Despite economic stagnation, Russia's central bank cuts its key interest rate to just 17 percent

Author: Klaus Dormann

According to new calculations by the Federal State Statistics Service (Rosstat), there was no “technical recession” in the first half of 2025. However, since the beginning of 2025, output in the Russian economy has been virtually stagnant. How quickly must the Russian Central Bank lower its still very high key interest rate to stimulate new growth? This question remains a subject of debate in Russia. The Central Bank has apparently opted for a gradual rate cut. On September 12, it lowered the key interest rate not by 2 percentage points as it did in July, but by just one percentage point to 17 percent.

The Russian economy is now growing only on a year-over-year basis

For the full year 2025, the vast majority of experts—including German economic research institutes—now expect a drastic slowdown in the annual growth rate of the Russian economy. For example, the average of the growth forecasts in the Central Bank’s analyst survey, which was completed on September 3, fell to just 1.2 percent. In the two preceding years, however, Russia had achieved growth rates of 4.1 percent (2023) and 4.3 percent (2024).

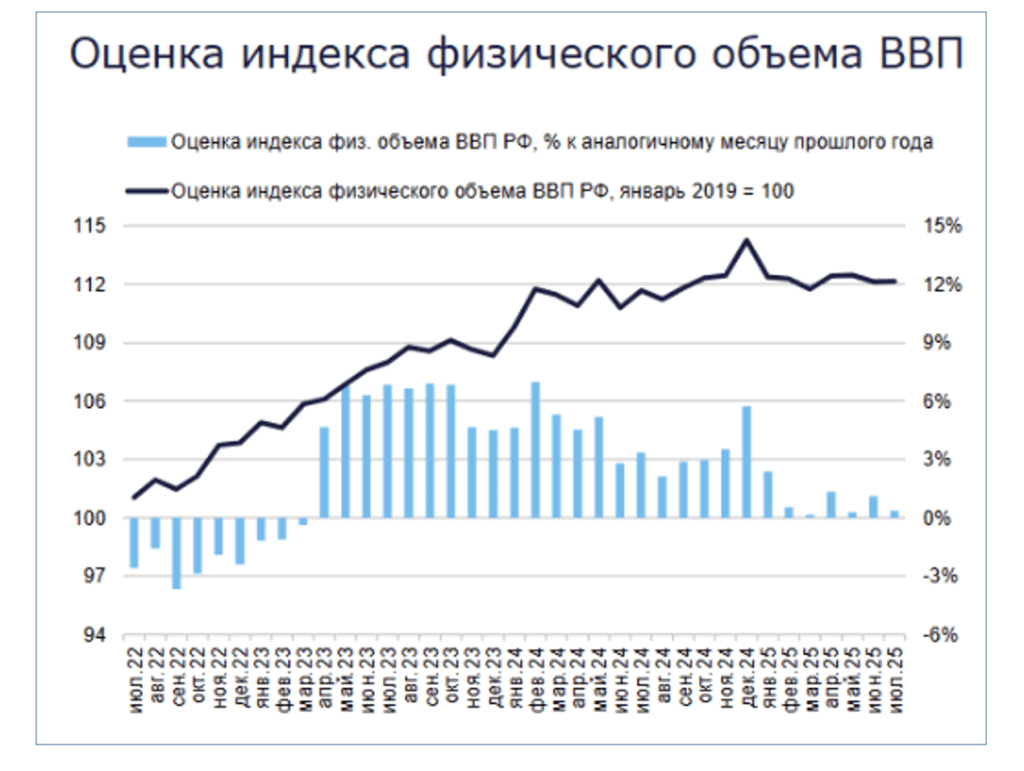

In its “short-term economic analysis” for 2025, published in early September, the Institute of Economic Forecasting of the Russian Academy of Sciences (IEF RAS) also expects growth of only 1.1 percent year-over-year. The following figure from the institute’s analysis shows that, according to the institute’s estimates, the real gross domestic product index remained virtually stagnant over the course of the first seven months of 2025, with only minor month-to-month fluctuations. In July 2025, according to the institute, seasonally adjusted GDP was 0.2 percent lower than in January.

Estimate of the real gross domestic product index (January 2019=100)

Blue bars: Year-over-year changes in percent

Institute for Economic Forecasting of the Russian Academy of Sciences:

Short-Term Analysis of GDP Development – September 2025, 09/05/25

According to Rosstat, there was no “technical recession”

The question of whether Russia experienced a so-called “technical recession” in the first half of the year—meaning that seasonally adjusted real gross domestic product fell in two consecutive quarters compared to the previous quarter—has been hotly debated.

