IMF: Russia's growth will slow to about 1 percent in 2025 and 2026

Author: Klaus Dormann

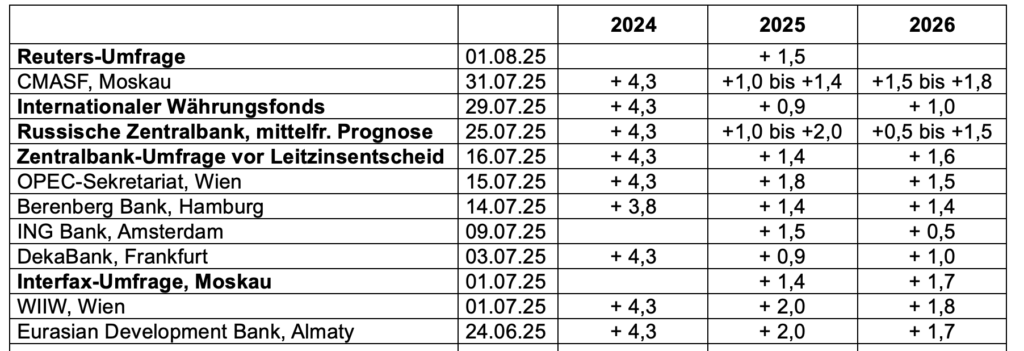

On July 29, the International Monetary Fund lowered its forecast for this year’s growth in the Russian economy from 1.5 percent to 0.9 percent. This makes the IMF the first of the international economic organizations to fall below the growth range that the Russian Central Bank reiterated as its forecast for 2025 on July 25. The growth forecasts published in mid-May/early June by the World Bank (+1.4%), the OECD (+1.0%), the European Commission (+1.7%), and the United Nations (+1.5%).

Contrary to what was announced, the statistics agency Rosstat has not yet fully published the economic data on the development of the Russian economy in June. Among other things, data on retail sales are still missing. Initial estimates of overall economic output in the second quarter are therefore not yet possible. However, according to initial calculations by the Federal State Statistics Service (Rosstat), Russia’s industrial production in the second quarter was 0.6 percent higher than in the previous quarter, according to the Moscow-based “Center for Macroeconomic Analysis and Short-Term Forecasting” (CMASF). This suggests that Russia’s overall economic output also grew in the second quarter compared to the previous quarter.

However, the results of the monthly business survey by the research firm S&P Global signal a significant further slowdown in business activity among companies in the “manufacturing sector” for July. The “Purchasing Managers’ Index,” the “S&P Global Russia Manufacturing Purchasing Managers’ Index,” fell to its lowest level in three years.

IMF: Tight monetary policy and lower oil prices are weighing on Russia’s growth

Petya Koeva-Brooks, Deputy Director of the IMF’s Research Department, summarized the new IMF forecast and the slowdown in Russia’s economic growth as follows during the IMF press conference (video, min. 33):

We expect growth in the Russian economy to slow in 2025. This is primarily due to policy tightening and lower oil prices. We expect growth this year to be 0.9 percent, 0.6 percentage points lower than we previously assumed (+1.5 percent).

This downward revision of the forecast also reflects the timing of growth. Growth in the fourth quarter of 2024 was higher than we expected, leading us to raise our growth forecast for 2024 (from +4.1 percent in the IMF Spring Forecast to +4.3 percent now). The flip side of this, however, is that we recorded lower-than-expected growth in the first quarter of this year.

At the same time, we also see “relative weakness” in current indicators, such as retail sales and industrial production, as well as the official monthly GDP figures, which in turn has led to this downward revision of the forecast for 2025.

At a press briefing ahead of the IMF’s forecast update, Julie Kozack, Director of the IMF’s Communications Department, cited the tightening of sanctions as another reason for the slowdown in Russia’s economic growth.

