Controversial economic analyses at the St. Petersburg Economic Forum

Photo: Klaus Dormann

The Russian government expects economic growth of 0.4 percent this year, which is even lower than almost all analysts’ forecasts. However, it anticipates growth will pick up again next year to 1.4 percent. President Putin assured attendees at the International Economic Forum in St. Petersburg that the economic slowdown had been intentional. He said Russia is now on the upswing.

Many analysts are less confident. For instance, the renowned Moscow-based “Center for Macroeconomic Analysis and Short-term Forecasting” (CMASF) lowered its growth forecast for 2027 from 1.2 to 1.5 percent to 0.8 to 1.0 percent. Currently, the CMASF views the Russian economy as “on the brink of stagflation.”

Ministry: Russia’s GDP grew by only 0.2 percent in the first four months

The trend in production so far suggests that the growth rate, which had already fallen to just 1 percent last year, cannot be sustained. In early June, the Federal State Statistics Service (Rosstat) released economic data for April. The Ministry of Economic Development estimates that real gross domestic product in the first four months was only 0.2 percent higher than in the previous year. About three weeks ago, it had already cut its forecast for this year’s growth of the Russian economy from 1.3 to 0.4 percent—a move that came as a surprise to many observers.

BOFIT: Annual GDP growth in the first four months was “practically zero”

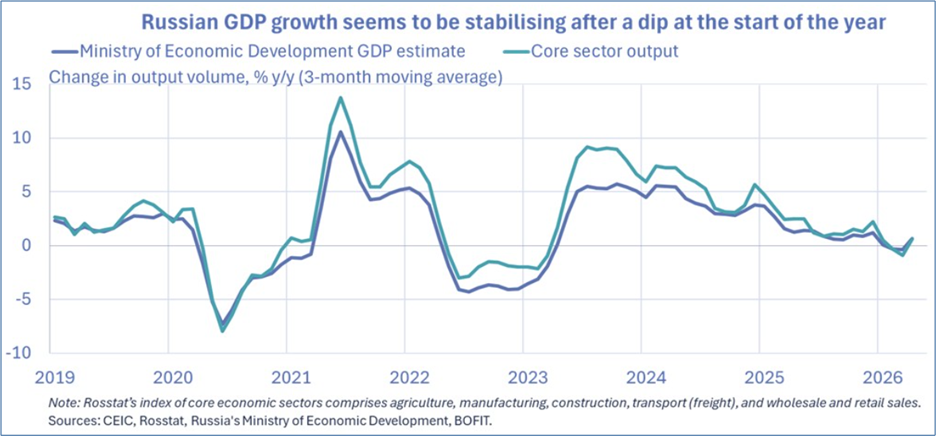

In its weekly report, BOFIT, the research institute of the Finnish central bank, compares in the following figure how production in the five “core sectors” of the Russian economy tracked by the statistics agency Rosstat and overall economic output have developed according to the Ministry of Economic Development’s estimates. To this end, BOFIT calculated the averages of the year-over-year change rates for each month over the preceding three months (a so-called “3-month moving average”).

Russia’s GDP growth appears to be stabilizing—

following a decline at the start of the year

BOFIT Weekly: Russian economy stabilising after weak start of the year, 06/05/26

According to the figure, production in the “core sectors” (agriculture, manufacturing, construction, freight transport, and wholesale and retail trade) fell slightly in March on a year-over-year basis in the 3-month moving average, according to the figure, following an increase at the end of 2025. However, it grew slightly again in April (green line).

According to BOFIT, real gross domestic product growth was “practically zero” (blue line) in the period from January to April compared to the previous year, due to the weak performance in the first two months of 2026.

