Russia

Key interest rate lowered to 15%, growth of 1% to remain

Author: Klaus Dormann

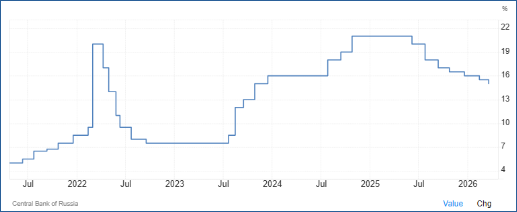

The Russian central bank cut its key interest rate again on Friday by 0.5 percentage points to 15.0%. It was the second cut this year and the seventh since June 2025, when the central bank began lowering the key interest rate from a long-term high of 21 percent. The high interest rates were intended to curb inflation, which was being driven up by a sharp rise in military spending. Now, lower interest rates are intended to stabilize the growth of the Russian economy, which fell from 4.9% to 1% in 2025.

Key interest rate of the Russian central bank in percent/year

Trading Economics, Russia Interest Rate, 20.03.26

Central bank expects "balanced growth"

Elvira Nabiullina, President of the Central Bank, commented on the reasons for the renewed key interest rate cut in her statement on the key interest rate decision on Friday:

"The economy is approaching a balanced growth path. This has enabled us to further loosen our monetary policy stance."

Nabiullina apparently believes that "balanced growth" will be achieved if the Russian economy grows by 0.5 to 1.5 percent in the current year, as expected in the central bank's "medium-term forecast". Although Russia's overall economic output in the first quarter of 2026 is unlikely to reach the annual growth rate of 1.6 percent previously expected by the central bank, she maintained in the press conference that the Russian economy will be able to grow by around 1 percent again in 2026.

In its recently updated quarterly forecast on economic development in Russia, the Institute for Economic Forecasts of the Russian Academy of Sciences (IEF-RAS) also expects a further increase in gross domestic product of around 1% in 2026 as a whole. However, it assumes that real gross domestic product is likely to stagnate in the first half of the year.

Artem Chugunov commented on this in a Kommersant commentary:

"At its core, the current discussion is about reviewing the Central Bank's thesis on the "normalization" of economic dynamics in Russia, which it set out in the latest edition of its report "What the trends say". The regulator describes the current situation as a transition from the overheated growth of 2023-2024 to a more sustainable development path - with falling demand, reduced inflationary pressure and a more balanced economic structure. According to this logic, the central bank interprets the current economic slowdown as a necessary phase in the transition to a new equilibrium."

Nabiullina: How the war in the Middle East could affect the economy

According to a Finam report by Olga Belenkaya among other things, Nabiullina commented on the consequences of the war in the Middle East for Russia and the global economy at the press conference following the key interest rate decision:

"The situation in the Middle East is significantly affecting global commodity markets. The final impact on the Russian economy will depend on the duration and scale of these geopolitical events."

On the one hand, higher oil prices could support Russia's export earnings and the rouble in the short term, according to Nabiullina. However, she warned at the same time:

"However, if we talk about longer-term effects, the situation in the Middle East could negatively affect growth prospects for global demand and investment, leading to higher inflation in energy-importing countries and supply chain disruptions. Essentially, this is another supply shock that will affect global costs and, to some extent, impact prices on the Russian market. In addition, logistical problems could also affect our export volumes."

Russia's inflation rate has almost halved since spring 2025

By March 2025, the annual rise in consumer prices had accelerated further to 10.3% compared to the same month in the previous year. However, it has now almost halved. In February 2026, the annual inflation rate was still 5.9%.

Increase in consumer prices compared to the same month of the previous year in percent

Trading Economics, Russia Inflation Rate, 20.03.26

The central bank expects a further decline in the rise in consumer prices to 4.5 to 5.5% in December 2026. The "inflation target" of 4% should be reached by the end of 2027.

Nabiullina: The price increase fell again in February

In her statement on the key interest rate decision, Central Bank President Nabiullina first emphasized that the rise in consumer prices had fallen again in February 2026. The increase in VAT, excise duties and fees in January had apparently mainly been passed on in prices in the first weeks of 2026.

According to Nabiullina, the inflation expectations of households and companies have only risen in the short term. In February and March, they fell back to the average level of 2025. However, they remained worryingly high.