Russia’s Ministry of Economic Development is working on a new forecast

According to Vedomosti, a spokesperson for the Russian Ministry of Economic Development commented on the IMF’s downward revision, noting that this was not the first time international financial institutions had issued negative forecasts regarding the Russian economy. However, in recent years, none of these overly conservative estimates have matched reality. The ministry is currently developing a forecast that will take all factors into account.

In the Ministry of Economic Development’s most recent forecast from April, which also served as the basis for budget planning, economic growth of 2.5 percent is expected for 2025. However, Finance Minister Anton Siluanov announced as early as the beginning of July on the sidelines of a BRICS conference in Rio de Janeiro that he expects growth of 1.5 to 2.0 percent in Russia this year (Vedomosti.ru).

Analyst surveys suggest growth of around 1.5 percent in 2025

In an analyst survey published by the Reuters news agency in early August, the 14 participants continued to expect, on average, real gross domestic product growth of 1.5 percent for 2025. The Moscow-based “Center for Macroeconomic Analysis and Short-Term Forecasts,” CMASF, maintained its forecast that real gross domestic product is likely to grow by 1.0 to 1.4 percent in 2025 following the release of data on the annual increase in industrial production in the second quarter (“Basic Version of Economic Forecast 2025-2028”). Surveys conducted by the Russian Central Bank and the Interfax news agency in July projected growth of 1.4 percent.

GDP Forecasts for 2024 to 2026

Change in real gross domestic product compared to the previous year, in percent

IMF: Russia’s growth in 2025 and 2026 will be similarly weak to that of the eurozone countries

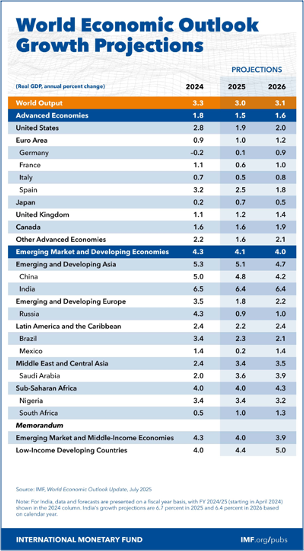

While the IMF lowered its growth forecast for the Russian economy this year by 0.6 percentage points compared to its April forecast, it raised its forecast for global economic growth by 0.2 percentage points to 3.0 percent (Finmarket.ru).

The IMF also raised its forecast for growth in the eurozone countries by 0.2 percentage points. Nevertheless, at +1.0% in 2025, growth in the eurozone countries will be nearly as weak as that of the Russian economy (+0.9%), according to the IMF forecast. In 2026, too, the eurozone countries will grow barely faster (+1.2%) than Russia (+1.0%).

In the last two years, the eurozone countries have grown much more slowly (2023: +0.5%, 2024: +0.9%) than the Russian economy (2023: +4.1%, 2024: +4.3%). The German economy even contracted slightly during the same period (2023: -0.3%; 2024: -0.2%). According to the IMF, it will also remain virtually stagnant in 2025 (+0.1%).

MF: World Economic Outlook Update, July 2025, July 29, 2025; Chart link

Comments from Russia on the IMF Forecast

Expert.ru gathered opinions from several Russian analysts on the IMF forecast. Below is a summary of their views.

Natalia Orlova, Chief Economist at Alfa Bank, suspects that the downward revision of the IMF forecast to 0.9 percent may be related to the IMF’s reassessment of the risks posed by sanctions to Russia. U.S. President Donald Trump had previously stated that he was giving Russia 50 days to resolve the armed conflict in Ukraine. On July 29, he shortened this deadline to 10 days and threatened to impose secondary tariffs, for example on India, at a rate of 100%. While Russia assumes that the sanctions could have only a limited effect, foreign experts generally expect more serious damage from sanctions, Orlova explained.

According to Orlova’s assessment, the Russian economy is on track for 1.3% growth so far this year. Regardless of whether the growth rate is 1.3%, 1.0%, or 0.9%, growth will amount to only about a quarter of the growth rates achieved in 2023 and 2024.

