Hormus Shock: How Big Will Russia's Unexpected Oil Windfall Be?

The attack by the U.S. and Israel in late February began as a military operation and turned into an energy crisis within a matter of days. The U.S. consulting firm Rapidan Energy Group, a Washington-based think tank specializing in energy policy, described last week’s events as the greatest disruption to the global oil supply in history.

20% Oil Shortfall – The Strait on Which Everything Depends

The British business newspaper Financial Times reported that around 20% of global oil shipments are currently affected by the closure of the Strait of Hormuz. In peacetime, more than 20% of the world’s oil passes through the strait. Bordering the strait are not only Iran, but also Bahrain, Iraq, Qatar, Kuwait, Saudi Arabia, and the United Arab Emirates. Countries in the Asia-Pacific region are the hardest hit: 46% of their oil imports come from the Persian Gulf.

The impact on financial markets was immediate and massive. The price of Brent crude oil—the benchmark for Europe—rose from around 60.3 euros per barrel before the war began to more than 90 euros at one point. As of Wednesday, March 11, at press time, the price of North Sea Brent crude stands at around 79 euros—91 dollars.

Analysts at JPMorgan, the largest U.S. investment bank, estimated potential global supply losses through the third week of the crisis at 4.7 million barrels per day—5% of global demand. According to analysis reports, Saudi Arabia, the region’s largest producer, had to cut its export capacity from the Persian Gulf to 2.5 million barrels per day.

In Tokyo, the Nikkei index temporarily plummeted by 7%. The South Korean stock market also recorded heavy losses. Since the attacks began, the DAX has lost up to 2,000 points, or a good 8%, representing a loss of around 150 billion euros in market value for the 40 DAX-listed companies. The Handelsblatt quoted capital market strategist Ed Yardeni, founder of the independent New York-based research firm Yardeni Research:

“Fears that a deteriorating economic situation could weigh on corporate profits have increased significantly.”

Iran War Costs: Scenarios Ranging from $100 to $200

Rory Johnston is the author of the Commodity Context newsletter, one of the most influential independent commodities publications in North America, and is regarded in the industry as an exceptionally level-headed analyst. This makes it all the more remarkable that he sounded the alarm explicitly on the “Odd Lots” podcast of the American business news site.

The permanent closure of the Strait of Hormuz, Johnston said in the podcast, is “the worst-case scenario that is typically used in industry circles only as a thought experiment. ‘It’s the kind of question you only ask hypothetically: What if this were to happen? And now this worst-case scenario has happened.”

The American analyst considers it realistic that oil could rise to $200—equivalent to 172 euros—and beyond: with severe consequences for fuel prices and potential serious supply shortages in the rest of the world.

Johnston explained the key point in the podcast: Since the global oil supply is relatively inelastic—oil fields cannot be ramped up at the push of a button—demand must be rationed through prices in the event of a prolonged supply disruption. A historical comparison was drawn in the podcast: A 20% drop in oil exports is comparable in scale to the decline in global oil consumption during the peak of the 2020 COVID lockdown:

“If 20% of supply disappears, demand must also fall by 20%. And that can only happen through price. That means price levels that most market participants have so far considered unthinkable.”

Using various scenarios and based on oil export and import data, the German-Russian Chamber of Foreign Trade has calculated what the oil price shock triggered by the war in Iran would mean for Russia and Germany. Hundreds of billions of euros are at stake.

The 2026 Russian state budget is based on a Urals price of 50.8 euros, or $59, per barrel at an exchange rate of 92.2 rubles per dollar. Kirill Rodionov, an energy analyst at the Moscow Center for Economic and Political Reforms, told the business newspaper RBC: “In recent months, the average price has been around $40—a level that was critical for the budget.”

According to Bloomberg, the discount of Urals relative to the global benchmark Brent widened to as much as $30, equivalent to €26, the highest discount level since April 2023. The main reason was the collapse of Russian oil exports to India after Washington imposed punitive tariffs on India’s purchases. Following the U.S.-Israeli attacks on Iran, Urals even traded above Brent at times.

According to the British market intelligence firm Argus Media, Indian refineries purchased Russian oil at a premium of $1 to $5 per barrel. On March 8, the U.S. Treasury Department granted India a 30-day sanctions waiver for the purchase of Russian oil. Analysts estimate that this 30-day waiver allowed Russia to resell around 125 million barrels—and the price spike within a few days brought Moscow additional revenue of over one billion dollars. The German Chamber of

Commerce Abroad’s own calculations, based on export data from the International Energy Agency (IEA) and using AI programs, show the impact of higher oil prices on the Russian economy.

