Bank, and leading economic research institutes is the wiiw’s assessment of Russia’s economic outlook for next year. According to the Vienna-based institute, Russia’s economic growth will not weaken further in 2026 but will instead accelerate back to 2.5 percent. To justify its growth optimism starting in 2026, the wiiw points primarily to “the prospect of a partial or complete lifting of U.S. sanctions” against Russia in the wake of “rapprochement with the U.S.”

The wiiw also expects only 2 percent growth in Russia in 2025

The Vienna Institute’s forecast for this year’s growth in the Russian economy is not unusually positive compared to other forecasts. Like almost all observers, the wiiw also expects the “overheated” growth of the Russian economy to cool significantly in 2025. After the rise in aggregate economic output accelerated to 4.3 percent last year, the wiiw expects growth to halve to just 2.0 percent this year.

Russia’s GDP growth is expected to pick up again as early as 2026

However, the wiiw takes an unusually positive view of the Russian economy’s outlook starting next year. While the BOFIT research institute of the Finnish Central Bank and the “Joint Forecast” of leading German economic research institutes expect Russian economic growth to halve again in 2026 to just +1.0 percent, the wiiw now assumes that Russia’s economic growth will pick up to 2.5 percent as early as next year.

With this, the wiiw is raising its forecast for 2026, published in early February, by 0.9 percentage points. Its new growth forecast of 2.5 percent for 2026 is now even slightly higher than the forecast by the Russian Ministry of Economic Development (+2.4 percent in the “base scenario”).

The Munich-based ifo Institute expects a completely different economic trajectory in Russia next year than the Vienna-based wiiw. In its “Spring Forecast” published in mid-March in the ifo Express, it does expect Russia’s economy to grow at a similar rate in 2025 (+1.9 percent) as the wiiw forecasts (+2.0 percent). However, in 2026, Russia’s total economic output is projected to decline significantly (-0.8 percent). This illustrates how differently even renowned research institutes assess the economic outlook in Russia. The primary reason for this is likely the high level of uncertainty surrounding the course of the war in Ukraine and the policies of U.S. President Trump.

“Russia’s economic isolation by the U.S.” could end

In its forecast, the wiiw apparently assumes a significant improvement in the geopolitical conditions for the Russian economy. In any case, according to the press release, wiiw’s Russia expert, Vasily Astrov, points out that existing U.S. sanctions against Russia are already being implemented “only half-heartedly” today. “Should a ceasefire or peace agreement actually be reached in Ukraine, the economic isolation of Russia by the US would likely come to an end. Possibly even without an agreement. This would allow US capital and American technology to flow back into the country. US allies Japan, South Korea, and Taiwan could also follow this example,” says Vasily Astrov.

The press release also notes that “in the wake of Trump’s change of course in Ukraine,” discussions regarding “future economic cooperation between the U.S. and Russia, such as oil production projects in the Arctic,” have been taking place from the very beginning. Foreign companies such as Renault, Hyundai, and Samsung are now considering a return to Russia. The South Korean electronics conglomerate LG has even recently ramped up production at its Moscow plant again.

Regarding the argument that Russia’s economy could suffer if the war ends due to the loss of growth-boosting government spending, Astrov states in the wiiw press release: “The partial resumption of economic relations with the West following an end to the war would likely offset the loss of high salaries for soldiers and compensation for their families, which have so far helped sustain Russian growth.”