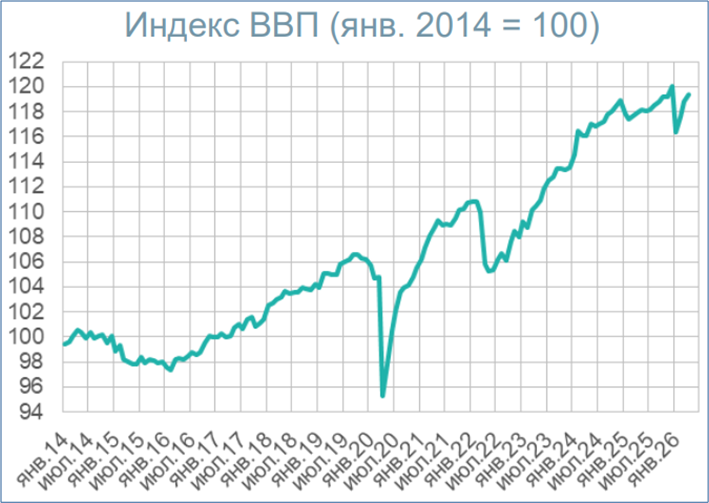

VEB Institute: The sharp GDP slump in January has almost been made up

The research institute of the state-owned development company VEB.RF estimates each month how Russia’s aggregate economic output is developing from month to month on a seasonally and calendar-adjusted basis. In January 2026, the VEB Institute recorded a sharp decline in real gross domestic product after it had reached a new high at the end of 2025. However, aggregate economic output has since largely recovered from this decline.

Real Gross Domestic Product Index (Jan. 2014=100)

, seasonally and calendar-adjusted; VEB Institute estimate

VEB Institute: Global Economy and Markets, June 5, 2026.

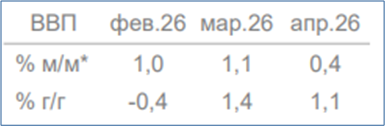

According to the VEB Institute, GDP growth continued in April for the third consecutive month. The growth rate reached +0.4% on a seasonally and calendar-adjusted basis compared to the previous month (first row of the table below). Compared to April 2025, total economic output rose by 1.1% according to the VEB Institute.

Real GDP growth compared to the previous month (seasonally and calendar-adjusted) and compared to the same month of the previous year, in percent

Almost all economic sectors contributed positively to economic growth in April compared to March. The VEB Institute reported declines in production only for wholesale trade and mining. Production in agriculture stagnated.

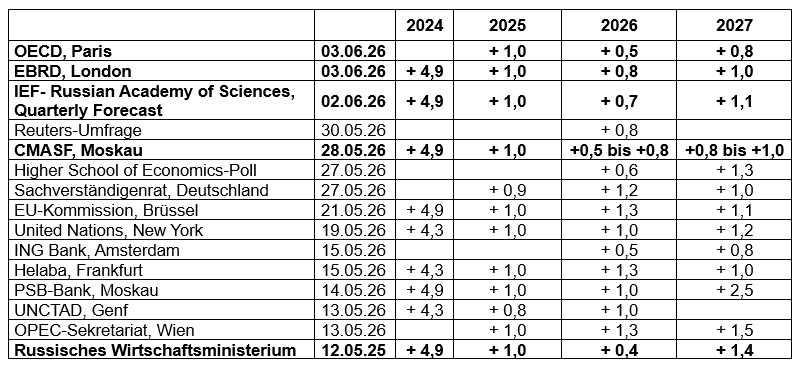

EBRD and OECD maintain their low growth forecasts for Russia

The London-based European Bank for Reconstruction and Development had already forecast at the end of February that the real growth of Russia’s gross domestic product would likely slow from 1.0 to 0.8 percent in 2026. It is also expected to be barely higher in 2027 (+1.0%). The EBRD maintained these forecasts on June 3 (press release).

The Paris-based OECD continues to expect even slightly lower growth in Russia. In its “Economic Outlook,” it has now slightly lowered its forecast for Russia in 2026 to 0.5 percent. This means the OECD’s forecast is now almost as low as the Russian government’s growth forecast (+0.4%). According to the OECD, Russia’s economic growth will also remain below one percent next year (+0.8%). The government, however, expects economic growth to pick up to 1.4 percent in 2027.

In its quarterly forecast, the Institute for Economic Forecasting of the Russian Academy of Sciences (IEF-RAS) now estimates Russia’s growth trajectory almost exactly in line with the EBRD’s projections. The Institute for Economic Forecasting lowered its growth forecast for 2026, published in mid-March, from +1.1% to +0.7% and its forecast for 2027 from +1.4% to +1.1%.

GDP Forecasts for Russia 2024–2027

Year-over-year change in real gross domestic product, in percent

The CMASF currently views Russia’s economy as being “on the brink of stagflation”

The Moscow-based “Center for Macroeconomic Analysis and Short-term Forecasting” (CMASF) slightly raised the forecast range for GDP growth in 2026 to +0.5 to +0.8 percent during its monthly update of its forecast for Russian economic growth at the end of May. However, it lowered its growth forecast for 2027 from +1.2 to +1.5 percent to just +0.8 to +1.0 percent. In an accompanying commentary, the CMASF views the Russian economy as currently “on the brink of stagflation”:

“In terms of the relationship between inflation and aggregate economic output, the Russian economy has effectively entered a period of stagflation—GDP fell in the first quarter despite a significant rise in prices. Although a slight economic recovery is already expected in the second quarter, it is unlikely to change the position on the brink of stagflation.”

