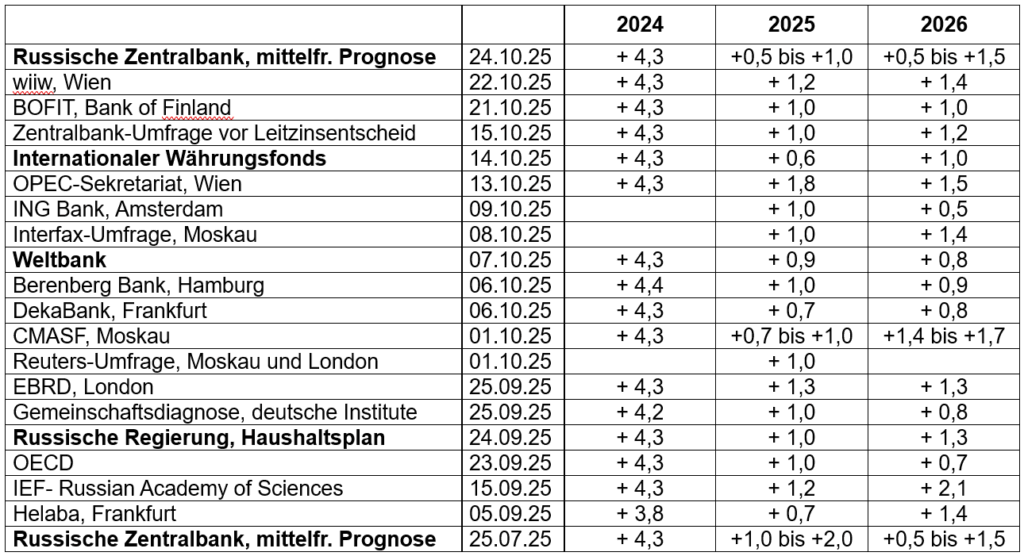

Forecasts by the Russian Central Bank

Author: Klaus Dormann

On the occasion of its key interest rate decision last Friday, the Russian Central Bank updated its “Medium-Term Forecast” for the development of the Russian economy. It no longer expects Russia to achieve real GDP growth of between +1.0% and +2.0% in 2025. According to the new forecast, the economy will grow by only +0.5% to +1.0% this year.

At the upper end of this narrowed forecast range from the Central Bank lies the Russian government’s forecast for Russia’s growth this year (+1.0%). The range of +0.5% to +1.0% also covers, among others, the forecasts of the World Bank and the International Monetary Fund. The World Bank recently lowered its forecast for this year’s growth in Russia to +0.9%, and the IMF to +0.6%.

The Central Bank is maintaining its forecast range for Russian economic growth next year at +0.5% to +1.5%. Almost all forecasts from international economic organizations, banks, and research institutes for 2026 fall within this range.

GDP Forecasts 2024–2026

Year-over-year change in real gross domestic product, in percent

Criticism of the Central Bank’s restrictive monetary policy persists

Given the numerous forecasts that the Russian economy is likely to grow by only around 1 percent or even slightly less in 2025, and that GDP growth next year is expected to be barely higher, many analysts and representatives of the Russian business community are calling for a significant cut in key interest rates. One day before the latest key interest rate decision, Sberbank CEO German Gref said it had been a mistake to focus too much on inflation while neglecting economic growth. “This year, growth will likely be around 0.8 percent, and may God grant us the same figures next year,” Gref said, according to Interfax, at a meeting of the Presidential Council for Population and Family Policy (Politico.eu; Cash.ch; Capital+; Bernd Ziesemer: Putin’s Banker: Cracks in the Leadership).

The Central Bank Slowed the Pace of “Monetary Easing”

Despite calls for a rapid easing of its monetary policy, the Central Bank lowered its key interest rate last Friday by only half a percentage point to 16.5 percent. In her statement on the key interest rate decision, Central Bank President Elvira Nabiullina noted that “significant pro-inflationary risks” had emerged. These risks are primarily linked to the rise in the budget deficit in 2025 and increased fuel prices. While the approved tax increases would help reduce inflation in the medium term, they would lead to a one-time price spike in the short term. For this reason, the central bank has “slowed the pace of easing its monetary policy.” To bring the inflation rate back down to 4%, higher key interest rates are needed than the Central Bank had previously anticipated.

