Autumn Economic Outlook in Russia – Data, Forecasts, and Opinions

Author: Klaus Dormann

At the end of September, the Russian government released new economic forecasts as part of its budget planning. It now expects economic growth of only +1.0 percent for the current year 2025 (previously +2.5 percent). At the same time, this year’s budget deficit is projected to be much higher than previously estimated. It is projected to rise to 2.6 percent of gross domestic product in 2025. In 2026, the government plans to raise the value-added tax to boost revenue. The budget deficit is then expected to fall back to 1.6 percent of GDP.

What do the latest economic data for August look like? And how do experts currently assess Russia’s economic development? Among others, Dr. Michael Heise (Chief Economist at the Harald Quandt Trust),

Vasily Astrov (Vienna Institute for International Economic Comparisons), and the former Deputy President of the Russian Central Bank, Sergey Aleksashenkov.

Gross domestic product in August was only 0.4% higher than a year ago

Last week, Russia’s Federal State Statistics Service (Rosstat) released initial economic data for August. Based on this, the Research Institute of the State Bank for Foreign Economic Affairs (“Vnesheconombank”) published an estimate of the monthly trend in aggregate economic output on Friday for the first time in two months. According to the VEB Institute’s estimate, seasonally and calendar-adjusted GDP fell by 0.4 percent in June compared to the previous month and by 0.2 percent in July. In August—as the Ministry of Economy also reported—it stagnated at the level reached in July (see table below).

Real Gross Domestic Product

: Month-over-month changes in % (seasonally and calendar-adjusted).

Year-over-year changes in %

VEB Institute: “World Economy and Markets Review,” 10/03/25

Compared to the previous year (bottom row of the table), total economic output in August was only 0.4 percent higher. In the first eight months of the current year, GDP rose by only 1.0 percent year-over-year. This increase is in line with the Ministry of Economy’s new annual forecast for 2025 (GDP growth of +1.0%) and the lower end of the central bank’s forecast range (+1.0% to +2.0%).

Will GDP decline year-over-year starting in September?

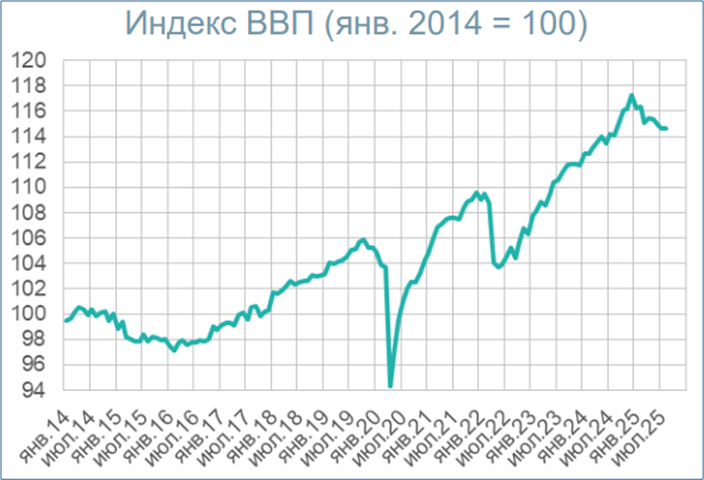

The following chart from the VEB Institute shows that Russia’s total economic output rose sharply one year ago during the September–December period, after seasonal and calendar adjustments, and reached a new high at the end of 2024. To avoid a year-over-year decline in gross domestic product in the remaining months of 2025, aggregate economic output must grow correspondingly strongly.

Real Gross Domestic Product Index (January 2014=100)

VEB Institute: “World Economy and Markets Review,” Oct. 3, 2025

Olga Belenkaya, Head of Macroeconomic Analysis at the Moscow-based financial institution FINAM, believes that a “soft landing” for the Russian economy is possible. However, she warns that a year-over-year decline in aggregate economic output is possible in the fourth quarter, which has just begun. In addition, a reduction in government spending is expected in the current quarter because the Ministry of Finance intends to distribute budget expenditures more evenly throughout the year than in previous years.

Belenkaya expects that the value-added tax increase from 20 to 22 percent, announced for January 2026, will stimulate consumer demand ahead of the tax hike. Consumption is also receiving a boost from the decline in deposit interest rates and increased lending. The cut in the key interest rate has already led to accelerated growth in corporate loans, mortgages, and auto loans.