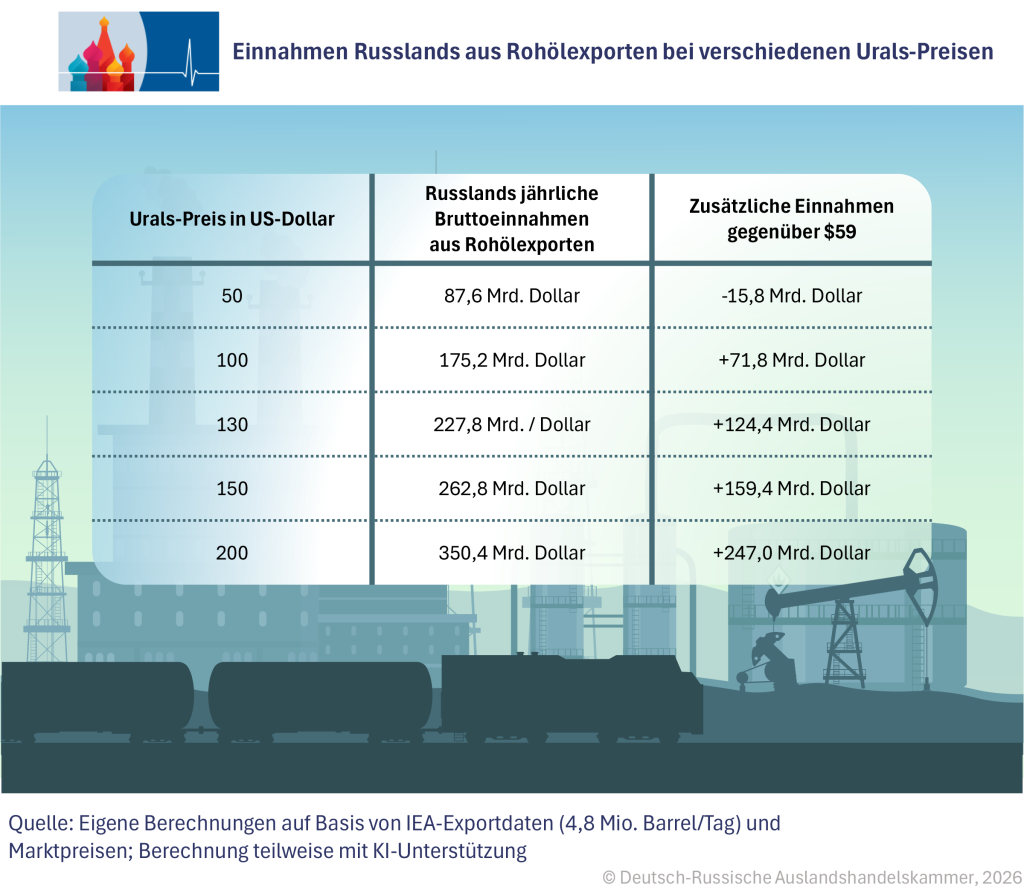

At an average Urals price of $50, Russia’s annual gross revenue from crude oil exports would be around $87.6 billion—$15.8 billion below the budget estimate. At a Urals price of $75, Russia’s annual gross revenue from crude oil exports would be around $131.4 billion—already $28 billion more than budgeted. At $100, it would already be $175.2 billion, an increase of $71.8 billion over the budgeted price. At $130, revenues would rise to $227.8 billion, an additional $124.4 billion. At $150, they would rise to $262.8 billion, an increase of $159.4 billion. And in the extreme scenario of $200 per barrel, the total would be $350.4 billion: $247 billion more than budgeted. By comparison: Russia’s 2026 military budget amounts to approximately $145 billion, or about €125 billion.

Russian estimates remain conservative

Since the beginning of 2026, Russia’s national budget has been under considerable pressure: the price of Russian oil was lower than expected, and the ruble was strong against the dollar. Unlike Western experts, who consider extreme oil prices possible, Russian experts are cautious in their comments but also forecast higher revenues for the Russian budget.

Finam analyst Sergey Kaufman—Finam is one of Russia’s largest online brokers and operates its own macro research team—expects the price discount for Urals relative to Brent to fall below 17 euros per barrel.

“In recent months, the price discounts have widened due to competition between Russian and Iranian oil—but now Iranian supplies have practically come to a standstill for obvious reasons,” said Kaufman. This means that not only is the absolute price of oil rising for Russia, but so is the relative price of Russian oil compared to grades such as Brent and WTI.