Nabiullina continues to view the Russian economy as being in a “phase of economic overheating.” However, last year’s severe overheating is gradually subsiding. Demand growth is slowing while companies simultaneously expand their production capacities. The Central Bank estimates that the phase of overheating will end in the first half of 2026.

Central Bank: Current Trends in Production, the Labor Market, and Prices

In its press release on the key interest rate decision, the Central Bank assesses the current trends in Russian economic production, the labor market situation, and price developments as follows:

The rise in production in the Russian economy continues to deviate upward from a “balanced growth path.” However, high-frequency data and survey indicators point to a slowdown in overall economic growth in the third quarter of 2025. Export-oriented sectors are experiencing a significant “cooling off” in production growth. Domestic demand, on the other hand, is being supported by rising household incomes and higher public spending. Growth in consumer demand has accelerated somewhat.

The labor market remains tight. While wages are rising more slowly than in 2024, their growth continues to outpace the rise in labor productivity. Unemployment is at a record low. However, surveys indicate that the share of companies reporting labor shortages is gradually declining.

The annual inflation rate stood at 8.2% on October 20. It is expected to fall to between 6.5% and 7.0% by the end of 2025. The seasonally adjusted inflation rate, extrapolated to an annual rate, fell to 4.4 percent in the second quarter of 2025. In the third quarter, however, it rose again to 6.4 percent. This acceleration in price increases was largely influenced by one-time factors. These include higher fuel prices and an above-average rise in fruit and vegetable prices during the fall months.

According to the central bank’s assessment, current inflationary pressures will temporarily increase in late 2025 and early 2026. It expects inflation expectations to rise in light of the upcoming value-added tax increase in early 2026.

The central bank’s inflation forecasts have risen slightly

According to the central bank’s new forecast, the annual inflation rate will still reach +6.5% to +7.0% in December 2025. Previously, the central bank had also considered a decline in the inflation rate to 6.0% by the end of this year to be possible (July forecast: +6.0% to +7.0%).

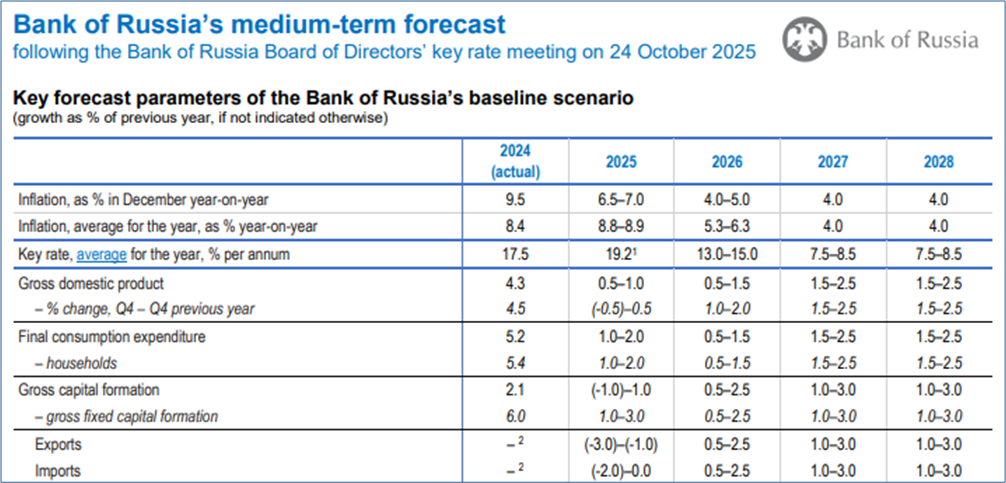

According to the new forecast, the rate of price increase will fall to +4.0% to +5.0% by December 2026 (see the first line of the following excerpt from the central bank’s new forecast). Previously, the central bank had forecast that it would reach its inflation target of +4.0 percent by the end of next year. It justifies the expansion of its inflation forecast to a range of +4.0 to +5.0 percent by citing “one-off pro-inflationary factors.” In 2027 and beyond, the central bank estimates that annual inflation will remain within the “target range of 4.0 percent.”

