Klepatsch: Russia's growth is slowing down, but will reach 1.5 percent in 2025

Author: Klaus Dormann

There is still speculation as to whether, following a strong growth spurt at the end of 2024, output in the Russian economy declined not only in the first quarter but also in the second quarter of 2025 compared to the previous quarter. If so, Russia would have entered a “technical” recession. Initial estimates on this are expected to be released in early August, once the Federal State Statistics Service (Rosstat) has published the economic data for the month of June.

Information on the “month-to-month” development of Russia’s real gross domestic product is provided by monthly estimates from the research institute of the state-owned Bank for Foreign Economic Affairs, Vnesheconombank (VEB). However, the VEB Institute has not yet published an estimate for the seasonally and calendar-adjusted trend in May.

Andrey Klepach, the 66-year-old chief economist at Vnesheconombank, has commented on the current economic situation in Russia in several interviews. He also addressed the effectiveness of Western sanctions, pointing out the risks of Russia’s growing dependence on China. Journalist Andrey Gurkov now views Russia as “China’s dependent junior partner.”

Klepatsch’s forecast: The economy will grow by around 1.5 percent in 2025

In a Le Monde interview published in early July, former Deputy Minister of Economic Development Klepach, when asked whether the Russian economy had entered a recession, said he would rather describe the situation as stagnation or a pause in growth. Gross domestic product fell by about 0.5 percent in the first quarter of 2025 compared to the fourth quarter of 2024 (see VEB Institute: GDP Index April 25). Compared to the first quarter of 2024, it had risen by 1.4 percent.

Regarding further developments in the second quarter of 2025, Klepatsch said that, according to initial calculations by the VEB Institute, there was likely neither an increase nor a decrease in aggregate economic output in the second quarter compared to the first quarter. In May and June, the decline in production compared to April was insignificant. Russia is not in a recession.

Regarding the development of demand, Klepatsch noted that while the year-over-year increase in consumption had certainly slowed, consumption continues to grow. Investments rose by about 5 percent in the first quarter—more than expected. This trend was evident not only in public but also in private projects. That was a good sign.

“In theory,” Klepatsch said, Russia’s economy will begin to grow again in the third quarter or in the second half of the year. This will depend mainly on developments in agriculture and the defense sector.

In May 2025, real gross domestic product grew by 1.2 percent compared to the same month last year, according to the Ministry of Economic Development. In the first five months of the year, it was 1.5 percent higher than in the same period of the previous year, according to the ministry (Interfax.com, Kommersant.ru).

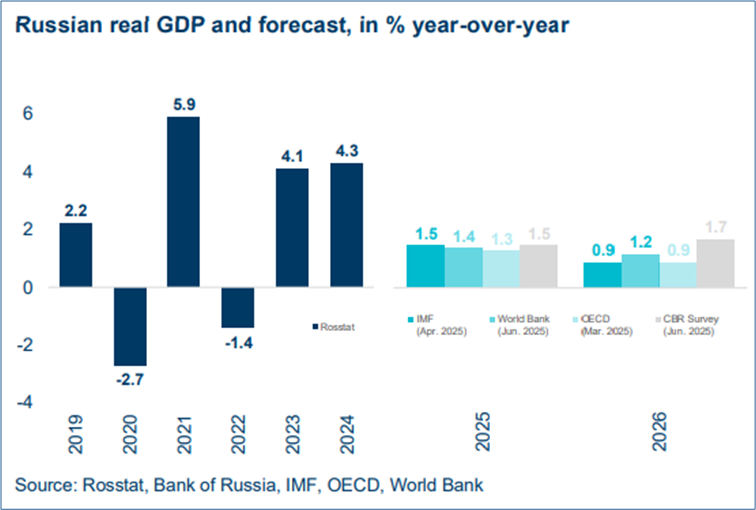

Andrey Klepach also expects the Russian economy to grow by 1.5 percent for the full year 2025. This forecast largely aligns with the expectations of international economic organizations and the “consensus” among Russian analysts. This is illustrated by the following chart from the “Russia Chartbook” of the Kyiv School of Economics, which includes forecasts from the IMF, the World Bank, and the OECD, as well as the average of forecasts from the Russian Central Bank’s analyst survey.