“Country Overview Russia” by the wiiw

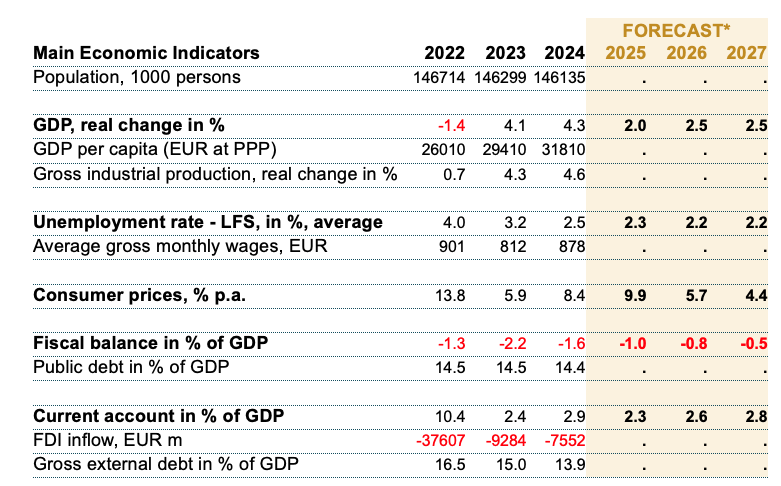

In its updated “Country Overview: Russia” on its website, the wiiw also highlights that its growth forecasts for the Russian economy in 2025 and 2026 have improved compared to its winter forecast. This is “attributable to the solid performance to date and the expected easing of U.S. sanctions.”

After two years of overheating, the economy is likely to cool significantly in 2025, according to the wiiw. This is primarily due to the “very restrictive monetary policy.”

However, the wiiw estimates that the inflation rate in Russia will peak at 9.9 percent year-over-year in 2025 compared to 2024. Starting in mid-2025, “a gradual easing of monetary policy” should be possible.

Country Overview: Russia—Key Economic Indicators

WIIW: Country Overview Russia, April 2025

In an interview with Deutsche Welle, Vasily Astrov raises many questions

A few days before the release of the wiiw’s “Spring Forecast,” Vasily Astrov also commented in detail on economic developments in Russia during a podcast interview with Deutsche Welle that lasted a good half-hour. In conversation with editor Thomas Kohlmann, he revealed that the WIIW expects growth in Russia to slow to perhaps around 2 percent in 2025, but did not provide a forecast figure for 2026. He emphasized several times that we do not know whether there will actually be increased cooperation between Russia and the U.S. While the wiiw’s “Country Overview” cites “the expected easing of U.S. sanctions” as the rationale for the upward revision of growth forecasts for Russia, Astrov emphasized in the Deutsche Welle interview that it is not certain whether U.S. sanctions will actually be lifted.

Among other things, he commented on the following questions during the interview as summarized below.

Why has Russia been able to increase its arms production so significantly?

The high level of arms production is possible, on the one hand, because the Russian state continues to have relatively high revenues. By international standards, Russia has a very low level of public debt, at around 15 percent of GDP. On the other hand, Russia is also able to import all the “critical inputs” required for arms production, such as semiconductor chips.

How has U.S. policy toward Russia changed?

Under President Trump, there was a “massive departure” from the policies of U.S. administrations toward Russia in recent decades, and not just in rhetoric. The Trump administration also took “concrete steps” to change its policy toward Russia; for example, monitoring of third-party compliance with so-called “secondary sanctions” against Russia was significantly relaxed.

How will Russia’s economic cooperation with the U.S. and Europe develop?

Future economic cooperation with the US and Europe naturally depends primarily on how the geopolitical conflict unfolds. Whether there will actually be increased cooperation with the US or Europe cannot be said at this time. There are many uncertainties. First, we do not know whether the U.S. sanctions will actually be lifted. We do not know whether there will truly be increased cooperation between Russia and the U.S. We do not know that for certain yet.

And secondly: Even if the U.S. sanctions are lifted, we don’t know whether, for example, European countries will follow the new course of U.S. policy toward Russia. For instance, I have relatively strong doubts that the European Union will follow the U.S. example. Certainly not immediately. That means it will likely take some time before economic ties between Russia and Europe are strengthened again. In the long term, I do believe that will happen. It could take 10 years; it could take even longer. I don’t know.

How can the sharp appreciation of the ruble be explained?

Geopolitical factors were decisive for the ruble’s appreciation. There was renewed confidence in the Russian economy due to the prospects of increased cooperation between Russia and the U.S. Even if this optimism was probably somewhat exaggerated. We don’t really know whether there will be increased cooperation with the U.S.

