Despite rising oil prices, growth forecasts remain at 1%

Author: Klaus Dormann

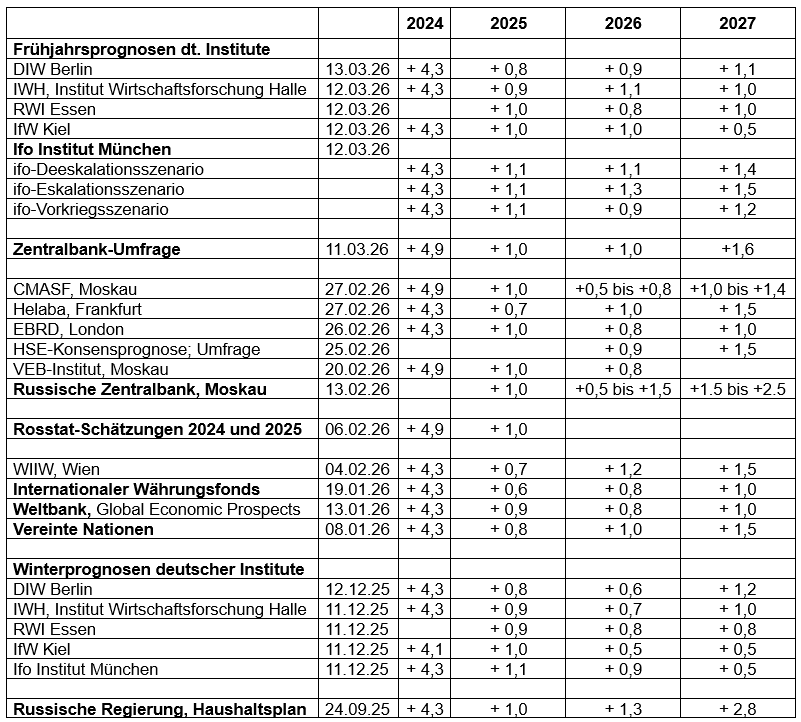

On March 12 and 13, the five leading German economic research institutes published their “spring forecasts” for Germany and the global economy. Compared to their “Winter Forecasts” published in mid-December, they have barely raised their expectations for Russian economic growth in 2026, despite the current sharp rise in energy prices. Three months ago, the range of the institutes’ forecasts was 0.6 percent to 0.9 percent; now it is 0.8 to 1.3 percent.

In the Russian Central Bank’s analyst survey published last week, participants also expected, on average, that the Russian economy would grow by only 1.0 percent this year, as it did in 2025. Next year, they expect a slight acceleration in growth to 1.6 percent. Among German institutions, only the Munich-based ifo Institute considers a similar uptick in growth in 2027 likely.

Will Russia’s budget revenues recover in 2026?

One of the most difficult questions in making economic forecasts at present is likely to be how energy prices will develop. How long will the current sharp rise in oil and gas prices triggered by the war in Iran last?

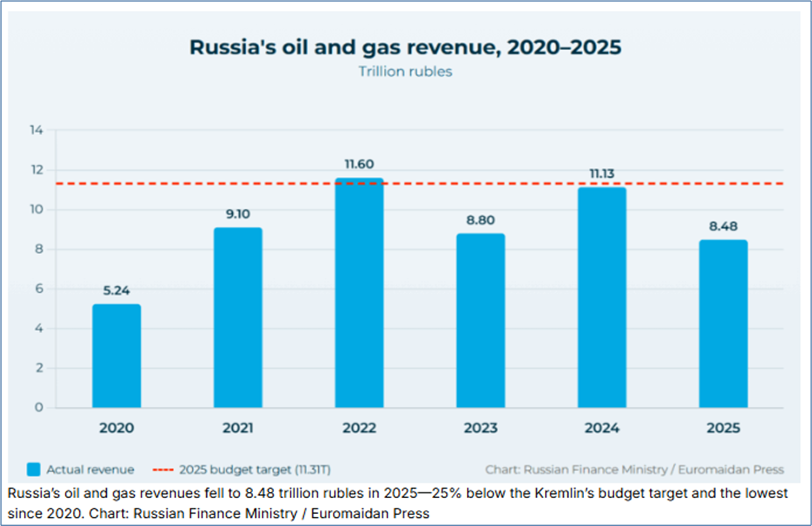

In 2025, Russia’s budget revenues from the oil and gas sector fell by nearly a quarter to around 8.5 trillion rubles. Will a sufficiently strong price increase in 2026 lead to a recovery in revenues from the oil and gas sector?