In its press release, the central bank reaffirms that it will make its monetary policy as restrictive as necessary to bring the inflation rate down to the target rate of 4.0 percent. In the baseline scenario, this implies that the average policy rate will be kept in the range of 13.0 to 15.0% in 2026 (see third line). According to the Central Bank, there will be “a long period of restrictive monetary policy.”

Medium-term forecast of the Russian Central Bank dated Oct. 24, 2025

Russian Central Bank: Bank of Russia’s medium-term forecast, October 24, 2025; (excerpt)

The central bank also lowered its GDP forecast for the fourth quarter of 2025

According to the new forecast, real gross domestic product will grow by only +0.5% to +1.0% for the full year 2025 (see fourth row of the table above). The Central Bank now considers it possible that aggregate economic output in the fourth quarter of 2025 will be 0.5 percent lower than in the same quarter of the previous year, when output rose sharply. The central bank revised its GDP forecast range for the fourth quarter of 2025 downward by 0.5 percentage points to a range of -0.5% to +0.5% (fifth row). Previously, it had expected aggregate economic output in the fourth quarter of 2025 to at least remain flat compared to the same quarter of the previous year.

The prospect of a decline in gross domestic product in the current fourth quarter of 2025 compared to the same quarter of the previous year is likely to intensify criticism of the central bank’s monetary policy. President Putin also weighed in on the controversial discussion regarding the consequences of restrictive monetary policy at the Valdai Forum in early October. He supported the Central Bank. A Focus Analysis by the German-Russian Chamber of Foreign Trade quotes him as saying:

“…as early as the end of last year, we said: Yes, to combat inflation, we must sacrifice such record growth rates. And the Central Bank raised the key interest rate, which is affecting the entire economy. I hope this doesn’t freeze the economy again. We will take measures that involve a forced slowdown. We will sacrifice these growth rates to restore the macroeconomic indicators that are crucial to the overall health of the economy.”

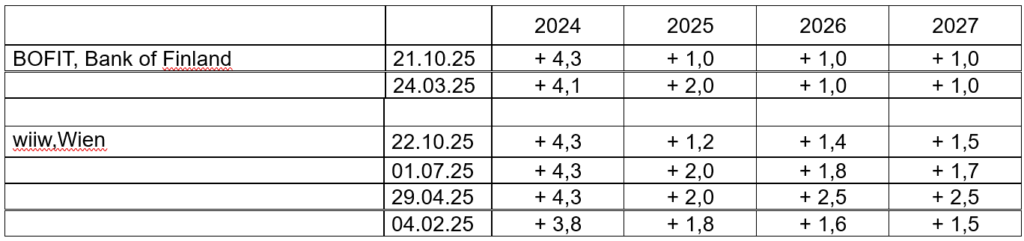

BOFIT expects only about 1 percent growth each year from 2025 to 2027

Two well-known Western research institutes, which publish forecasts on the Russian economy several times a year, have also significantly lowered their expectations for Russian economic growth in the past week.

BOFIT, the Finnish Central Bank’s research institute for “Emerging Economies,” publishes forecasts for Russia’s economic growth roughly every six months, rounded to whole percentage points. The institute has now halved its growth forecast for 2025, published at the end of March, from around 2 percent to around 1 percent. It also expects the Russian economy to grow by only around 1 percent in each of the next two years (Further details on the new BOFIT forecast can be found at the end of this article).

Comparison

of GDP forecasts for Russia by BOFIT and wiiw Year-over-year change in real gross domestic product, in percent

wiiw: Russia’s growth will only pick up to +1.5 percent by 2027

The wiiw, the “Vienna Institute for International Economic Comparisons,” publishes detailed forecasts for Russia on a quarterly basis. The institute now expects slightly stronger growth than BOFIT. The wiiw forecasts a slow recovery in the growth rate from +1.2 percent in 2025 to +1.5 percent in 2027 (press release).

Six months ago, at the end of April, the wiiw had raised its growth forecast for 2025 to +2.0 percent, thus forecasting growth in Russia at the same level as BOFIT at that time. In early July, it maintained its 2 percent forecast for 2025.