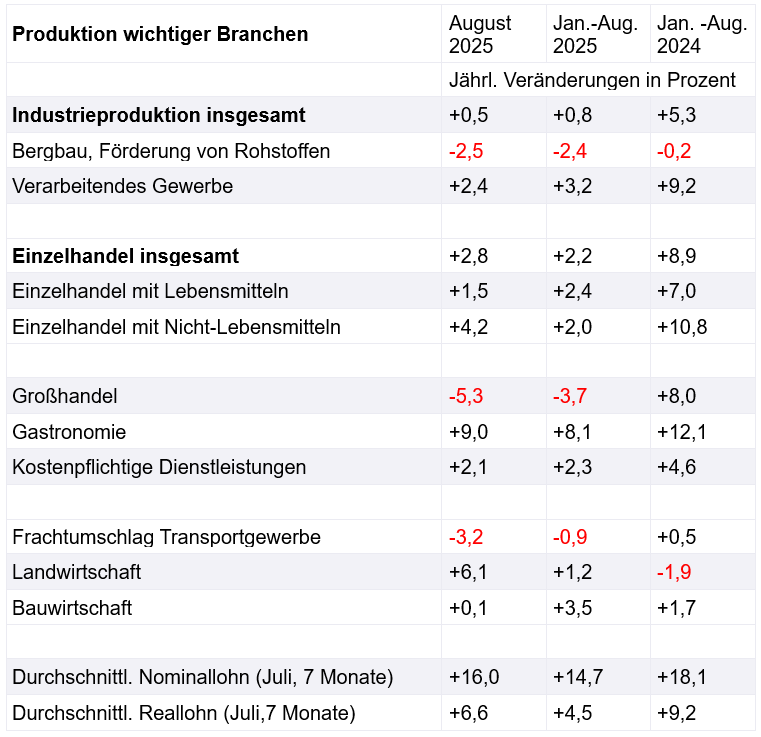

How production in key sectors developed through August

According to Belenkaya, the economic situation for the manufacturing sector is becoming increasingly difficult, especially for industries focused on civilian products. However, Russia’s economy is being supported by strong wage growth and consumer demand.

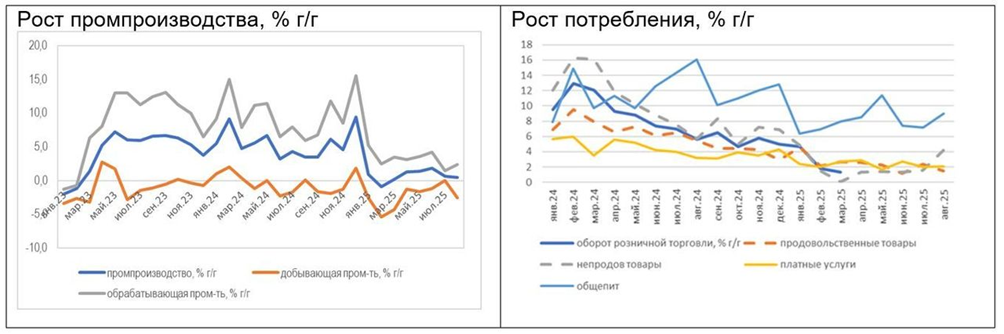

The left of the two figures below shows the trend in industrial production. The upper gray line shows the trend in the “manufacturing” sector, the blue line shows the trend in industry as a whole, and the red line shows the trend in the “mining and extraction of raw materials” sector.

The right-hand figure shows production trends in the consumer-oriented sectors of food services (upper light blue line), services (yellow line), and retail (food retail: dashed red line; non-food retail: dashed gray line).