Russia’s budget revenues from the oil and gas sector

in trillions of rubles

euromaidanpress.com; Peeter Helme:

Russia’s oil revenues collapse 24% as global prices slide further (INFOGRAPHICS), 02/02/26

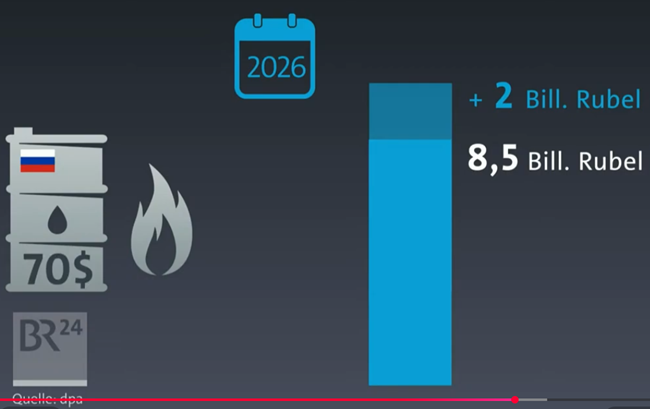

According to a report in the newspaper Izvestia, experts estimate that budget revenues are likely to rise by around 2 trillion rubles in 2026 if the average annual price of Urals crude oil rises to $70 per barrel, according to a dpa report. BR24 showed the following chart in a related broadcast.

Experts’

estimate of a 2 trillion ruble increase in budget revenues from the oil and gas sector

if the oil price rises to $70/b in 2026

BR24: Oil and Gas: How Putin Benefits from the War in Iran; March 13, 2026

If budget revenues from the oil and gas sector do indeed rise to around 10.5 trillion rubles this year, they would still be slightly lower than in 2024, when they reached 11.1 trillion rubles. Ina Ruck, ARD correspondent in Moscow, commented on Russia’s budget developments on the BR24 program starting at the 8-minute mark.

Revenues from energy exports also have a lot of catching up to do

Russia’s revenues from fossil fuel exports have plummeted just as sharply as government revenues from the oil and gas sector. According to the Finnish think tank CREA, revenue from exports of oil, gas, coal, and refined products fell by 19 percent in the twelve months leading up to February 24, 2026, compared to the same period the previous year. Compared to the period before the start of the war in Ukraine, they were even about 27 percent lower. This is reported by Tagesschau.de.

The following figure from the “Russia Chartbook” published by the Kyiv School of Economics in late February shows that, according to the institute’s estimates, Russia’s revenue from the export of crude oil and petroleum products fell to $160 billion in 2025 (-15% year-over-year). At the same time, revenues from natural gas exports are expected to have fallen to around $40 billion (-13%). Overall, these revenues from oil and gas exports, at around $200 billion, were approximately 15 percent lower than in 2024 ($235 billion).

Exports of crude oil, petroleum products, and natural gas

in billions of U.S. dollars

KSE Institute: Russia Chartbook, February 2026; February 27, 2026

In its report published on February 27, the Institute of the Kyiv School of Economics projected a further sharp decline in oil and gas export revenues in 2026, by about a quarter to just around $150 billion. While the institute speculates in the report that global energy prices could rise in February and March due to “geopolitical tensions,” it assesses that fundamental factors in the oil market suggest a “challenging price environment” for Russia for the remainder of the year.

IfW: The price reaction to the “worst-case scenario” was “still moderate”

The Kiel Institute for the World Economy comments in detail on the current rise in energy prices in its economic report “The World Economy in Spring 2026.” The IfW views the effective closure of the Strait of Hormuz as the worst-case scenario for oil price developments. The “worst-case scenario” has materialized. However, the subsequent reaction of oil prices has been “still moderate.”

The IfW describes the price trend for crude oil as follows:

“Oil prices had already been on an upward trend since the end of last year, even though production was rising faster than consumption and the International Energy Agency expected a supply surplus of nearly 3.5 million barrels per day for 2026. The reasons for this were, in addition to tightened U.S. sanctions on Russian oil, increasing tensions between the United States and Iran.

With the outbreak of war and the effective closure of the Strait of Hormuz, the ‘worst-case’ scenario of past Middle East crises became a reality. Given this, the market’s reaction was still moderate. Initially, the price jumped by about $10 to just over $80 per barrel of Brent, then briefly climbed to over $100; most recently, it was trading at around $90, a level that would have just barely fallen within the usual price range in 2023 and 2024.”