In early July, the wiiw lowered its growth forecast for 2026 from +2.5% to +1.8%. Now, the Vienna-based institute expects growth next year to be only about half as strong (+1.4%) as it did at the end of April (+2.5%).

For 2027, the wiiw expects a slight acceleration in growth in Russia to +1.5 percent. BOFIT, on the other hand, anticipates persistently weaker growth of just +1.0 percent throughout the entire forecast period up to and including 2027.

wiiw: “Russia’s Economy on the Brink of Near-Stagnation” – “Monetary Policy Too Restrictive”

After two good years, Russia is heading toward “near-stagnation,” according to the wiiw press release. This year, the economy is expected to grow by only 1.2% (2024: +4.3%). The press release notes that the forecast from early July has been revised downward by 0.8 percentage points. According to Vasily Astrov, a Russia expert at wiiw, the Russian Central Bank in particular has “stifled” the economy:

“The main reason for the slump in growth is the Russian Central Bank’s overly restrictive monetary policy. While it has significantly reduced inflation, it has simultaneously stifled the economy because this made loans unaffordable.”

The government’s austerity measures also play a role, as it must curb a budget deficit that is high by Russian standards. “Declining government spending and tax hikes will naturally also slow growth,” explains Astrov.

Thanks to the “extremely restrictive monetary policy,” inflation has largely been brought under control, according to the wiiw’s “Country Overview Russia.” However, this success has been accompanied by a weakening of domestic demand.

Vasily Astrov told Newsweek that a drastic cut in the key interest rate of four to five percentage points in the coming months could help stimulate growth. However, he said the likelihood of this happening is low. The central bank currently appears to be more concerned about a possible rise in inflation than about stagnation. So if the key interest rate is lowered, it will likely not be by much, Astrov surmises.

Growth will accelerate only slightly in 2026 and 2027

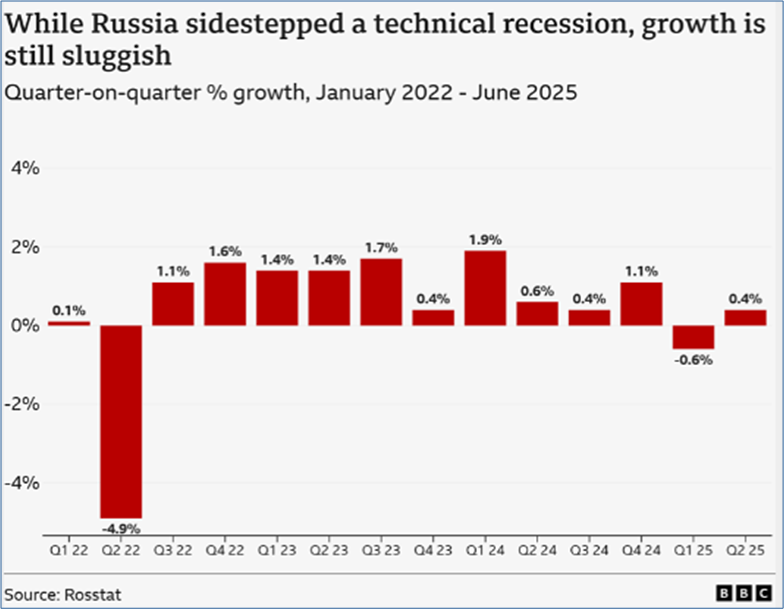

In its press release, the wiiw notes that Russia narrowly avoided a “technical recession” (a decline in GDP over two consecutive quarters) in the first and second quarters of this year. In a very informative “explainer,” the BBC published the following chart:

While Russia avoided a technical recession,

growth remains sluggish

Quarter-over-quarter growth in percent

Q1 2022 to Q2 2025 BBC

Explainer, Evgeny Pudovkin: Why is Russia’s economy slowing down? 09/23/25

According to the wiiw, industrial production rose by just +0.8% in the first eight months of the year, driven almost exclusively by the still-booming defense industry.

In 2026 and 2027, economic growth is expected to accelerate slightly, according to the wiiw, reaching +1.4% and +1.5%, respectively. Further easing of monetary policy is expected to support consumption.