What challenges does a return from a “war economy” to a “peace economy” pose for Russia?

I believe there are two factors at play: On the one hand, I don’t think there will be a massive shock once the war is over. A great deal of military stockpiles were depleted during the war. Many military experts say it will take years to replenish those stockpiles, including tanks. Weapons manufacturers will likely be supplied with substantial orders for several more years.

On the other hand: Where there will likely actually be a massive decline in government spending is in payments to mercenaries, because there probably won’t be a need for as many mercenaries anymore. A certain number of mercenaries will still be needed along the “contact lines” in Ukraine. However, salary payments to mercenaries, as well as compensation for soldiers wounded in the war and the families of those killed in action, will drop dramatically.

Ibelieve there will initially be a significant “negative shock” to household incomes and also to private household consumption. Whether this shock could plunge the Russian economy into a recession depends primarily on whether the state finds other priorities for its spending. Instead of spending money on the war, for example, it could spend more on improving the economic structure. There are many areas that have been severely underfunded in recent decades.

Will it be difficult for Russia if the oil price remains below $60 per barrel?

$60 per barrel isn’t that bad yet. If the price of Russian oil heads toward $40, things will get difficult. Revenues from the energy sector account for one-third of the federal budget. Not only do oil prices play a major role here, but so does the exchange rate. The combination of low oil prices and a strong ruble is the worst possible scenario for the Russian budget. And right now, the ruble is very strong. That is an additional factor putting pressure on government revenue from the energy sector. However, an oil price of $60 per barrel is still acceptable for Russia, although budget deficits could rise slightly compared to the original plans.

Regarding the latest revision of the budget plan, Ostwirtschaft.de reported on May 3:

“The Russian Ministry of Finance expects the national budget deficit for the current year to be three times higher than previously assumed. Instead of 1.17 trillion rubles (12.6 billion euros), the budget shortfall will amount to 3.79 trillion rubles (41 billion euros), according to the new forecast.

Measured against gross domestic product (GDP), the deficit forecast rises from 0.5% to 1.7% of GDP. The reason for this is the lower expectation for oil and gas revenues due to falling oil prices.

The ministry expects an average price of $56 per barrel for the Russian Urals crude for the full year. The original draft projected $69.7.”

Quellen und Lesetipps:- wiiw Spring Forecast: Trump’s tariffs likely to have limited impact on Eastern Europe; Press Releases: English, German; April 29, 2025; wiiw in the press; country overview: Russia

Vasily Astrov (WIIW), in a Deutsche Welle podcast interview with Thomas Kohlmann:

How Russia’s Economy Is Really Doing, 37 min., 04/25/25

news ORF.at: Wiiw: Central and Eastern Europe Still on Track for Growth, with video, 04/25/25

Inosmi.ru; Die Presse, Aloysius Widmann: Trump Stimulates Russian Economic Growth. Die Presse: Experts predict growth of the Russian economy by 2026, April 29, 2025

bneIntellinews, Clare Nuttall: Trump policies won’t harm Emerging Europe badly – and will actively benefit Russia, April 29, 2025 - WIIW Forecast Report: Assessing the impact of Trump’s tariffs on the region;

Richard Grieveson: Executive Summary

; Marcus How and Benedetta Locatelli: Political risk: Endgame scenarios for the Ukraine war and their impact on CESEE, April 29, 2025 - axinocapital Video: US-Ukraine Commodities Deal: All Just for Show?! – What’s Really Behind It!, 19 min., May 2, 2025

- Welt-Nachrichten Video; Interview with US Correspondent Stefanie Bolzen: Commodities Deal: Putin Under Pressure! “A Commitment from the US – and a Sort of Substitute for Security Guarantees,” May 1, 2025

- ARTEde video: “Mit offenen Karten”: Russia’s Economy: Robust or Weak? May 3, 2025