In mid-March, the annual inflation rate was 5.9%

The central bank's press release on the key interest rate decision includes the following data on current price trends:

In the January-February period, the seasonally adjusted and annualized price increase averaged 10.2%, compared to 4.4% in the fourth quarter of 2025. In February, the inflation rate slowed significantly after the effects of one-off factors from the beginning of the year had subsided.

As at March 16, the annual inflation rate was 5.9%.

According to the central bank's medium-term forecast, the annual inflation rate will fall to between 4.5% and 5.5% in December 2026 if the current monetary policy is maintained (see table below).

From 2027, annual inflation is expected to be in the target range of 4.0%.

Medium-term forecasts of the Russian central bank (excerpt)Development of inflation, key interest rate and economic growth 2025 to 2028

Bank of Russia: Commentary on the Bank of Russia's Medium-Term Forecast, 26.02.26

Nabiullina: Domestic demand is cooling, especially private consumption

According to the central bank governor, high-frequency data from the beginning of the year points to a slowdown in domestic demand, particularly consumer spending. A contributing factor was that many consumers brought forward expensive purchases to 2025 due to the increases in VAT and the car recycling fee. In addition, small companies reported significantly lower demand expectations in surveys at the beginning of the year.

Surveys also showed that the shortage of skilled workers was gradually easing because companies were planning to hire fewer staff. However, unemployment remains at a record low.

The increase in fixed asset investments will be "more moderate" in 2026

According to Nabiullina, the central bank estimates that the economy's production capacities were further expanded last year. Although investment in fixed assets fell slightly at the end of 2025, it remained close to the record levels of recent years. In real terms, they were almost a quarter higher in 2025 than in 2021.

Investment activity remained high, particularly in the manufacturing and service sectors. Among other things, this was due to government support measures and investments to substitute imports.

According to the central bank president, investment plans for 2026 are more moderate. Company surveys show that more companies are planning to expand their production capacities in 2026 than to reduce them.

Annual GDP growth in the first quarter of 2026 was probably lower than expected

In its commentary of February 26 on its latest "medium-term forecast", the central bank predicted that real gross domestic product in the first quarter of 2026 would be 1.6% higher than a year ago. However, at the press conference on March 20, Central Bank President Nabiullina said that according to the latest economic data from Rosstat, growth in the first quarter is likely to be below this forecast. At the same time, according to Finmarket.ru, she explained: "It is still too early to talk about the sustainability of the trend (of weakening economic activity). We expect more information to be available by the April rate decision meeting, including a quarterly breakdown of data (on GDP growth) for the past year. This is crucial to draw conclusions about emerging economic trends."

As reasons for the weak production development at the beginning of 2026, she again referred to the "base effect", among other things: the economy grew strongly in the comparative month of January 2025. In addition, there were two fewer working days in January this year than in the previous year. In addition, the exceptionally cold weather this year has slowed down production in the construction industry. There was a countermovement in private consumption at the beginning of the year following the sharp rise at the end of last year;

The deputy chairman of the central bank, Alexey Zabotkin, also stated that economic growth in the first quarter of 2026 was likely to be somewhat lower than the central bank had previously expected. However, the development of production in the economy as a whole is within the forecast range of +0.5 to +1.5 percent, which the central bank stated in its medium-term forecast published in February (see table above).

Regarding price trends, Zabotkin said that the inflation rate, which was probably also slightly lower than the central bank had expected in the first quarter, would also be within the range of 4.5 to 5.5 percent mentioned in the central bank's medium-term forecast in 2026. He was probably referring to the annual price increase in December 2026. The central bank expects consumer prices to rise by an average of 5.1 to 5.6 percent in 2026 (see table above).

Central bank bulletin: Inflation and growth are "normalizing"

In the central bank bulletin "What do the trends say?", which is regularly published shortly before the key interest rate decisions, the central bank's research and forecasting department had already pointed to a "normalization" of the rise in consumer prices and economic growth rates. The Russian economy is returning to a "balanced growth path" after the "unsustainably high momentum" at the end of 2025. A press release from the central bank summarizes this:

'The rise in consumer prices slowed as expected in February following a sharp increase in January. It approached a level that corresponds to a seasonally adjusted and annualized inflation rate of 4%.

The passing on of the increase in VAT and other taxes and fees implemented at the start of 2026 to prices is largely complete. The inflation expectations of households and companies fell compared to the peak reached at the end of 2025.