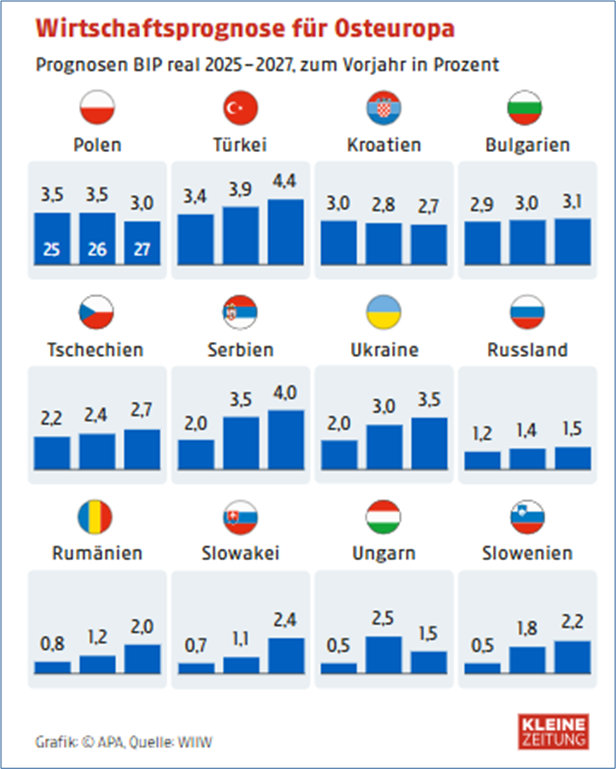

In 2027, Russia will slip to the bottom of the growth rankings in Eastern Europe

According to the wiiw forecast, only a few countries in Central, Eastern, and Southeastern Europe will grow as weakly as Russia between 2025 and 2027. This is shown in the following APA chart. In 2027, with the exception of Hungary, all of the comparable countries shown in the chart in Eastern Europe are expected to grow faster than Russia, with growth of +1.5 percent.

Kleine Zeitung: Central and Eastern Europe is growing significantly faster than the Eurozone, 10/22/25

The wiiw forecasts were discussed on Ö1’s Mittagsjournal by wiiw Director Mario Holzner.

Russia lacks investment in new machinery and labor

Russia expert Vasily Astrov emphasizes in the press release:

“New growth would require investments in greater productivity. However, these are stagnating. Investments in new machinery and equipment—which are normally the biggest drivers of modernization and productivity gains—have stabilized at the relatively low pre-war level of 2021.”

The wiiw points out that the Russian economy is operating at full capacity in many sectors. The unemployment rate is expected to fall to a record low of 2.3 percent in 2025.