Russia’s real gross domestic product,

year-over-year changes in percent

However, according to Le Monde, Klepatsch expects growth to rise to “over 2.3 to 2.5 percent” in 2026. International economic organizations, on the other hand, anticipate a further slowdown in Russian economic growth next year. Their forecasts for 2026 are now only around 1 percent.

The median growth forecast for 2026 in the Central Bank’s analyst survey published in early June was also notably lower than Klepatsch’s forecast, at +1.7 percent. The results of a new Central Bank survey will be published on July 16 (survey calendar).

The defense sector is a growth driver for Russia

In the Le Monde interview, also cited by Inosmi.ru, Klepatsch confirmed that the defense sector is a key driver of growth for the Russian economy. Together with the energy sector, this sector now forms “the core” of the Russian economy. Spending on defense and national security now accounts for more than 8% of gross domestic product. This level of spending is roughly equivalent to that of the U.S. during the Korean War. The defense sector is currently growing by “more than 10%” per year.

High interest rates and the strong ruble are causing problems

Regarding the development of the “civilian sectors” of the Russian economy, Klepatsch noted that they are also growing, but at a significantly slower pace. Their development depends largely on monetary policy. By 2026, these sectors could once again become the economy’s most important driving forces.

Klepatsch pointed out that companies are currently finding it difficult to secure financing for investments and growth due to very high interest rates. However, the share of loans granted by banks with interest rates above 20% is low. More than 70% of investments come from companies’ own funds, and more than 20% from government funds.

The ruble’s current strength is also a problem for companies, as it further reduces export revenues. Klepatsch believes that while it would be beneficial for the Russian economy if the exchange rate returned to 100 rubles per U.S. dollar, this is unlikely in 2025. A rate of 85 rubles per U.S. dollar by year-end is more likely (TASS).

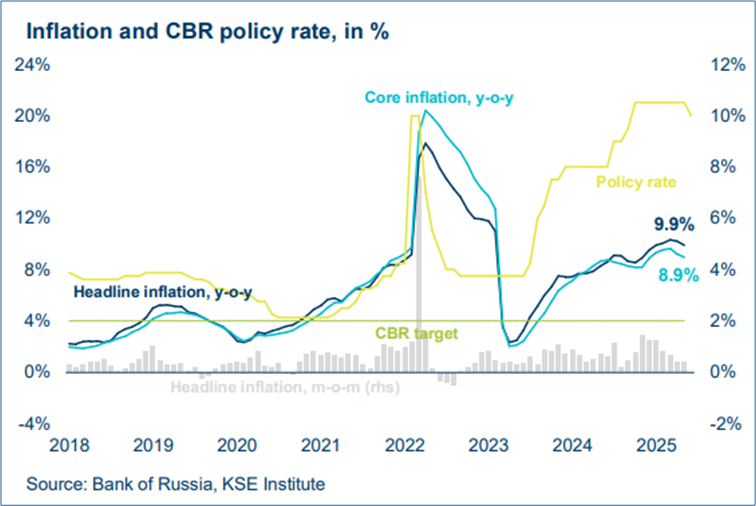

Klepatsch: Inflation rate to drop to 6 to 7 percent by the end of 2025

The chief economist at Vnesheconombank expects inflationary pressures to ease as 2025 progresses. On July 9, on the sidelines of the Innoprom exhibition in Yekaterinburg, he predicted that the annual rise in consumer prices would likely fall to 6 to 7 percent by the end of 2025 (TASS). The key interest rate could be lowered from 20 percent to 15 percent by the end of the year (nakanune.ru).

The following chart from the “Kyiv School of Economics” shows the Russian Central Bank’s reduction of the “policy rate” to 20 percent on June 6. However, “headline inflation,” the annual increase in consumer prices, fell only slightly to 9.9 percent in May. “Core inflation” stood at 8.9 percent (TradingEconomics chart). The inflation rate of 4 percent targeted by the Russian Central Bank (“CBR target”) is still being significantly exceeded.

At the same time, however, the gray bars in the figure show that the month-over-month increase in the consumer price index has slowed significantly since the beginning of 2025.

Inflation and the Russian Central Bank’s Key Interest Rate

Kyiv School of Economics: Russia Chartbook, July 3, 2025

In June, the annual inflation rate fell further to 9.4 percent. The month-over-month increase in consumer prices halved in June to just 0.2 percent (TradingEconomics chart, Finmarket.ru).

