Is weak economic growth forcing Russia to make peace?

Author: Klaus Dormann

In 2023 and 2024, Russia’s high defense spending caused the country’s gross domestic product to rise by 4.1 percent and 4.3 percent, respectively. In 2025, military spending was increased further. However, overall economic output did not rise by 2.5 percent as originally planned by the government. Since late September, the government has been projecting only a 1.0 percent increase in gross domestic product. Many analysts, however, expect that growth was likely even lower and may have fallen to around 0.5 percent.

Few believe a strong economic recovery is likely in the near future. Most observers expect that growth in the Russian economy in 2026 and in the coming years will be as weak as it was in 2025. This is another reason why, after nearly four years of war with Ukraine, the question is being raised more and more frequently: how much longer can Russia continue the war against Ukraine?

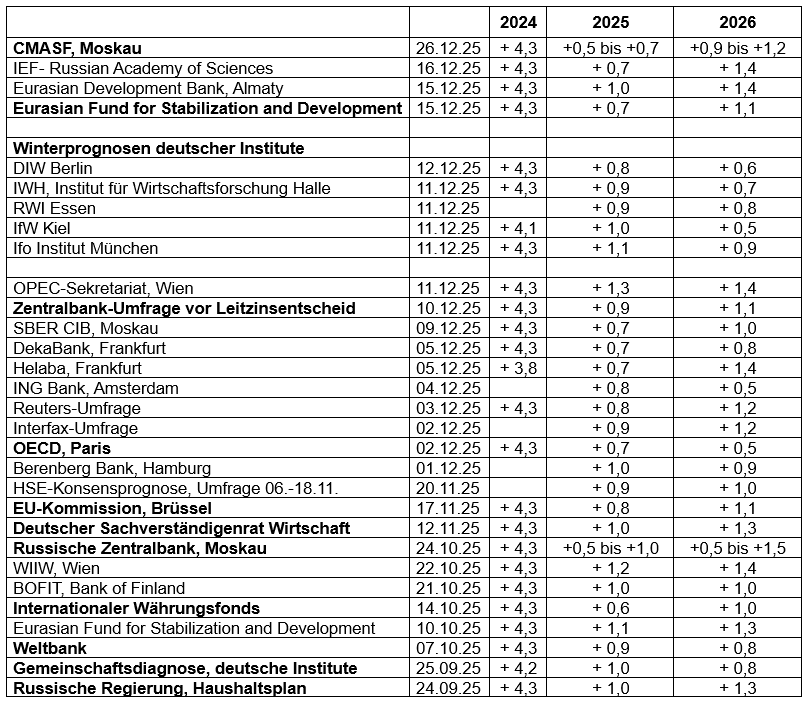

CMASF: Growth Could Have Dropped to 0.5 Percent by 2025

Based on developments in the fall months, the Moscow-based “Center for Macroeconomic Analysis and Short-Term Forecasting” (CMASF) has now further lowered its forecast for Russian economic growth in 2025 to just +0.5 to +0.7 percent. At the same time, it slightly raised its forecast for 2026 to +0.9 to +1.2 percent. With these forecasts, it remains within the Central Bank’s forecast ranges published at the end of October (2025: +0.5 to +1.0%; 2026: +0.5 to +1.5%), which also cover the government’s growth expectations (2025: +1.0%; 2026: +1.3%).

GDP Forecasts 2024 to 2026

Year-over-year change in real gross domestic product, in percent

How did the Russian economy perform in the summer and fall of 2025?

Regarding current economic developments, the CMASF notes in its “Analysis of Macroeconomic Trends” published on December 23 that, according to its estimates, real gross domestic product rose slightly by 0.1% on a seasonally adjusted basis in the third quarter of 2025 compared to the second quarter . In the second quarter, it stagnated at the level of the previous quarter, while in the first quarter it fell by 0.3% compared to the previous quarter.

According to the institute, the data on economic development in October point to a “volatile economic situation.” On the demand side, only consumption is growing (in anticipation of an increase in the value-added tax and the vehicle recycling fee).

The decline in fixed investment slowed to -1.7% in the third quarter compared to the previous quarter on a seasonally adjusted basis. In the second quarter, fixed investment actually fell by 3.7% compared to the previous quarter—more than double the rate of the previous quarter (Q1: +2.9% compared to the previous quarter, seasonally adjusted)

Industrial production also showed “volatile” trends in October/November

Regarding economic developments in November, the statistics agency Rosstat published data on industrial production on December 24. In its report on industrial developments in November, published on December 26, the CMASF states:

According to Rosstat, seasonally adjusted industrial production jumped by 2.9% in October compared to September. In November, however, it fell by 1.4% compared to the previous month. On average, industrial production grew by only 0.2% per month from September to November.