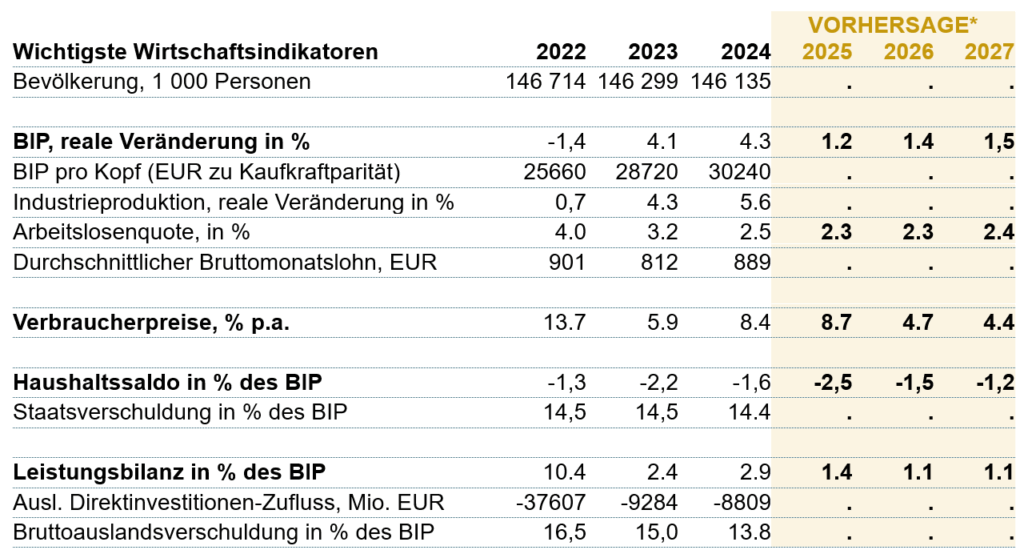

Key economic indicators with forecasts for 2025 to 2027

wiiw: Country Overview Russia, Oct. 22, 2025

Annual price inflation is expected to accelerate slightly in 2025

According to the wiiw forecast, the consumer price index is expected to rise by an annual average of +8.7 percent in 2025, which is still slightly higher than in 2024 (+8.4 percent).

However, the current week-over-week increase in consumer prices, extrapolated to an annual rate, has now fallen to around 4%, according to wiiw. This prompted the central bank to lower the key interest rate slightly further. At 17%, it remains at a very high level. Further rate cuts are foreseeable, according to wiiw (shortly before the key interest rate was cut to 16.5 percent).

Taxes are being raised due to the sharp rise in the budget deficit

The wiiw comments on fiscal developments as follows:

In 2025, Russia will post a budget deficit of 2.5% of GDP, the largest since the COVID-19 pandemic. The government can only borrow domestically. Since interest rates are high, it must cut spending and increase revenue.

Taxes on corporate profits and personal income have already been raised.

In 2026, the value-added tax will also be increased.

In addition, military spending is to be cut by 6 billion euros, or 0.3 percentage points of GDP.

BOFIT cuts its growth forecast for 2025 in half again

The BOFIT research institute of the Bank of Finland has lowered its forecast for Russian economic growth in 2025 even more sharply than the wiiw. At the end of March, BOFIT had still expected Russia’s gross domestic product to “only” halve this year, from just over 4 percent to 2 percent. It had projected that growth would slow to just around 1 percent starting in 2026.

Now, BOFIT expects economic growth to fall to “at most” 1 percent as early as this year. Furthermore, it is expected to remain this weak in 2026 and 2027 as well (barring any significant changes in Russian domestic policy or “external shocks”).

BOFIT Weekly: New Sanctions Hamper Russia’s Exports

In its weekly report dated October 24, BOFIT summarizes its assessment of the impact of the new sanctions imposed by the U.S., the U.K., and the EU on the Russian economy as follows:

The US and the UK have added Russia’s largest oil company, the state-owned Rosneft, and the private company Lukoil to their sanctions lists. Together with the existing sanctions, Russia’s four largest oil producers are now subject to US and UK sanctions. They account for around 80 percent of Russian oil production.

The EU has adopted its 19th sanctions package. Rosneft and another major oil company, Gazpromneft, are now also being added to the EU’s sanctions list. The EU is also imposing a complete ban on imports of liquefied natural gas (LNG) from Russia starting in early 2027. An additional 117 so-called “shadow ships” used to transport sanctioned Russian oil have been added to the EU sanctions list. Efforts to prevent the circumvention of sanctions are also being strengthened by adding more banks operating in Russia and other countries to the sanctions list.

The new sanctions are likely to further hamper Russia’s exports. The sanctions are expected to lead to a decline in government budget revenues. This year, revenues from oil and gas trade accounted for about a quarter of Russia’s government revenues.

BOFIT: Defense and internal security spending are supporting demand

In its new Russia forecast, the Finnish Central Bank’s research institute highlights the following two developments:

- Public spending is supporting domestic demand, particularly production in “war-related” sectors.

- Growth in other economic sectors is being held back by labor shortages and tighter credit restrictions.