Production trends in industry (left chart)

and in retail, services, and food service (right chart)

Year-over-year changes in percent

Olga Belenkaya, Finam.ru: The likelihood that the Central Bank will lower the key interest rate to 15 percent by year-end has decreased; 10/02/25

Data shown in the left chart (industry) for August 2025:

Upper gray line: “Manufacturing” (August: +2.4% after +1.5% in July)

Middle blue line: “Total industry” (August: +0.5% after +0.7%)

Bottom red line: “Mining, extraction of raw materials” (August: -2.5% after +0.0%)

Data shown in the right-hand chart (consumer-related sectors) for August 2025:

Top light blue line: Food service (August: +9.0% after +7.2% in July)

Dotted gray line: Non-food retail (+4.2% after +1.6%)

Yellow line: Paid services (+2.1% after +2.0%)

Dotted red line: Food retail (+1.5% after +2.4%)

FINAM Chief Economist expects growth of 1 to 1.4 percent in 2025

Olga Belenkaya does not expect a recession this year or next. Economic growth of 1 to 1.4% is projected for 2025. Only “slightly positive growth rates” are expected next year as well. She points to the planned increase in the tax burden. Furthermore, a cut in the key interest rate will not take effect until after three to six quarters (Finam.ru).

However, the Moscow-based “Center for Macroeconomic Analysis and Short-term Forecasts (CMASF)” lowered its growth forecasts for 2025 and 2026 in early October. Previously, like Olga Belenkaya, it had expected GDP growth of +1.0% to +1.4% in 2025. Now it anticipates growth of only +0.7% to +1.0% for this year. For 2026, it expects growth to accelerate to +1.4 to +1.7% (previously: +1.5 to +1.8%). Dimitri Nikitin of Finam.ru reported on further assessments by Russian analysts.

Alexander Schochin, chairman of the Russian Union of Industrialists and Entrepreneurs for the past 20 years, said in an interview with the television channel Rossiya 24 (Business Insider): “I have the impression that this slowdown or ‘soft landing’ is not very soft.”

Dr. Heise expects growth “around the zero line,” not a recession

Dr. Michael Heise (Chief Economist at the Harald Quandt Trust) also commented on the development of the Russian economy last week in the podcast “Zaren.Daten.Fakten” by the German-Russian Chamber of Foreign Trade. In a conversation with Thomas Baier on the topic of “Military Keynesianism,” the focus was on the development of the German economy. However, in the podcast, Heise also provides an overview of the development of the Russian economy (starting at min. 15). He emphasizes:

Following strong economic growth driven by high military spending, Russia is now “moving more toward the zero line.” The pressures on the Russian economy are significant. Interest rates remain high—despite the central bank’s slight cut in the key interest rate. Inflation is very high, which reduces people’s purchasing power. And oil prices are not very high, which reduces Russia’s oil revenues. In light of significant wage increases, the Russian economy’s competitiveness is declining. The labor supply is tight, especially given the personnel needs arising from the war in Ukraine.

Dr. Heise, Allianz’s chief economist until the end of 2019, does not believe, however, that Russia will experience a “truly hard landing in the sense of a significant recession.” The national budget still offers the government room to maneuver. Despite low oil prices, there are still opportunities to expand the budget deficit somewhat. That is exactly what the government will do if the economy were to falter too severely. He could, however, envision “growth hovering around zero.” The 1.2 percent growth forecast for 2025 in the Russian Central Bank’s latest analyst survey will likely “move downward” next year.

The growth stimulus from military spending is diminishing

According to Heise’s assessment, a significant increase in military spending will not lead to sustained higher economic growth. The “most important lesson” from the development of the Russian economy is that rising military spending can only generate growth momentum for a certain period of time. Following the massive increases in military spending to date, Russia has now reached a level that is no longer easy to raise. Financing military spending is becoming increasingly difficult. And for that reason, its stimulus for economic growth will also continue to diminish.

Furthermore, one must of course recognize that a sharp increase in military spending has “collateral effects” in other areas of spending, for example in research and development, not to mention spending on education and other important investments. In the long term, “military Keynesianism” has negative effects on growth (see the current discussion in Germany: Surplus Magazine video: Is Merz Practicing Military Keynesianism? with Prof. Adam Tooze).

“The Economist”: The “economic boom” is over in Russia

At the end of September, two editors from the British business magazine “The Economist” also discussed the state and prospects of the Russian economy—following two years of growth averaging just over 4 percent—on the podcast “The Intelligence.” Host Jason Palmer interviewed Callum Williams (“senior economics writer”). On September 21, the business magazine had already published an article on the Russian economy under the following headline:

“Russia’s besieged economy is clinging on. The good times have firmly come to an end, but wage growth remains strong.”

