Russia

Russia's seeds: self-sufficiency with weak points

Russia wants to become largely independent when it comes to seeds. In future, anyone growing maize, sunflowers or sugar beet in Russia is to work primarily with seeds from domestic breeding. The import quota for seed from "unfriendly" states - i.e. from countries that have imposed sanctions against Russia - will fall to 15,000 tons in 2026. In 2023, seed imports from these countries still amounted to 73,300 tons, according to the Russian plant protection service Rosselkhoznadzor. According to the state food safety doctrine, the proportion of domestic seeds should increase to 75% by 2030

German farmer Steffen Hauschild, who runs the Nekrasovo Pole Agropark in the Kaliningrad region, describes the consequences of this policy in the podcast of the German-Russian Chamber of Commerce Abroad: "What is hitting farmers in Russia hard are the countermeasures taken by the Russian Federation. In other words, the Russian Federation has now taken countermeasures, for example with regard to Western seeds. This is actually hitting us much harder than the EU sanctions."

Market size: sown area and monetary value

The Russian Ministry of Agriculture states a sowing area of 80.5 million hectares for 2025. More than 83.1 million hectares are planned for 2026. According to government figures, around 10 million tons of seeds will be sown each year. The industry center of the state agricultural bank Rosselkhozbank estimated the Russian seed market at the beginning of 2025 at around 150 billion roubles - about 1.7 billion euros at the current exchange rate. One of the largest Russian agricultural holding companies, AgroTerra, estimates the commercial seed market at 222 billion roubles, the equivalent of 2.5 billion euros.

Germany is on a different scale. The Federal Statistical Office Destatis reported a cereal area of 5.86 million hectares for 2025, plus 1.1 million hectares of winter rapeseed, 1.94 million hectares of silage maize and 131,700 hectares of vegetable cultivation. For the 2024/25 marketing year, the Federal Plant Variety Office reports approved seed quantities of 744,400 tons, of which 639,100 tons are cereals and maize, 74,400 tons are fodder plants and 25,600 tons are oil and fibre plants.Russia's seed market is physically around ten times larger than Germany's, but roughly the same size in monetary terms. Russia distributes seed over significantly larger areas, while Germany relies on smaller quantities with a higher unit value.