His colleague Nikolai Dudchenko, also at Finam, calculated: If the average Urals price remains in the range of 51.7 to 55.9 euros through the end of 2026, Russia’s oil and gas revenues would exceed projected figures by up to 775.0 billion rubles, or roughly 9 billion euros.

Alexander Frolov, Deputy Director General of the Institute for National Energy, is more optimistic: “I expect oil and gas revenues to rise by 30 to 50% compared to January and February 2026.”

The Ministry of Finance had reported revenues of 825 billion rubles for those two months—an increase of 30 to 50% would therefore mean an additional 247.5 to 412.5 billion rubles, or 2.7–4.5 billion euros.

Ruble, Dollar, Barrel: The Three Key Variables

The impact of rising oil prices on Russia’s public finances is inextricably linked to the ruble exchange rate—and this interplay is more complex than it appears at first glance. The budget is denominated in rubles; export revenues are earned in dollars and then converted into rubles. A weaker ruble increases the ruble equivalent of dollar revenues. A rising oil price tends to strengthen the ruble, which partially offsets the positive effect.

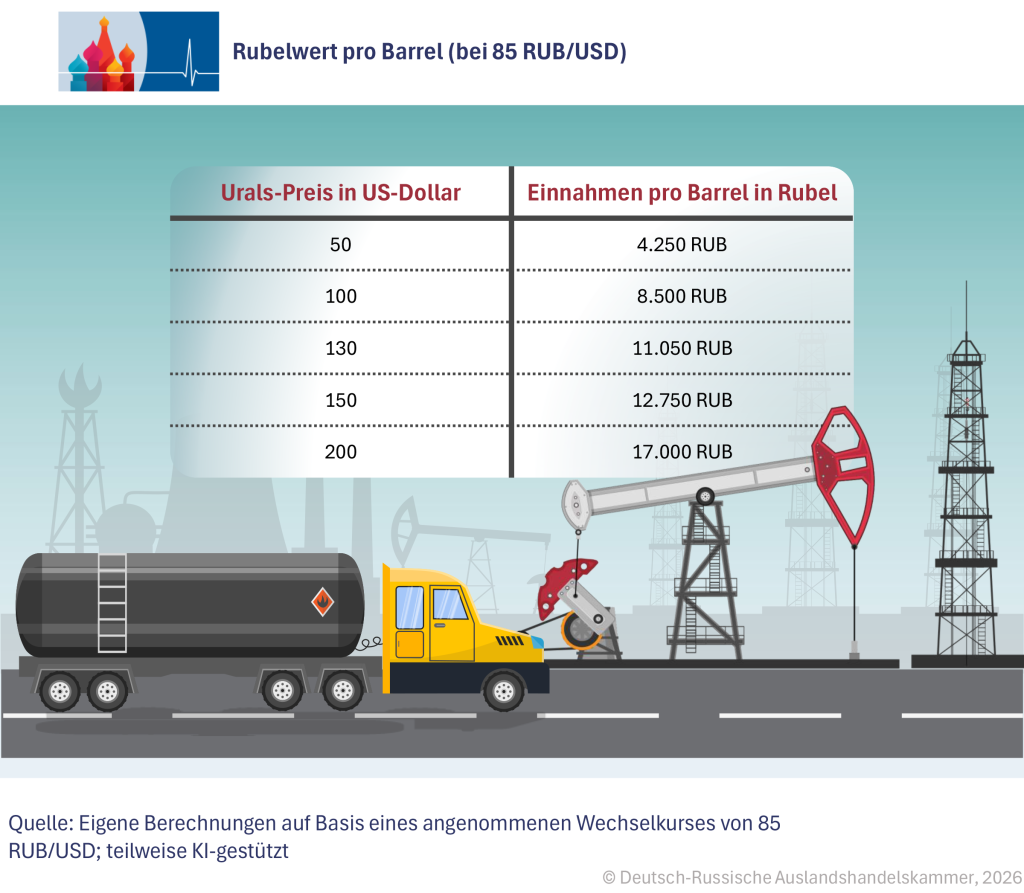

Based on the exchange rate of 92.2 rubles per dollar assumed in the budget and an Urals price of 50.8 euros, this results in a revenue per barrel of around 5,440 rubles. In the pre-war market environment—with an exchange rate of about 80 rubles and a Urals price of 45 euros—the ruble revenue is around 3,600 rubles: significantly below the budgeted figure.