The CMASF believes that the measures taken by the government and the central bank have continued to dampen economic activity. Negative impulses from government fiscal policy (withdrawal of funds from the economy) have been compounded by the central bank’s high interest rates.

Symptoms of “Dutch disease” in the Russian economy

Against the backdrop of expectations that rising energy prices will stimulate growth in the Russian economy, the CMASF comments on the projected economic development in 2026:

“Despite the very favorable external economic conditions, the macroeconomic forecast parameters have changed only slightly. In the baseline scenario, the external economic situation—due to the strong ruble exchange rate and high interest rates—leads to growth through increased exports and growth along the consumption chain (With rising wages and incomes, private consumption will ultimately increase by 1.7 to 2.0% in 2026).

At the same time, there are no signs of increased investment activity (a decline in investment is expected), and growth in private consumption is increasingly being offset by rapidly rising imports.

Consequently, the result is… meager GDP growth of 0.5 to 0.8% in 2026 against a backdrop of inflation ranging from 4.6 to 5.0%.”

In light of these forecasts, the CMASF draws a parallel to the “Dutch disease.”

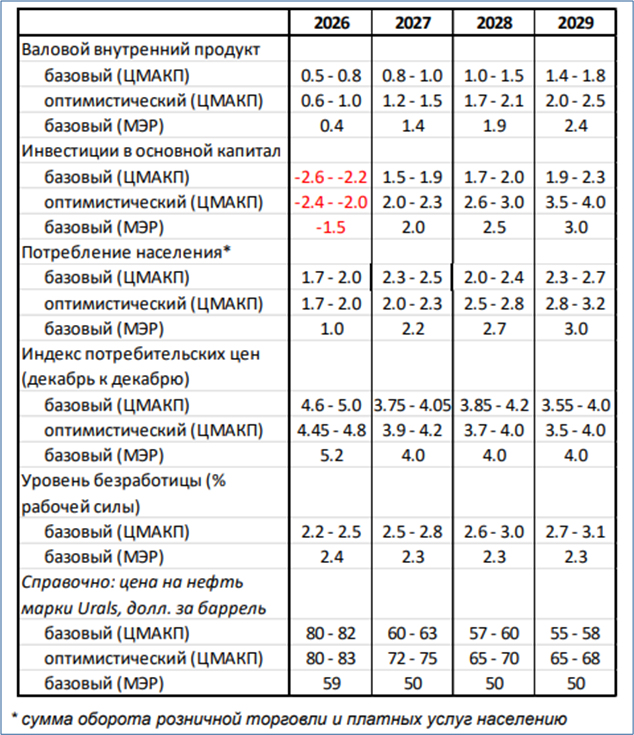

Comparison of CMASF Forecasts with Government Forecasts

In the table below, the CMASF compares its forecasts for real gross domestic product growth in the “base scenario” and the “optimistic scenario” with the base forecasts of the Russian Ministry of Economic Development.

The table below compares forecasts for:

- Investments in fixed assets,

- Private household consumption (total retail sales and paid services to the population),

- Inflation: consumer price increase (December compared to December),

- unemployment rate (as a percentage of the labor force),

- Ural crude oil price, dollars per barrel

CMASF and government forecasts for 2026 to 2029

When comparing the baseline scenarios of the CMASF and government forecasts, the CMASF expects the following in 2026:

- a sharper decline in investment in fixed assets

(CMASF: -2.6% to -2.2%; government: -1.5%), - a significantly stronger increase in private consumption

(CMASF: +1.7 to +2.0%; government: +1.0%), - a lower annual increase in consumer prices in December

(CMASF: +4.6 to +5.0%; government: +5.2%), - a similarly low unemployment rate

(CMASF: 2.2% to 2.5%; government: 2.4%)

Estimates of oil price trends differ significantly: While the government anticipates an Urals oil price of $59 per barrel for 2026 in its baseline scenario, the CMASF expects a price of $80 to $82 per barrel this year.

Russian Finance Minister Anton Siluanov noted at the SPIEF, however, that while his ministry had assumed an oil price of about $59 to $60 per barrel in its calculations for 2026, market conditions have since improved significantly. Siluanov explained that the Russian budget could generate additional revenue of around one trillion rubles due to the situation in the Strait of Hormuz. This could contribute to achieving the budget targets (Financial One; 06/05/26).

