Monetary policy under pressure: Ankara halts interest rate cuts for the time being

The Turkish central bank has not lowered its key interest rate any further for the time being in the face of growing geopolitical uncertainty. The Monetary Policy Committee decided on March 12 to leave the one-week repo rate at 37 percent.

Just a few days earlier, many market participants had expected a rate cut. However, the escalation in the Middle East abruptly changed investors' assessments. Rising energy prices and a decline in risk appetite on the international financial markets increased the pressure on Turkish monetary policy.

In its statement, the central bank pointed out that the geopolitical developments had created new uncertainties for inflation and economic growth.

Tighter monetary policy through the back door

Parallel to the decision, the central bank implemented several technical measures to effectively increase financing costs in the banking system.

At the beginning of March, regular repo auctions were suspended - an instrument that the central bank occasionally uses in order to increase banks' access to short-term credit facilities. As a result, the average refinancing rate for banks temporarily rose to around 40 percent.

The central bank's interest rate corridor also remained unchanged. The overnight interest rate remains at 40 percent, while the deposit rate remains at 35.5 percent. In extreme cases, the central bank could also refer banks to the so-called late liquidity window, where the interest rate is even higher.

Billions to stabilize the lira

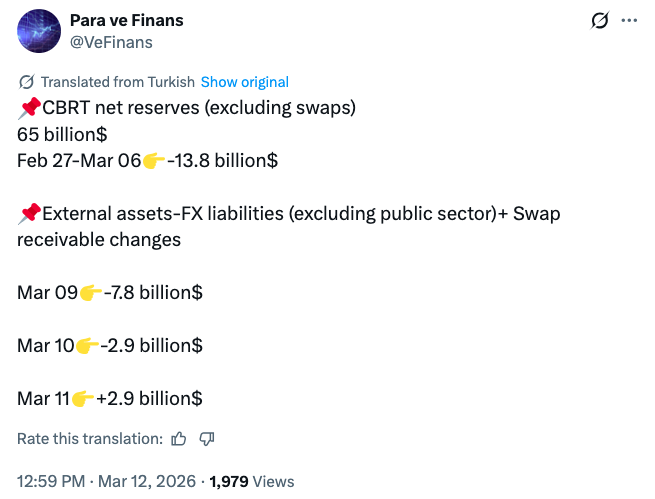

In order to curb turbulence on the foreign exchange market, the central bank also intervened massively in the market. According to estimates, it sold around 22 billion dollars from its reserves between 2 and 10 March.

Tweets: Interventions are reflected in the central bank's account balance with a one-day lag. Data indicate strong foreign exchange demand on the first trading day (Monday, March 2) and the last trading day of the first week of intervention (Friday, March 6).

The interventions followed significant capital outflows: In the days following the start of the geopolitical escalation alone, investors withdrew more than eight billion dollars from Turkish financial assets.

Despite this, the national currency remained relatively stable. The dollar appreciated only moderately against the lira and recently hovered around the 44 lira mark.

Risk premiums for Turkish government bonds also remained comparatively calm. Credit default swaps stabilized at around 250 basis points.

Inflation remains high

Parallel to this, inflation remains at a high level. According to the statistics office, consumer prices rose by more than 31 percent in February compared to the previous year.

Rising energy prices are having a particularly strong impact. The rise in fuel prices has recently accelerated significantly.

In order to limit the burden on consumers, the government reactivated a tax mechanism for fuel. A large part of the price increases will initially be cushioned by a reduction in excise duty.

However, this leeway is limited: If the price of oil continues to rise, price increases could soon be passed on in full to consumers.

Interest rate policy remains uncertain

The future course of monetary policy depends heavily on the development of energy prices and the geopolitical situation.

The next interest rate meeting of the central bank is scheduled for April 22. If the situation stabilizes, the central bank could resume its path of interest rate cuts. If uncertainty remains high, a renewed tightening of monetary policy cannot be ruled out.

Many economists already expect inflation to be significantly higher than previously forecast this year.

Content navigation

Central bank likely to leave key interest rate unchangedOriginal article (German):

Read on ostwirtschaft.de →