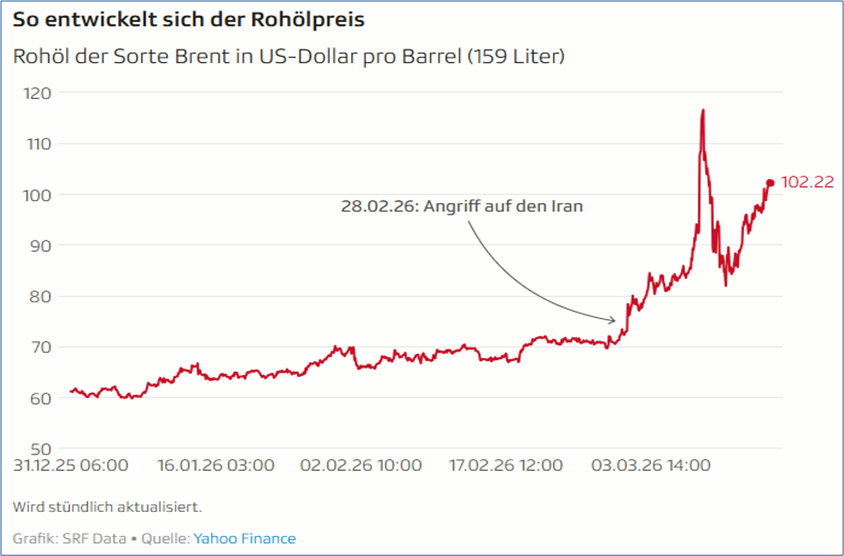

The following SRF chart, which is updated hourly, shows that the Brent price continued to rise to around $102 by March 13.

SRF: Sanctions Eased Because of Iran? Trump Plays the Oil Whisperer – the Kremlin Listens Closely; 03/10/26

Regarding the price development of liquefied natural gas (LNG), the IfW states:

“The effects on the LNG market were also significant. Here, prices in Europe roughly doubled; the increase was even steeper in Asia, where the majority (around 80 percent) of the liquefied natural gas supplied from the Persian Gulf is delivered. In contrast, natural gas prices on the American market have hardly risen at all.”

IfW Forecast: Oil Prices Will Quickly Fall Back to Pre-War Levels

However, the Kiel Institute does not expect a prolonged period of high energy prices. On the contrary: It points out that most observers currently assume that oil supplies from the Persian Gulf will return to normal within a few weeks. The institute bases its forecast on a scenario in which oil prices remain at their current high levels for three months at most and then fall rapidly again starting in the summer.

“We expect energy exports from the Gulf to resume shortly and prices to fall rapidly back to pre-war levels.The military superiority of the United States and Israel makes it likely that safe passage through the Strait of Hormuz can be restored in the foreseeable future and that the disruption to shipments of crude oil, petroleum products, and LNG from the Persian Gulf will last no more than a few weeks. In this case, prices for energy commodities are likely to fall again soon.”

The Kiel Institute expects the price of crude oil to return to roughly pre-war levels by the end of 2026. By the end of 2027, the oil price is expected to fall to the level recorded in the second half of 2025.

The market situation will also be eased by the fact that the OPEC+ member countries have decided to increase production quotas and that the United States appears willing to ease sanctions on Russian oil to meet demand.

According to the IfW, the decline in LNG prices is expected to be somewhat slower. Storage facilities in the Northern Hemisphere are largely empty after the winter. Restocking over the summer suggests high demand is expected.

However, the Kiel-based institute is not entirely certain about its above forecast for the development of the oil market:

“Should it turn out that safe passage through the Strait of Hormuz remains impossible for an extended period, or should production facilities in the neighboring countries be damaged on a large scale, resulting in a prolonged production outage that cannot be offset by additional production elsewhere (the majority of short-term spare crude oil capacity is located in Saudi Arabia), significantly higher prices would certainly be expected for an extended period.”

IfW: Russia’s economic growth slowed significantly in 2025

As the only one of the five German institutes, the spring forecast from the Kiel Institute for the World Economy also offers some insights into current economic developments in Russia. The IfW explains the significant slowdown in Russian economic growth to 1.0 percent in 2025 as follows: .

“On the one hand, the economy is likely operating at the limits of its capacity. Here, the loss of labor due to the war against Ukraine and emigration is making itself felt, but increasingly so are the sanctions-related problems in maintaining and modernizing the capital stock, which threatens to erode gradually. The prioritization of production for military needs is supported by high real interest rates, which are suppressing private consumption and non-war-related investments. On the other hand, the financial resources needed to continue the war deteriorated last year due to falling oil prices and tightened sanctions.”

IfW: Higher energy prices ease the financing of the war in Ukraine

Given the current rise in energy prices, the IfW estimates that Russia’s ability to finance the war in Ukraine will improve significantly in the coming months:

“Not only is Russia now once again earning significantly more than the $59 per barrel that served as the basis for the Russian federal budget. Apparently, the U.S. sanctions—which had been tightened at the end of last year to hinder sales of Russian oil—are also set to be eased. As a result, the price discounts for Russian oil relative to Western grades such as Brent had widened noticeably; currently, however, they have practically disappeared.”

Christof Rühl: If anyone is “profiting” from the war in Iran, it is Russia

In an interview published by Deutsche Welle’s English service, Christof Rühl, Senior Research Scholar at Columbia University’s Center on Global Energy Policy, makes a case very similar to that of the Kiel Institute (The Dip podcast, starting at minute 11). Rühl worked at the World Bank from 1998 to 2005, serving as head of the World Bank’s representative office in Moscow, among other roles, and subsequently served as chief economist at the oil company BP until 2014.

