German research institutes and BOFIT: Russia's growth will slow to 1 percent in 2026

Author: Klaus Dormann

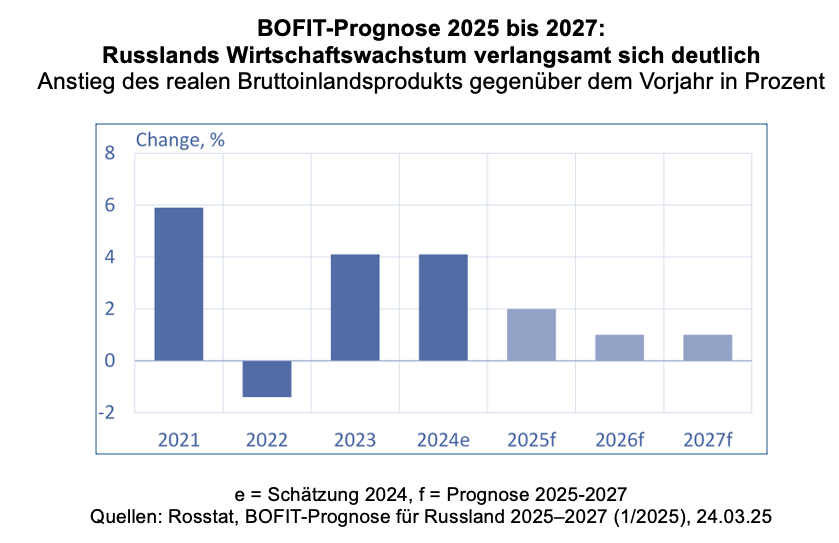

According to a new estimate by the Federal State Statistics Service (Rosstat), the Russian economy grew by 4.3 percent last year (Finmarket.ru). In 2023, Russia’s gross domestic product had already risen by 4.1 percent. Will it now take three years for it to grow by another 4 percent?

BOFIT, the “Institute for Emerging Economies” of the Finnish Central Bank, expects such a sharp slowdown in the growth of the Russian economy. The institute’s forecast: In 2025, Russia’s economic growth will halve to around 2 percent, and in 2026 and 2027, it will reach only around 1 percent in each year.

The Finnish institute’s growth forecasts for 2025 and 2026 align with the expectations of the five leading German economic research institutes. In their “Joint Economic Assessment” published on April 10 on behalf of the German government, they also assume that Russia’s economic growth will halve to 2.0 percent in 2025 and reach only 1.0 percent in 2026. The German institutes have not yet issued a forecast for 2027, a year in which BOFIT expects the growth rate to stagnate at 1.0 percent.