If the Urals price rises to $100 and the ruble exchange rate to 85 rubles, the ruble revenue climbs to 8,500 rubles per barrel—more than twice the budgeted figure. At $130, it would be 11,050 rubles; at $150, 12,750 rubles. In an extreme scenario of $200 per barrel, ruble revenue per barrel would be 17,000—more than three times the budgeted amount.

Following the closure of the strait, Politico, Bloomberg, The Guardian, and the Associated Press all reported that Russia was the main beneficiary of the crisis among oil suppliers. Politico also noted that, in parallel with the events in Iran, the U.S. continues to maintain control over Venezuelan oil—which means that major buyers such as India and China must increasingly turn to Moscow for additional supplies.

Self-sufficient versus dependent: Why America barely feels what is hitting Germany

Gabor Steingart, publisher and founder of the Berlin-based media company The Pioneer and long-time editor-in-chief of Handelsblatt, commented pointedly on the asymmetry of the crisis’s effects in his March 10 Morning Briefing: “Crazy but true: The U.S., which started the war in the Middle East, is barely affected. Germany, which neither wanted nor started this war, is suffering like a dog.” According to Steingart, the main reason lies in energy policy: America has made itself nearly independent of the world market by ramping up liquefied natural gas production, while Germany, following its nuclear phase-out, is more dependent on fossil fuel imports than ever before.

According to a recent analysis by the German Economic Institute (IW Cologne), would cost the German economy 0.3% of gross domestic product in 2026 and 0.6% in 2027—a total loss of economic output of around 40 billion euros over two years. In the extreme scenario of a persistently high oil price, this damage increases significantly: In absolute terms, this would correspond to a real loss of over 80 billion euros over two years, accompanied by a 1.6% increase in consumer prices in 2026 and 1.9% in 2027.