Rühl points out that Russia had previously found itself in a difficult situation because oil prices had fallen significantly. Furthermore, following the tightening of sanctions by the U.S., Russia was only able to supply India with much less oil. The tankers of Russia’s “shadow fleet” had been unable to find buyers for enormous volumes of oil. Now, however, the U.S. has eased sanctions due to the sharp rise in oil prices. Russian oil is finding buyers again—and at much higher prices, even if there are still price discounts for Russian oil. Instead of $50 or $55, Russia can now sell its oil for $95. That is a very big difference.

Three scenarios from the ifo Institute for oil price trends and the growth of the Russian economy through 2027

In its “Spring Forecast,” the Munich-based ifo Institute emphasizes that it remains entirely unclear how the conflict in the Middle East will unfold in the coming days and weeks and what impact it will have on crude oil and natural gas production as well as on supply chains. It developed a “de-escalation scenario” and an “escalation scenario” for future economic development. The institute compares these scenarios with a “pre-war scenario,” which would have unfolded without the “hostilities.”

In the “de-escalation scenario,” the conflict is expected to end quickly following temporary increases in crude oil and natural gas prices to an average of $80 per barrel and €55 per MWh, respectively, in the months of March through May. Once the conflict is resolved, crude oil prices in this scenario fall rapidly again but remain higher than before the outbreak of the war. According to the ifo, these assumptions regarding energy price trends largely correspond to market expectations as of March 4, 2026.

In the “escalation scenario,” it is assumed that the conflict will last significantly longer and be accompanied by a sharper and more sustained rise in energy prices. However, even in this scenario, the ifo Institute assumes a moderate increase in the oil price of only around 21 percent year-over-year in 2026 compared to 2025, which is relatively modest compared to other forecasts.

To quantify the economic impact of the war in Iran, the ifo compares these scenarios with a “pre-war scenario.” The assumptions of the pre-war scenario correspond to market expectations for the trajectory of energy prices prior to the outbreak of the war in late February.

Scenarios from the ifo Institute dated March 12, 2026

, for Brent oil price trends

and Russian economic growth

Even in the “escalation scenario,” GDP growth accelerates only slightly

In the “de-escalation scenario,” it is assumed that the annual average Brent crude oil price in 2026 will rise by only about 5 percent, increasing from $68.4/barrel in 2025 to $71.9/barrel in 2026. Given this oil price trend, the ifo Institute expects Russia’s real gross domestic product to grow by 1.1 percent in 2026, as it did in 2025. In 2027, the ifo Institute expects a slight acceleration in economic growth to 1.4 percent, assuming an oil price of $70—about 1 percent lower than in 2026.

In the “escalation scenario,” the Institute forecasts that Russia’s economy will grow by 1.3 percent in 2026, assuming an oil price increase of around 21 percent, which is slightly stronger than in the “de-escalation scenario” with growth of 1.1 percent. In 2027, the oil price would fall to only $75 in the “escalation scenario.” Economic growth would then pick up to 1.5 percent, barely stronger than in the “de-escalation scenario” (+1.4 percent).

According to the “pre-war scenario”—that is, without the war—the oil price would fall to $65.9 in 2026 and further to $64.5 in 2027. With this decline in the oil price, Russia’s economic growth would fall to 0.9 percent in 2026 and would recover to only 1.2 percent in 2027.

German institutes raise their growth forecasts only slightly

A comparison of the winter and spring forecasts from the five leading German economic research institutes shows that their projections for Russian economic growth in 2026 remained unchanged (RWI Essen: 0.8%) or were raised only slightly to around 1 percent.

The IfW Kiel raised its forecast the most (from 0.5% to 1.0%). The DIW Berlin now expects 0.9 percent growth in Russia (previously: 0.6%), while the IWH Halle forecasts 1.1 percent (previously: 0.7%).

The Munich-based ifo Institute had previously projected 0.9 percent growth for the current year. The institute would have maintained this projection had there been no war in Iran and no rise in energy prices. In its new “de-escalation scenario,” which assumes an imminent end to the war and a modest rise in oil prices, the ifo Institute now expects slightly higher growth of 1.1 percent in Russia for 2026. In an “escalation scenario” featuring an oil price increase of around 20 percent, the ifo Institute anticipates an even slightly stronger GDP growth of 1.3 percent.

The DIW, IWH, and RWI also expect Russia’s aggregate economic output to rise by around 1 percent in 2027. The IfW Kiel, however, stands by its assessment that Russia’s GDP will grow by only half as much, at 0.5 percent. In contrast, the ifo Institute raises its growth forecast for 2027 in its “de-escalation scenario” from 0.5 to 1.4 percent and, in its “escalation scenario,” to an even higher 1.5 percent.

GDP Forecasts 2024 to 2027

Change in real gross domestic product compared to the previous year, in percent

Results of the Central Bank Survey on Inflation, Key Interest Rates, and Growth

Ahead of its next key interest rate decision on March 20, the Russian Central Bank once again conducted an analyst survey (Survey Calendar). The survey was conducted from March 6 to 10, just a few days after the U.S. and Israeli attacks on Iran began on February 28.

