How widely German forecasts of Russia's growth vary

Author: Klaus Dormann

Will Russia’s economy grow by only 0.4 percent this year? That is what the Munich-based ifo Institute now expects. Or will Russia still achieve economic growth of 2.7 percent in 2025? That was the forecast issued on May 21 by the “German Council of Economic Experts.” Uncertainty regarding Russia’s economic development is apparently very high.

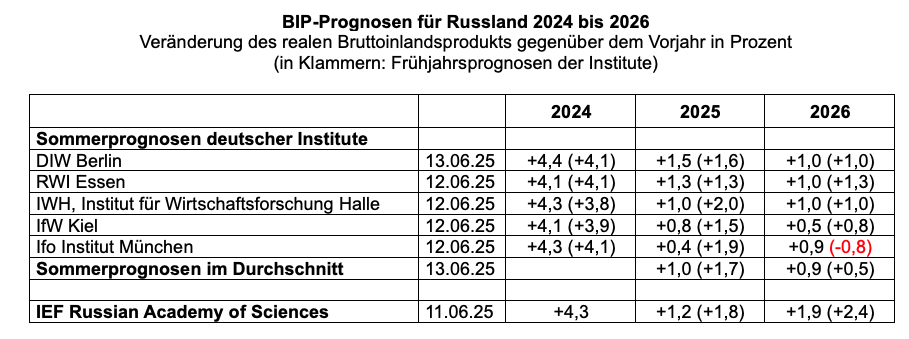

On average, German institutes now expect growth of just 1 percent

The five leading German economic research institutes published their “summer forecasts” for the development of the German and global economies in mid-June. According to the statistics agency Rosstat, Russia’s economic growth rose to 4.3 percent in 2024. Three months ago, in their “spring forecasts,” German institutes expected on average that it would slow to 1.7 percent in 2025.

In their “Joint Assessment” in April, they projected that Russia’s economic growth would still reach 2.0 percent in 2025. Now, in their “summer forecasts,” they expect on average that it will drop to just 1 percent this year.

For comparison, here are some forecasts from Russia: The Institute for Economic Research of the Russian Academy of Sciences (IEF RAS) expects a very similar trend in 2025 as the German institutes. Over the past three months, it has revised its forecast for Russia’s GDP growth down from +1.8 percent to +1.2 percent—a reduction nearly as steep as that of the German institutes. However, in recent analyst surveys conducted by the Russian Central Bank as well as the news agencies Interfax and Reuters, participants on average still expected slightly stronger growth of +1.5 percent for 2025.

For 2026, German institutions on average expect even slightly weaker growth in Russia (+0.9 percent) than in 2025 (+1.0 percent). The RAS Institute, however, anticipates that Russia’s economic growth will pick up as early as next year, rising from +1.2 percent to +1.9 percent.

The range of growth forecasts for 2025 has widened

Of the five institutes, the Berlin-based “German Institute for Economic Research” now expects the strongest economic growth in Russia in 2025. It lowered its forecast only minimally from 1.6 to 1.5 percent compared to the spring.

The Essen-based “RWI Leibniz Institute for Economic Research” was the only institute to stick with its spring growth forecast (+1.3 percent).

In contrast, the “IWH Leibniz Institute for Economic Research Halle” (from +2.0 to +1.0 percent) and the “Kiel Institute for the World Economy” (from +1.5 percent to +0.8 percent) have significantly lowered their growth forecasts. The Munich-based “ifo Institute” made the sharpest cut to its forecast for Russia’s economic growth in 2025 (from +1.9 percent to just +0.4 percent).

Six months before the end of 2025, the range of growth forecasts from the five German institutes for 2025 now extends from +0.4 percent (ifo Institute) to +1.5 percent (DIW Berlin). This range has not narrowed since the spring but has widened from 0.7 percentage points to 1.1 percentage points.

The growth forecasts for 2026 differ much less

However, the institutes largely agree on the development of aggregate economic output in Russia next year. As many as four institutes expect economic growth of 1 percent (DIW, IWH, RWI) or 0.9 percent (ifo) in 2026. The Kiel Institute for the World Economy, on the other hand, expects Russia’s economic growth to slow from +0.8 percent to +0.5 percent next year.

The ifo Institute has now significantly raised its forecast for 2026. Three months ago, it had still expected gross domestic product to rise by 1.9 percent in 2025, while at the same time anticipating a recession in Russia next year (-0.8 percent). Now, the ifo Institute expects the economic downturn in Russia to take effect sooner. As early as 2025, growth is projected to plummet to just +0.4 percent. In 2026, it is then expected to accelerate to +0.9 percent.

IfW Kiel: Russia’s economy is operating at full capacity

The Kiel Institute for the World Economy has now nearly halved its forecast for this year’s growth in the Russian economy to just 0.8 percent. The IfW outlines the current economic development in Russia in its economic report “World Economy in Summer 2025” as follows:

“Production in Russia was only 1.4 percent higher in the first quarter of 2025 than a year earlier and may even have contracted compared to the previous quarter—seasonally adjusted figures are not available from official sources.