The Research Institute of the Academy of Sciences did not address this question in its analysis. However, on September 12, the statistics agency Rosstat provided more clarity. According to Interfax, the agency reported that, based on its calculations, real gross domestic product did not decline further after falling by 0.6 percent in the first quarter of 2025 compared to the fourth quarter of 2024. In the second quarter of 2025, GDP rose by 0.4 percent on a seasonally adjusted basis compared to the first quarter. The increase in the second quarter thus offset about two-thirds of the decline in the first quarter.

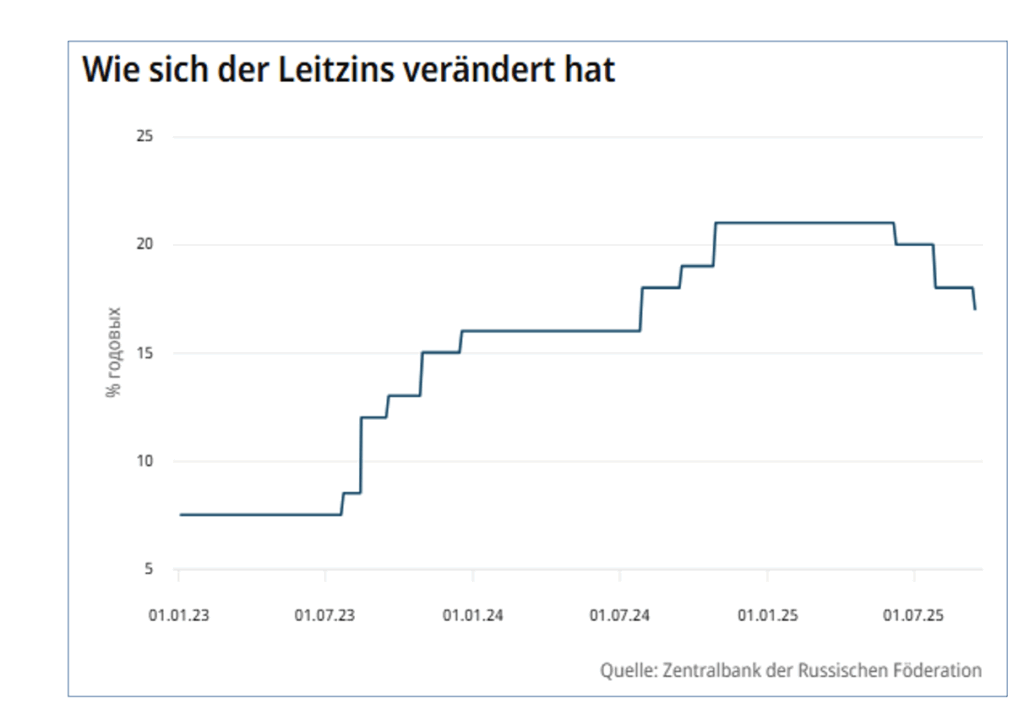

The Central Bank cut the key interest rate less than expected

Despite the largely stagnant output of the Russian economy, the Central Bank cut its key interest rate by only one percentage point to 17 percent on September 12. By contrast, the majority of analysts surveyed by Reuters had expected a cut twice as large, from 18 to 16 percent.

Key interest rate in percent per year

Kommersant; Vadim Visloguzov: The Central Bank slowed the decline. It lowered the interest rate to 17%, 09/12/25

Calls from prominent bank executives and business associations for significantly lower key interest rates apparently had little effect on the Central Bank. Sberbank CEO German Gref had stated at the Vladivostok Economic Forum in early September that the key interest rate should be lowered to 12 percent by the end of 2025. Then, he said, growth in the Russian economy could pick up again (Ostwirtschaft.de).

A key interest rate of 12 percent could have been achieved by the end of the year, for example, if the Central Bank had cut the key interest rate by 2 percentage points at each of its three remaining meetings in September, October, and December. At the September meeting last Friday, however, the widely anticipated 2-percentage-point cut in the key interest rate was not even considered by the Central Bank’s board, according to Central Bank President Elvira Nabiullina. The only options discussed were a cut of 100 basis points or maintaining the interest rate at 18 percent (Interfax.ru).

Alexander Shokhin, president of the Russian Union of Industrialists and Entrepreneurs (RSPP), did welcome the one-percentage-point cut in the interest rate. However, he hopes for a “more radical cut” in the near future. “This is a step in the right direction,” Shochin told Interfax. However, he noted that a key interest rate of 17 percent is still too high for companies to resume heavy investment. For this reason, his association expects a “significantly more radical cut.” Earlier, Shokhin had told journalists that companies are expecting a gradual reduction of the key interest rate to 14 percent by the end of the year (“The Moscow Times,” RSPP.ru).