On average, a decline in growth to 1.5 percent is expected

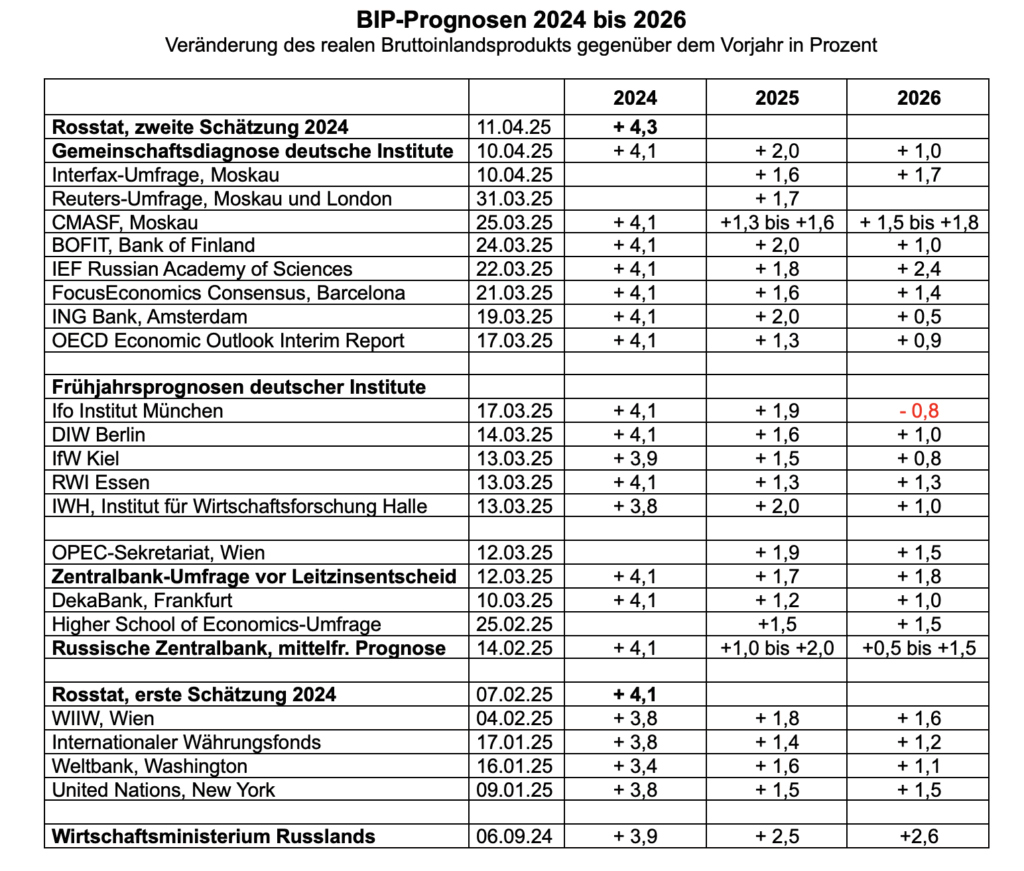

However, the vast majority of Russian and foreign analysts do not expect the Russian economy’s growth to slow to just around 1 percent in 2026. According to surveys, Russia’s economic growth is likely to stagnate at around 1.5 percent in 2025 and 2026.

For instance, in a survey conducted in early April by the Interfax news agency, analysts expected on average that the Russian economy would grow by 1.6 percent in 2025 and 1.7 percent in 2026.

The Russian Central Bank’s analyst survey conducted in early March also indicated that economic growth in Russia is unlikely to decline further in 2026. According to the Central Bank survey, GDP growth is expected to pick up slightly next year, from 1.7 to 1.8 percent.

FocusEconomics Consensus: Growth will remain below 2 percent through 2029

In contrast to the analysts in the surveys conducted by the Central Bank and the Interfax news agency, Western analysts—such as BOFIT—often consider a further slowdown in growth in 2026 to be likely. However, this slowdown is expected to remain within very narrow limits.

This is shown by the forecasts of 34 analysts (including only a few Russian ones) compiled by the Barcelona-based research firm FocusEconomics. On average, the “consensus” among analysts is that Russia’s economic growth is expected to decline only slightly from 1.6 percent in 2025 to 1.4 percent in 2026.