In the survey, participants expected a slight acceleration in the growth of aggregate economic output from 1.0% to 1.6% next year, following stagnation in real gross domestic product growth in 2026. The rise in consumer prices is expected to slow from an annual average of 8.7% in 2025 to 5.3% in 2026 and to fall further to 4.4% in 2027.

For 2026, the approximately 30 participants expect the following developments, among others:

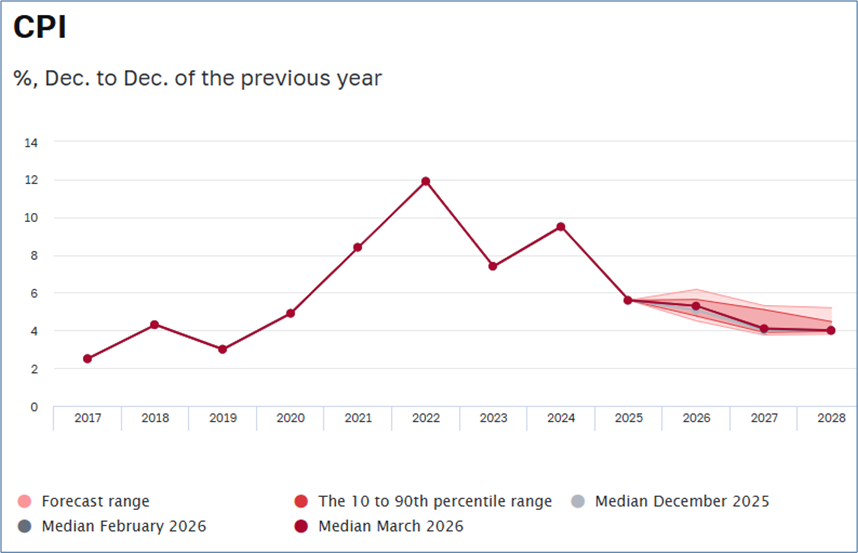

The annual increase in the consumer price index will slow to 5.3 percent in December 2026. By December 2025, the annual inflation rate will have already fallen to 5.6 percent. At the end of 2024, it had reached 9.5 percent.

On an annual average for 2026, the annual inflation rate will fall to just 5.3 percent. On an annual average for 2025, it was 8.7 percent, still slightly higher than in 2024 (+8.4 percent).

The key interest rate will average 14.0 percent this year, a good 5 percentage points lower than in 2025 (19.2 percent).

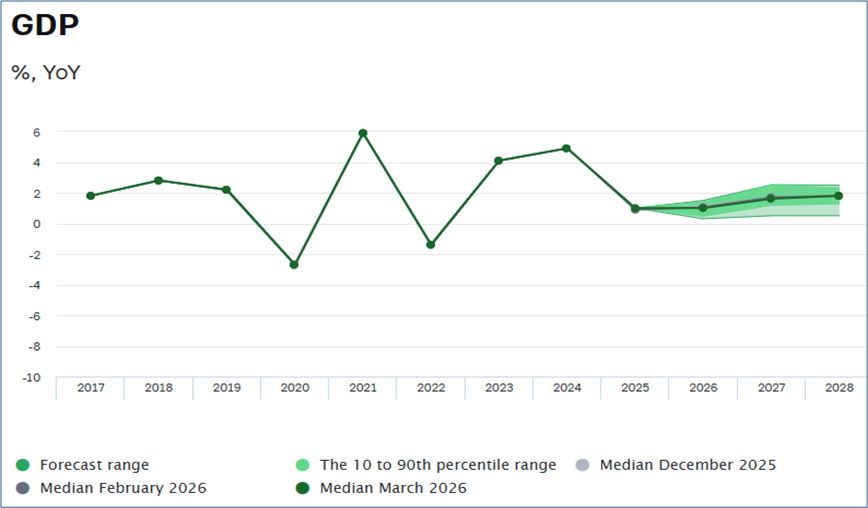

Annual economic growth will stagnate at 1.0 percent in 2026. In 2025, it had fallen from 4.9 to 1.0 percent.

Results of the Central Bank survey from March 6–10, 2026

(results of the February survey in parentheses)

Bank of Russia: Macroeconomic Survey of the Bank of Russia, March 11, 2026 (excerpt)

Survey: Inflation will still significantly exceed the 4% target at the end of 2026

The following figure shows the projected development of the inflation rate according to the analyst survey. The Central Bank’s target inflation rate of 4.0 percent will not yet be reached by the end of 2026 based on the average of the survey participants’ estimates (black line). According to the survey, consumer prices will still rise by 5.3 percent in December 2026 (thus slightly exceeding the range of 4.5 to 5.5 percent cited in the central bank’s medium-term forecast). By the end of 2027, the survey indicates that the inflation target will be nearly met, with a price increase of 4.1 percent.

