Russia

Controversial voices on the Russian economy - What does the central bank expect?

Author: Klaus Dormann

In mid-February, the Russian central bank dared to forecast that the Russian economy would grow by 1.6% year-on-year in the first quarter of 2026. However, it had to revise this expectation significantly on May 7. The central bank now estimates that Russia's real gross domestic product fell by 0.5% in the first quarter. The "Institute for Economic Forecasts of the Russian Academy of Sciences" estimates the decline in GDP in the first quarter at 0.4%, while the Russian Ministry of Economy estimates it at 0.3%. The Rosstat statistics office will publish its first estimate for GDP development in the first quarter on May 15 (Kommersant, Vedomosti).

But how credible is "official" Russian economic data anyway?

The variety of preliminary estimates and forecasts on the development of the Russian economy and the rather controversial debate on economic development within Russia speak for the credibility of the economic data ultimately compiled by the Rosstat statistics office and the government. However, the credibility of this data was recently disputed by the head of Swedish military intelligence, Lieutenant General Thomas Nilsson, in an interview with the "Financial Times" on April 19.

Many Western media reported on this. "Der Spiegel wrote that Nilsson said in the FT interview that Sweden had intelligence information that Russia was systematically manipulating its economic data. The official government data already painted an "alarming picture" of the development of the economy. According to Nilsson, however, the actual situation is even worse. The Russian central bank is "playing down inflation". According to watson.ch, Nilsson doubts that inflation in Russia is at 5.86% as reported by Rosstat. Rather, he believes that the inflation rate is close to the central bank's key interest rate of 15 percent.

However, Alexander Kolyandr, Senior Fellow at the Brussels-based "Center for European Policy Analysis (CEPA)", immediately rejected this assessment in a commentary for the British magazine "The Spectator" on April 21. According to Kolyandr, Nilsson's assumption that the Russian inflation rate is actually around 15% is probably based on earlier publications on price trends by the Russian market research company Romir. However, Romir did not determine a representative consumer price index like the Rosstat statistics office, but only the prices at retailers in around 250 Russian cities ("the prices of products for weekly supermarket shopping"). Romir regularly recorded significantly higher price increases than the representative Rosstat index. However, Kolyandr's criticism apparently went largely unnoticed in Germany.

Janis Kluge: "There is no systematic falsification of inflation data"

In a Spiegel interview last week, Dr. Janis Kluge, Russia expert at the German Institute for International and Security Affairs, also commented on the claims that Russian economic statistics are not credible. According to the Russian website inosmi.ru, which is a "foreign press review" of the state media group "Rossiya Segodnya", Kluge offers extensive quotes from the Spiegel interview:

"Overall, I still consider Russian economic data to be informative and suitable for scientific analysis. I see no signs that Russia is systematically falsifying inflation data."

Kluge argues: If inflation were really as high as the Swedish military intelligence service claims, i.e. close to the key interest rate, yields on Russian government bonds would also have to be significantly higher than at present.

Kluge: "I see no compelling reasons for a deep economic crisis"

According to Inosmi.ru, the SWP expert also assesses the general development of the Russian economy much more positively than Nilsson. Kluge says:

"The Russian economy is not on the verge of collapse. For most Russians, the current situation does not feel like an economic crisis and many have benefited from rising wages in recent years."…

"Russia is of course benefiting considerably from rising oil prices. The price of Russia's most important type of crude oil, Urals, rose from 45 US dollars in February to 95 US dollars in April, more than doubling. According to my calculations, Russia earned ten billion US dollars more from oil exports in April than in February. This will improve the budget situation, albeit with a slight delay."…

"I see no compelling reasons why the Russian economy should fall into a deep crisis in the coming years. It is true that Russia's long-term growth potential has been reduced by the conflict in Ukraine and economic activity is currently cooling noticeably. But even if the conflict in Ukraine continues for a long time, this does not automatically mean problems or economic instability."

Prof. Dr. Alexander Libman, Head of the Department of Politics at the Institute for East European Studies at the Free University of Berlin, also said in an interview with the Berliner Zeitung: "Economically, Russia is still not in a state of collapse" (as it was in the 1990s, for example).

What Russia is experiencing now is the end of the phase of rapid growth after the slump in 2022. "Russia is now clearly in a state of stagnation, possibly even in a minor recession," says Libman.