Fluctuations in industrial production over the past few months have been driven by production trends in sectors with a high share of defense-related products. Total production in the core civilian sector of “manufacturing” has been stagnant for four months.

In its “Analysis of Macroeconomic Trends,” the CMASF also reports, among other things, on the development of foreign trade, the seasonally adjusted development of wages, income, and consumption, as well as the development of consumer prices:

Foreign Trade: Export revenues are stagnating amid low prices

Imports of goods (at current prices) continued to decline on a seasonally adjusted basis in October, driven by falling demand for capital goods.

Exports of goods (at current prices) remained stagnant in October on a seasonally adjusted basis.

Ruble-denominated gas prices have recovered significantly, while metal prices have risen only slightly. In both cases, however, ruble-denominated export prices remain at a “historically moderate level.” At the same time, ruble-denominated oil prices are at a historic low.

A similar crisis situation prevails with regard to revenues from wheat exports; prices here are at the level of the “COVID winter crisis” of 2021.

Wages, Income, Consumption: Front-loaded Purchases Due to Tax Hike

Real wages recovered in September. With a 1.0% increase (seasonally adjusted compared to August), the 0.8% decline in August compared to July was offset.

Real household income is likely to have recovered seasonally adjusted in line with real wages (September: +0.6%; August: -0.4%),

Seasonally adjusted private consumption surged in October compared to September (+1.3%; third quarter average +0.4% per month).

Almost the entire increase in consumption is attributable to purchases of non-food items (October: +2.0%, seasonally adjusted). This is likely due to consumers bringing forward purchases in anticipation of the upcoming increase in the value-added tax and the introduction of the vehicle recycling fee.

The markets for food and services continue to show “normal” growth on a seasonally adjusted basis (October: food: +0.9%; services: +0.4%).

The annual increase in consumer prices falls below 6 percent in December

Based on data from December 15, the CMASF estimates the annual increase in consumer prices in December at 5.5 to 5.6%. Inflation continues to fall rapidly.

The CMASF cites the weak price increase for most non-food items and the appreciation of the ruble as reasons for the more stable price trend. However, the CMASF considers it possible that inflation will pick up again toward the end of the year, as demand growth is emerging and the ruble is weakening.

Ministry of Economic Development: GDP grew by 1 percent in the first eleven months

Following the full release of Rosstat’s economic data for November on December 26, the Russian Ministry of Economic Development estimated that Russia’s real gross domestic product in the first eleven months of 2025 was 1.0 percent higher than in the same period of the previous year. In November, GDP exceeded the previous year’s figure by only 0.1%, according to the ministry, following a strong increase of 1.6% in October. This development was partly due to calendar-related factors—November 2025 had two fewer working days than November 2024 (Finmarket.ru).

In September, the ministry had lowered its forecast for Russian GDP growth in 2025 from 2.5% to 1.0%. It revised its forecast for 2026 downward from 2.4% to 1.3%.

Forecasts by the “Eurasian Fund for Stabilization and Development”

Like the Moscow-based CMASF, the “Eurasian Fund for Stabilization and Development”—supported by six successor states of the Soviet Union—sees economic development in 2025 and 2026 similarly to the Russian government. The EFSD expects only slightly less growth than the government. It forecasts a 0.7% increase in GDP for 2025 (government: 1.0%) and an acceleration of growth to 1.1% in 2026 (government: 1.3%).

In summary, the EFSD published the following forecasts in the winter edition of its quarterly “Regional Economic Outlook” on December 15:

Economic growth will pick up to just 1.1 percent in 2026

The EFSD estimates Russia’s GDP growth in 2025 at 0.7%. The forecast was revised downward by 0.4 percentage points compared to the forecast from October 10.

The main reason for the slowdown in growth in 2025 is a significant decline in investment, which grew at a lower rate than expected. Inventory drawdowns and a sharper-than-expected decline in oil and gas exports are also dampening GDP growth. Consumption remains the sole driver of growth.

In 2026, the economy will continue to grow slowly, with GDP growth at 1.1%. Investment will remain under pressure due to restrictive monetary policy. Consumption will slow due to a weaker labor market and lower income growth.

Real Gross Domestic Product

Year-over-year changes in percent

Eurasian Fund for Stabilization and Development: Regional Economic Outlook, Winter 25, Dec. 15, 2025

The above figure from the EFSD indicates that, according to Rosstat, the annual growth rate of real gross domestic product will decline over the course of 2025 from +1.4% in the first quarter of 2025 to +1.1% in the second quarter to just +0.6% in the third quarter. According to the figure, the “Eurasian Fund for Stabilization and Development” considers a slight year-over-year decline in real gross domestic product in the fourth quarter of 2025 to be likely.