President Putin: After the intended “cooling-off,” we are on the upswing

The current state of the Russian economy was also one of the central themes of President Putin’s speech at the plenary session of the St. Petersburg Economic Forum (speech text in English: en.kremlin.ru; video from DRM News). He acknowledged the slowdown in economic growth but emphasized that it had been intended by the government.

Putin compared the decline in growth in Russia with economic trends in the Eurozone:

“Of course, we hear criticism from all sides that growth has lost momentum. Yes, but we have merely fallen to the same level that the countries of the Eurozone have experienced in recent years. And now we are on the upswing. Most importantly, we have preserved the principles of our macroeconomic policy.”

In his speech, the president noted that the government is pursuing the goal of returning to “sustainable” economic growth rates next year. This can only be achieved under one condition: through higher investment with the launch of a new investment cycle. From 2021 to 2024, investments in Russia did indeed rise by a total of nearly 38 percent in real terms. Last year, however, there was a decline in investments (capital investments fell by 2.5% in 2025 according to Rosstat, according to the Moscow Times).

According to the president, it is important to achieve balanced growth supported by domestic demand and accompanied by a further decline in inflation. In 2026, the rate of price increases is expected to fall to 5.2% (according to the government’s year-end forecast).

According to fontanka.ru, the president thus endorsed the government’s fiscal policy and the policy of the Central Bank of Russia, which aims to combat inflation, even at the expense of economic growth. fontanka.ru highlights as the “Kremlin’s core message” that the current economic slowdown is a temporary phase considered necessary for long-term economic stability.

In his speech, Putin also hinted that the budget deficit could continue to grow in the current year. However, he emphasized that it currently stands at only 2.6 percent, which is below the deficit ratios of European countries. DPA notes: Due to the high interest rates on loans associated with inflation, the Russian government must spend comparatively more money to service the national debt than EU countries.

BOFIT: Capital investments continued to decline in the first quarter of 2026

Regarding the decline in investment mentioned by President Putin, the BOFIT research institute of the Finnish Central Bank summarized the following information in its latest weekly report:

According to preliminary figures from Rosstat, investment in fixed assets fell by around 14% in the first quarter of 2026 compared to the previous year. Such a sharp decline in investment activity was last recorded in 2009 during the global financial crisis.

Capital investment slumped by around 14 percent

in the first quarter Year-over-year change in capital investment, in percent

BOFIT Weekly: Russian economy stabilising after weak start of the year, 06/05/26

Investment has fallen significantly this year in nearly all sectors of the economy. Among the few exceptions are public administration and national defense services, finance and insurance, the aerospace industry, and tourism.

Financing investments has become significantly more difficult. In recent years, companies have increasingly financed their investments from their own resources. From January to March, however, total corporate profits fell by 26% compared to the previous year, with 37% of companies reporting losses in the first quarter. The proportion of loss-making companies is slightly higher this year than in the pandemic year of 2020, when the last peak was reached.

The government has also raised corporate taxes. The corporate income tax was already increased last year. Further tax hikes are in the works.

Borrowing costs for companies have also remained high, as the central bank has only been able to lower the key interest rate gradually. The share of bank loans in investment financing declined last year.

Surveys show that companies are also less optimistic about their future investment plans. In their assessment, the outlook for demand has dimmed, and capacity utilization has fallen significantly in many sectors.

On the production side, the weakness in investment was particularly evident in the construction sector. Construction output fell by a further 5% in April compared to the previous year. From January to April, construction output was 8% lower.

Olga Belenkaya, chief economist at the financial institution FINAM, Olga Belenkaya, notes in her detailed economic analysis for April that the Ministry of Economic Development’s new economic forecast for 2026 anticipates a 1.5% decline in fixed capital investment. According to Economy Minister Reshetnikov, the 14.3% decline in investment in the first quarter is not consistent with the simultaneous slight decline in GDP (-0.2%). The minister expects investment and GDP trends to converge more closely over the next two quarters (see also: United24 Media).