In her view, the slowdown in growth is partly due to lower subsidies for taking out mortgage loans. This has dampened production in the construction sector. Orlova also believes that the increase in the key interest rate in 2024 had a negative impact. The higher interest rates slowed growth in the credit markets and, consequently, the growth of the economy as a whole.

Vladimir Eremkin, a researcher at the “IPEI Structural Research Laboratory” of the “Russian Presidential Academy of National Economy and Public Administration (RANEPA),” believes that the development of the Russian economy continues to be weighed down by a high key interest rate, a labor shortage, and the threat of additional sanctions. Potential cuts to the national budget could also slow growth. However, Eremkin believes that the situation in these areas has not noticeably worsened since April 2025 (when the IMF published its latest forecast). Therefore, there is no reason to lower the growth forecast by 0.6 percentage points. He expects GDP growth this year to be between 1.4 and 1.6 percent.

According to Eremkin, GDP growth could be driven by the following factors:

stable domestic demand coupled with rising real incomes among the population;

a slowdown in inflation and an easing of monetary policy;

higher government spending with the continuation of major infrastructure projects.

Elena Akhmedova, Chief Economist at JSC Euler Analytical Technologies, believes that increased oil production could provide an additional boost to growth as restrictions under the OPEC+ agreement are eased. Overall, the Russian economy will move toward a “balanced growth path.” Production potential is rising due to investments, while demand growth is gradually slowing under the influence of restrictive monetary policy. She forecasts GDP growth of 1.5 to 2% in 2025 and around 1.5% in 2026.

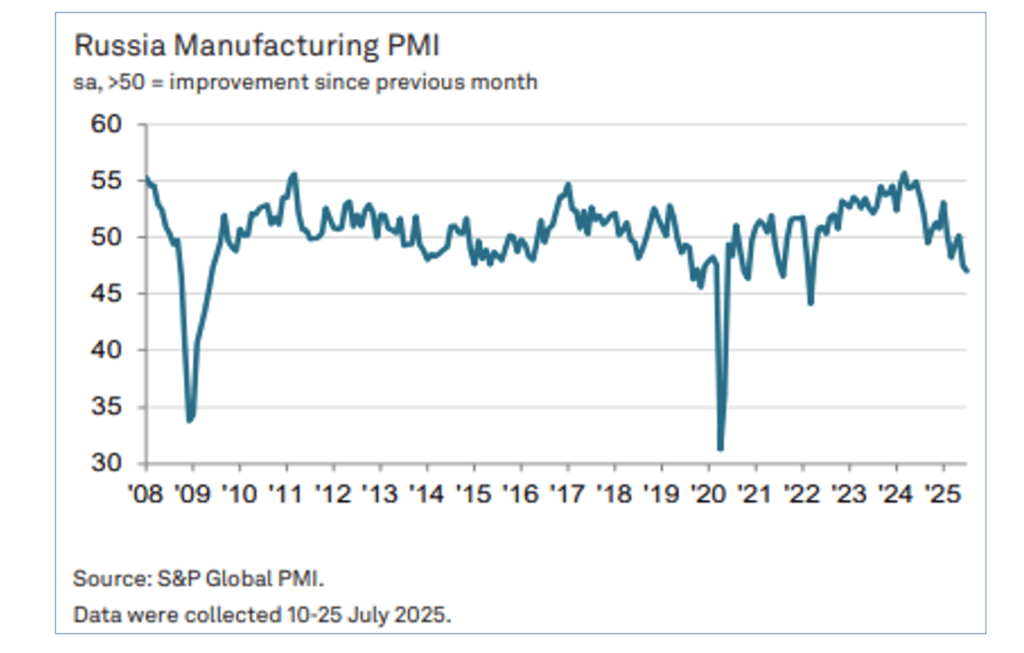

Purchasing Managers’ Index for the “manufacturing sector” well below the “growth threshold”

However, surveys on the business performance of Russian companies signal a significant deterioration in growth prospects. The globally active research firm “S&P Global” also surveys Russian companies monthly on business performance. Last week, the results of the July survey in Russia’s “manufacturing sector” were published, the so-called “Purchasing Managers’ Index.”