According to The Economist, Russia’s struggling economy is thus able to “stay afloat.” However, the magazine believes the “good times” are over.

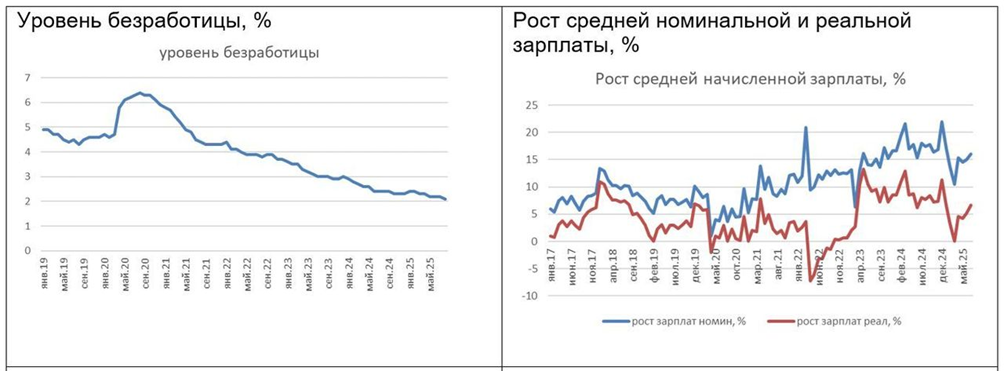

Employment remains high, and retail sales are still expected to grow by 2.3 percent in 2025

Although the crisis is now becoming noticeable, the labor market is still proving surprisingly resilient, notes Economist editor Cullum Williams. Real wages are at a historic high. Above all, consumer confidence in the strength of the economy is stronger than ever before.

An analysis by Russia’s Alfa Bank also points to continued strong growth in private consumption. The bank reports on developments in August:

Real retail sales growth accelerated to 2.8% year-over-year in August, up from 2.0% in July. In the first eight months, real sales rose by 2.2%. This was due to several factors:

Income growth remained strong. Nominal wages rose by 16% in July compared to the previous year.

The unemployment rate fell to a new low of 2.1% in August.

Unemployment rate in percent and year-over-year change in nominal and real wages in percent

Olga Belenkaya, Finam.ru: The likelihood that the Central Bank will lower the key interest rate to 15 percent by year-end has decreased; 10/02/25

The increase in consumer loans also supported consumption. In August, the portfolio of non-mortgage loans grew for the first time since the beginning of the year.

Given the planned VAT increase from 20% to 22% in January, Alfa Bank estimates that strong consumption momentum is likely to continue in the coming months. It expects real growth in retail sales of at least 2.3% year-over-year this year.

Russia’s Path from Boom to Stagnation

Cullum Williams, The Economist’s Russia expert, describes the development of the Russian economy since 2022 as follows:

Time and again, Russia has been predicted to suffer an economic collapse, primarily as a result of sanctions. Yet these predictions have repeatedly proven false. While there was a brief recession in 2022, the Russian economy has been booming ever since.

Now, however, Russia is entering a situation where economic output is slowing to a near standstill. Corporate profit growth is quite weak, and this is affecting the stock market. Real wage growth has also slowed.

In 2023 and 2024, there was still a sort of “economic party” due to the massive increase in government spending. Real wages boomed, corporate profits boomed. Consumer confidence grew significantly. But that party is now finally over.

Fiscal and monetary policy have killed the boom

Williams cites not only the central bank’s interest rate hikes as the cause of the end of the economic boom. He also points to budget cuts:

One cause of “the end of the economic party” was the government’s decision to cut a large portion of the fiscal stimulus measures. In 2023, fiscal stimulus still accounted for about 5% of GDP. This was the result of high additional military spending, as well as significant increases in social benefits. In 2025, however, we expect “mild fiscal consolidation.”

A downside of the boom in 2023 and 2024 was the rapid rise in inflation. As a result, the central bank raised interest rates. The higher interest rates are now having a negative impact. Loans have become more expensive. And people have a strong incentive to hoard their money in bank accounts and earn interest rather than spend it.