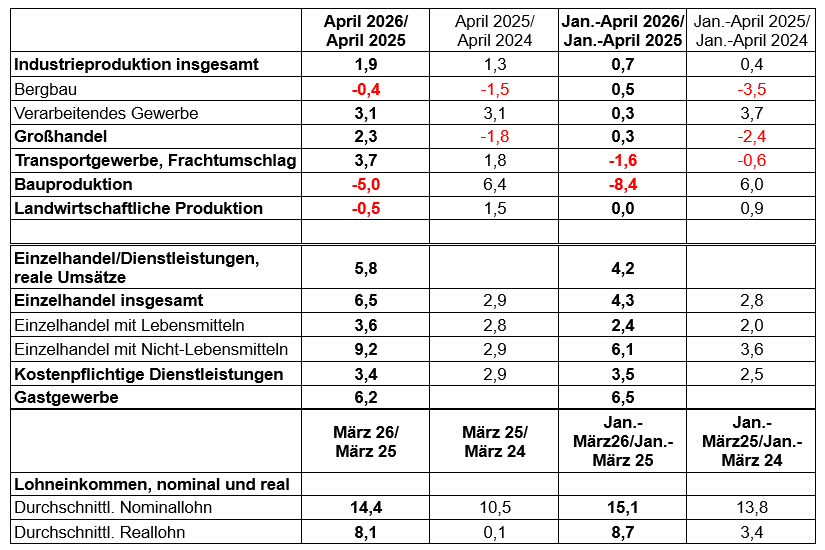

Additional current economic data for April

In her analysis, Olga Belenkaya highlights the following current trends, among others:

According to the Ministry of Economic Development, real gross domestic product showed a slight upward trend in the first four months of 2026 (+0.2% year-on-year), after having fallen by 0.2% year-on-year in the first quarter of 2026.

The Ministry estimated GDP growth in April at 1.3% year-on-year, following 1.9% in March. On a seasonally adjusted basis, GDP declined by 0.5% in April compared to the previous month. Growth in aggregate economic output in April was supported by developments in industry, consumer demand, and freight transport.

In industry, the rise in output in April (+1.9%) continued to be driven by only a few sectors, primarily the defense industry. Among the numerous sectors experiencing declining production, the metallurgy sector is suffering most from the consequences of falling construction activity and the strong ruble. The refining sector recorded the largest decline in production in April (damage to facilities caused by attacks from Ukraine).

According to the “Center for Macroeconomic Analysis and Short-Term Forecasts (CMASF),” industrial production in the “civilian” industrial sectors was 2.9 percent lower in April than a year ago. Excluding the refining sector, the decline is estimated at 2.2 percent.

Seasonally adjusted industrial production growth compared to the previous month accelerated slightly to 0.3% in April, according to Rosstat (March: +0.2%).

In wholesale trade, growth slowed to +2.3% year-over-year in April, down from +8% in March.

Freight traffic volume recorded annual growth (+3.7%) in April for the first time this year, driven primarily by rail transport (+4.1%). The above-average growth in freight volume indicates an increase in transport distances (shift of transport toward the east).

In the construction sector, the annual decline in production eased slightly in April (-5%), but the cumulative decline over the first four months was -8.4% compared to the previous year.

The indicator of consumer trends—real total sales in retail, services for the public, and the restaurant industry—rose by 5.8% in real terms year-over-year in April 2026, according to the Ministry of Economic Development, following a 5.9% increase the previous month. In the first four months of 2026, consumer activity grew by 4.2% compared to the previous year.

In the retail sector, real sales growth in April, at 6.5 percent, exceeded market expectations, as it had in March. The Ministry of Economic Development attributes this primarily to the rise in automobile sales (+40.6% year-over-year).

In the hospitality sector, revenue rose by 6.2% year-over-year in April. From January to April, revenue increased by 6.5%, according to Rosstat’s report on the socio-economic situation in the Russian Federation (Financial One.ru).

Economic Indicators for April 2026 Compared to April 2025

Year-over-year changes in %

Unemployment rate remains low and wages are rising sharply

The labor market situation in April remained virtually unchanged compared to the previous month. The unemployment rate remained near a historic low (2.2%). However, there are signs that the labor shortage is easing, such as reduced hiring plans by companies.

According to the data available so far, wages rose even more sharply in the first quarter of 2026 than in the first quarter of 2025 (15.1% nominal, 8.7% real). Olga Belenkaya notes, however, that a breakdown by industry shows that the trend is highly uneven. Wage growth rates in many industries are well below the national average. Apparently, the salary statistics show distortions due to shifts in the timing of annual bonus payments. She expects a clearer picture of salary trends once data for the second quarter of 2026 becomes available.