The EFSD expects that the excess of demand over supply, the so-called “positive output gap,” will be eliminated in the second half of 2026. Subsequently, the Russian economy is expected to return to a “balanced growth path” with annual GDP growth of 1.6% in 2027 and 1.7% in 2028.

Consumer price inflation will fall to 5.1 percent in December 2026

The EFSD lowered its inflation forecast for December 2025 from 7.6% to 6.9%, as inflation in the third quarter came in lower than expected. The main reason for this is a sharper seasonal decline in fruit and vegetable prices due to favorable weather conditions. Many other observers, however, such as CMASF, expect the inflation rate to fall below 6 percent in December 2025.

Year-over-year increase in consumer prices, in percent

Eurasian Fund for Stabilization and Development: Regional Economic Outlook, Winter 25, Dec. 15, 2025

The EFSD anticipates that inflationary pressures will continue to decline in the medium term under the influence of restrictive monetary policy. However, the economy will face several “inflationary shocks.” These include the increase in the value-added tax from 20% to 22% starting in January 2026, the introduction of new recycling fees for imported vehicles starting in December 2025, and ongoing tensions in the fuel market. Taking these factors into account, the EFSD forecast for the annual inflation rate in December 2026 is now 5.1% and 4.1% for December 2027. A return to the central bank’s 4.0% target is expected by December 2028.

According to the EFSD, the rapid cooling of the economy, the easing of labor market conditions, and the steady decline in inflation are creating the conditions for further gradual monetary policy easing. The EFSD anticipates that, following the Russian Central Bank’s reduction of its key interest rate to 16% per annum, monetary policy easing will continue in 2026. The key interest rate is expected to fall to an annual average of 13.5% in 2026.

According to the EFSD, the average ruble exchange rate for 2025 will be around 84 rubles per dollar. With the decline in the key interest rate and the recovery in demand for foreign investments, the EFSD expects a gradual depreciation to 91 rubles per dollar in 2026 and to 95 to 96 rubles in 2027 and 22028.

EFSD Forecasts: Growth, Inflation, Exchange Rate, and Key Interest Rate 2024–2028

CNN: Economic Developments Will Not Force Russia to Make Peace

A CNN analysis by Lauren Kent points out that the Russian government is not only grappling with a significant slowdown in economic growth. In addition, inflation remains “unchecked.” Furthermore, the budget deficit is rising sharply. Key factors behind this are the massive increase in military spending and declining government revenues from the oil and gas sector.

However, based on interviews with experts, CNN concludes that it is unlikely that the crisis-ridden economic situation will force the Russian government to negotiate an end to the war in Ukraine in the foreseeable future.

CSIS Expert Snegovaya: Russia Can Continue the War for Three to Five Years

Maria Snegovaya, an expert on Russia and Eurasia at the Washington-based Center for Strategic and International Studies (CSIS), says, according to CNN, that the current situation is “not a disaster, but manageable” for the Russian government. Russia could continue the war for the next three to five years. However, reliable assessments beyond that are difficult.

In late September, Snegovaya wrote in a CSIS brief on the war in Ukraine that, from an economic perspective, Russia could sustain the war in Ukraine for at least another two to three years. Despite a growing budget deficit, rising inflation rates, and slowing growth in the civilian and industrial sectors, the Russian government continues to view the situation as manageable and persists in its geopolitical confrontation with the West.

According to Snegovaya, Russia has offset the slump in foreign investment through massive government spending on its military-industrial complex. A combination of technocratic management, flexible supply chains, low debt, support from China, Iran, and North Korea, as well as stable energy revenues, has enabled Russia to sustain both its “military operations” and its social spending.

Speaking to CNN, Snegovaya explained that history shows Russia is more likely to agree to a peace deal unfavorable to Russia when it is in the midst of an economic crisis, such as at the end of World War I and during the Soviet war in Afghanistan. However, the current economic situation in Russia is “nowhere near that point,” she told CNN. It would require significantly greater pressure on the Russian economy and a much longer period of time before that point is reached, she explained.

Citizens are being burdened with tax hikes and rising prices

According to Snegovaya, what has changed for Russia is that the initial economic upswing appears to be over due to the sharp rise in military spending. The government must now place the burden of the war on Russian society. This burden on society is reflected in a significant increase in corporate and income tax rates, as well as a rise in the value-added tax, to finance record military spending.

Russian consumers are also being burdened by sharply rising prices, particularly for imported goods. Unlike in the West, however, high inflation in Russia “does not lead to significant social discontent,” argues Snegovaya, citing the effects of state propaganda and repression.