The economy appears to be operating at full capacity; due to the shift to

war production, bottlenecks are becoming increasingly noticeable, and high interest rates—the key interest rate had stood at 21 percent since October and was only slightly reduced to 20 percent in early June—are holding back both consumer spending and non-war-related investment.”

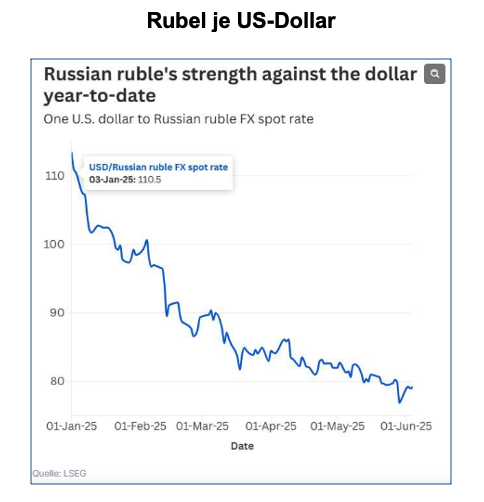

Regarding external economic developments, the IfW also points to Russia’s price-driven decline in revenue from crude oil sales and the ruble’s appreciation against the U.S. dollar (exchange rate chart from TradingEconomics).

Falling oil prices amid ruble appreciation: “A toxic combination” for Russia

In “The European,” Ansgar Graw analyzed the impact of falling oil prices in U.S. dollars coupled with a simultaneous appreciation of the ruble on Russia’s economy. This combination was described by Vasily Astrov, the Russia expert at the “Vienna Institute for International Economic Studies (wiiw),” as a “truly toxic combination” for Russia in an interview with the newspaper “Die Welt.”

According to the following Finam chart, while Russian dollar sellers on the foreign exchange markets were still receiving 110.5 rubles for one U.S. dollar on January 3, by mid-June that figure had dropped to only around 80 rubles.

Finam.ru: The ruble is the best performing currency in the world this year, 06/14/25

Graw notes regarding the ruble’s sharp appreciation:

“The strength of the Russian ruble is hurting the Russian economy because energy exports—primarily oil and gas—are settled almost exclusively in foreign currencies, mainly in U.S. dollars and increasingly in Chinese yuan. A strong ruble means that, for the same selling price in dollars, fewer rubles flow into Russian coffers.”

The current situation makes it “truly particularly dangerous for the Russian budget,” Astrov said in “Die Welt”: “If nothing changes about this combination, a budget deficit of three to four percent of GDP is entirely possible” (see also: Investment Week: Ruble Shock: When Strength Becomes Weakness, April 20, 2025).

In an interview with Die Welt, Vasily Astrov pointed out that a drop in oil prices usually leads not to an appreciation but to a depreciation of the ruble. When the ruble depreciates, ruble revenues per U.S. dollar increase. The lower dollar revenues from Russia’s oil exports are then offset by higher ruble revenues per dollar.

RWI: Russia’s current account surplus remained substantial in the first quarter

In its “Early Summer 2025 Economic Report,” the Essen-based RWI takes a closer look at Russia’s foreign trade performance in the first quarter of 2025. Both exports and imports declined slightly in value:

“Between January and March, the value of Russian exports of goods and services shrank by 4% compared to the same period last year. The main factor was the weaker performance of oil exports. Tighter sanctions by the U.S. and the EU against Russian oil shipments made transportation more expensive and forced Russia to offer even deeper price discounts. In addition, natural gas supplies to the EU plummeted after pipeline transit through Ukraine was halted.

Imports of goods and services fell by 3% in the first quarter compared to the same quarter of the previous year. The main factor was a significant decline in imports of machinery, equipment, and transportation vehicles; the latter were additionally impacted by a sharp increase in recycling fees for imported vehicles at the start of the year. By contrast, the food and tourism services import segments recorded growth.

The current account surplus for the period from January to March was slightly below the previous year’s figure but remained substantial.”

RWI: Defense spending does little to boost growth potential

Regarding its forecast that Russia’s overall economic growth is likely to fall by about two-thirds this year to just 1.3 percent, the RWI summarizes:

“Following strong growth in the previous quarter, economic momentum in Russia has noticeably weakened in the first months of this year. Gross domestic product grew by 1.4% year-over-year in the first quarter. Since the growth peak at the end of the year, industrial production and the construction sector have noticeably lost momentum.” …

“The sharp drop in crude oil prices has further clouded Russia’s economic outlook. Economic growth is likely to slow noticeably this year, while inflation is expected to remain at a high level.” …

“In April, consumer prices were 10.2% higher than a year earlier, with food and services in particular driving inflation. Despite a slight easing, inflation expectations remain elevated.

At its June meeting, the central bank implemented only a moderate interest rate cut from 21% to 20%.” …

“Labor shortages and low productivity are holding back output growth. At the same time, capacity utilization is at a historic high, but sanctions are making it difficult to import capital goods. Government investment is flowing primarily into military equipment, which does little to support the future growth potential of the overall economy.” …

“Overall, gross domestic product is expected to grow by 1.3% in 2025 and 1.0% in 2026.”