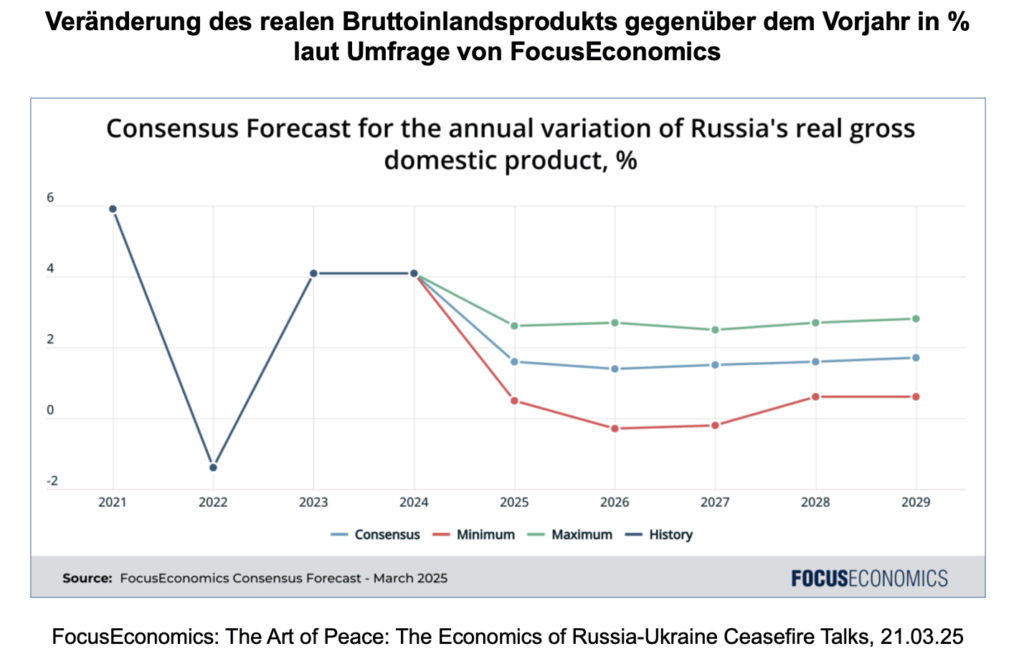

FocusEconomics solicited forecasts through 2029. As the following figure from a FocusEconomics study on the economic aspects of the talks regarding a ceasefire in Ukraine shows, Russia’s economic growth is unlikely to pick up significantly by 2029 according to the “consensus” and will remain below 2 percent (blue line).

High uncertainty: Forecasts vary widely

The uncertainty surrounding the future output trend of the Russian economy is reflected in the wide range between the lowest and highest forecasts compiled by FocusEconomics. The forecasts for 2026 diverge particularly widely. The range of forecasts for output growth next year extends from a mild recession (red line in the figure above) to growth of just under 3 percent (green line).

Some observers of the Russian economy expect the Russian economy to slide into a recession. For instance, in its “Spring Forecast” for 2026 published in mid-March, the Munich-based ifo Institute projected a 0.8 percent decline in the Russian economy’s real gross domestic product.

Professor Igor Lipsits, a co-founder of Moscow’s “Higher School of Economics” who emigrated from Russia, even described Russia’s economy in an interview with “NV – The New Voice of Ukraine” as already being “on the brink of collapse.” BOFIT, on the other hand, emphasizes that a “full-blown economic crisis” is not in sight in Russia (further details on the forecasts by BOFIT and Lipsits can be found at the end of this article).

The Institute for Economic Forecasts at the Russian Academy of Sciences is particularly optimistic about Russia’s overall economic development. The RAS’s “Institute for Economic Forecasts” (IEF) expects, much like BOFIT, that the growth in aggregate economic output will roughly halve by 2025, reaching only 1.8 percent. However, the IEF of the RAS does not anticipate a prolonged period of weak growth. Unlike BOFIT, it expects GDP growth to accelerate back to 2.4 percent as early as 2026.

Joint Assessment: The War Provided a Demand Boost to the Economy

In their “Joint Economic Forecast,” the German economic research institutes note, in retrospect, that the Russia’s “military activities” resulted in a sharp rise in government spending and increased investment in the defense industry. The sanctions-induced slump in Russian imports from Europe not only led to higher imports from China but also to an increase in domestic production.

However, private consumption in Russia has also risen, the German institutes note. This was made possible, on the one hand, by transfer payments to private households. On the other hand, immigration to Russia has declined sharply, resulting in a labor shortage and a significant rise in wages, particularly in sectors critical to the war effort. Because capacity is likely to be fully utilized, the institutes estimate that the overall economic growth rate will slow significantly. They expect growth of 2.0 percent in 2025 and 1.0 percent in 2026.

Ministry: In February, the annual GDP growth rate fell to 0.8 percent

On April 2, the Russian Ministry of Economic Development released key economic data for February. According to the ministry, real GDP growth fell to 0.8 percent in February compared to the same month last year. In January, the annual growth rate had still reached 3.0 percent. However, the ministry’s press service noted that February 2025 had one fewer working day than February of the leap year 2024. If this factor were factored out, economic growth in February would be “comparable to that in January,” according to the ministry (Finmarket.ru).

Comparing total economic output in the first two months of 2025 with output in January/February 2024, GDP grew by 1.9 percent, according to the ministry (Monocle.ru).