The consensus forecast of analysts surveyed by Interfax in early July for the inflation rate at the end of 2025 fell to 6.8%. By the end of 2026, analysts expect the inflation rate to decline further to 4.9% on average.

Further key rate cut likely on July 25

RBC.ru reports on the current trend in consumer prices for the week of July 1–7: According to the Ministry of Economic Development, year-over-year inflation rose from 9.39% to 9.45%. Since the beginning of the year, the consumer price index has risen by 4.58%.

Many experts surveyed by RBC Investments expect the Central Bank to cut the key interest rate by 200 basis points to 18% on July 25. However, some anticipate a smaller cut.

Central Bank officials have repeatedly raised the possibility of a further cut in the key interest rate since late June. According to RBC.ru, Deputy Central Bank President Alexei Zabotkin commented on June 30 regarding a cut of more than 100 basis points:

“The decision at the July meeting will depend on how confident we are that inflation is on a path that ensures a return to 4% in 2026. If the data available by then on the economy, the labor market, lending activity, inflation itself, and inflation expectations indicate that a slowdown in inflation to 4% is compatible with a larger cut, then this option will also be considered.”

Natalia Vaschelyuk, Senior Analyst at Pervaya Management Company, considers a key interest rate cut to 18 percent likely. At the same time, she points out, among other things, the sharp increase in federal budget spending to date and the continuing tight labor market conditions. These “inflation risks” could limit the scope for a key interest rate cut.

Federal budget spending rose by about 20% in the first half of the year compared to the previous year (Finam.ru). To meet the annual spending plan (42.3 trillion rubles), spending in the July–December 2025 period must be 1.5 trillion rubles lower than in the second half of 2024. According to the analyst, this is a “fairly ambitious goal.”

The unemployment rate reached a new historic low of 2.2% in May (TradingEconomics chart). The slowdown in nominal wage growth in April to 15.3% year-over-year cannot yet be considered sufficient, according to the analyst. In real terms, wages in April were 4.6 percent higher than a year ago (TradingEconomics chart).

The federal budget deficit will be much higher than planned in 2025

An analysis in the U.S. edition of the Spanish newspaper “El País” also addresses the unexpectedly unfavorable development of the federal budget. The authors see Russia “on the brink of economic collapse after 40 months of war.” Regarding the federal budget’s trajectory, they state:

“The government had hoped to end 2025 with a public deficit of just 0.5 percent, the lowest since 2021, when the war had only just begun and high fossil fuel prices were filling the state coffers. But the extremely costly fighting in Ukraine continues, and the lower house has just revised its deficit forecast to more than triple that figure: it now expects a deficit of 1.7 percent, the same as in 2024.”

At the same time, the authors point out that Russia’s “sovereign wealth fund” now holds less than four trillion rubles in liquid reserves. The projected deficit for 2025 is said to be just as high.

The sanctions problem cannot be solved by imports from China alone

Regarding the effectiveness of Western sanctions, Andrey Klepach says in an interview with Le Monde that while the sanctions pose very serious technological and financial obstacles for the Russian economy—because the Russian economy remains heavily dependent on imports— However, over the past three years, many Russian companies have been able to find alternatives to supplies from the West by establishing their own domestic production or sourcing imports from other countries, primarily China. “The Russian economy knows how to adapt,” Klepach said.

At the same time, Klepach pointed out the risks of Russia’s increased dependence on China. The Chinese government is primarily concerned with its country’s economic interests. Trade with the U.S. and Europe is more important to them than trade with Russia. Furthermore, out of fear of the “side effects” of the sanctions imposed on Russia by the U.S. and the EU, Chinese banks have been forced to partially suspend the processing of payments. Klepach argues that Russia must find alternatives to China. There is a risk that China could halt its supplies to Russia for various reasons, just as the Europeans had done previously.

In an interview with RIA Novosti, Klepach said that for the Russian economy today, it is above all important to expand domestic production, particularly in sectors that will determine the future and international competitiveness. “We are only at the very beginning of import substitution,” he said (1Prime.ru).

Andrey Gurkov: Russia has become a “dependent junior partner of China”

Journalist Andrey Gurkov, author of the book “For Russia, Europe Is the Enemy,” recently summarized his analysis of Russia’s dependence on China in a ZDF interview (“Global PolitiX”) as follows:

Since the start of the war in Ukraine, Russia has become a dependent junior partner of China with astonishing speed. This is because, the moment Europeans firmly sided with Ukraine, Putin destroyed the decades-long “business model” between Russia and Europe in a matter of months, if not weeks. The business model consisted of most Russian exports (primarily energy, but also metals, timber, and fertilizers) going to Europe. Europe was by far the most important market for Russia. The war has destroyed this model.