According to preliminary data and surveys, economic growth slowed at the start of the year compared to the strong development in December 2025.

The labour market is slowly returning to normal. The rise in wages is gradually catching up with productivity growth. The central bank believes that this provides the basis for a further increase in consumption and overall economic activity.

Strong fluctuations in production at the turn of the year

The following chart from the central bank's bulletin shows how strongly the index of production in the "core sectors" of the Russian economy fluctuated at the turn of the year 2025/2026. A strong growth spurt in December was followed by an even stronger slump in production in January (red line).

In the following chart, the central bank compares the development of production in the "core areas" of the economy with the development of the seasonally and calendar-adjusted index value of total real gross domestic product (4th quarter 2021 = 100). According to the central bank's estimate, overall economic production in the fourth quarter of 2025 is likely to have been higher than in the third quarter. This is shown by the dashed blue line. Rosstat will publish revised quarterly GDP data for 2025 on April 10.

Development of the production of the "core sectors" (red line) and the total gross domestic product of the Russian economy, 4th quarter 2021 = 100

Russian Central Bank: What the trends say, 2/26,12.03.26

Commenting on the sharp fluctuations in production at the turn of the year, the Central Bank's bulletin says that the increase in production in the "core sectors" of the economy in December was probably due to "peculiarities of statistical accounting". For some products that take a particularly long time to complete, the production data is only recorded after the products have been shipped. This was probably the case at the end of 2025 in the sector "Production of base metals and other non-ferrous metals and production of nuclear fuel". At the beginning of 2026, production would have returned to the average level of fall 2025.

Production in the manufacturing sector also fluctuated strongly

According to the central bank's report, production in the "manufacturing sector" (red line in the following figure) slumped in January in a similar way to production in the core sectors of the Russian economy as a whole (seasonally adjusted). Production in the mining sector, on the other hand, remained virtually stagnant.

Production in mining (gray line)and manufacturing (red line)2021 = 100, seasonally adjusted

Russian Central Bank: What the trends say, 2/26 ,12.03.26

The Central Bank also notes the economic trends in January:

Only some consumer goods sectors recorded a stable upward trend in January. Demand for their products continued to be supported by high wage growth at the end of 2025. Demand for Russian exports remained "subdued" in the face of tighter sanctions.

Together with the results of most business surveys (e.g. S&P Global purchasing managers' indices, Central Bank business climate survey), this points to "a gradual slowdown in economic growth". At the beginning of 2026, this trend continued according to the financial flow data of the Central Bank of Russia's payment system.

IEF RAS: GDP almost completely stagnates in the first half of 2026

Unlike the central bank, which only expects a slowdown in the growth of the Russian economy, the new quarterly forecast by the Institute for Economic Forecasts (IEF) of the Russian Academy of Sciences (RAS) assumes that GDP growth will come to an almost complete standstill in the first half of the year. Nevertheless, according to the institute, Russia's economic growth could reach a rate of 1.1% in 2026. However, this is only possible if growth accelerates correspondingly strongly in the second half of the year. In the first half of the year, overall economic production is likely to virtually stagnate. The recovery from the current cooling phase will be slow, according to the IEF, reports Kommersant.

As the following table shows, growth in gross domestic product will continue to be driven primarily by private consumption in 2026 (+ 2.7 %; second line). Government consumption, on the other hand, is expected to be 1.0% lower this year than in 2025 (third row). According to the IEF forecast, growth in fixed asset investments will continue to weaken significantly in 2026 and only reach 0.3 %.

Forecast of real gross domestic product and its use by 2028Changes compared to the previous year in %

IEF RAS: Quarterly GDP Forecast. Issue No. 69, 16.03.26; soon also with English abridged version

Critical comments by the IEF on the central bank's restrictive monetary policy

With regard to the economic impact of the Russian central bank's monetary policy, the IEF of the RAS believes that the development of the Russian economy in 2025 has been shaped by the "restrictive" monetary policy in place since at least October 2024.

The key interest rate cuts that began in June 2025 were accompanied by an almost equally strong slowdown in inflation. Although the nominal key interest rate had been cut to 15.5% by February 2026, the key interest rate was still just under 10% in real terms after deducting the inflation rate. This level continues to have a dampening effect on demand and, more importantly, on supply.