RUSI expert Dr. Connolly: Russia has enough money for its war plans

Dr. Richard Connolly, a “Senior Associate Fellow” for International Security at the London-based think tank “Royal United Services Institute (RUSI),” also told CNN that inflation in post-Soviet Russia has always been high and that Russian consumers are therefore accustomed to it.

Connolly points out to CNN that Western sanctions have not harmed Russia’s energy-dependent economy enough to alter the government’s war plans. “As long as Russia is producing oil and selling it at a reasonably decent price, they have enough money to get by somehow,” Connolly says. The financial situation is unlikely to play a role in Putin’s deliberations on continuing the war, even if the state of the Russian economy “doesn’t paint a particularly rosy picture.”

Recommended reading:

- CMASF: On the development of industrial production in November, 12/26/25

- Finmarket.ru: Russia’s GDP growth was 0.1% in November and 1.0% for the period from January to November, Dec. 26, 2025

- Finmarket.ru: In November, Russian retail sales rose by 3.3% and by 2.5% over the past eleven months, Dec. 26, 2025

- Finmarket.ru: Real wage growth in Russia accelerated to 6.1% in October and reached 4.7% over the past ten months, Dec. 26, 2025

- Finmarket.ru: Industrial production in Russia fell by 0.7% in November, while growth over the past eleven months stood at 0.8%, 12/24/25

- Politcom Economic Report; Marina Voitenko: On the Path to the Inflation Target “Without Autopilot,” Dec. 25, 2025

- MK.ru; Igor Nikolaev, Institute of Economics of the Russian Academy of Sciences: A Year of Unfulfilled Expectations: Economic Results for 2025, 12/24/25

- globalmsk.ru: Experts Summarized the Economic Results for 2025, Dec. 24, 2025

- Kommersant: Work efficiency without additional benefits. Why focusing on productivity does not yet lead to economic growth, 12/24/25

- The Conversation; Yerzhan Tokbolat, Queen’s University Belfast: Russia’s war economy is not collapsing, but neither is it stable, Dec. 17, 2025; see also Asia Times, Dec. 23, 2025

- The Telegraph; Melissa Lawford: Putin’s ‘dear friend’ Xi piles pain on Russia’s economy, 12/23/25

- CMASF: Analysis of macroeconomic trends, Dec. 23, 2025

- Vedomosti: Mishustin: Russia’s GDP growth has approached 10% over the past three years; Dec. 22, 2025

- Business Punk; Oliver Stock: One Percent of Hope: How Putin is sugarcoating Russia’s economy—and what the numbers really say, 12/22/25

- Russia.capital: Russian Central Bank cuts key interest rate to 16 percent, 12/22/25

- MSK1ru: Economists explained why Russian GDP growth will be 1% by 2025. Vladimir Putin also said that the unemployment rate in Russia has fallen to 2.2%, 12/21/25.

- CNN Analysis, Lauren Kent: Russia’s economy is struggling. But that won’t bring Putin to the negotiating table for years, Dec. 20, 2025

- Focus.online; Christoph Sackmann: Only $40 per barrel. Oil crash hits Russia hard: Putin’s main source of revenue is drying up, with reader debate; Dec. 19, 2025

- Börsenzeitung; Eduard Steiner: Sentiment ahead of Putin’s annual press conference: Russia’s economy wants peace—and expects a shock, Dec. 18, 2025

- Expert.ru; Ekaterina Futurova, “Expert”: Getting on a positive track. How to boost GDP growth, 12/17/25

- CSIS Brief; Max Bergmann, Maria Snegovaya: Russia’s War in Ukraine: The Next Chapter, 09/30/25

- German-Russian Chamber of Foreign Trade: Focus Analyses:

- Inflation Falls, Growth Slows: Why the Central Bank Is Still Only Cutting the Key Rate by 0.5%

- Russian analysts and German institutes expect growth to remain weak, Dec. 23, 2025

- Russian President on the EU, the West, and the Economic Situation, Dec. 19, 2025

- Showdown in Brussels: The Decision on Russian Central Bank Funds, 12/17/25

- Podcast “Tsars, Data, Facts” by the German-Russian Chamber of Foreign Trade:

Thomas Baier in conversation with: - Philip Pilkington: Geopolitical Shifts and Economic Impacts; Topics: Frozen Russian assets in the EU; Russia’s economic strategies, growth forecasts, 12/23/25

- Ben Aris, Editor of BNE IntelliNews, on frozen Russian assets in the EU: “Russian Frozen Money: Europe’s Tough Decision,” 40 min, Dec. 15, 2025