Consumer

Price Index: Year-over-year increase in December compared to December of the previous year (in %)

Skeptical growth forecast for 2026: GDP rises by only about 1 percent

Survey participants’ expectations regarding economic growth have deteriorated slightly further since the February survey. Following a 1.0 percent increase in real gross domestic product in 2025, output is expected to stagnate at this level in 2026. In 2027, GDP growth is expected to accelerate to 1.6 percent and to 1.8 percent in 2028. However, this means that analysts’ growth forecasts from 2027 onward remain well below the government’s projections, which anticipate growth rates of 2.8 percent in 2027 and 2.5 percent in 2028.

Real Gross Domestic Product

Year-over-year change in percent

Bank of Russia: Macroeconomic Survey of the Bank of Russia, March 11, 2026

Possible effects of the war in Iran on oil prices and the ruble exchange rate

The war in Iran, which began in late February, likely had the greatest impact on the survey’s assessment of the development of the oil price and the ruble exchange rate.

The forecasts for the annual average oil price (for tax purposes) were raised by an average of around 10 percent for 2026, from $50/barrel to $55/barrel.

However, analysts expect slightly lower oil prices over the next two years than previously anticipated. Their oil price forecast for 2027 fell from $56/barrel to $55/barrel, and for 2028 from $60/barrel to $59/barrel.

Analysts expect a slightly weaker depreciation of the ruble against the U.S. dollar over the next three years compared to the previous survey. They have lowered their forecasts for the average annual ruble/U.S. dollar exchange rate as follows:

For 2026 to 84.0 rubles—down from 85 rubles per US dollar previously;

for 2027 to 92.3 rubles—down from 94.5 rubles per US dollar previously;

for 2028 to 97.8 rubles—down from 98.9 rubles per US dollar.

Recommended reading:

- German-Russian Chamber of Foreign Trade:

Analyses, in German; also in Russian; (selection):

Hormuz Shock: How big will Russia’s unexpected oil windfall be? 03/11/26 Economic Consequences of the War in Iran: Oil Price, Russia, Tourism; 03/02/26 Weak Growth, Dwindling Reserves, and High Military Spending; 02/18/26 - Podcast “Tsars, Data, Facts” by the German-Russian Chamber of Foreign Trade, hosted by Thomas Baier:

Russia’s Economy: Sanctions and Growth Prospects; Guest: Prof. Jacques Sapir, 44 min., 03/09/26 Low Gas Storage Levels: Europe’s Challenge in the Energy Market; Guest: Dr. Heiko Lohmann, “energate Gasmarkt”; 34 min., 03/01/26 - “Die Presse” podcast on the Russian economy: Russia – Gas, Sanctions, Oligarchs:

Is Russia the big winner of the Iran war and China the loser? Recorded on 03/10/26;

The war in Ukraine has made Russia the economic loser and China the beneficiary. The war in Iran, however, has entirely different implications. Vladimir Putin is already laughing up his sleeve. And China? Sinology professor Dr. Susanne Weigelin-Schwiedrzik and Russia economist Vasily Astrov (WIIW) in conversation with Eduard Steiner; March 11, 2026

The Iran War, Energy Supply, and Russia

- BBC Newscast with Steve Rosenberg in Moscow: Will Putin benefit from the Iran war? Steve Rosenberg on the U.S. decision to ease sanctions on Russian oil, March 15, 2026

- Deutsche Welle; The Dip Podcast: The cost-of-living shock if the Strait of Hormuz remains closed; Christof Rühl, formerly head of the World Bank’s office in Moscow and now a Senior Research Scholar at Columbia University’s Center on Global Energy Policy, explains, among other things, why Russia stands to benefit from the war in Iran. Neil Shearing, Chief Economist at Capital Economics, explains the potential consequences of higher energy costs for Europe, Asia, and the U.S.—ranging from inflation to delayed interest rate cuts, March 14, 2026

- Sky News Explainer: Why Russia is the big winner in Trump’s war with Iran. Sky’s Paul Kelso looks at how soaring oil prices are benefiting Vladimir Putin and Russia’s war against Ukraine, March 13, 2026

- Al Jazeera English: Who wins and loses in the global energy crisis? Guests: Adi Imsirovic, former global head of oil at Gazprom Marketing & Trading; lecturer in energy studies, Oxford University; Neil Atkinson, National Center for Energy Analytics; Muyu Xu, Senior Crude Oil Analyst, Kpler; March 13, 2026

- BR24: Oil and Gas: How Putin is Profiting from the War in Iran; Sanctions against Russia are being eased, and the purchase of Russian crude oil and petroleum products is temporarily permitted; with Prof. Klemens Fischer, University of Cologne, and ARD correspondent Ina Ruck, March 13, 2026

- Rüdiger von Fritsch, former German ambassador to Russia, in a DLF interview with Dirk-Oliver Heckmann: War in Iran: The Great Benefit for Putin and Russia, Audio, 8 min., 03/13/26

- Joe Blog’s video: Force Majeure Explosion. Energy markets are entering dangerous territory. Oil prices have surged above $100 per barrel as the war in Iran approaches the two-week mark, March 13, 2026