The effects of the sanctions were more than offset

On the question of the sanctions’ effectiveness, Williams notes that while they have had negative effects, the impact of the economic policy measures taken by the Russian government has far outweighed the negative effects of the sanctions. The government has provided the economy with “incredibly massive fiscal incentives.” It was able to do so because it had accumulated substantial savings in the run-up to the war in Ukraine. Williams also points to Russia’s unexpectedly high flexibility in circumventing the sanctions.

The decline in oil production can hardly be attributed to the sanctions

In assessing the effectiveness of the sanctions, Williams also analyzes the causes of the decline in Russian oil production in recent months. The drop in oil production can hardly be attributed to the sanctions. Williams cites three other reasons for this:

“Interest rates were very high. This means it has become significantly more expensive to borrow money for the exploration and production of new oil reserves.

Global oil prices were very low, which reduced the incentive for oil exports.

The ruble has appreciated this year, making exports less profitable for Russian oil companies.”

Williams’ conclusion: While the sanctions have disrupted Russian oil trade, Russia is still selling large quantities of oil, particularly to India. “Therefore, one can hardly say that the sanctions have had a truly significant impact on the Russian economy.”

The new rounds of sanctions will also have far less impact than expected

The EU has now announced a 19th sanctions package. The U.S. plans to impose higher tariffs as a penalty on exports from countries that buy Russian oil.

According to Cullum Williams, however, past experience suggests that these new EU and U.S. sanctions will also have little impact. He states in the Economist podcast that his base-case scenario is that the latest rounds of EU and U.S. sanctions will have far less effect than politicians expect. Williams points out that Russia is increasingly engaging in barter trade:

“Russia supplies China with wheat, and China supplies Russia with cars. This means the banking system doesn’t have to be involved. So banking sanctions don’t really have much of an effect.”

In addition, a growing number of neutral or non-aligned countries are acting as intermediary “middlemen” in trade with Russia.

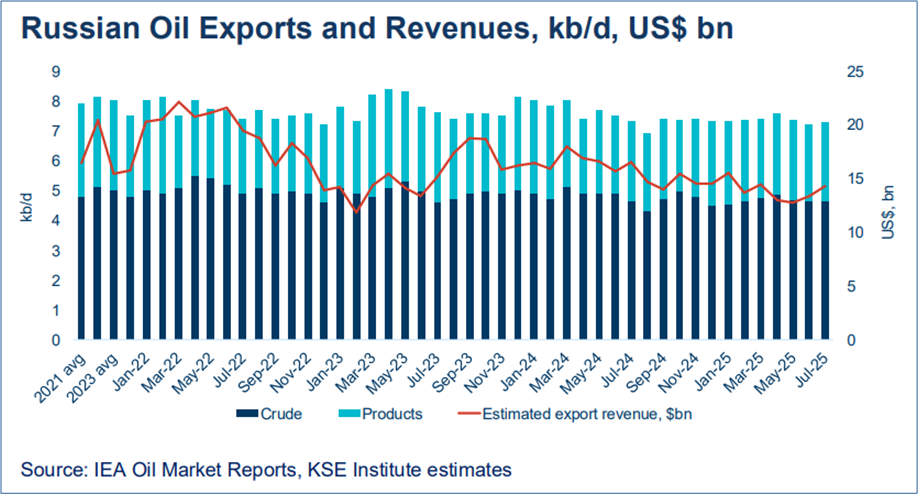

KSE Institute: Oil export revenues have not fallen further since early 2023

The monthly “Russian Oil Tracker” published by the Kyiv School of Economics noted in mid-September: “High oil prices and weak enforcement of sanctions are driving up the Kremlin’s revenues.”

The following figure shows that Russia’s revenues from exports of crude oil and petroleum products in July 2025, at around $15 billion, were still slightly higher than at the low point in early 2023 (red line). However, oil export revenues have been trending downward for nearly two years.

Russia’s exports of crude oil and petroleum products

: Volume in 1,000 barrels/day (bars);

Revenue in billions of U.S. dollars (red line)

Kyiv School of Economics:

Russian Oil Tracker, August 2025:

High oil prices and weak sanctions enforcement boost the Kremlin’s war revenues, 09/12/25

Unexpectedly sharp rise in budget deficit and VAT increase

In its new budget plan, the Russian government anticipates that the budget deficit will rise unexpectedly sharply to 2.6 percent of GDP this year. To generate higher revenues, it plans to raise the VAT rate from 20 to 22 percent starting in January.