The “S&P Global Russia Manufacturing Purchasing Managers’ Index (PMI)” had reached a long-term high in the spring of 2024. Since then, it has fallen sharply in a seasonally adjusted trend, with significant fluctuations. Since September 2024, it has repeatedly fallen below the “growth threshold” of 50 index points. This signals a decline in business activity among companies compared to the previous month.

Purchasing Managers’ Index for the “Manufacturing Sector”

Long-term trend since January 2008, seasonally adjusted

S&P Global: Steepest drop in Russian manufacturing production for three years in July, 08/01/25

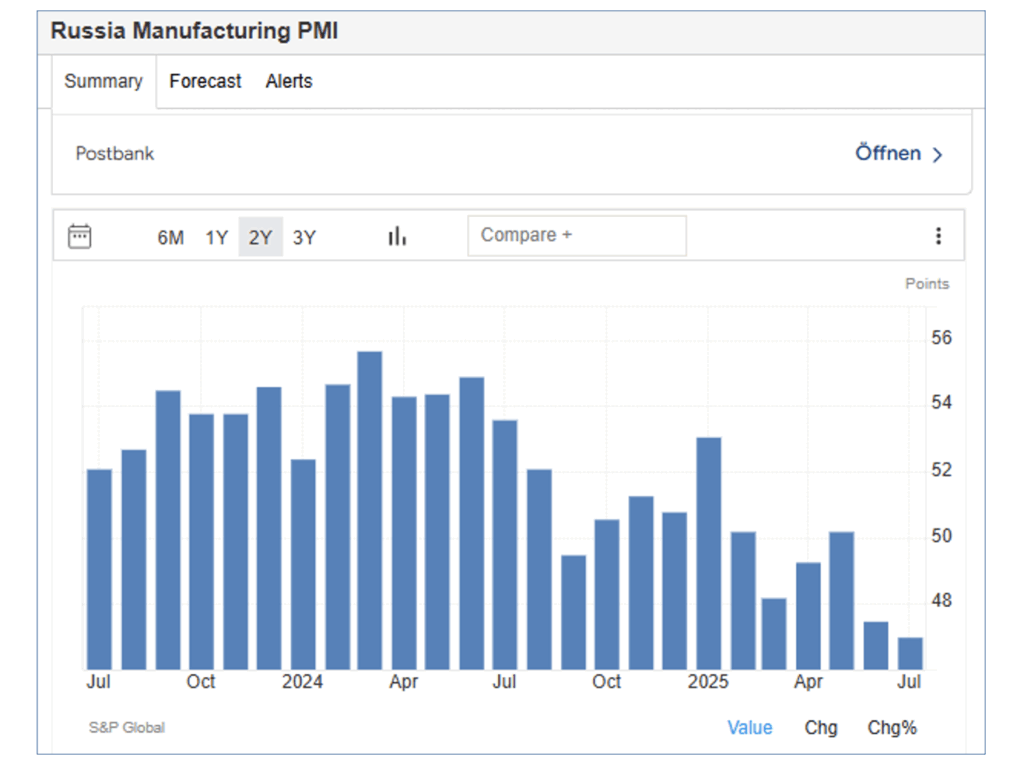

In June 2025, the Purchasing Managers’ Index fell to 47.5 points; in July, it dropped to just 47.0 points. This is the lowest level since spring 2022, shortly after the start of the war in Ukraine.

Purchasing Managers' Index for the "Manufacturing Sector"

Trend since July 2023

TradingEconomics: Russia Manufacturing PMI, August 1, 2025

S&P Global reports on current business developments in the manufacturing sector, noting among other things:

New orders at companies declined in July for the fourth time in the last five months. The decline accelerated to the fastest pace since March 2022. Companies reported that weak demand was partly due to customers’ financial problems.

