Growth forecasts for 2026 slip below one percent

Author: Klaus Dormann

The London-based European Bank for Reconstruction and Development (EBRD) has also lowered its forecast for Russian economic growth in 2026 to below 1 percent. In September, like the Russian government, it had still expected Russia to achieve a 1.3 percent increase in real gross domestic product in 2026. Now, the European Bank for Reconstruction and Development (EBRD) expects Russia’s economy to grow by only 0.8 percent in 2026—slightly less than in 2025 (+1.0 percent).

For 2027, the EBRD—like the IMF and the World Bank—expects only a very slight pickup in growth to 1.0 percent. The Russian government is much more optimistic. It currently expects economic growth to accelerate to 2.8 percent next year. However, the government plans to update this September forecast in March/April. It is now nearly twice as high as the average growth forecasts in analyst surveys. For instance, analysts surveyed by the Economic Research Institute at Moscow’s “Higher School of Economics” surveyed in mid-February in the “consensus forecast” assumed that growth in the Russian economy would pick up only from 0.9 percent in 2026 to 1.5 percent in 2027.

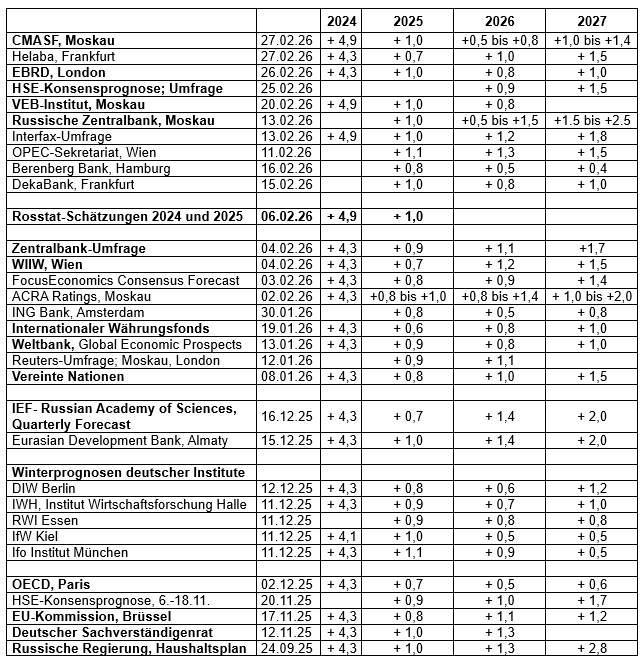

GDP Forecasts 2024–2027

Year-over-year change in real gross domestic product, in percent

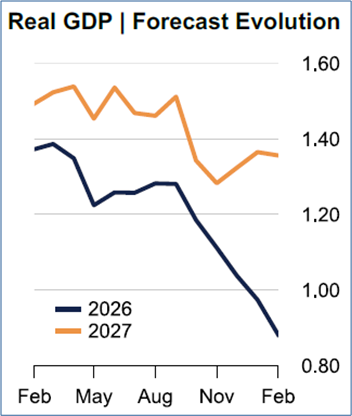

FocusEconomics: Growth forecasts have fallen this sharply

The Barcelona-based research firm “FocusEconomics” publishes monthly analyses of global economic trends. In its report “Consensus Forecast, CIS Plus Countries,” the following figure shows how sharply the forecasts of international institutes and banks (including only a few Russian ones) for Russian economic growth in 2026 and 2027 have fallen over the past 12 months.

Decline in analysts’ forecasts for growth rates in 2026 and 2027

Year-over-year increase in real gross domestic product in %

FocusEconomics: “Consensus Forecast, CIS Plus Countries,” 02/03/26

The analysts’ “consensus forecast” for growth in 2026 has fallen from 1.4 percent in the spring of 2025 to 0.9 percent today (black line). Their average growth forecast for 2027 fell from around 1.5 percent to just under 1.4 percent (orange line).

FocusEconomics comments on GDP growth in 2026:

“Our consensus assumes that GDP growth this year will remain at the 2025 level. Domestic demand is expected to slow due to declining investment activity, higher taxes, restrictive monetary policy, and fiscal consolidation. However, exports are expected to rise despite Western sanctions.”

And how is inflation developing?