Vasily Astrov, a Russia expert at the Vienna Institute for International Economic Comparisons, discussed this on the podcast “Russia – Gas, Sanctions, Oligarchs” by the Austrian newspaper “Die Presse” in a conversation with longtime Moscow correspondent Eduard Steiner (minutes 12 to 25).

Astrov first pointed out that this year’s increase in the budget deficit is primarily caused by the decline in government revenue from the energy sector.

A budget deficit of around 2.5 percent of GDP—which he also expects—is indeed the highest figure since the start of the war in Ukraine. However, by international standards, the deficit is not high. Furthermore, the Russian government’s debt level amounts to only around 15 percent of GDP. That is very low by international standards. There can therefore be no talk of a “catastrophic situation” in public finances. Even before the war, the Russian government had pursued a strategy of reducing public debt to a minimum in order to lessen vulnerability to sanctions.

According to Astrov, the planned increase in the value-added tax is already the third tax hike, even though President Putin and Finance Minister Siluanov had promised not to raise taxes. Since January 2025, the corporate tax rate has been raised from 20 to 25 percent. Taxation on personal income has also been tightened.

As a result of the VAT increase, Astrov expects inflation to rise, at least in the short term. The price increase will

. This will reduce consumer purchasing power and slow the growth of private consumption. In her opinion, however, these effects will “not be dramatic.” With the tax increase, the government is prioritizing “fiscal stability,” albeit at the expense of economic growth.

Astrov: Lower interest rates would weaken the ruble and reduce the deficit

Regarding the decline in government revenue from Russia’s energy exports, Astrov points out that lower interest rates by the Central Bank would also have positive consequences for Russia’s budget, because lower interest rates would increase the Russian government’s revenue in rubles.

According to Astrov, the ruble’s current strength is primarily linked to the very restrictive monetary policy. Because interest rates in Russia are still so high, there are incentives to shift investments from other currencies into the ruble. In his view, the Central Bank could take a “more active” role in lowering the general interest rate level in Russia. This would weaken the ruble and therefore have positive consequences for the development of Russian government revenues (because Russian export proceeds earned in foreign currency would increase in rubles if the ruble depreciates).

Defense spending will decline—and with it, investment

The new Russian federal budget calls for a reduction in military spending. Vasily Astrov suggests that one reason for this could be cost savings resulting from a transition to mass production in the defense industry.

He points out that there was an investment boom across the entire economy in the first two or three years of the war. However, figures for the first half of 2025 showed significantly slower investment growth. The Russian Ministry of Economic Development even expects total investment to decline in 2026. For this reason, he believes that investment trends in the Russian economy are heavily influenced by trends in military spending.

Particularly noteworthy points made by Sergey Aleksachenko

Sergey Aleksachenko served as deputy chairman of the Russian Central Bank from 1995 to 1998 and previously as deputy finance minister from 1993 to 1995. He emigrated in 2014. Today, the 65-year-old lives in the U.S. He heads economic research at the London-based think tank “New Eurasian Strategies Centre (NEST).”

Moritz Gathmann conducted an interview with him that was published in the German Bundestag’s newspaper “Das Parlament.” Below are some of Aleksachenko’s particularly noteworthy theses:

“Russia exports raw materials, and global demand is growing steadily, so growth of three to four percent would be normal; instead, the economy is sliding into stagnation.” … “When we talk about forecasts ranging from minus one to plus one and a half percent, as in the case of Russia, that is stagnation, no more and no less.”

“Western politicians like to delude themselves. The Soviet economy collapsed because it could not bear the burden of military spending. But back then, we had a planned economy. Today’s Russian economy, on the other hand, is a market economy; its balance is ensured by the market mechanism of price changes. Inflation is bad, but inflation is the economy’s response to imbalance.”

“Call Putin’s economic policy what you will, but he respects free price formation. He advocates very strict limits on the budget deficit and public debt.”

“Russia is financing the war primarily not through loans, but through taxes on citizens and the private sector. In this way, the deficit remains quite low at less than two percent of gross domestic product (GDP). By global standards, such a figure is perfectly acceptable.”

“Yes, investment spending must be cut, and the budget deficit in the regions is slightly higher than before the war. But it’s no catastrophe. The challenges facing the German economy are significantly greater.”