Kolyandr and Prokopenko: "Russia has entered a recession"

In a commentary for "The Bell", Alexander Kolyandr and Alexandra Prokopenko say that the Russian economy has already entered a "recession" after the Ministry of Economy estimated that gross domestic product in the first quarter of 2026 was 0.3% lower than in the first quarter of 2025. A decline of 0.3% in the first quarter is "not a catastrophe", according to Kolyandr and Prokopenko. However, they note:

"Years of fiscal stimulus fueled by military spending are finally no longer driving growth. It seems that the economy is now bottoming out after overheating. While military demand continues to drive growth in the defense sector, civilian industries are stagnating, consumer demand is weakening and investment is waning."

Kolyandr and Prokopenko point to the following signs of a decline in business activity:

The central bank's business climate index fell into negative territory in February for the first time since 2022.

The Sberindex recorded a 2.2% decline in turnover, also the first since 2022.

The increase in real cash income has slowed from 6.6% to 2.6%. Consumer demand, the most important growth driver to date, is losing momentum.

Although the unemployment rate remains close to the historic low of 2.2%, this is not a sign of a healthy economy. Rather, it is a consequence of the labor shortage, which is dampening growth potential and at the same time driving up wages.

Why the central bank revised its forecast for the first quarter so sharply

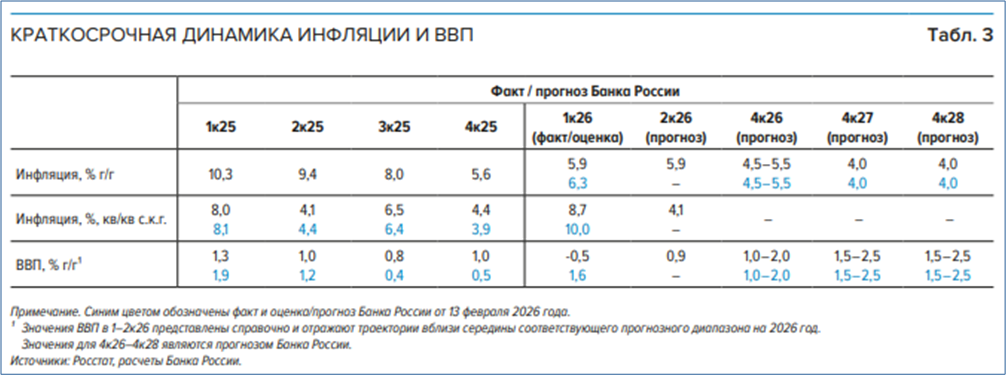

On May 7, the Central Bank published a commentary on the update of its "medium-term forecast" for the Russian economy following the last key interest rate decision. The commentary contains the following table on the quarterly development of gross domestic product. In the bottom two rows, it documents the reduction in the central bank's forecast for economic growth in the first quarter of 2026 from +1.6% to -0.5%.

Short-term quarterly development of inflation and real gross domestic product; year-on-year changes in percent

Note: The lines with the blue numbers show the data and the central bank's estimates and forecasts for inflation and growth as of February 13, 2026Central Bank of Russia: Commentary on the medium-term forecast of the Central Bank of Russia; 07.05.26

The central bank justifies the lowering of its forecast for annual economic growth in the first quarter of 2026 from +1.6% to -0.5% with reference to the "calendar effect" and unfavorable weather conditions. In summary, it argues that January and February 2026 together had three fewer working days than January and February 2025. The impact of the lower number of working days was estimated to be slightly lower in the central bank's February forecast than in the new forecast. In addition, there were unexpectedly unfavorable weather conditions in the first quarter, which affected production in some sectors, including construction.

The GDP forecast for 2026 as a whole remains unchanged at 0.5 to 1.5%

The central bank expects economic activity to recover in the second quarter of 2026, with GDP growth of 0.9%. The second quarter will have three more working days than the second quarter of 2025 and the "calendar effect" will have a positive impact. The central bank also notes that there are signs of a recovery in production in March and April. The business climate assessments for April would approach the level of the third and fourth quarters of 2025.

Taking these factors into account, the central bank is sticking to its forecast that the Russian economy will grow by a "moderate" 0.5 to 1.5% in 2026. Subsequently, GDP growth will grow by 1.5 to 2.5% in line with long-term estimates for the production potential of the Russian economy ("Medium-term forecast" from 24.04.26).

In the following central bank chart on the development of gross domestic product, the gray columns show that the central bank expects GDP to rise by 0.9% in the second quarter of 2026 after falling by 0.5% in the first quarter. The blue dots show the forecast ranges in the central bank's "medium-term forecast" for the years 2026, 2027 and 2028. The black dots show, among other things, the decline in real GDP growth from 4.9% in 2024 to 1.0% in 2025.