What President Nabiullina said about the discussion of a technical recession

Shortly before Interfax reported on September 12 that, according to Rosstat, there had been no “technical recession” in Russia, Central Bank President Nabiullina addressed the question of a “technical recession” in Russia during the press conference following the key interest rate decision. She stated that, in the Central Bank’s assessment, there had been no “technical recession” in the first half of the year.

According to Interfax, the Governor explained that, based on the Central Bank’s estimates and the views of some analysts, seasonally adjusted gross domestic product in the second quarter was higher than in the first quarter. Claims by other analysts that there had been a “technical recession” therefore at least warrant further discussion.

Nabiullina took the opportunity to make some fundamental remarks regarding the challenges of comparing seasonally adjusted quarterly GDP figures. In this context, she noted three points:

First, it is a mistake for commentators to describe a decline in real gross domestic product over two consecutive quarters as a “full-blown recession.” A recession must be confirmed by additional indicators in addition to gross domestic product. The generally accepted definition of a recession is a significant decline in macroeconomic activity over several quarters. A broad range of indicators must be taken into account, including trends in employment, real income, consumer demand, and production and sales across a variety of industries.

Second, GDP data—and particularly its quarterly breakdowns—are subject to significant revisions. For this reason as well, the assessment of the economic situation should not be reduced solely to trends in gross domestic product.

Third, estimates of seasonally adjusted GDP growth varied considerably.

Nabiullina confirmed that Russia’s gross domestic product had indeed fallen in the first quarter compared to the previous quarter, but at the same time noted that there had previously been a sharp rise in aggregate economic output in the fourth quarter of last year.

How Nabiullina views current trends in output and prices

According to Reuters, the Central Bank president emphasized at the press conference the need to restore a “balance” between supply and demand in the Russian economy. She summarized her views on current economic trends as follows:

According to the Central Bank’s assessment, Russia’s economy will continue to grow this year and next, albeit at a slower pace than in the previous two years. Growth will pick up again once production capacity catches up with demand and both demand and supply rise steadily. For inflation, this means a return of price increases to the 4 percent rate targeted by the Central Bank. The Central Bank’s interest rate cuts will bring the economy back into balance, and demand will no longer exceed production capacity. According to the Central Bank’s forecast, this will be the case by early 2027.

Nabiullina emphasized: “If we try to accelerate growth now, before demand has fallen to the level of the supply of goods and services, inflation will rise and undermine sustainable growth. That is why we are determined to bring inflation down to a sustainably low level.”

According to Interfax, the president also stated during the press conference that the growth of the Russian economy is currently closer to the lower end of the Central Bank’s current forecast range. According to the Central Bank’s latest medium-term forecast from July, the Central Bank expects aggregate economic output to rise by 1.0 to 2.0 percent this year.

Analysts surveyed by Interfax in early September forecast a 1.1% increase in GDP for 2025. In early August, they had still expected growth of 1.4%.

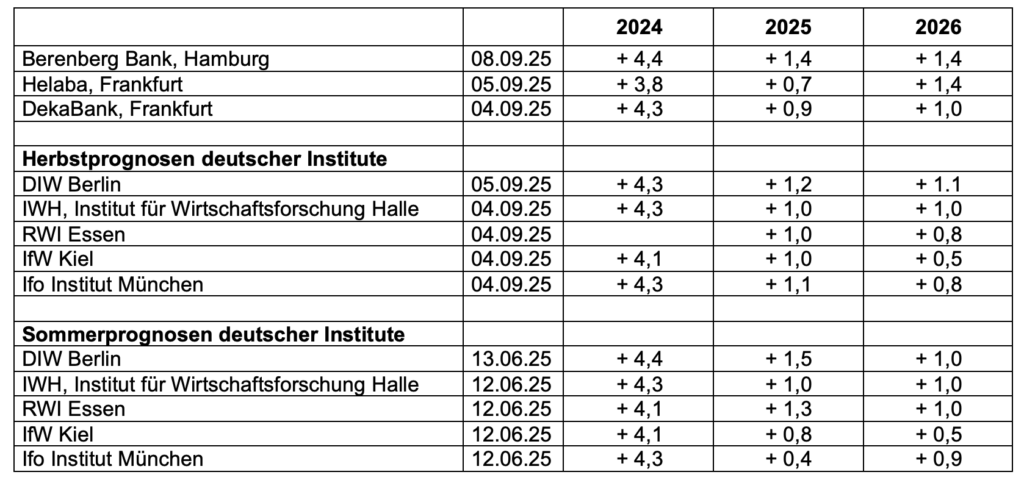

German institutes now also all expect around 1 percent growth in Russia in 2025

The expectations of leading German economic research institutes for Russia’s economic growth this year still varied considerably in their “summer forecasts” published in early June. While the Berlin-based DIW forecast a 1.5% rise in Russia’s GDP three months ago, the Munich-based ifo Institute predicted that the Russian economy would grow by only 0.4% in 2025.