However, orders from abroad rose for the first time in five months. Companies stated that the increase was not due to orders from new export markets, but rather to higher order intake from existing export markets.

Production has fallen in each of the past five months. The latest decline was the sharpest in three years. In light of the accelerating decline in sales, companies scaled back their production plans at the start of the third quarter.

Although purchase and selling prices continued to rise in July, the increase was only modest in a long-term comparison. Selling prices rose at the slowest pace since November 2022 due to increased competition and the very slow rise in operating costs.

With lower order intake and cost-cutting measures, a decline in production in July led to a further drop in employment and procurement purchases.

The order backlog was rapidly reduced in July. Companies were able to work through their order backlogs.

Inventories of raw materials were reduced for the sixth consecutive month, albeit at a slower pace. In contrast, order cancellations led to a renewed increase in finished goods inventories.

At the same time, companies remained optimistic that production will rise in the coming year. They hope that investments in new products, machinery, and equipment will help boost sales.

Podcasts and reading recommendations:

- Eduard Steiner in conversation with Vasiliy Astrov, wiiw: A rude awakening in Russia: Is the economy now paying the price for the war in Ukraine? 07/30/25

- ZEIT podcast “What Now?”: Is Putin running out of money? Michael Thumann, head of the ZEIT Moscow bureau, in conversation with Constanze Kainz about Russia’s economic situation and the question of whether a lack of funds could actually force Putin to back down; video, 22 min., July 24, 2025

- German-Russian Chamber of Foreign Trade: Podcast “Tsars. Data. Facts”; Thomas Baier in conversation with Oliver Kempkens: Banking crisis in Russia? A look behind the scenes, 07/23/25

- German-Russian Chamber of Foreign Trade: Focus Analyses, German; also in Russian: Trump’s Tariff Threat Against Russia and Its Trading Partners, July 21, 2025

- Kommersant, Artem Chugunov: There is nothing to warm up demand with; Sberindex; Income and Consumption, July 31, 2025

- The Moscow Times; Tatyana Rybakova: What Is Behind Russia’s Wartime Prosperity Paradox? July 30, 2025

- Business Insider; Huileng Tan: IMF Forecast: Russia’s Growth Slows Significantly in 2025. Russia’s Economy Loses Momentum: IMF Revises Economic Forecast Downward, July 30, 2025

- The Moscow Times: IMF Slashes Russia’s Economic Forecast as Wartime Growth Slows, June 30, 2025

- Vedomosti; Ksenia Kotchenko: IMF lowers forecast for Russian economic growth this year to 0.9 percent, July 29, 2025

- Finmarket.ru: Ministry of Economic Development: The ultra-conservative estimates by international financial institutions regarding the dynamics of Russian GDP have never come true, July 30, 2025

- Finmarket.ru: IMF lowers forecast for Russian GDP growth in 2025 to 0.9 percent, raises forecast for global economy to 3 percent, July 29, 2025

- FAZ+, Katharina Wagner: Putin’s Reserves: Could Russia Collapse Under the Burden of War? Full text on Inosmi.ru, July 29, 2025

- bne IntelliNews: Comment: Why Russia’s economic model no longer delivers, July 25, 2025

- The Telegraph; Jeremy Warner: Don’t bank on Russian economic collapse to save Ukraine. Western sanctions have failed to halt Putin’s expansionist ambitions, July 24, 2025

- US News; Reuters: Explainer—Why the Russian Ruble Is Outperforming and What It Means, July 24, 2025

- George Friedman; Cicero.de: The War in Ukraine – Putin’s Lost Bet, July 24, 2025; Geopolitical Futures: Putin’s Dilemma. Analyzing the Process by Which the Russia-Ukraine War Will End, July 22, 2025