The comparison of January/February 2025 with January/February 2024 also shows:

Industrial production rose by 1.2%, construction output by 9.8%, and agricultural production by 1.7%.

Freight transport fell by 0.7%, and real wholesale sales fell by 2.0%.

Real retail sales rose by 3.8%.

VEB Institute: Adjusted GDP in February was barely higher than in January

Preliminary calculations by the research institute of the state-owned “Vnesheconombank” (“Bank for Foreign Economic Relations”) on the current development of aggregate economic output in February differ slightly from the Ministry’s figures. According to the VEB Institute’s GDP index published on April 11, real GDP growth in February 2025 slowed to 0.5 percent compared to the same month a year earlier. In January, GDP had been 3.4 percent higher than a year earlier.

According to the VEB Institute, seasonally and calendar-adjusted GDP in February 2025 was 0.1 percent higher than in January 2025, after falling by 0.7 percent in January compared to December (see also the report by RBC.ru featuring contributions from Russian experts on the question of whether the Russian economy is stagnating).

Central Bank: The economic slowdown has likely begun

Shortly before the release of the February data, the Russian Central Bank published a summary of the discussion by its Board of Directors during the last key interest rate decision on March 21. It states that the “overheating” of the Russian economy likely began to ease in the first quarter of 2025. Current inflationary pressures are easing, growth in domestic demand is slowing, and there are signs of easing in the labor market. However, it is still too early to speak of a sustained reduction in the economy’s overheating. It cannot yet be said that the pace of cooling is sufficient to bring inflation back to the Central Bank’s target rate of 4% in 2026 (Finmarket.ru).

On February 14, the Central Bank raised its forecast for Russia’s GDP growth in 2025 from 0.5–1.5% to 1.0–2.0%. At the same time, it lowered its growth forecast for 2026 from 1.0–2.0% to 0.5–1.5%.

S&P Global Survey Signals Decline in Business Activity

Surveys of Russian companies conducted in March by the global research firm S&P Global to determine the “Purchasing Managers’ Indexes” point to a noticeable slowdown in business activity in the Russian economy’s industrial sector.

The “Purchasing Managers’ Index” (PMI) for manufacturing companies fell below the critical threshold of 50 index points in March. It dropped from 50.2 points in February to 48.2 points in March. The main reason for this was a decline in new orders. Both domestic and foreign demand declined (Finmarket.ru). According to “S&P Global,” falling below the “growth threshold” of 50 index points signals a decline in manufacturing output compared to the previous month. Despite the decline in new orders, however, companies remained optimistic about their production outlook for the next twelve months. They continued to hire new employees in March.

The PMI in the services sector remained just above the “growth threshold” in March. It fell from 50.5 index points in February to 50.1 index points.