Regarding the trend in consumer prices in Russia, FocusEconomics notes:

“The inflation rate fell to 5.6% in December (November: 6.6%), the lowest level since August 2023. … This year, average inflation is likely to reach a six-year low due to weaker domestic demand. Nevertheless, the VAT increase and a weakening of the ruble, which is driving up import costs, are likely to keep inflation above the Central Bank’s target of 4.0%.”

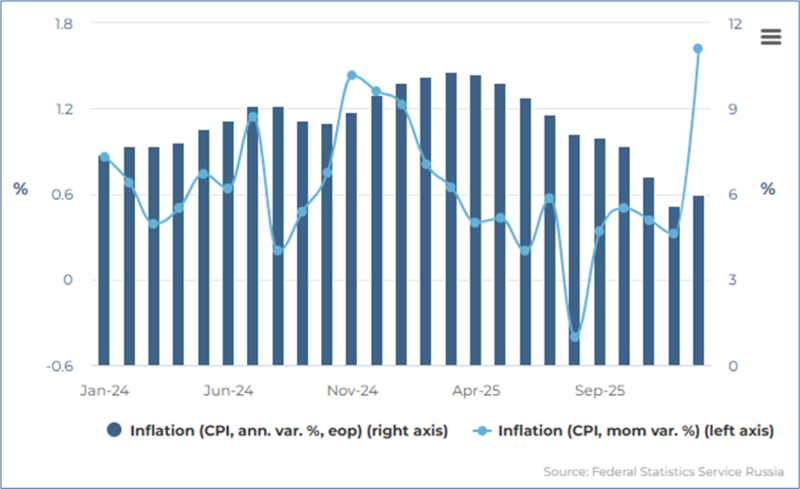

FocusEconomics also published the following chart showing the rise in the inflation rate in January 2026 to 6.0 percent compared to January 2025 (right column).

Monthly inflation trends in Russia

Bars: Year-over-year change in consumer prices in %; right scale

Blue line: Month-over-month change in consumer prices in %; left scale

FocusEconomics: Russia Inflation December 2025, Jan. 16, 2026 (with updated chart)

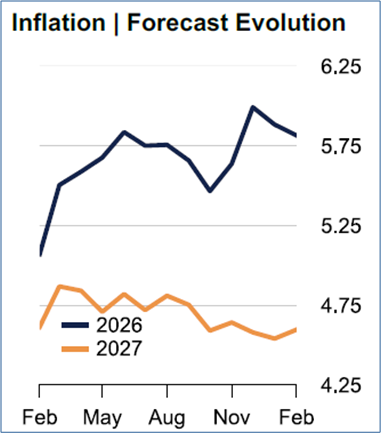

Consensus forecast: In 2026, the annual inflation rate will fall to 5.8 percent

The following figure shows how the inflation forecasts tracked by FocusEconomics have evolved since February 2025. Analysts now expect the annual average inflation rate for 2026 to fall to 5.8% (black line). That would still be about 3 percentage points lower than in 2025, when the annual inflation rate in Russia rose to 8.7%. In 2027, analysts estimate that the annual inflation rate will fall by another percentage point to 4.6% (orange line).

Trend in inflation rate forecasts (in percent)

FocusEconomics: “Consensus Forecast, CIS Plus Countries,” 02/03/26

The EBRD’s view on the Russian economy

Although Russia remains a member of the London-based “European Bank for Reconstruction and Development,” the EBRD has not invested in Russia since 2014, and its office in Moscow was closed in 2022 (“The EBRD in Russia”). In the February issue of its biannual report “Regional Economic Prospects,” the EBRD therefore provided only the following brief overview of current economic developments in Russia:

Economic growth slowed to 1.0 percent year-on-year in the period from January to September 2025. The main reason for this was robust government spending, particularly in the defense and administrative sectors. Rising military spending boosted production in the automotive and metal industries.

Real wages rose significantly last year, while the unemployment rate hit a record low of 2.1 percent.

Inflation fell to 5.6 percent year-over-year in December 2025—a five-year low.

However, as oil and gas revenues fell by a quarter in 2025, the budget deficit widened to 2.6 percent of GDP. In response, the authorities raised the VAT rate from 20 to 22 percent effective January 1, 2026, which could temporarily fuel inflation.