- ZDF heute live: Marcus Keupp, lecturer in military economics at the Military Academy of ETH Zurich, in an interview with Marc Burgemeister: Did Trump miscalculate? War in Iran also has consequences for Russia and Ukraine, March 12, 2026

- Deutsche Welle discussion “Auf den Punkt”: Oil shock caused by the war in Iran: Who loses—and who really benefits? Host: Tina Gerhäusser; Guests: Prof. Claudia Kemfert, Head of Department at DIW Berlin; Markus Bickel, Editor-in-Chief of the Security.Table newsletter at Table Media; Ulrike Herrmann, TAZ journalist; March 12, 2026

- Die Zeit podcast “Was jetzt? — Die Woche”: Oil as a Weapon: The Power Game Behind the Iran War. How great is the risk of a new global oil price shock? Is the conflict in the Middle East accelerating a new phase of economic and geopolitical bloc formation? Dilan Gropengiesser discusses this with Dr. Eva Seiwert from the Mercator Institute for China Studies, March 12, 2026

- Deutsche Welle News.com: How Russia seeks economic and strategic gains from the Iran war; Guest: Ivana Stradner, Foundation for Defense of Democracies, March 12, 2026

- mk.ru; Igor Bokovu: The U.S. has granted a one-month license for the processing of Russian oil: Experts have analyzed the consequences. March 12, 2026

- Watson.ch; AFP Moscow: “Russia’s reputation in Iran is inevitably suffering.” Russia benefits from the Iran war, Putin’s reputation in the region suffers, March 11, 2026

- DLF. Der Tag, Philipp May. Consequences of the Iran War – Is the Next Energy Crisis Coming?, 03/11/26

- FR.de; Mark Simon Wolf: Oil price shock as Putin’s bonus: Is the war in Iran, of all things, filling Russia’s war chest? 03/10/26

- Sky News Analysis; Sky’s Ed Conway explains: Will the release of emergency oil reserves bring costs down? Countries in the International Energy Agency, including the UK, have agreed to release 400 million barrels of oil to curb rising prices, March 11, 2026

- Bloomberg Podcast “Odd Lots”: Rory Johnston, author of the newsletter “Commodity Context,” explains how the oil price could rise to over $200 per barrel, 03/10/26

- Welt News Channel: WAR AGAINST IRAN: Now dealmaker Trump appears to be offering Putin the prospect of sanctions relief; Christoph Wanner from Kyiv, March 10, 2026

- BBC News: Could countries run out of oil and gas amid the US-Israel war with Iran? The BBC’s deputy economics editor Dharshini David, Middle East correspondent Barbara Plett Usher, and energy analyst Bill Farren-Price answer questions, March 9, 2026.

- aawsat.com: Four Years into War, Russia’s Energy Revenues Drop but Oil Keeps Flowing, February 28, 2026

- DLF Background; Gunnar Köhne: Oil Business – Russia’s Shadow Fleet in European Waters; 19 min., 02/26/26

Oil Prices and the National Budget

- Yahoo Finance; Artur Kryzhnyi, Financial Times: Russia to gain billions in additional revenue from oil price surge due to war with Iran, March 12, 2026

- German-Russian Chamber of Foreign Trade; Analysis: Hormuz Shock: How Big Will Russia’s Unexpected Oil Windfall Be? 03/11/26

- Joe Blogs Video: RUSSIA’s Secret. A new report from German intelligence suggests Russia’s real budget deficit could be more than $30 billion higher than the official figures published by Moscow. In this video we break down: • the intelligence report claiming Russia is hiding the real deficit, • why oil revenues are falling • how the strong ruble is damaging government finances • the impact of high interest rates on the economy • signs that Russian consumers are cutting back • and whether Russia can continue funding the war at the current pace, 03/11/26

- FR:de; Felix Busjaeger: Floating War Chest: How a Blockade of Putin’s Shadow Fleet Could End the War; 03/11/26

- Global Banking & Finance Review: Russian oil price used for taxation exceeds budget target, helping state coffers, 03/11/26

- Reuters, Energy News: Sources say that Russia is preparing a 10% cut in “non-sensitive” spending by 2026, 03/11/26

- Expert.ru: The budget deficit amounted to 3.45 trillion rubles in January and February, 03/11/26

- FR.de; Simon Schröder: Russia’s economy on the brink of collapse: EU sanctions coordinator sees “Hemingway moment” approaching, 03/11/26

- Börsennews.de; dpa: High oil prices please Russia – How much is Putin benefiting?, 03/10/26

- New Izvestia; Maria Sokolova: A deficit of 3.5 trillion: Where has the Russian national budget gone, and will high oil prices provide relief? The decline in oil and gas revenues has led to a massive deficit in the Russian state budget, 03/10/26

- Kommersant: Oil and gas revenues in the Russian national budget fell by 47% in January and February, 03/10/26