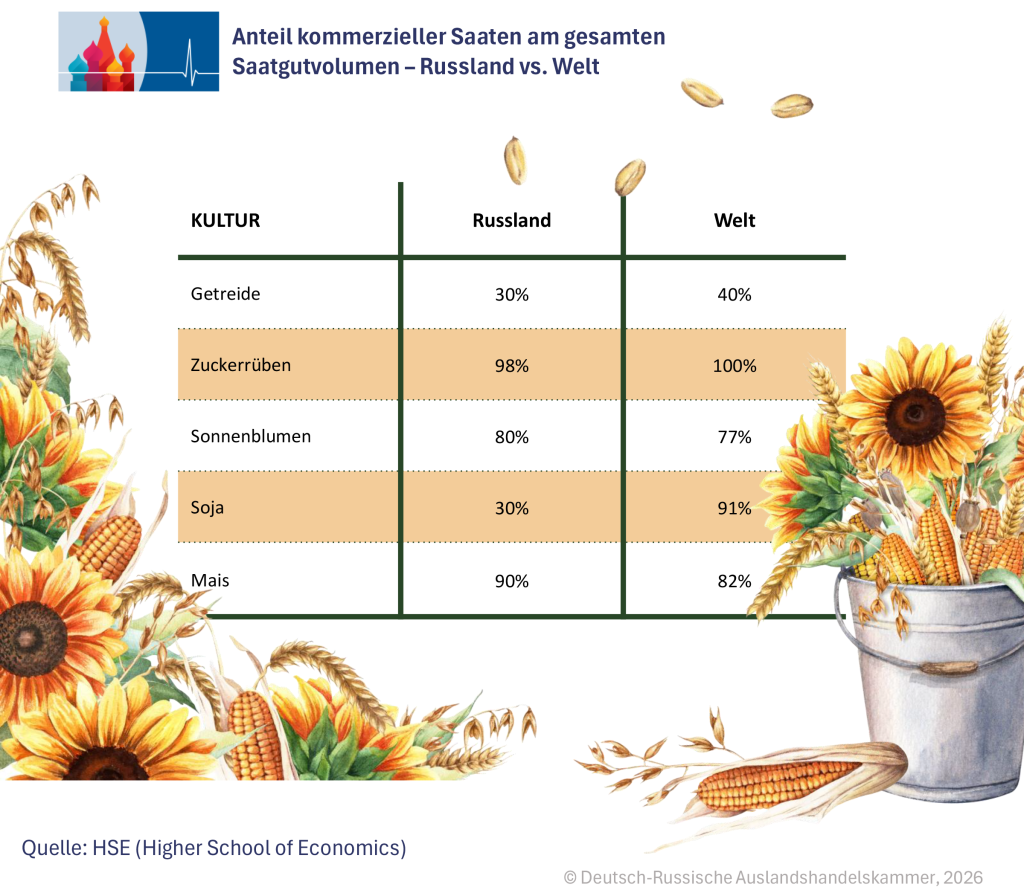

Self-sufficiency is increasing, but unevenly distributed

According to official figures, Russia's import substitution for seeds is measurably advanced, but varies greatly depending on the crop. According to government figures, the proportion of domestic seeds will already reach 69% by 2025. By 2030, it should be 75%. Russia is close to self-sufficiency in cereals and pulses. According to Rosselchosbank, the proportion of domestic seed for these crops is around 80%. The figure is 93% for winter wheat, 87% for spring wheat, 89% for spring barley and 86% for winter barley, but the situation is different for hybrid crops. In 2022, the Ministry of Agriculture reported a domestic quota of 43.5% for soybeans, 30.6% for rapeseed, 23% for sunflowers, 6.7% for potatoes and 1.8% for sugar beet. By 2025, according to the ministry, it had risen to 65% for soybeans, 61% for rapeseed and more than 50% for sunflowers. Sugar beet reached around 19%.

A look from the field shows that this substitution does not work smoothly everywhere. Steffen Hauschild describes the situation as follows: "The Russian Federation has its own institutes that breed grain seed and for the core areas in Russia [...] these are very, very good varieties. But for us here, with the much colder climate, with the more intensive climate, these varieties are completely unsuitable. We have 20% lower yields here." Industry experts put the yield gap between domestic and western seeds at 15% to 50%, depending on the crop. Those who rely on inferior goods lose the profitability of cultivation.

At the same time, a wave of small local garden breeders is emerging. They propagate seeds without investing in their own research and development. The industry says: It often remains unclear where parent lines and germplasm come from. Russian farmers buy the goods without reliable quality control.

Sunflower is considered the most visible substitution segment, while sugar beet is the sharpest bottleneck. In the Krasnodar Territory, one of the most important growing regions, the share of domestic sugar beet seed in the 2026 sowing season only reached 24%.2025, the state variety testing commission Gossortkomissija added more than 1000 varieties and hybrids to the state register. More than 73% of applications for state variety testing came from domestic breeding. AgroTerra expects the seed market to grow by 8.3% per year until 2030.

Import policy: quotas, audits, bans on origin

Import policy is the central lever of the Russian seed strategy. For 2025, the government has set a total quota of 34,000 tons of seed from "unfriendly" countries. For 2026, this quota will fall to 15,000 tons. Permitted are: 10,000 tons of seed potatoes, 1900 tons of sugar beet seed, 2000 tons of seed maize, 500 tons of high-oleic hybrid sunflower seed and smaller quantities of waxy maize and malting barley seed.Imports of the top-selling crops, maize and sunflowers, have effectively been halted since 2025. The ban applies equally to hybrids, parent seeds and germplasm components. Only two niche segments are exempt: Waxy maize and high oleic sunflower.In addition, there are targeted bans on origin. Rosselkhoznadzor banned the import of certain maize and sunflower seeds from Chile, Turkey, Hungary and France at the end of 2024. Since June 30, 2025, there has been a ban on the import of seed and planting material from the Netherlands, a traditionally important supplier country, and the most effective import control instrument is the audit of foreign laboratories by Rosselchosnadzor. So far, not every EU country has undergone this procedure - an additional brake on imports. The effect can be seen in the figures. Seed imports fell from 73,300 tons in 2023 to around 30,000 tons in 2024 and 18,500 tons in 2025. Imports of sunflower seed fell to 525 tons in 2025, maize to 295 tons and soya to 59 tons. There are no signs of a major deficit in these segments for the 2026 sowing season. Domestic producers have produced high volumes. There are also significant imports from the CIS states, especially Kazakhstan. Market observers estimate the share of gray imports at 20% to 25%. At the same time, the proportion of counterfeit seed is growing significantly. Own exports remain small. The Rosselchosbank stated a volume of 137 million US dollars in 2025 - this corresponds to 32nd place on the world market.