Central Bank: “Inefficient allocation of labor” and “underemployment”

In the “Summary of the Key Interest Rate Discussion” published by the Central Bank of Russia, participants noted regarding labor market developments: “Although labor shortages are declining, many companies continue to suffer from staffing shortages. At the same time, others are reluctant to lay off employees—partly because they have already experienced staff shortages in previous years—and are therefore trying to retain their workforce even as demand for their products declines. They fear that it will be difficult to restore their workforce levels in the future.

As a result, an inefficient allocation of labor arises. … Under these conditions, the labor market adjusts primarily through slower wage and bonus growth and an increase in underemployment.”

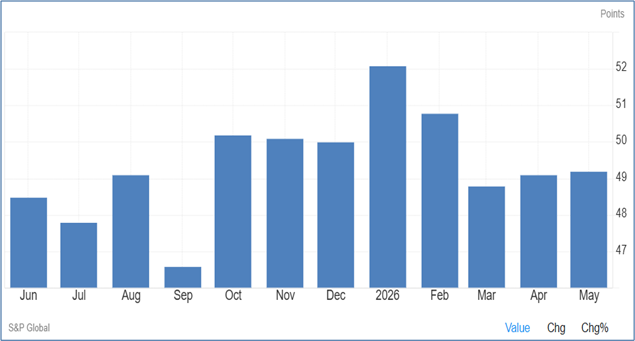

“Leading indicators” signal an economic slowdown in May

The composite “Purchasing Managers’ Index” (PMI), compiled by S&P Global based on surveys of Russian companies, remained slightly below the “growth threshold” of 50 points in May at 49.2 index points. As S&P Global notes, despite a recovery in production growth in the “manufacturing sector,” a sharper decline in service sector output had a negative impact on the composite index. A decline in new orders led to further job cuts. The order backlog fell at its sharpest rate in four years.

Russia: Composite Purchasing Managers’ Index

Tradinig Economics: Russia Composite PMI, June 3, 2026

The Russian Central Bank’s business survey also pointed to a slowdown in business activity growth in May, driven by lower price expectations.

PSB Bank recommends a more expansionary monetary policy

Denis Popov, chief analyst at the state-owned PSB Bank, draws the following conclusion from the economic data:

Despite generally positive signals regarding the current economic situation (increased economic activity in March and April), indicators for medium- and long-term economic development continue to deteriorate. Rosstat recorded a sharp decline in fixed capital investment in the first quarter (-14.3% year-on-year; the steepest drop since the third quarter of 2009). This points to a significant decline in production potential. As companies are generally pulling back from investments, the volume of completed construction projects is also falling rapidly. Negative investment trends have now been observable for a year. The downward trend is even accelerating. Under these circumstances, we consider a more expansionary monetary policy advisable (t.me; see also: Finam.ru).

Recommended reading:

German-Russian Chamber of Foreign Trade:

Analyses, German; also Russian; (selection):

- SPIEF 2026: Lots of Asia, but Germany No. 1 Among Western Countries, 06/04/26

- Ruble exchange rate: Why strength lies in weakness, 05/29/26

- Hormuz implications for Russia and Germany: between model and reality, May 28, 2026

- Russia and China: More Tourists, Fewer Business Deals, May 26, 2026

“Die Presse” podcast on the Russian economy: Russia – Gas, Sanctions, Oligarchs:

Host Eduard Steiner (Die Presse) and economist Vasily Astrov (wiiw) in conversation with guests:

- Is peace in Ukraine in sight? And how dangerous will Russia’s military then be for Europe?

Guest: Military expert Wolfgang Richter, retired German colonel, June 3, 2026;

from min. 16:30 to 28: Vasily Astrov on Western companies’ participation in SPIEF, the development of the Russian economy, and economic policy priorities - Fear in the Kremlin: Are the Russians ready to oust Putin from office?

Guest: Prof. Gerhard Mangott (University of Innsbruck), April 30, 2026

SPIEF 2026:

- The Moscow Times: Putin Talks Multipolarity and Shrugs Off Economic Pain at ‘Russian Davos’, June 6, 2026

- Russia’s Pivot to Asia: Putin’s Speech at SPIEF 2026: Full Content & Detailed Analysis, June 6, 2026

- Finanzmarktwelt; Josephine Bollinger-Kanne: The Four Horsemen of the Apocalypse for Economic Growth in Russia. In Russia, key interest rates, taxes, a strong ruble, and administrative hurdles are cited as major burdens; June 6, 2026

- fontanka.ru: Putin at SPIEF 2026: No Isolation, Russia’s “Cooling Off,” War in Iran, and “Get to Work, Brothers!” Russia is betting on a new global economy, technological independence, and long-term sustainability; June 5, 2026

- Der Stern, DPA: Putin acknowledges economic problems in Russia, 06/05/26

- rte.ie; AFP: The Russian economy has not collapsed, says Putin at a major forum, June 5, 2026

- en.kremlin.ru: Plenary session of the St. Petersburg International Economic Forum. Vladimir Putin took part in the plenary session; Speech text, English; 06/05/26.