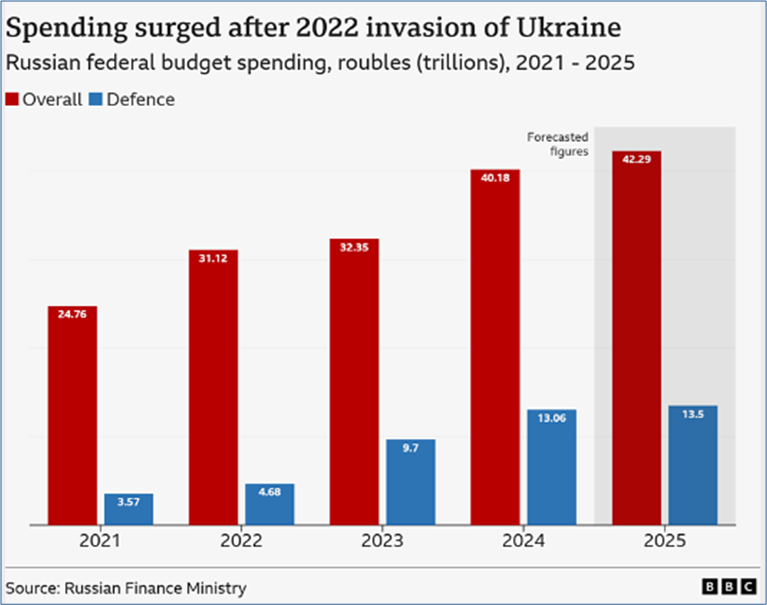

According to BOFIT, financing the war of aggression against Ukraine has led to an average nominal growth in consolidated budget expenditures of around 17% per year over the past three years. In this year’s federal budget, spending on “defense” and “internal security” together would have accounted for over 40% of total spending.

According to the BBC Explainer, defense spending planned for 2025 alone accounts for about 32 percent of total spending in the 2025 federal budget.

Russian Federation Budget 2021–2025

Total Expenditures (red bars) and Defense Expenditures (blue bars) in Trillions of Rubles

BBC Explainer, Evgeny Pudovkin: Why is Russia’s economy slowing down? 09/23/25

BOFIT considers it “highly unlikely” that spending on defense and internal security can be cut during the 2025–2027 forecast period. The macroeconomic significance of the development of the “military-industrial complex” is unlikely to diminish. BOFIT states:

“While it is becoming more difficult to channel economic resources into sectors critical to the war effort, it is still possible. A prolonged hiatus in military activities would provide the Russian economy with a welcome respite, but the significant role of the military-industrial complex is unlikely to diminish in the foreseeable future.”

Rising budget deficit, but still relatively low public debt

Regarding the development of public finances, BOFIT notes:

Despite tax increases, public sector revenues have lagged behind expenditures, leading to a rise in the deficit. So far, the deficit has been covered by withdrawals from the National Welfare Fund and the issuance of domestic government bonds.

At around 13% of GDP, Russia’s public debt remains at a relatively low level by international standards. The majority of public debt is denominated in rubles, and a significant portion of it is held on the balance sheets of domestic banks.

Foreign investors are effectively barred from Russian bond markets by sanctions. This makes borrowing more expensive and difficult for the Russian government. Public budget deficits and government debt are expected to remain at this year’s levels throughout the forecast period. Under this assumption, further tax increases will be necessary to finance public spending.

Growth in private consumption is slowing to around 1 percent

BOFIT also points out that the prospects for growth in private household consumption and for an increase in investment are very limited.

Regarding the development of private consumption, BOFIT points to the following trends in wages, other income, and private borrowing:

The war has increased demand for labor and led to a rapid rise in average wages. Nationwide, wage growth outpaced consumer price inflation. Unemployment fell to a record low. Remarkably, according to surveys, most Russian households feel better off financially than they did before the invasion of Ukraine in 2022.

Rising wage income and household borrowing have supported retail sales and demand for many domestic services. As traveling abroad has become more difficult for most Russians, the domestic hospitality sector has seen strong growth, partly thanks to government subsidies.

Looking ahead, however, BOFIT expects a significant slowdown in private consumption growth. As economic growth slows, real wage growth is likely to level off. On the other hand, falling inflation is supporting real wage growth. BOFIT does not expect real incomes to decline. However, the rise in incomes will slow significantly.

According to BOFIT, private borrowing has also slowed. This was driven by the significant cuts to government-subsidized housing loans in 2024 and extremely high interest rates.

Overall, BOFIT expects growth in private consumption in Russia to slow significantly to about +1% per year.

Strong growth in fixed investment is also slowing

BOFIT notes that the strong growth in fixed investment in recent years has contributed significantly to the growth of the Russian economy.