The expected acceleration in growth will be "very difficult"

The IEF does expect growth rates to accelerate in the second half of 2026. However, it believes that this can probably only be achieved by continuously boosting demand for domestic products, increasing the utilization of production capacities and then "stimulating" the investment cycle. However, achieving this chain of measures will be "very difficult" in view of the increasing financial bottlenecks in the national budget.

The Institute considers it advisable to set new priorities in government spending policy, apart from spending on "national security". This means reducing ineffective spending or spending that has no immediate stimulating effect in favor of spending items that can boost the development of the economy in the short term - above all by supporting final demand for domestic products.

The IEF believes it is possible that annual GDP growth of 1.5 % to 2 % can be achieved in the second half of 2026 by realizing previously "postponed" consumer and investment demand and by replenishing inventories.

However, as in previous years, the main risk is a "negative development of foreign trade indicators".

Reading tips:

German-Russian Chamber of Commerce Abroad: Analyses, German; also Russian; (selection): Hormuz shock: Europe facing new gas crisis, 18.03.26 Hormuz shock: How big will Russia's unexpected oil windfall be? 11.03.26 Economic consequences of the Iran war: oil price, Russia, tourism; 02.03.26

Podcast "Tsars, Data, Facts" of the German-Russian Chamber of Commerce Abroad by Thomas Baier: Russia’s Economy: Sanctions and Growth Prospects; Guest: Prof. Jacques Sapir, 44 min., 09.03.26 Low gas storage levels: Europe's challenge in the energy market; Guest: Dr. Heiko Lohmann, „energate Gasmarkt“; 34 min., 01.03.26

"Die Presse" podcast on the Russian economy: Russia - gas, sanctions, oligarchs: Is Russia the big profiteer of the Iran war and China the loser? Recording on 10.03.26; The Ukraine war has made Russia the economic loser and China the profiteer. The Iran war, however, has a completely different impact. Vladimir Putin is already laughing up his sleeve. And China? Sinology professor Dr. Susanne Weigelin-Schwiedrzik and Russia economist Vasily Astrov (WIIW) in conversation with Eduard Steiner; 11.03.26

Monetary policy, key interest rate decision on 20.03.26

Olga Belenkaya, FG Finam: The Russian central bank continues to ease its monetary policy, 20.03.26

Kommersant, Erdni Kagaltynov: Nabiullina on inflation, the impact of the Iran war on the economy and labor shortages, 20.03.26

International Investment: The Russian Central Bank has lowered the key interest rate for the seventh time in a row to 15%. 20.03.26

Finmarket.ru: The situation in the Middle East could also affect the Russian market, says Nabiullina, 20.03.26

Finmarket.ru: The forecast for Russian GDP growth in 2026 of 0.5-1.5% is still maintained, 20.03.26

Central Bank of Russia: The Central Bank of Russia has decided to cut the key interest rate by 50 basis points to 15.00% per annum, 20.03.26

Central Bank of Russia: Statement by the Governor of the Central Bank of Russia, Elvira Nabiullina, following the meeting of the Board of Directors on March 20, 2026, 20.03.26

Finmarket.ru: Inflation in Russia amounted to 0.73% in February, the annual rate was 5.9%, 13.03.26

Overall economic development:

European Leadership Network; Sinikka Parviainen; Senior Economist, Bank of Finland Institute for Emerging Economies: Understanding Russia's wartime economy and why it matters for Euro-Atlantic security, 20.03.26

International Investments: Russia's economy in the years 2025-2026: Slowing growth and industrial decline; EDB forecasts and government positions; 19.03.26

Deutsche Welle.com/ru; Oleg Loginov: SIPRI: Russia has passed the peak of military spending growth, 19.03.26

IEF RAS: Quarterly GDP forecast. Issue No. 69, 16.03.26; soon also with English abridged version; Nezavisimaya Gazeta; Mikhail Sergeev: Russians do not believe in a peace agreement for Ukraine. According to the survey participants, the most difficult times still lie ahead for the economy, 17.03.26

Kommersant; Artem Chugunov: The economy is not meeting forecasts. Analysts' short-term assessments differ from the expectations of the Russian Central Bank, 17.03.26

RBC.ru: The Eurasian Development Bank reported a slowdown in the Russian economy, 17.03.26