When western seeds cost twice as much

The effects can also be seen in the prices. The market is divided into two blocks. In March 2026, Russian trade media reported a premium of around 70% for imported sunflower seed compared to domestic goods. The price of imported corn was around twice as high as the Russian competitor product. In 2024, the premium for Western sunflower seed was still between 20% and 30%. The difference has therefore widened. Domestic producers have also added significantly. Industry sources say: 15% to 30% above the previous year's level, and distribution is centralizing. According to Ruseed, it will sow more than 1 million hectares with its own hybrids in 2025 - over 10% of Russia's sunflower area. Ekoniva-Semena sells in 74 regions and exports to 10 countries. Schelkovo Agrohim integrates plant protection, seeds and consulting. AgroTerra says it plans to test more than 500 corn and sunflower hybrids on around 20,000 hectares of its own land, with a target production of 70,000 tons.

Strict controls, but hardly any license money

The Russian regulatory framework has been significantly tightened and digitalized since 2022. At its core is Federal Law No. 454 on the Seed Industry, extended by Law No. 499 at the end of 2024. The state platform FGIS "Semenovodstvo" (seed breeding) now requires traceability of origin and batches. A new version of the GOST 12036-2025 standard has been in force since January 1, 2026; it stipulates an additional average sample for the detection of genetically modified organisms when taking samples. In the case of seed potatoes, the state now links the granting of subsidies to compliance with the test requirements. The system remains de facto GMO-free, i.e. free of genetically modified organisms, while Russia lags behind in the collection of license fees. AgroTerra puts the current volume of royalties in Russia at 250 to 300 million roubles - around 2.5 to 3.2 million euros a year. The rates are therefore five to seven times below the international level. AgroTerra estimates the potential at 14.7 billion roubles for wheat alone, 3.8 billion for soya and 3.6 billion for barley - together around 22 billion roubles or around 230 million euros per year.The Russian seed market is one of the most heavily regulated segments of the economy. The import quotas of the last three years have fundamentally changed its structure. Russian farmers are losing access to high-quality seeds that could ensure higher yields. Industry experts see this as a burden on the overall economic situation.

Germany: Less area, more yield

Germany controls its seed market institutionally, not geopolitically. The Seed Marketing Act defines seed as an object of consumer protection. A variety may only be marketed if it is included in the German list of varieties or in the common EU catalog, according to the Federal Plant Variety Office. The recognition system links breeders, propagation organizations and marketing companies. The key political indicator is not the proportion of domestic selection, but the so-called seed replacement - i.e. how often farmers actually use new seed instead of replanting their own. According to the German seed industry, 61% of German farmers used Z seed (certified seed) for cereals in the 2023/24 marketing year.

The productivity gap to Russia is large. Destatis reported a German grain harvest of 45 million tons and a yield per hectare of 75.5 decitons for 2025. Russia achieved 27.2 decitons per hectare in the 130-million-tonne 2024 season - just over a third of the German level. Germany produced 4 million tons of winter rapeseed and 4.5 million tons of vegetables. The comparison is not complete due to climate, crop rotation and soil system, but the direction is clear: Russia mobilizes area, Germany yield.

Both countries are effectively GMO-free. In the EU, only the MON810 maize line is currently approved for cultivation; in Germany, according to the Federal Office of Consumer Protection and Food Safety, there is no approval for commercial cultivation. Russia is taking control through bans and sampling, Germany through a lack of national cultivation approvals. This article was written for the German-Russian Chamber of Commerce Abroad.

The post Russia's seeds: self-sufficiency with weak points appeared first on ostwirtschaft.de.

Original article (German):

Read on ostwirtschaft.de →