Real GDP growth is expected to slow to 0.8 percent in 2026 before recovering to 1.0 percent in 2027. Downside risks stem from weak oil prices and the possibility of further economic sanctions.

Was the 1 percent growth in 2025 high or low by global standards?

The EBRD also estimates Russia’s economic growth in 2025 at 1.0 percent, in line with the initial estimate from the Russian statistics agency Rosstat. The Russian online newspaper “New Izvestia” (Novye Izvestia / Новые Известия) analyzed which countries grew even more slowly, at roughly the same rate, or much more strongly. The results of this international growth comparison:

In 2025, the overall economic output of many European countries grew even more slowly than in Russia. High energy prices and U.S. trade policies dampened growth. For example, the German economy grew by only 0.2% last year, and the Austrian economy by 0.3%. Economic growth in Finland and Italy (both 0.5%) as well as in France (0.7%) was also lower than in Russia. Surprisingly, Ireland grew far more strongly than the other EU countries. According to preliminary estimates by the IMF, GDP there rose by 9.1%. One reason for this may have been that international corporations based in Ireland significantly increased their exports to the U.S. in 2025 due to the threat of U.S. tariff hikes.

GDP Growth by Country in 2025

New Izvestia; Maria Sokolova:

Better than Europe, but worse than Asia. What does Russia’s 1% GDP growth mean? 02/26/26

Growth in Russia in 2025 was roughly on par with growth in Mexico (1%) and Japan (1.1%).

Ukraine recorded roughly twice as much growth at 2%, partly because Western countries supported arms production in Ukraine. The U.S. economy also grew by 2%. GDP continued to rise much more strongly in 2025 in China (4.8%) and, above all, in India (6.6%).

In 2025, aggregate economic output also grew much more strongly than in Russia in some Central Asian countries: Tajikistan’s GDP grew by 8.4% last year, and Kyrgyzstan’s GDP by as much as 11.1%. Domestic demand in the Tajik economy was supported by remittances from “guest workers” employed in Russia. Growth momentum for the gold-rich country also came from rising gold prices and increased investment. Kyrgyzstan has developed into an important transit country for goods that are shipped on to Russia.

Consensus forecasts by the Higher School of Economics through 2032

The Economic Research Department at Moscow’s Higher School of Economics surveys Russian and foreign analysts quarterly on economic developments in Russia over the next seven years. This “consensus forecast” from the HSE Center of Development Institute also determined in mid-February that growth in the Russian economy will remain weak in 2026, falling to 0.9 percent. By 2030, it is expected to pick up gradually to around 2 percent.

Consensus Forecast 2026–2032 (Survey conducted February 12–24, 2026)

Higher School of Economics; S.V. Smirnov: The latest consensus forecast, “Survey of Independent Experts: Minor Adjustments Based on Current Data,” was published on February 25, 2026.

FAZ Commentary: The “warning signs” for the Russian economy are mounting

Katharina Wagner, economic correspondent for Russia and the CIS at the Frankfurter Allgemeine Zeitung since 2019, views the development of the Russian economy after four years of war as follows:

“Economists have become cautious when it comes to forecasting the collapse of the Russian economy. When Western sanctions were drastically tightened following the invasion of Ukraine four years ago, many predicted a collapse. Yet massive government investments in the military and defense industry led to an economic upswing in 2023 and 2024 unlike anything Russia had seen in a long time.

Above all, drone factories and tank foundries were now running at full speed. In supermarkets, Western brands were soon replaced by Russian knockoffs—Dr. Oetker became Dr. Bakers. For Russians who were not on the front lines or living in border regions, the war seemed to have mostly positive consequences.

But over the course of the past year, the situation has changed. The high interest rate, intended to combat inflation fueled by government spending, labor shortages, and sanctions, plunged many companies into crisis. Recently, complaints have been mounting from employees who have had to wait months for their pay.”

Russia’s budget deficit could be three times higher than planned by 2026

Katharina Wagner sees “warning signs” for economic development primarily in rising public budget deficits amid sharply falling revenues:

Revenues from oil and gas exports have already shrunk significantly in 2025, and they are likely to halve again in January and February. The blame lies with the sanctions, which—despite all skepticism—are having an effect and are forcing Russia to sell its oil only at additional cost and with price discounts.