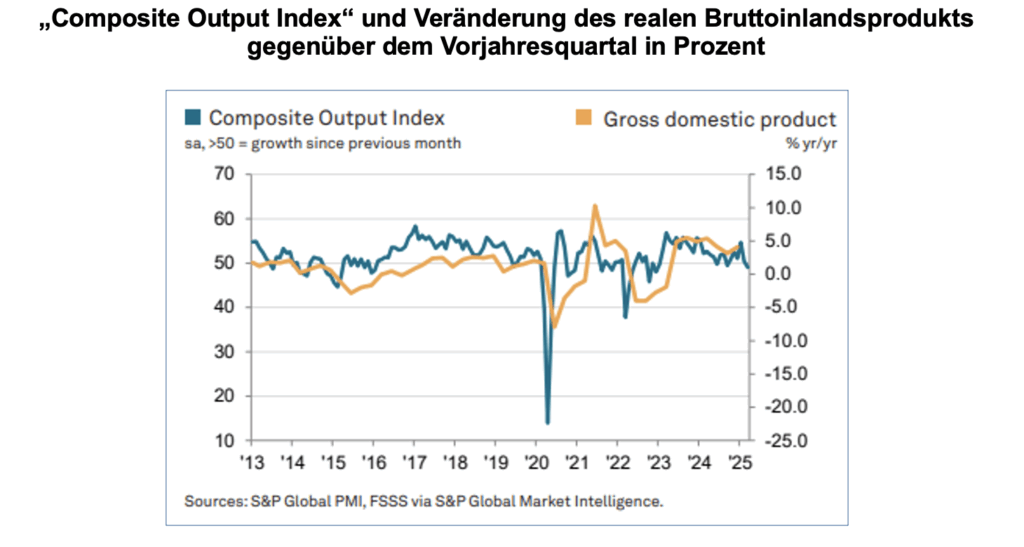

The combined index for industry and services, the “Composite Output Index,” fell from 50.4 index points in February to 49.1 index points in March. The following figure compares the trend of the “Composite Output Index” (blue line) with the annual rate of change in quarterly real gross domestic product (orange line). The figure shows that a significant decline in the “Composite Output Index” below 50 index points (left scale) is typically followed by a period of year-over-year decline in quarterly real gross domestic product figures (right scale).

S&P Global: S&P Global Russia Services PMI, Russia Composite PMI, April 3, 2025

Real incomes have risen sharply since 2023

The strong growth of the Russian economy over the past two years has also led to a sharp rise in incomes. Average real wages rose by 8.2 percent year-over-year in 2023 and by 9.1 percent in 2024. In January 2025, they were 6.5 percent higher than a year earlier (Finmarket.ru).

In his report on the government’s work in 2024 to the State Duma on March 26, Russian Prime Minister Mikhail Mishustin (video with German translation), he noted, among other things, that the population’s real incomes had risen by 8.5 percent in 2024 (Lenta.ru, TASS). According to Rosstat, they had risen by 5.8 percent in 2023, following a 1 percent decline in 2022 (Finmarket.ru).

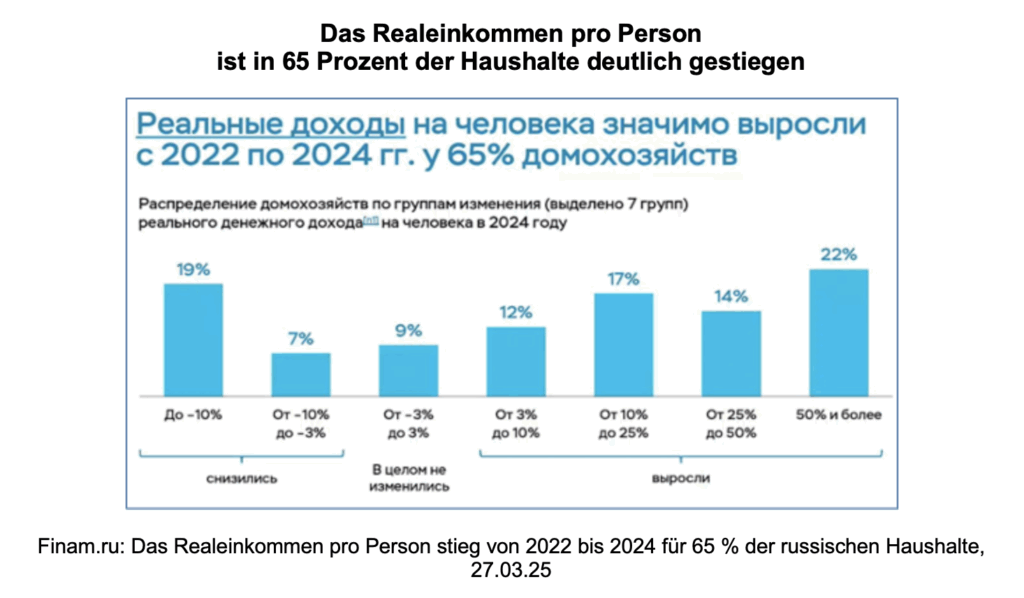

In 43 out of 100 households, real incomes are at least 10% higher than in 2023

The Russian Central Bank published further data on the development of real incomes at the end of March in its report on the results of its “All-Russian Household Survey on Consumer Finances” for the year 2024. The following figure provides information on changes in real income per person in a two-year comparison of 2024 and 2022. The Central Bank determined the proportions of households in which real income fell, remained largely unchanged, and rose significantly.