Eurasian Development Bank, EDB: Macroeconomic overview, 17.03.26

Peace Research Institute Oslo, PRIO; Pavel K. Baev: Moscow calculates benefits of Gulf conflict, coming short, 17.03.26

Marxist.com; Alexandra Sablina: How the global crisis strengthens Russia,16.03.26

infosperber.ch: Money almost exclusively for war, debt interest and pensions. The war does not allow Russia to invest in the future of the economy. The future looks bleak.16.03.26

Nezavisimaya Gazeta; Anastasia Bashkatova: 100 roubles per dollar is no panacea for the Russian budget. A devaluation of the national currency without comprehensive import substitution harbors the danger of economic collapse, 15.03.26

Russian Central Bank: What the trends say, 2/26 , Excecutive Summary in English; 12.03.26

Interfax.ru: The Central Bank of Russia pointed to an expected slowdown in economic activity at the beginning of the year. The reasons include tax changes, which required adjustments from businesses and the population, holidays and the weather. 12.03.26

RE:RUSSIA: The vicious circle of military post-Keynesianism: why rapid income growth failed to boost domestic production; 11.03.26

Deutsche Welle com/ru; Oleg Loginov: Instead of acceleration: What is happening to the Russian economy? 27.02.26

Carnegie Politika; Alexandra Prokopenko, Carnegie Berlin Center for Russian and Eurasian Studies: Altitude sickness: what threat does the continuation of the war pose to the Russian economy? 10.03.26; The original English text was published on 16.02.2026 in „The Economist“.

Iran war, energy supply and Russia

Focus.de; Analysis by Ulrich Reitz: Putin deal? Hidden by the Iran war, an explosive idea is circulating, 22.03.26

FR.de; Marcus Giebel: Hundreds of billions of dollars: How Putin could profit from the Middle East war - three scenarios. Study by the "Kyiv School of Economics" (KSE); 21.03.26

Kyiv School of Economics: Iran war helps Russia; long conflict would fundamentally undermine economic pressure campaign; sanctions easing does not resolve energy market challenges - KSE Institute, Study: Assessment of the Impact of the Iran War on Russia, 20.03.26

BBC; Dharshini David, Deputy economics editor: Russia, China and the US - the global winners and losers of the Iran war, 19.03.26

Focus de; Lars-Eric Nievelstein: Putin reaches for Ukraine treasure: He faces these hurdles, 16.03.26

BBC Newscast with Steve Rosenberg in Moscow: Will Putin benefit from the Iran war?Steve Rosenberg about the US decision to loosen sanctions on Russian oil, 15.03.26

Janis Kluge, German Institute for International and Security Affairs, in an interview with Tagesschau.de by Carl-Georg Salzwedel: Relaxation of oil sanctions. „Russia is a big profiteer“, text with video, 13.03.26

Tagesschau.de analysis by Björn Blaschke: Iran war. Profiteer Putin? 13.03.26

Oil prices and the national budget

Deutsche Welle.com/ru; Oleg Loginov: SIPRI: Russia has passed the peak of military spending growth, 19.03.26

The Moscow Times; Sergei Shelin: Why High Oil Prices Won’t Fix Russia’s Budget Crisis, 19.03.26

Nezavisimaya Gazeta; Anastasia Bashkatova: 100 roubles per dollar is not a panacea for the Russian budget. A devaluation of the national currency without comprehensive import substitution harbors the danger of economic collapse, 15.03.26

The Moscow Times; Sergey Shelin: Oil prices skyrocketed, but they decided to tighten the oil screws immediately, March 13, 2026

Yahoo Finance; Artur Kryzhnyi, Financial Times: Russia to gain billions in additional revenue from oil price surge due to war with Iran, 12.03.26

Monthly and weekly economic reports:

VEB Institute: World Economy and Markets, weekly report

Politcom.ru; Marina Voitenko: Weekly report: Extremely high volatility of oil prices and extreme uncertainty of consequences, 19.03.; Weak macrodynamics require regulatory support, 12.03.26

CREA, Vaibhav Raghunandan: February 2026 - Monthly analysis of Russian fossil fuel exports and sanctions, 12.03.26

CMASF monthly report: Trends in the Russian economy, January 2026, 12.03.26

The post Key interest rate cut to 15%, growth of 1% to remain appeared first on ostwirtschaft.de.

Original article (German):

Read on ostwirtschaft.de →