Due to Donald Trump’s threats against India, China—as the last major customer—can now demand even lower prices. As a result, Russian Urals oil currently costs much less, and the ruble is significantly stronger than projected in the Russian budget. If this continues, the deficit could be about three times larger this year than the planned 1.6 percent of GDP. To plug such a large hole, up to three-quarters of the country’s remaining financial reserves in the National Welfare Fund would have to be used.

The government is trying to take more money from citizens through higher taxes and fees. But people are already starting to cut back on essentials. This is likely to harm economic growth.

Katharina Wagner’s conclusion: An “economic downturn” is not certain…

“The state of the Russian economy is more fragile than at any time since the invasion of Ukraine. Nevertheless, it is too early to predict a certain decline. Things could still turn out differently: Higher oil prices in the wake of an escalation of the conflict between Washington and Tehran could temporarily alleviate Russia’s financial problems, as could a devaluation of the ruble. And even if revenues remain low, the state still has other options—from printing money to taking on more debt and raising taxes even further, to making budget cuts.”

… but it is very likely that the “gradual decline” will continue

“It is very likely, however, that the gradual decline of the economy will continue.

Even a peace deal with the Americans would not be followed by an immediate reintegration into the global market. There are no signs of growth momentum on the horizon. The inflation rate, currently just under six percent, will remain high as long as the state pumps large amounts of money into the war.”

Recommended reading:

German-Russian Chamber of Foreign Trade:

Focus analyses, German; also Russian; (selection):

Weak growth, dwindling reserves, and high military spending, 02/18/26

Podcast “Tsars, Data, Facts” by Thomas Baier:

- From Boom to Stagnation: Russia’s Economy in 2026; Guest: Vasily Astrov, 36 min., Feb. 17, 2026;

- Low gas storage levels: Europe’s challenge in the energy market; Guest: Dr. Heiko Lohmann, “energate Gasmarkt”; 34 min., 03/01/26

Economic data and forecasts:

- CMASF, Moscow: Base-case macroeconomic forecast for 2026–2029, Feb. 27, 2026

- CMASF, Moscow: “Analysis of Macroeconomic Trends,” Feb. 27, 2026

- Finmarket.ru: Industrial production in Russia fell by 0.8% in January; 02/27/26

- Interfax.ru: Inflation in Russia stood at 0.19% from February 17 to 24, slowing to 5.8% year-over-year; February 27, 2026

- Interfax-Russia.ru: A key interest rate of 15.5% amid a noticeable slowdown in inflation still constitutes a restrictive monetary policy that curtails lending, according to the Central Bank; February 27, 2026

- Reuters; Elena Fabrichnaya and Gleb Bryanski: Russian ruble expected to fall sharply this year as oil sales decline and the deficit rises, 02/26/26

- EBRD: Growth in EBRD regions remains resilient despite continued trade tensions, 02/26/26

- Trend.at; APA: EBRD: Higher growth expected in Eastern Europe in 2026, 02/26/26

- bneIntellinews, Clare Nuttall in Glasgow: EBRD lifts growth outlook as regional economies prove resilient to trade tensions, 02/26/26

- Berliner Zeitung; Peter Steiniger: The European Bank for Reconstruction and Development (EBRD) raises its growth forecasts—despite U.S. tariff policies under President Trump, 02/26/26

- Ukraine News: The EBRD has significantly revised downward its forecast for Ukraine’s GDP growth, 02/26/26

- FAZ commentary by Katharina Wagner: Putin’s War Economy: Warning Signs for Russia’s Economy Are Mounting, 02/26/26

- bneIntellinews, Ben Aris: Russia’s finance ministry to tighten budget rule as oil revenues sink, 02/26/26

- Anadolu; Elena Teslova: Russia acknowledges 50% drop in energy revenues, insists economy remains stable. Kremlin says oil and gas income down 50%, but non-energy revenues offset losses, 02/26/2026 –

- Bank of Russia: Summary of the Key Rate Discussion released, 02/26/26;

- Bank of Russia: Commentary on the Bank of Russia’s Medium-term Forecast, February 26, 2026

- Finmarket.ru: The Russian Ministry of Economic Development will present a revised macroeconomic forecast in April, February 25, 2026