The first blue bar on the left side of the figure shows that in 19 percent of households, real income per person fell by more than 10 percent. In 7 percent of households, it fell by 3 to 10 percent compared to 2024/2022.

In 9 percent of households, the rate of change in real income ranged from –3 percent to +3 percent.

In 65 percent of private households, real income per person rose by at least three percent; in 43 percent of households, it rose by at least 10 percent:

In 12% of households, they rose by 3 to 10%,

in 17% of households by 10 to 25%,

in 14% of households by 25 to 50%,

and in 22% of households by 50% or more.

Alexey Zabotkin, Deputy Chairman of the Russian Central Bank, explained the survey results in a presentation (video: press conference on March 28, 2025).

Andrei Yakovlev: Well-above-average wage increases for soldiers

Andrei Yakovlev (Associate at the Harvard University Davis Center & visiting research fellow at the Excellence Cluster “Contestations of the Liberal Script (SCRIPTS)” at Freie Universität Berlin) pointed out in a commentary in the Russia Analyses at the end of February that the rise in real wages in Russia in 2023 and 2024 merely reflects “the average temperature in the hospital.” Rosstat reports average figures. These figures are composed of the increased incomes of the families of mobilized soldiers and professional soldiers (with increases of three to four times) and “the lack of an increase in the incomes of doctors, teachers, retirees, and many employees in the private sector.” Their salaries and wages have not been able to keep pace with those in the defense industry (see also the commentary by Konstantin Ordov, Director of the School of Finance at Plekhanov University of Economics, on Prime Minister Mishustin’s annual report in russland.capital).

At the same time, however, Yakovlev, who worked at the Moscow Higher School of Economics (HSE) from 1993 to 2023, believes that none of this means Russia’s economy will “collapse tomorrow or the day after.” However, he says it faces a prolonged period of stagnation.

Reuters Survey: Russia’s Inflation to Drop to 6.8 Percent by End of 2025, Ruble Appreciation to Fade by End of September

In a Reuters survey of 18 participants published at the end of March, analysts predicted on average that the central bank would leave its key interest rate at 21 percent on April 25. Some analysts do not expect interest rate cuts to begin until the second half of the year. On average for the second quarter of 2025, analysts expect a key interest rate of 20 percent. Their forecast for the annual increase in consumer prices in December 2025 fell from 7.0 to 6.8 percent.

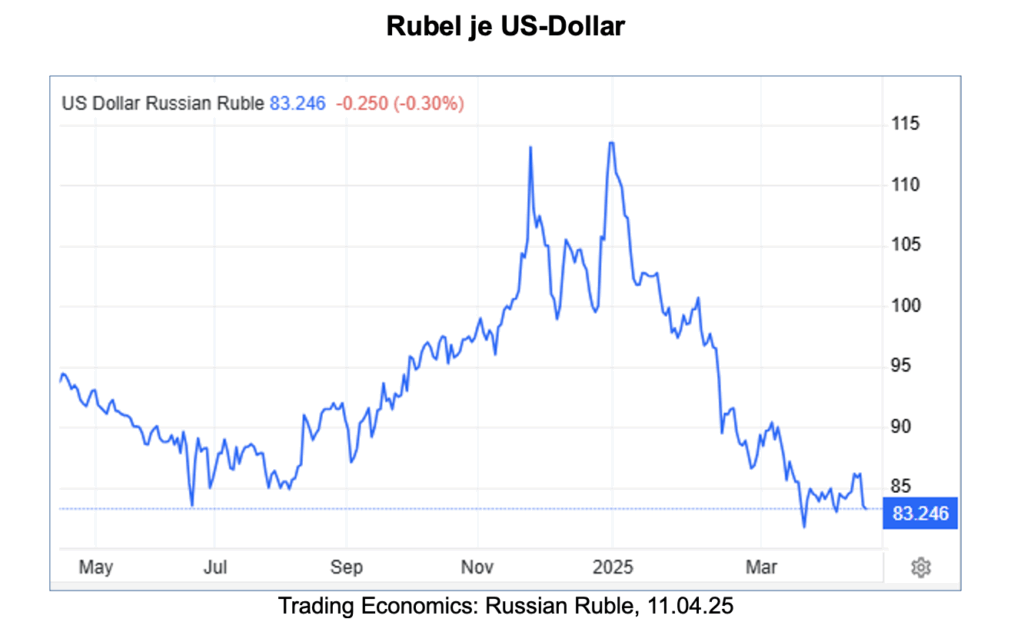

According to analysts, the Russian ruble is likely to fall back to a level of around 100 rubles per U.S. dollar in a year’s time, following its sharp rise since the start of the year. Since the beginning of 2025, the ruble has appreciated by about a quarter against the dollar.