Real gross domestic productAnnual changes in percent

Central Bank of Russia: Commentary on the medium-term forecast of the Central Bank of Russia; 07.05.26

The Central Bank did not change its inflation forecasts

On the development of consumer prices, the central bank says in its commentary:

The inflation rate in the first quarter of 2026 was 5.9%, slightly below the central bank's February forecast (6.3%; see table above). This is due to weaker domestic demand and lower rates of price increases for some volatile components than expected in the February forecast.

The central bank expects the annual inflation rate to fall to between 4.5% and 5.5% in December 2026 and return to the target level of 4% in December 2027 (blue dots in the following chart). In December 2025, the inflation rate had already fallen to 5.6% (see black dot in the chart).

Year-on-year increase in consumer prices in percent black and blue dots: annual inflation rate in December

Central Bank of Russia: Commentary on the medium-term forecast of the Central Bank of Russia; 07.05.26

The Central Bank raised its key interest rate forecasts slightly

In February, the central bank still expected its key interest rate to fall to an average of 13.5 to 14.5% in 2026. In April, however, it raised its forecast for the average key interest rate range slightly to 14.0 to 14.5%. For the annual average in 2027, it raised its key interest rate forecast from 8.0 to 9.0% to 8.0 to 10.0% (see blue dots). To explain why it now expects a "somewhat more cautious path of key interest rate cuts" than in its February forecast, the central bank points to inflation risks that are to be expected from the development of the "external environment" and the national budget. In 2028, the central bank still expects the key interest rate to return to the "neutral range" of 7.5 to 8.5% per year.

Key interest rate in percent per year

Central Bank of Russia: Commentary on the medium-term forecast of the Central Bank of Russia; 07.05.26

How the use of GDP will develop

The central bank has also published forecasts on the development of the use of overall economic production. The most important results:

Consumption: the forecast for the development of real consumer spending remains unchanged. It continues to assume that the growth in total private and government consumption of 2.9% achieved in 2025 will slow to a more moderate rate of 0.5 to 1.5% in 2026. This is partly due to the fact that the increase in the VAT rate from 20% to 22%, which came into force at the start of 2026, has brought forward some consumer demand into the second half of 2025. The central bank expects consumption to return to growth rates of 1.5% to 2.5% in 2027 and 2028.

Private consumption (red columns) and public consumption (pink columns) will therefore remain by far the most important drivers of economic growth.

Use of real gross domestic product,GDP changes compared to the previous year in % (dark line),growth contributions of the areas of use in percentage points (colored columns)

red column: private consumption; pink column: government consumption; dark blue column: gross fixed capital formation; light blue column: changes in inventories; green column: net exports; dark line: GDP changes compared to the previous year in %; red dots: Domestic demand; % on previous year

Gross investment: The forecast range for gross investments was also maintained. It remains at 1.0% to 3.0% per year in the years 2026 to 2028. In 2025, gross investment fell unexpectedly sharply by 4.9% (original Rosstat estimate: -3.0% year-on-year). Going forward, the central bank expects investment activity to recover with a positive contribution to GDP from changes in inventories.

The estimate of the rate of change in gross fixed capital formation (GFCF) in 2025 was lowered by Rosstat from +1.7% to -0.4% compared to the previous year. The Central Bank of Russia is forecasting a slight recovery in investment activity compared to the previous year due to monetary easing. It is therefore sticking to its forecast range for growth in gross fixed capital formation of 0.0% to 2.0% for 2026. In 2027 and 2028, it expects investments to grow steadily by 1.0% to 3.0% per year, partly due to the realization of infrastructure projects.

Net exports: The central bank has left its export and import forecasts unchanged.

Real export growth of 0.5% to 2.5% is still expected for 2026. The forecast for import growth also remains at 0.5 to 2.5%. Growth of 1.0% to 3.0% is still expected for exports and imports in 2027 and 2028.