“The only real restriction on Russian oil could be a physical one: blocking the Danish straits so that tankers transporting oil from Primorsk can no longer pass through. Such a naval blockade would halt half of Russia’s oil exports, and that would be a very severe blow to Russia. But are we prepared for world market prices to rise to $150 or even $250 per barrel?

Recommended reading:

- Olga Belenkaya, FG Finam: The likelihood that the Central Bank will lower the key interest rate to 15% by year-end has decreased. Rosstat has published the economic indicators for August, 10/02/25

- Finam.ru; Dmitri Nikitin: No Drama: What the Latest Russian Statistics Say, 10/02/25

- TVP World: The state of the Russian economy; Interview with Marius Dubnikovas, Member of the Executive Committee of the Lithuanian Business Confederation, Video, 15 min., 09/30/25

- Cicero.de; Ekaterina Zolotova, US think tank Geopolitical Futures: Russia’s 2026 budget crisis—between war, deficit, and inflation—Moscow’s fiscal policy at the limit; 09/30/25

- Ukraina.ru; Ivan Lizan: Pay and keep hitting: Russia’s 2026 state budget, September 30, 2025

- CEPA, Alexander Kolyandr: The Kremlin to Russian Consumers — Pay for Our War. Russia’s 2026 budget reveals a stark reality: keeping the war going means consumers must pay more for less, September 29, 2025

- Sergey Blinov: Macro Report No. 39 (2025), featuring “Putin’s Two Dozen.” Why economic growth in Russia during Putin’s second twelve years was lower than in the global economy, September 29, 2025

- “The Economist,” daily podcast “The Intelligence”; Jason Palmer and Callum Williams, senior economics writers: Fortunes of war: Is Russia’s economy slowing? 09/29/25

- Sergei Alexashenko in an interview with Moritz Gathmann, freelance journalist; Das Parlament: “Western politicians like to delude themselves.” Former Russian Deputy Central Bank Chief Alexashenko is skeptical about new EU sanctions against Moscow, September 26, 2025

- Inosmi.ru: The Economist: How the Russian economy is staying afloat. The Economist: Predictions of Russia’s imminent collapse due to sanctions have not come true, 09/22/25; Original article: The Economist: Russia’s besieged economy is clinging on. The good times have firmly come to an end, but wage growth remains strong, 09/21/25

- Leading British Conversation; Matt Frei in conversation with Timothy Ash, Associate Fellow, Russia and Eurasia Program, Chatham House: Is Trump right about Russia’s money troubles? Donald Trump has declared that Russia’s economy is “going to the dogs.” Is he right?, Video, 09/27/25

- Tagesschau.de: A Weakening Economy. The State of the Russian Economy, 09/27/25

- n-tv.de, André Ballin, dpa: “A difficult situation.” Signs point to an economic slump in Russia, 09/26/25

- BR24, Peter Jungblut: “Stability in sight”: Is Putin’s economy “going down the drain”? 09/26/25

- The Bell: High interest rates have harmed the economy no less than the coronavirus and, to a certain extent, the sanctions as well – CMASF Institute, 09/26/25

- In an interview with WELT, Frank Umbach analyzes the precarious state of the Russian economy, the consequences of Western sanctions, and the military stalemate in the war in Ukraine: WAR IN UKRAINE: “There is great concern”—Putin trembles before Trump! And is resorting to drastic measures, video, 5 min., 09/25/25

- Deutsche Welle.com/en; Arthur Sullivan: How Russia’s mounting economic woes could force Putin’s hand, 09/25/25

- bne Intellinews, Ben Aris: Russia’s 2026 budget draft cuts military spending for the first time, introduces new taxes, 09/25/25

- Russland.capital: Ministry of Economy has lowered its forecast for GDP growth in 2025, 09/25/25; Russland.capital: Three-year budget draft presented: VAT hike to counter spending pressure, 09/25/25

- Alfa Investor: The Ministry of Finance has presented the draft budget: Revenues are rising, but risks remain. The VAT increase and the high deficit will drive up prices, 09/26/25

- Janis Kluge, SWP Podcast 2025/P 17: Sanctions, Inflation, Recession: Challenges for Russia’s Economy in the Fourth Year of the War, Audio, 19 min., June 30, 2025