According to Reuters, the ruble is currently about 12 percent stronger than assumed in the budget. An unexpectedly strong ruble could, according to Reuters, widen Russia’s budget deficit in 2025 and force the government to borrow more than planned. Reuters cites, above all, the expectation that a reduction in geopolitical tensions is possible following the resumption of talks between the U.S. and Russia as the main reason for the ruble’s rise. Analysts expect the ruble to fall from its current level of about 85 rubles per U.S. dollar to 97 rubles per U.S. dollar by the end of September.

BOFIT: The growth effects of budget spending are weakening

In its weekly report “BOFIT Weekly,” the BOFIT research institute of the Bank of Finland highlights in a summary of its Russia forecast that Russia’s economic growth in recent years has been achieved primarily through sharp increases in government spending, particularly to finance the costs of the war. Although the government is planning another significant increase in budget spending this year, it must expect the growth effects of this spending to diminish because the Russian economy is already suffering from an acute labor shortage and capacity constraints in many sectors.

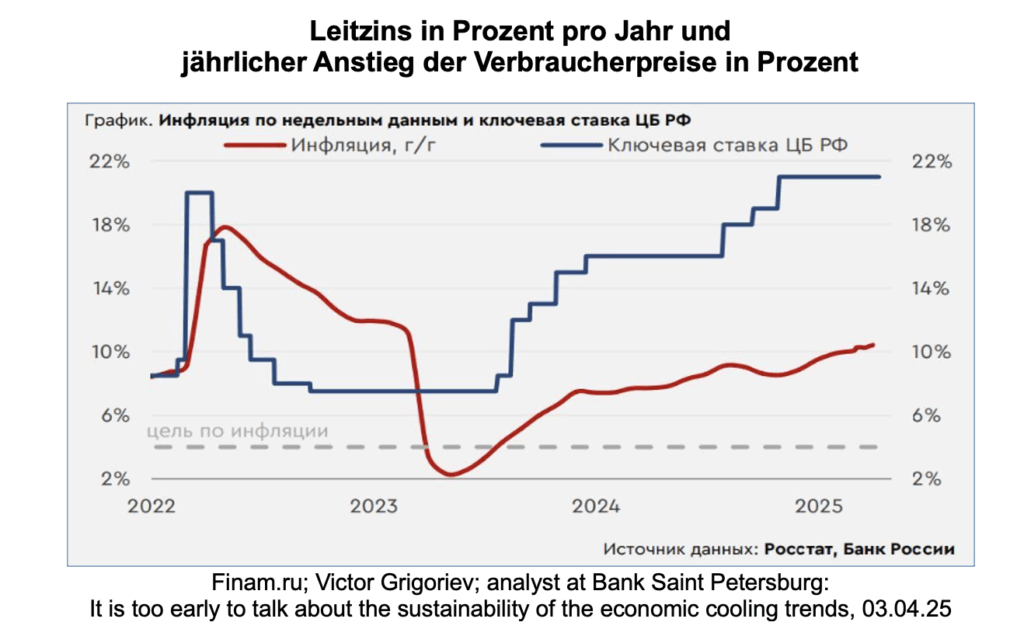

The annual inflation rate rose to 10.3 percent in March

BOFIT notes: “Inflation has accelerated, and consumer prices rose by 10% year-over-year in January and February. The Russian Central Bank was also forced to raise its key interest rate to a historic high of 21% last fall to curb inflation.”

However, the annual rate of consumer price inflation has not yet declined. On April 3, Bank Saint Petersburg noted that the annual inflation rate rose to 10.3 percent in the last week of March (see the red line in the following chart on Finam.ru).