However, in their “fall forecasts” published in the first week of October, all five institutes now expect economic growth of around 1 percent in Russia this year. The Berlin-based DIW lowered its forecast for Russia from +1.5 percent to +1.2 percent. The Munich-based ifo Institute raised its forecast from +0.4 percent to +1.1 percent. The institutes in Halle, Essen, and Kiel now expect +1.0 percent growth.

For next year, nearly all German institutes forecast slightly weaker growth in the Russian economy than for 2025. The DIW expects total economic output to rise by +1.1 percent in 2026. The Kiel-based IfW stuck to its forecast that the Russian economy will grow by only +0.5 percent next year.

In contrast, Frankfurt-based Helaba expects Russia’s growth to pick up next year from +0.7 percent to +1.4 percent. Hamburg-based Berenberg Bank also expects +1.4 percent growth in Russia in 2026 (as in the current year). Frankfurt-based DekaBank continues to anticipate growth of around 1 percent in Russia in 2026.

GDP Forecasts 2024 to 2026

Change in real gross domestic product compared to the previous year in percent

IfW Kiel: The Russian economy has apparently reached its capacity limit

Of the research institutes, only the Kiel Institute for the World Economy comments on its Russia forecast with a few sentences. The IfW believes that the Russian economy’s production reserves are increasingly depleted. It has apparently reached its capacity limit. Regarding current production trends, the IfW notes:

“Gross domestic product in Russia was… only 1.1 percent higher in the second quarter of 2025 than a year earlier. This represents a further slight slowdown compared to the first quarter (1.4 percent) and a significant decline from the high growth rates recorded over the past two years (annual growth of 4.1 percent each year).”

DekaBank: The key interest rate is likely to be lowered only cautiously

Frankfurt-based DekaBank outlines the current development of the Russian economy in its “Emerging Markets Trends” report published in early September as follows:

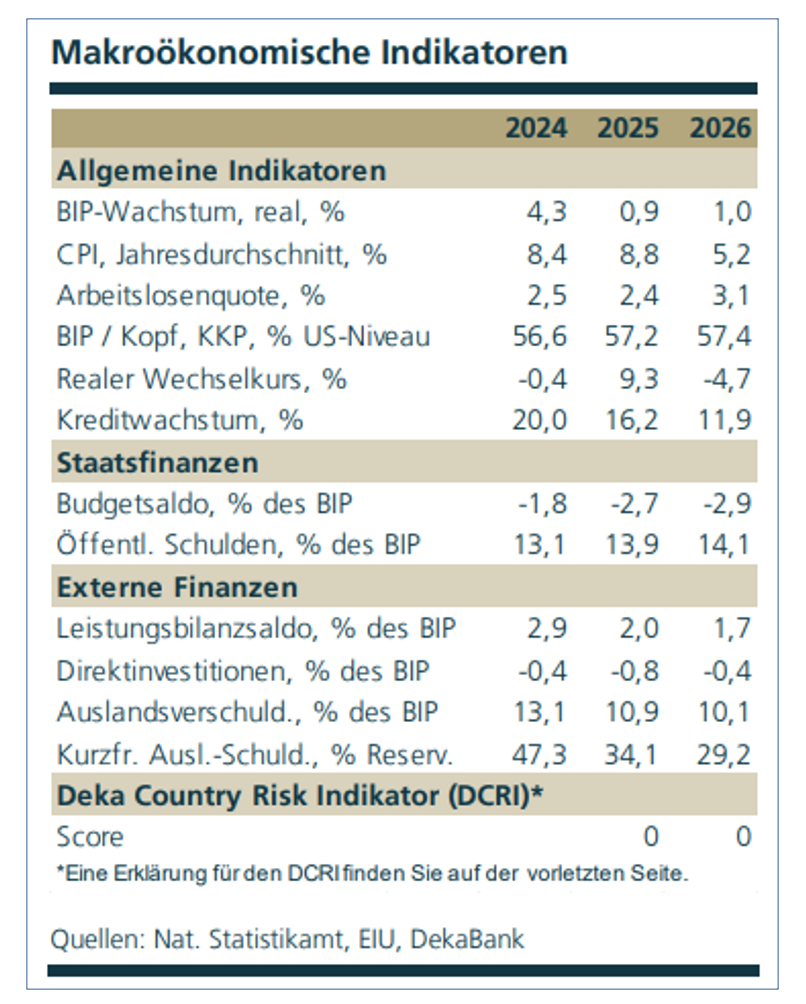

“The Russian economy has shifted heavily toward military production. Spending on the military and security sectors is expected to account for approximately 40% of central government spending by 2025.

Given the numerous state-subsidized credit lines and high fiscal spending, monetary transmission is low. Consequently, a massive key interest rate hike was necessary to curb inflation. This monetary tightening is having an impact primarily in the non-military sector, which further exacerbates the division of the economy.

The fiscal stimulus from military production has lost momentum, so the economy is likely to remain weak in the coming quarters.

Labor is extremely scarce. Furthermore, the high (albeit officially unpublished) number of war casualties and the wave of emigration are exacerbating Russia’s demographic problems.

Consequently, the central bank is likely to lower the key interest rate only cautiously in the coming months so as not to reignite inflationary pressures.”

DekaBank; Emerging Markets Trends: Russia: No Ceasefire in Sight, 09/04/25

Regarding the development of public finances and “external finances,” DekaBank comments:

“The liquid portion of the sovereign wealth fund, which is used to plug budget holes, has shrunk by approximately 50% since 2022. It currently amounts to approximately $48 billion (about 2% of GDP) and is likely to be depleted within the next two years if the current pace of spending continues.

Low oil prices and the discounts that buyers of Russian oil repeatedly demand are complicating the financing situation.”

Recommended reading:

- Central Bank, Press Release: Bank of Russia cuts key rate by 100 bp to 17.00% p.a., September 12, 2025

- Central Bank: Statement by Bank of Russia Governor Elvira Nabiullina following the Board of Directors meeting on September 12, 2025, with video (English)

- RBC.ru: Official data suggests there is no technical recession in Russia, 09/12/25

- Interfax.ru: According to Rosstat, the Russian economy avoided a technical recession in the second quarter, 09/12/25

- Finam.ru; Alla Kolesnikova: The market is disappointed by the Central Bank’s decision. But is that fair? 09/12/25

- TASS.ru: Nabiullina called the statement about a technical recession in the economy controversial, 09/12/25; Izvestia.ru: Nabiullina called statements about a technical recession in the Russian economy controversial, 09/12/25

- Interfax.ru: Rosstat confirmed the estimate of Russian GDP growth in the second quarter at 1.1% year-over-year, 09/12/25

- Reuters, Filipp Lebedev; Global Banking and Finance Review: Russia’s Nabiullina and her deputy Zabotkin on rates, the economy, and the budget, 09/12/25

- Interfax.ru: The shadow of the budget falls on the interest rate. Statement by the Bank of Russia, 09/12/25

- Interfax.ru: The Central Bank did not even consider the possibility of cutting the interest rate by 2 percentage points, 09/12/25

- Interfax.ru: GDP growth is closer to the lower end of the Central Bank’s forecast for 2025, 09/12/25

- FR.de; Lars-Eric Nievelstein: Putin with his back against the wall – Kremlin experts warn of a crisis in Russia’s war economy, 09/11/25

- FR.de; Lars-Eric Nievelstein: Pressure on Putin’s economy grows: Trump urges EU to impose massive tariffs, 09/11/25

- BBC, Peter Hoskins: Trump lobbies EU for 100% tariffs on China and India, 09/10/25

- Kommersant; Artem Chugunov: The economy is changing course. Experts predict a weakening of the ruble by year-end, 09/10/25

- Forbes.ru; Oleg Shibanov, Professor of Finance at the New Economic School: Delayed Effect: What Impact Will the Central Bank’s Interest Rate Cut Have on the Economy?, 09/10/25

- Pavel K. Baev, PRIO, Oslo: Putin’s Vladivostok Forum underwhelming and alarming, 09/10/25

- BBC, Peter Hoskins: Trump lobbies EU for 100% tariffs on China and India, 09/10/25

- Elitetrader; Tinkoff Bank, Sophia Donetsk: Four economic scenarios from the Bank of Russia: What to expect in the coming years, 09/10/25

- Monocle.ru: The Bank of Russia has broken down GDP into scenarios, 09/08/25