- Business-magazine; Sergei Lysenkov: The share of oil and gas in Russia’s GDP has nearly halved, Putin said; 06/05/26

- russland.capital: Putin promotes Nord Stream: “At the push of a button”—but Berlin would have to decide, June 5, 2026

- Prime.ru: Novak issued a forecast for Russia’s GDP growth. Deputy Prime Minister Novak said he expects Russian GDP growth to reach 0.4% by the end of 2026, 06/05/26

- vesti.ru; Alexey Karpenko: Novak expressed confidence that investment in the Russian economy will increase by the end of 2026, 06/05/26

- vesti.ru: Gref explained why it is necessary to shift to a policy of economic stimulus, 06/05/26

- Financial One: High oil prices could reduce the budget deficit by 1 trillion rubles. Finance Minister Anton Siluanov stated this at SPIEF, 06/05/26

- vesti.ru: The Russian Union of Industrialists and Entrepreneurs (RSPP) announced what key interest rate would be favorable for companies in Russia, 06/05/26

- German-Russian Chamber of Foreign Trade: SPIEF 2026: Lots of Asia, but Germany No. 1 among Western countries, June 4, 2026

- Moscow Newspaper; Sascha Paraponow: In Adaptation Mode: German Companies in Russia. Just in time for the St. Petersburg International Economic Forum, the German-Russian Chamber of Foreign Trade presented the results of its survey of German companies in Russia, June 4, 2026

- Inosmi.ru; Die Welt; Andreas Macho, Daniel Zwick, Carsten Dierig: St. Petersburg International Economic Forum. Doing business with Russia for “ethical reasons”—the myth of a mass exodus of German companies, June 5, 2026; original article in “Die Welt,” June 4, 2026

- Inosmi.ru: Putin answered questions from leading international media representatives at SPIEF 2026, June 4, 2026

- russland.capital: Manturov sees Russia’s industry on track despite sanctions, June 4, 2026

- NDR Info; “Das Thema”; Peter Mücke: Four Years of War – Is Russia’s Economy in Shambles? Audio, 11 min., featuring an interview with Janis Kluge, German Institute for International and Security Affairs (SWP), June 4, 2026

- NDR Info; Podcast: “Ten Minutes of Economics,” Astrid Kühn and Nicolas Lieven: German Companies at the Putin Forum: Business as Usual Despite the War? June 4, 2026.

- Tagesschau.de: Economic Forum in St. Petersburg: How Putin is using the event; conversation with ARD correspondent Silke Diettrich about the background; June 4, 2026

- Welt News Channel; Interview with Michael Roth, SPD, on the SPIEF and the participation of AfD politicians: Fierce attack against the AfD! “Embarrassing! That’s a kind of treason!” June 4, 2026

- DW.com; Sabine Klose: Who from the Alternative for Germany attended Putin’s forum? 06/04/26

- t-online.de, Jakob Hartung: Bruch, Dürr, Friedrich. These German business leaders are heading to Putin’s economic forum, June 3, 2026

- Tagesschau; Kerstin Dausend: AfD politicians and German companies in St. Petersburg: Marc Henrichmann, CDU: “Naive and stupid,” video, 2 min., 06/03/26

- ntv.de; Frauke Niemeyer: Forum in St. Petersburg. A German on Putin’s stage; Thomas Bruch, Globus Holding, which has a stake in food hypermarkets in Russia; with quotes from Prof. Michael Rochlitz on the effectiveness of sanctions; June 3, 2026

- Berliner Morgenpost, Funke Media Group; Jo Angerer, freelance correspondent: St. Petersburg Economic Forum. Renewed interest in doing business with Putin: German companies in Russia satisfied, June 2, 2026

- Der Standard; Jo Angerer from Moscow: Economic Meeting. Some companies are sticking with business in Russia—and want gas from Russia again. This year’s St. Petersburg Economic Forum also features a German-Russian economic dialogue, 06/03/26

- Russia’s Pivot to Asia: SPIEF 2026 International Investment Forum Opens in St. Petersburg: US Attends For First Time In Years, June 3, 2026