- Alfa Bank; Pavel Gavrilov, Investment Analyst: Oil prices rise and fall: from $120 to $90 in a single day. Cheap oil could be a thing of the past. Outlook for the commodities market, 03/10/26

- FOCUS-online; dpa: Trillions of rubles in extra revenue: Oil price shock has Russia celebrating, 03/10/26

- dts News Agency: EU Sanctions Coordinator David O’Sullivan sees the Russian economy on the brink of collapse, 03/10/26

- SRF: Sanctions easing for Iran? Trump plays the oil whisperer—the Kremlin is listening closely. The U.S. president wants to end the “brief detour” into Iran soon. This is proving to be good business for Russia; March 10, 2026

- n-tv.de: Putin offers Europe oil supplies – with conditions, March 9, 2026

- The Moscow Times: Low Oil Prices, Strong Ruble Squeezed Russia’s Budget in February, 03/09/26

- Kommersant: Sofia Donetsk, chief economist at T-Investments, on the reasons and consequences of the change in budget rules: Austerity is painful for the economy, 03/09/26

- Politico.eu; Eva Hartog: Why Vladimir Putin is the biggest winner from the war in Iran. U.S.-Israeli strikes have driven up the price of oil, strengthening the Kremlin’s ability to fund its military campaign, March 9, 2026

- Andreas Goldthau, Professor of Public Policy at the University of Erfurt, in a DLF interview with Bianca von der Au: Stock Market Talk: $100/barrel – Why the oil price continues to rise rapidly, 03/09/26

- SberCIB Investment Research: Oil Market: The Impact of the Middle East Conflict and the Blockade of the Strait of Hormuz on Global Oil Prices and Russia, 03/06/26

- bne IntelliNews, Ben Aris: Russia’s oil windfall from Middle East conflict already apparent, but may prove fleeting, March 5, 2026

- Joe Blogs Video: Russia crippled. Russia’s oil industry is facing a growing list of problems — and rising global oil prices may not be enough to solve them, 10 min., 03/05/26

- CEPA; Alexander Kolyandr: Iran War Won’t Save Putin’s Crumbling Economy. Russia is in serious trouble due to a ballooning budget deficit. Rising oil prices are unlikely to change the math, March 4, 2026

- GIS Report; Carole Nakhle: Shadow fleet keeps Russia’s oil exports beyond Western reach, March 2, 2026

- FinanceRambler: Oil and gas prices are rising due to the war in the Middle East: What does this mean for Russia and the ruble? 03/02/26

- Inosmi.ru; Berliner Zeitung: Oil for India, LNG for Europe: The Iran War Brings Russia Back into the Game; BZ: India Considers Increasing Oil Imports from Russia; 03/03/26; Original Article, 02/03/26

- Meduza; Yulia Starostina: Russia’s oil and gas revenues are shrinking. Meduza explains what that means for the Kremlin’s war chest, 01/28/26

Spring forecasts from German institutes:

- DIW Berlin: DIW Weekly Report: German economy on the upswing – global economy continues to grow moderately, 03/13/26

- IWH Halle: Current Economic Outlook: Oil Price Shock Threatens Recovery in Germany, March 12, 2026

- IfW Kiel: The Global Economy in Spring 2026, March 12, 2026

- RWI Essen: Economic Report Spring 2026: Rising Energy Costs Weigh on Economic Recovery, March 12, 2026

- Ifo Institute Munich: ifo Economic Forecast Spring 2026: Consequences of the Iran War Dampen Recovery, 03/12/26

Monthly and Weekly Economic Reports:

- CREA, Vaibhav Raghunandan: February 2026 – Monthly Analysis of Russian Fossil Fuel Exports and Sanctions, 03/12/26

- CMASF Monthly Report: Trends in the Russian Economy, January 2026, March 12, 2026

- Politcom.ru; Marina Voitenko: Weak macroeconomic dynamics require regulatory support, March 12, 2026

- Sergey Blinov: Russia’s Economy Has Chronically Lagged Behind the Global Average Since 2013; in: Macro Overview No. 10 (2026), March 11, 2026

- Kyiv School of Economics: Russia Chart Book February 2026, 02/27/26

- CMASF, Moscow: Base-case macroeconomic forecast for 2026–2029, Feb. 27, 2026

- CMASF Monthly Report: “Analysis of Macroeconomic Trends,” Feb. 27, 2026

Additional economic data and forecasts:

- Interfax.ru: The Russian Central Bank pointed to an expected slowdown in economic activity at the start of the year. Among the reasons cited were tax changes requiring adjustments by businesses and the public, holidays, and the weather. March 12, 2026

- Finmarket.ru: The Russian economy is on the brink of stagflation, March 10, 2026

- Newdaynews.ru; Natalia Petrova: Just a step away from stagnation: Russia’s economy is on the brink of stagflation; 03/10/26

- Tagesspiegel; Miriam Rathje: “Russia is on the brink of a financial crisis”: Why economic pressure will not make Putin back down, 03/10/26