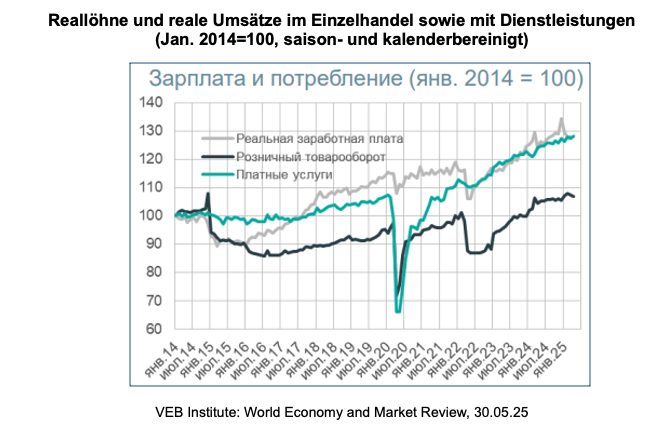

How real wages and private consumption developed in Russia

Regarding the development of the Russian retail sector, the RWI notes:

“Although the average real wage continued to rise in many sectors, retail sales have hardly changed in recent months. According to a consumer survey conducted by the Russian Central Bank, 25% to 30% of respondents reported a deterioration in their financial situation.”

The Research Institute of the Russian state-owned Bank for Foreign Economic Affairs (Vnesheconombank) published the following chart in its weekly report on the development of private consumption. It shows the trend in real retail sales (black line) and services (green line) against the backdrop of the trend in real wages (gray line).

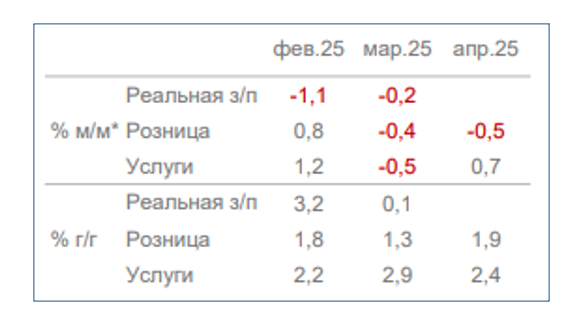

According to initial estimates by the VEB Institute, seasonally and calendar-adjusted real retail sales (black line) fell by 0.4 percent in March and by 0.5 percent in April compared to the previous month. In the services sector (green line), the decline in real sales in March (-0.5 percent) was offset by an increase in April (+0.7 percent).

Trends in real wages, retail sales, and services

compared to the previous month and the same month of the previous year

VEB Institute: World Economy and Market Review, May 30, 2025

Compared to April 2024, real retail sales rose by 1.9 percent in April 2025, and real sales in the services sector rose by 2.4 percent. However, the rise in real retail sales has slowed significantly since spring 2024.

Marina Voitenco, an “economic observer” for the Russian online magazine Politicom.ru, cites the following data on wage and private consumption trends in her latest weekly report:

Real wages rose by only 0.1 percent year-over-year in March 2025 (February: +3.2%). This weak increase is due to the fact that bonus payments for the first quarter were brought forward to December 2024 this year (primarily in the oil and gas sector as well as in the financial sector). In the first quarter of 2025, real wages were 3.4% higher than in the first quarter of 2024. Their increase was significantly higher than the rise in labor productivity.

Total real sales in the “retail,” “food services,” and “paid services” sectors rose by 2.3% year-over-year in April, following a 2.0% increase in March. In the first four months of 2025, real sales in these three sectors grew by a total of 2.7% year-over-year.

Sources and recommended reading:

- IWH Leibniz Institute for Economic Research Halle: Press Release: Current Economic Situation: Economic Recovery in Germany – Structural Problems and U.S. Trade Policy Weighing Down: IWH, Current Economic Situation, Vol. 13 (2), 2025, June 12, 2025

- German Institute for Economic Research Berlin: Press Release: First Glimmers of Hope for the German Economy – DIW Berlin Significantly Revises Forecast Upward; DIW Economic Forecast: DIW Weekly Report 24/2025, June 13, 2025

- RWI Leibniz Institute for Economic Research, Essen: Press Release: RWI in Early Summer: Tentative Upturn Despite Tariff Drama, June 12, 2025; RWI Economic Report Early Summer 2025, Vol. 76 (2025) A03: Global Economy Under the Spell of Trade Policy, June 12, 2025

- Kiel Institute for the World Economy: Kiel Economic Reports including: The Global Economy in Summer 2025: Trade Policy Headwinds Slow Expansion, June 12, 2025; Dossier: Economy: Key Data Table for the World

- Ifo Institute Munich: Economic Forecasts; Press Release: ifo Economic Forecast Summer 2025: Recovery Draws Near – Economic Policy Uncertainties Remain High; in: ifo Schnelldienst, 2025, 6, No. 7: ifo Economic Forecast Summer 2025, June 12, 2025