Rising domestic demand, the significant decline in import competition

, and rising corporate profits have encouraged companies to expand their production capacities.

These investments were largely financed from the companies’ own funds or with loans from Russian banks. In addition, funds from the National Welfare Fund were used to finance strategically important infrastructure projects. Industries critical to the war effort also benefited from government subsidies.

Regarding the strong growth in investment to date, however, BOFIT points out that the production of weapons systems and equipment for military purposes is classified as “investment” according to international standards. Furthermore, some construction investments are directly linked to military requirements.

BOFIT assesses current and future investment trends as follows:

Investment growth has stalled this year. Corporate profits have fallen, the tax burden has risen, and the costs of external financing have increased. The investment outlook for private companies has deteriorated significantly.

Surveys of companies point to a significant, broad-based slowdown in their investment, with declines in some sectors such as construction.

Since the government will be cutting subsidy programs during the forecast period, a deterioration in the growth outlook for fixed investment is expected. Nevertheless, war-related production and investment are likely to continue to rise in the coming years. It is possible that infrastructure projects starting toward the end of the forecast period could slightly boost growth in fixed investment.

Recommended reading:

- Olga Belenkaya, FINAM: The central bank’s neutral signal paves the way for a rate cut to 16% in December, 10/24/25; The central bank’s rhetoric and macroeconomic forecasts appear quite hawkish, 10/24/25

- Global Banking and Finance Review, Reuters: Russian central bank cuts key rate by ’symbolic‘ 50 bps after new US oil sanctions, 10/24/25

- Global Banking and Finance Review; Reuters: Russia’s Nabiullina and her deputy on future rate decisions, oil prices, and the impact of sanctions, 10/24/25

- Moscow Times: Russian Central Bank Cuts Key Rate to 16.5% as Economy Slows, 10/24/25

- Kommersant, Evgeniya Kryuchkova: Half a step down. The Bank of Russia lowered its key rate from 17% to 16.5% per year, 10/24/25

- Vedomosti; Maria Vikulova, Ekaterina Litova: The Bank of Russia lowered its key rate to 16.5%. This demonstrates the regulator’s willingness to continue the previously outlined course of monetary policy easing, 10/24/25

- Cash.ch/Reuters: Putin Confidant: Mass Immigration for Russia Is a “Matter of Survival.” Top Banker German Gref Addresses Demographic and Family Policy at the State Council, Oct. 24, 2025

- Capital+, Bernd Ziesemer: Putin’s banker: Cracks in the leadership, 10/24/25

- Interfax.com: Economic growth neglected during fight with inflation, Russian GDP will only grow 0.8% in 2025 – Sberbank’s Gref, Oct. 23, 2025

- ZDFheute Update; Jan Schneider: New Pressure on Russia. Can Oil Sanctions End the War in Ukraine? Featuring an interview with Janis Kluge, German Institute for International and Security Affairs (SWP), October 23, 2025

- BBC, Gavin Butler: What’s the significance of US sanctions on Russian oil? 10/23/25

- Kurier.at; Michael Bachner: Economy is weakening, but Putin could theoretically wage war “forever,” 10/23/25

- Kleine Zeitung: Central and Eastern Europe is growing significantly faster than the Eurozone, 10/22/25

- MSN.com, Kronen Zeitung; Vergil Siegl: “Russia Can Finance the War for a Long Time Yet!”, 10/22/25

- Newsweek; Brendan Cole: Russia’s Economy Heading Toward Stagnation: Report Published, 10/22/25

- ORF: Ukraine: When will the war be over? Prof. Gerhard Mangott analyzes the situation in Ukraine. What impact does Donald Trump’s erratic course have on President Putin; ZIB2, October 20, 2025

- SRF, Calum MacKenzie: Budget for 2026—Putin apparently expects a long war, 10/17/25

- Military economist Marcus Keupp on ZDFheute live: Ukraine: Putin changes tactics—Trump plans new meeting. YouTube video, from min. 39: This is the economic situation in Russia; Oct. 16, 2025

- German-Russian Chamber of Foreign Trade Focus Analysis: Valdai Forum: Key Economic Messages, October 6, 2025