According to Rosstat, the annual inflation rate also rose to 10.3 percent for the entire month of March (TradingEconomics). Despite the key interest rate hike to 21 percent in October 2024 (see dark blue line), the year-over-year price increase has thus risen by 1.8 percentage points since October 2024. In the Interfax analyst survey conducted in early April, participants expected the annual inflation rate to reach 7.9 percent by December 2025 (Finmarket.ru).

However, the month-over-month increase in the consumer price index has been declining since January 2025. Central Bank Governor Elvira Nabiullina emphasized this in a speech to the Duma (Finam.ru). In March, the month-over-month price increase fell to 0.65 percent (Finmarket.ru).

Investment and private consumption are growing more slowly in Russia

BOFIT expects private-sector demand in Russia to weaken due to high inflation and high interest rates.

In particular, the outlook for private-sector investment is “weak.” Investment opportunities are being constrained by rising borrowing costs, rising labor and material costs, and tax hikes. Corporate profits are declining.

BOFIT also estimates that growth in private consumption is likely to slow significantly. Wage growth is weakening, and high inflation is eroding purchasing power.

Russia can continue to finance its budget deficits

Regarding the development of public finances, BOFIT notes that strong growth in government spending during the war in Ukraine has pushed Russian public finances into deficit. Since the start of the war, deficits have reached around 2 percent of GDP per year.

According to BOFIT, current budget planning calls for a reduction of the annual deficit to around 1 percent of GDP between 2025 and 2027. However, this plan is based on “rather optimistic assumptions.” The deficit could therefore turn out to be higher than planned once again.

According to BOFIT, the government budget deficits are likely to persist over the forecast period. However, Russia still has options for financing these deficits. The government plans to cover the deficits through increased borrowing on the domestic market.

BOFIT notes that Russia’s national debt is relatively low at around 20 percent of gross domestic product (see also the Focus Analysis “Russian National Debt” by the German-Russian Chamber of Foreign Trade).

According to BOFIT, Russia’s “National Wealth Fund” still holds liquid assets amounting to nearly 2 percent of GDP. However, two-thirds of the fund’s liquid assets have since been depleted due to the war.

BOFIT: A “full-blown economic crisis” is not currently in sight

In conclusion, the research institute of the Finnish central bank emphasizes that while it expects a “significant slowdown” in the growth of the Russian economy, However, a “full-blown economic crisis” is not currently in sight in Russia. Despite weaker growth, Russia can continue to produce what is needed for the war.

Igor Lipsits: A catastrophe in the Russian economy is inevitable

Igor Lipsits, a former professor at the Higher School of Economics who emigrated from Russia, views Russia’s economy as being in a much more critical state than BOFIT does. In an interview with Mikhail Khodorkovsky’s YouTube channel, he even stated that a “catastrophe” for the Russian economy is inevitable. This is reported by the Ukrainian “Odessa Journal.”

Russia will be at a crossroads in 2025, says Lipsits. Either it will end the war and somehow return to a peaceful life, or it will find itself in a situation from which there is no turning back, only total destruction.

Lipsits believes it is clear that the Russian economy can no longer grow solely through arms production. It faces very serious financial problems. The ruble has gained strength, which is a blow to the state budget.

In a detailed three-part interview with the Ukrainian online magazine “The New Voice of Ukraine,” Lipsits also stated that Russia’s economy is “on the brink of collapse.” Russia’s official statistics were already “questionable” before the war; today, they are “downright manipulated.”

For years, the government had pumped enormous sums—about $180 to $200 billion per year—into the economy, particularly into the military-industrial complex. This spending policy initially gave the appearance of economic growth. At the same time, however, it also destroyed civilian industry.

Russia’s economy is being flooded with money. But there aren’t enough

goods to absorb it, according to Lipsits. Imports are shrinking and domestic production is collapsing.

To curb inflation, the government has raised deposit interest rates, temporarily tying up the money in bank accounts. But if interest rates were to fall, these savings would flood the market all at once and trigger hyperinflation, Lipsits warns.