- Higher School of Economics; Development Center Institute; S.V. Smirnov: The latest consensus forecast, “Survey of Independent Experts: Minor Adjustments Based on Current Data,” has been published (survey conducted February 12–24, 2026); February 25, 2026

- Finmarket.ru: VEB expects an economic slowdown and a decline in investment, 02/25/26

- Lenta.ru; Kirill Lutsyuk: Russia is forecast to see a decline in investment and accelerating inflation. VEB: Inflation in Russia will rise to 6.2 percent by the end of the year, 02/25/26

- expert.ru; Mikhail Mishustin: Russia is developing despite external attempts to hinder it, 02/25/26

- expert.ru: Mikhail Mishustin reported that Russia’s GDP has grown by more than 10% over the past three years, 02/25/26

- Finmarket.ru: Economists estimate industrial production growth in Russia at 0.9% in January and inflation at 1.96%; Interfax survey; 02/13/26

4 Years of the War in Ukraine – Economic Aspects:

- Merkur.de; Nils Thomas Hinsberger: Four years of the war in Ukraine: Russia’s most important economic sector collapses, 02/26/26

- Inosmi.ru: Why haven’t the more than 20,000 Western sanctions destroyed the Russian economy? Die Welt: Sanctions failed because Russia was prepared for an economic conflict, 02/25/26; Die Welt+, Eduard Steiner: Why 20,000 Western sanctions did not destroy Russia’s economy; 02/25/26

- Inosmi.ru: Four years of conflict in Ukraine: an unpleasant outcome for Germany. Berliner Zeitung: EU sanctions against Russia have hit Germany the hardest. The Ukraine conflict has exposed the limits of the European sanctions strategy and exacerbated internal divisions in Germany, writes Lukas Moser in the BZ; 02/24/26

- BR24; Peter Jungblut: “Real Negative Trends”: How Much Longer Can Putin Hold Out? 02/25/26

- Moscow Times; Igor Lipsits: The economic consequences of the war: The Russian state has become unprofitable; 02/24/26

- Moscow Times; Vladislav Inozemtsev: Madness has become the norm, 02/25/26

- Moscow Times; Dmitry Nekrasov; Politician, economist, and entrepreneur, co-founder and director of the European Center for Analysis and Strategies: Russia “will not stop drinking”—or why you shouldn’t expect an economic crisis, 02/23/26

- Focus online; Christoph Sackmann: Four Years of War in Ukraine: Four Charts Show How Much the War Is Harming Russia, 02/26/26

- Business-gazeta.ru: Interview: Economist Alexey Zubets: “Russia is doomed to GDP growth of no more than 1–2 percent per year,” 02/25/26

- Meduza asks researcher Janis Kluge: Russia’s military recruitment numbers remain steady, but how long can the regions foot the bill? 02/23/26

- The Bell; Alexandra Prokopenko, research fellow at the Carnegie Berlin Center, and Alexander Kolyandr, visiting scholar at the Center for European Policy Analysis (CEPA); Irreversible Russia 2026: Seven key new features of the Russian economy that will shape it for years to come, 02/23/26

- Bob Savic, head of international trade and sanctions consulting at the Global Policy Institute, London; GIS Report: Russia’s economy faces years of low, but stable growth, 02/20/26

- Dr. Moritz Kraemer, Chief Economist / Head of Research at LBBW: Four Years of War. The West Could Bring Russia’s Economy to Its Knees, February 20, 2026

- Janis Kluge, German Institute for International and Security Affairs (SWP), in the podcast “Ostausschuss der Salonkolumnisten”: Russia’s Economy in 2026 – with Janis Kluge, 96 min., Jan. 17, 2026

German Trade with Eastern Europe 2025:

- Eastern Committee of German Business: Companies continue to focus on Eastern Europe. Trade with the East to exceed 550 billion euros in 2025. Poland consolidates its 4th place as a sales market, 02/24/26

- Berliner Zeitung; Michael Maier: German Economy: Things are going well with Poland, but there are problems with Hungary. The Eastern Committee of German Business praises Poland, criticizes Hungary, and expresses disillusionment regarding Ukraine, February 24, 2026

- Handelsblatt: German trade with Eastern Europe grows noticeably despite the war in Ukraine. Nearly one in five German exports went to Eastern Europe in 2025, 02/24/26