Reading tips:

German-Russian Chamber of Commerce Abroad:Analyses, German; also Russian; (selection):The Druzhba pipeline - once a symbol of friendship, now a bone of contention, 06.05.26Income and prosperity: Are Russians better off than before? 30.04.26Background and comments on the key interest rate decision, 28.04.26

Forecasts:

Central Bank of Russia: summary of the discussion on key interest rates during the "Week of Silence" and during the meeting of the Board of Directors of the Bank of Russia on April 24, 2026, with: Commentary on the medium-term forecast of the Central Bank of Russia; 07.05.26

IEF RAS: Analysis of short-term GDP dynamics: May 2026,05.05.26

YahooFinance Reuters: High oil prices won’t rescue Russian growth, think tank says, CMASF, 04.05.26

Overall economic development:

Politkom.ru; Marina Voitenko; Weekly report: macrodynamics: a trend towards a change of sign, 07.05.26;

Inosmi.ru: The Mirror: Is the Russian economy in crisis? Reports of an imminent collapse of the Russian economy are false, economist Janis Kluge told Der Spiegel. Even if the conflict in Ukraine continues for a long time, there will not be a collapse; 06.05.26; Original article: Der Spiegel+; Interview by Ann-Dorit Boy with Janis Kluge, Stiftung Wissenschaft und Politik: How big is the crisis in the Russian economy really, Mr. Kluge? Kluge contradicts Swedish intelligence that Russia is covering up a severe economic crisis: 05.05.26

The Bell: Alexander Kolyandr, Alexandra Prokopenko: Russia's economy shrinks for the first time since 2023, 06.05.26

Vbr.ru; Yaroslav Nikolaev: Horror show for everyone! Russia and the world are predicted to face an imminent economic crisis. 06.05.26

Kommersant; Artem Chugunov: Population and processing increased GDP. The rate of decline in the Russian economy has slowed in the first quarter. 04.05.26

Merkur.de; Lisa Weegner: Despite oil boom: Putin's economy is faltering, 04.05.26

ntv.de: Companies report weak demand. Russian industry slump continues for eleventh month in a row, 04.05.26

Berliner Zeitung; Liudmila Kotlyarova in conversation with Prof. Libman: "No collapse": Economist clarifies what will happen to Russia's economy now. Eastern Europe expert Alexander Libman explains what the country can expect in the long term, 04.05.26

russia.capital: Kremlin acknowledges downward trend in Russia's economy, 02.05.26

The Moscow Times: Russian Growth Outlook Darkens as Ukraine Hits Oil Infrastructure, May 01, 2026

Globalmsk.ru: The Ministry of Economic Development summarized the economic results for the first quarter of 2026, 01.05.26

RBC.ru: Russia’s GDP fell by 0.3% in the first quarter, 29.04.26

tek:fm: Russia’s GDP to decline by 0.3% in the first quarter of 2023, 29.04.26

inosmi.ru: The collapse of the Russian economy: fact or fiction? The Spectator: The West grossly exaggerates Russia's weakness; original article; 22.04.26

The Spectator; Alexander Kolyandr, Centre for European Policy Analysis: Is Russia's economy really on its last legs? The head of Swedish military intelligence, Thomas Nilsson, told the Financial Times this week that Russia's economy is far weaker than it appears, that the Kremlin systematically manipulates its statistics. One need not be a Kremlin agent to find this less than convincing. 21.04.26;

Euro News; Emma De Ruiter & Dimitri Kavalerov: Russia faked economic data to appear more resilient to its war and sanctions, intel report says, 21.04.26;

Business Insider Germany: Russia's economy is heading for "a financial catastrophe", according to Swedish military intelligence, 20.04.26

Monetary policy and inflation:

Finmarket.ru: Central Bank: Russian economy recovered from overheating in the first quarter, 07.05.26

Vedomosti: The Central Bank saw the economy recover from overheating in the first quarter; 07.05.26

Kommersant: Russian GDP fell by 0.5% in the first quarter; Central Bank estimate, 07.05.26

Interfax.ru: The Central Bank believes that the Russian economy recovered from overheating in the first quarter, 07.05.26

Central Bank of Russia: Summary of the discussion on key interest rates during the "Week of Silence" and during the meeting of the Board of Directors of the Bank of Russia on April 24, 2026, with: Commentary on the Central Bank of Russia's medium-term forecast; 07.05.26

SberCIB Investment Research: Inflation in Russia in 2026: Dynamics and Forecasts. We discuss price growth dynamics since the beginning of the year and forecasts. 05.05.26

SberCIB Investment Research: Key rate forecast for 2026. We discussed the Bank of Russia’s assessment of the current economic situation and how the key rate may change in 2026, 30.04.26

The post Controversial voices on the Russian economy - What does the central bank expect? appeared first on ostwirtschaft.de.

Original article (German):

Read on ostwirtschaft.de →