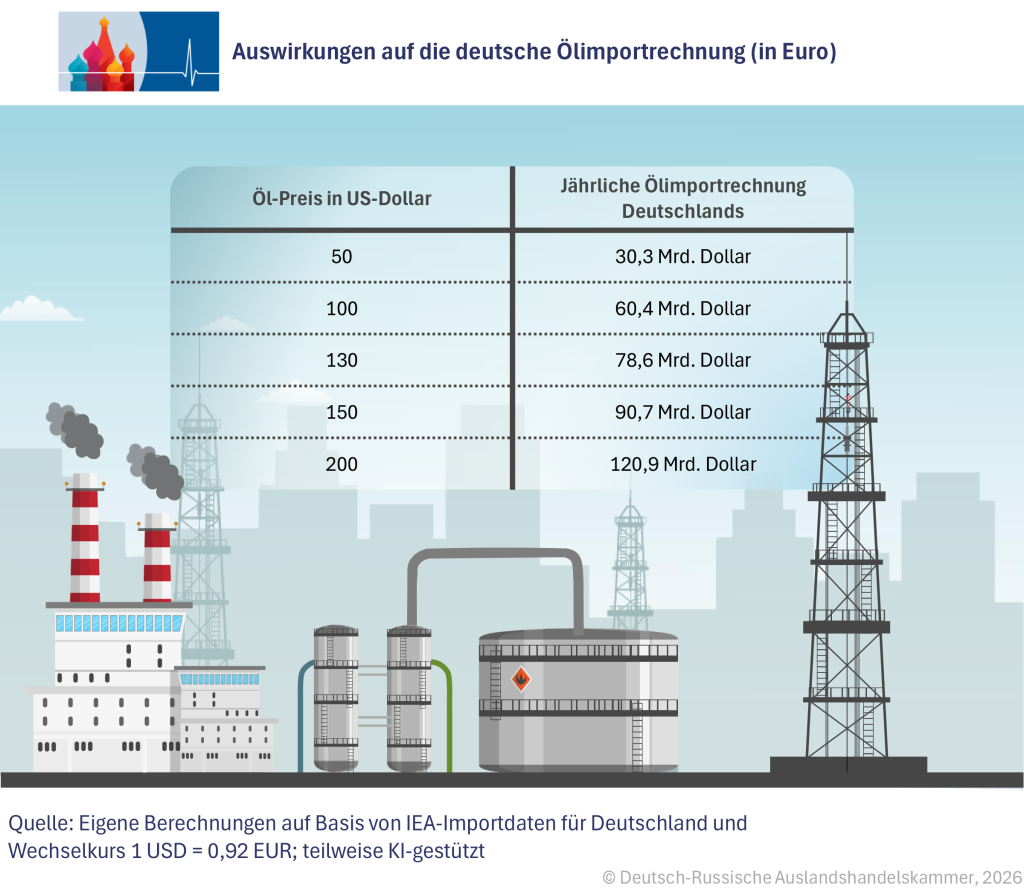

Calculations by the German-Russian Chamber of Foreign Trade show just how heavily the rise in oil prices could weigh on Germany’s import bill. According to the International Energy Agency (IEA), Germany imports around 1.8 million barrels of crude oil daily. At an oil price of $50 and an exchange rate of $1 to 0.92 euros, the annual import bill would be around 30.3 billion euros. At $100, it would already be 60.4 billion euros—a doubling of costs. At $130, costs would rise to 78.6 billion euros, and at $150 to 90.7 billion euros. In an extreme scenario of $200 per barrel, Germany would spend 120.9 billion euros annually on crude oil imports.

By comparison: The total federal budget for 2026 amounts to approximately 480 billion euros in expenditures. An oil import bill of 120 billion euros would thus correspond to a quarter of the entire federal budget.

The figures are model calculations based on simplifying assumptions: constant import volumes, a fixed exchange rate, and gross prices excluding processing margins. The reality is more complex. Nevertheless, they clearly illustrate the structural dilemma Germany faces: As one of the world’s most energy-import-dependent economies, Germany is highly vulnerable to an oil price shock.

Our own calculations based on IEA import data illustrate the scale behind these percentages. At an oil price of $50, Germany’s annual oil import bill amounts to around 30.3 billion euros. At $75 per barrel, the cost is around 45 billion euros. If the price rises to $100, the bill increases to 60.4 billion euros. At $130, it would be €78.6 billion; at $150, it would already be €90.7 billion. In the extreme scenario of $200, Germany would spend 120.9 billion euros on oil imports alone: four times as much as in the baseline scenario and more than a quarter of the total federal budget.

Sebastian Dullien, research director at the Düsseldorf Institute for Macroeconomics and Economic Research (IMK), put it succinctly: “Until the outbreak of the war, the trend was to raise our forecast of 1.2% economic growth for 2026 just a little further. That is now definitely off the table.” Should the war drag on and oil and LNG supplies from the region remain disrupted for an extended period, the energy price shock could be severe enough to derail the recovery of the German economy hoped for in 2026. The crisis is already immediately

noticeable at gas stations: On a nationwide daily average, Super E10 cost about 20.6 cents more than before the start of the war in Iran, and diesel even 37.1 cents more, averaging over 2.10 euros per liter. The ADAC motorists’ association accused the oil industry of exploiting the price increase beyond what is reasonable.

What the war in Iran means for peace in Ukraine

The war in Iran has not only shaken the oil markets; it may also derail the fragile efforts to find a diplomatic solution to the conflict in Ukraine.

Peace in Ukraine now seems a distant prospect, according to Jennifer Kavanagh, director of military analysis at the Washington-based think tank Defense Priorities, writing in the American journal Responsible Statecraft: “The Trump administration had hoped to slowly dry up Russia’s oil revenues to force Moscow into making greater compromises at the negotiating table. That leverage is now lost.”

Analysts at the Dutch ING Bank explain why this is the case: In the base scenario—a four-week disruption of transit through the Strait of Hormuz—Brent stabilizes at an average of $68 over the course of the year. In the event of a three-month partial blockade, the price would rise to $89 in the second quarter. In the extreme scenario of a complete three-month closure, Brent would climb to $110 in the second quarter and remain at an annual average of $95 in 2026.

Eurosintelligence, a Brussels-based economic research firm, writes: “Unfortunately, there is no easy solution to the Hormuz problem for Trump or for any of us. Oil markets will likely continue to grapple with disruptions for as long as this war lasts. The oil crisis won’t be over anytime soon.”

For Russia, this is news that could hardly be better. “So far, there is only one winner in this war: Russia,” said EU Council President António Costa on Tuesday in Brussels. Russia is gaining new resources to finance its military as energy prices rise. It is benefiting from the diversion of military capabilities that could otherwise have been deployed to support Ukraine. And it is benefiting from the fact that attention is being drawn away from the Ukrainian conflict as the conflict in the Middle East comes to the fore.

James Henderson of the Oxford Institute for Energy Studies put it this way to the American news network NBC: “It would surprise no one if Russian military spending were to rise as a result. More money is available, and therefore more money is available for military spending.”

This article first appeared in the exclusive newsletter of the German-Russian Chamber of Foreign Trade