China dictates prices and has no interest in investing in Russia

Now, according to Gurkov, Putin is inevitably forced to export to China and must import from China, for example machinery that used to come from Germany or other EU countries. This machinery can no longer be imported from Europe because most of it—which can also be used for military purposes—is subject to sanctions.

So Putin is not only buying consumer goods in China that were often purchased in Europe or the U.S. in the past; he is also buying machinery there. In doing so, he is dependent on how “generous” China is when purchasing Russian oil, gas, or coal. China is very focused on its own interests. It is clear that if Russia has no other major markets besides China, then the Chinese will dictate the prices.

This is a process that is greatly accelerating Russia’s economic decline and, at the same time, its dependence on China. In Russia, people see this process and are very disappointed that the Chinese are not investing in Russia. In Russia, people had thought that the Chinese, like the Europeans—such as Volkswagen, for example—would come to Russia with their investments and build car factories. But the Chinese have absolutely no interest in setting up any production facilities in Russia. They have more than enough of every kind of goods themselves. They are facing growing difficulties in selling these goods in the U.S. and also in Europe. Of course, Russia is not an exceptionally large market, but it is still a significant one for the sale of products manufactured in China. That is why China does not want to support production in Russia.

Recommended reading:

- Kommersant, Artem Chugunov: Investing is becoming increasingly difficult. The Institute of Economic Forecasting (IEF) of the RAS conducted another survey of enterprises, July 11, 2025

- National Security Journal, Jack Buckby: Dollars and Sense. Russia’s Economy Is in Deep Trouble, July 10, 2025

- nakanune.ru: Andrey Klepach believes that the economy is still close to recession, July 9, 2025

- Eurasian Times; Shubhangi Palve: Russia’s $300B War Expenditure Pulls Country Into Recession; Is Moscow’s Economy Dancing on Dynamite? 07/09/25

- Andrey Gurkov in a ZDF interview on “Global PolitiX” regarding the development of the Russian economy, the impact of sanctions, and Russia’s dependence on China. Russia’s Economic Crisis: Will the Recession End the War in Ukraine? YouTube video, July 9, 2025

- ZDF’s “Global PolitiX”; Felix Klauser: How Russia Is Leading the West by the Nose, July 8, 2025

- D.R. Belousov, Center for Macroeconomic Analysis and Short-Term Forecasting, in an RBC Channel interview: “Tamantsev. As a result,” “Is the Russian economy facing a recession?”; July 8, 2025

- Junge Welt; Reinhard Lauterbach: Economic Slump in Russia. The Price of War. The state-capitalist boom of military Keynesianism in Russia is apparently over, July 8, 2025

- El País, Javier G. Cuesta, Ignacio Fariza: Russia on the edge of economic collapse after 40 months of war. The Russian economic engine is showing clear signs of exhaustion—a reality the Kremlin is beginning to acknowledge. The military-driven boom of 2023 and 2024 is now in the past, July 7, 2025

- Eurasia Daily Monitor, Vadim Shtepa: Lack of Substantive Peace Talks Continues Russian Economic Downturn, July 7, 2025

- DW.com.ru, Oleg Loginov: Russia’s Oil Revenues Are Dwindling. What’s Next? 07/07/25

- Vedomosti: Siluanov predicted Russia’s GDP growth by the end of the year at 1.5–2%, July 6, 2025

- fr.de; Stefan Scholl: Debt Crisis in Russia, July 5, 2025

- russland.capital: Russian Central Bank Financial Congress: Nabiullina, Gref, and Kostin on shifts in the Russian economy, July 4, 2025

- Andrey Klepach in: Le Monde interview; Benjamin Quenelle: Inosmi.ru: “Today the core of our economy is defense and national security.” Russia will grow by the third quarter of 2025, July 3

- Kommersant, Artem Chugunov: The Economy of Cooling Growth, July 3, 2025

- Forbes.ru: Oleg Buklemishev, director of the Center for Economic Policy Research, Moscow State University: Recession in the minds: what is really happening with the Russian economy, July 3, 2025