- Kronenzeitung; Matthias Fuchs: The Economy Is Groaning. Russian Executives Urge Putin to End the War, June 2, 2026

- FOCUS online; Anne-Kathrin Oestmann: Risky Criticism of the War. Russian Business Leaders Rebel Against Putin, June 3, 2026

- Manager-Magazin: Meeting in St. Petersburg. Germans Participate Again in Putin’s Economic Forum. The Head of the German-Russian Chamber of Foreign Trade Does Not Want to “Leave the Market to Asia in the Long Run”; May 31, 2026

Forecasts:

- EBRD; Ksenia Yakustidi: Growth in EBRD regions slows as Middle East conflict sparks energy shock and disrupts supply chains, June 3, 2026

- OECD: OECD Economic Outlook, Volume 2026 Issue 1: Under Pressure, June 3, 2026

- Reuters, Press Reader: Analysts cut Russia’s GDP forecast, ruble to weaken less, May 29, 2026

- Institute for Economic Forecasting of the Russian Academy of Sciences; IEF-RAS: Quarterly GDP Forecast. Issue No. 70, June 2, 2026

- 1Prime.ru. Svetlana Medvedeva: “Better Than Us.” How Russia Surprised the EU. European Commission Spring Forecast for the EU, Russia, and Germany; May 28, 2026

- Higher School of Economics, S.V. Smirnov: Consensus forecast by the Development Center Institute, May 27, 2026; Archive of issues

- Kommersant on UNCTAD forecasts: Trade will slow down along with GDP. Forecast by the United Nations Conference on Trade and Development (UNCTAD), May 25, 2026

Current Economic Developments:

- VEB Institute: Global Economy and Markets, June 5, 2026.

- BOFIT Weekly: Russian economy stabilizing after weak start to the year, June 5, 2026

- Olga Belenkaya; Finam.ru: April 2026 Results – The economy shows signs of recovery in the spring. Macroeconomic data suggest that the Central Bank will continue its 50-basis-point interest rate cut in June; June 4, 2026

- The Moscow Times: Rosstat reported an unprecedented slump in investment in Russia since 2009, June 4, 2026

- United24 Media, Katherina Popilnichenko: Russian Investment Sees Record Decline in 16 Years as Economy Faces Pressure, 06/04/26

- Manager Magazin; Nele Geiger: Economic Forum in St. Petersburg. How Putin Wants to Brush Off the Russian Economic Crisis. It Is Having an Increasingly Severe Impact on Citizens and Businesses, 06/04/26

- Tagesschau; Silke Diettrich, ARD Moscow: Mood in Russia. Why many Russians are increasingly unsettled, June 4, 2026

- Tagesschau.de; Jürgen Buch, ARD Moscow: Poor economic situation. Russia’s debt is rising, the economy is stagnating; 06/03/26

- RBC.ru; Ivan Tkachev, Head of the Economics Department: The Ministry of Economic Development reported a slowdown in Russian economic growth, June 3, 2026

Politics and Economy in Russia; Overall Economic Development:

- t-online.de; Patrick Diekmann: Putin’s problems are growing. The closer you look, the clearer it becomes, 06/06/26

- Prime.ru: Novak issued a forecast for Russia’s GDP growth. Deputy Prime Minister Novak said he expects Russian GDP growth to reach 0.4% by the end of 2026, June 5, 2026

- vesti.ru; Alexey Karpenko: Novak expressed confidence that investment in the Russian economy will increase by the end of 2026, 06/05/26

- vesti.ru: Gref explained why it is necessary to shift to a policy of economic stimulus, 06/05/26

- russland.capital: Manturov sees Russia’s industry on track despite sanctions, 06/04/26

- Alexander Shokhin, President of the Russian Union of Industrialists and Entrepreneurs and Economic Ombudsman, in an interview with RBC-ru: Shokhin proposed “mirror-image” conditions for companies in Russia and the West, June 3, 2026

- ORF III Aktuell interview; WIIW economist Vasily Astrov: “Russian economy is stagnating.” Russia imposed an export ban on kerosene, video, 11 min., 06/02/26

- FR.de; Nils Thomas Hinsberger: Putin’s economy under pressure: Companies in Russia are fighting for survival, June 2, 2026

- Business City Petersburg, Anton Taranukha: GDP forecast, Shochin’s promotion, and preferential mortgages: The most important economic events in May, May 29, 2026

- russland.capital: Russia’s Business Association Warns Government: Don’t “Squeeze the Economy Too Hard,” May 26, 2026