Russia

New forecasts from Germany and Finland for Russia's economy

Author: Klaus Dormann

How will the "energy price shock" triggered by the Iran war affect global economic growth? In which countries is production growth likely to be particularly affected by high energy prices? Which countries could benefit from this? The answers to these questions are particularly relevant for Russia as a major energy exporting country.

"Joint diagnosis" by the German economic research institutes: less growth in Germany; more growth in Russia

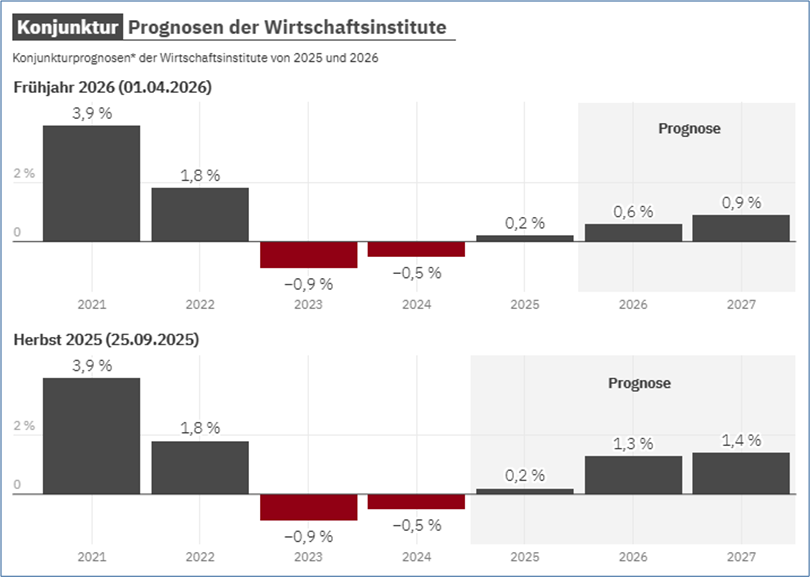

In their semi-annual "Joint Economic Forecast" updated on April 1, the five leading German economic research institutes have cut their forecast for this year's growth in the German economy in half from 1.3 percent to just 0.6 percent in light of the sharp rise in energy prices. "The energy price shock" will dampen the recovery of the German economy, but is unlikely to bring it to a complete standstill, the institutes write. The "considerably expansive course" of German financial policy will ensure this.

Forecasts of the "Joint Economic Forecast": Growth of the German economy

* Change in gross domestic product (GDP) compared to the previous year in percent, price-adjusted.Graphic: n-tv.de / lstSource: Joint Economic Forecast of the economic institutes, Destatisn-tv.de: Institutes: Iran war slows down German economic growth, 01.04.2026

In Russia, however, the German institutes now expect slightly stronger economic growth this year and next than in their last joint forecast at the end of September. They raised their forecast for Russia's economic growth in 2026 from 0.8 to 1.1 percent and their growth forecast for 2027 from 0.8 to 0.9 percent. The institutes did not justify this upward revision of their growth forecasts. However, they probably expect that Russia, as an important energy exporting country, will receive a boost to its economic growth from the rise in energy prices.

On March 26, the Paris-based OECD raised its growth forecasts for Russia to a similarly low level as the "Joint Economic Forecast". The OECD now expects Russia's real gross domestic product to increase by 0.6% in 2026, accelerating to 0.8% in 2027. This means that the German economic research institutes' forecasts for the increase in Russian gross domestic product in 2026 and 2027 remain slightly higher than the OECD's forecasts.

The growth forecasts of the "Joint Economic Forecast" for Russia also remain slightly higher than the forecasts published on March 30 by the Finnish central bank's BOFIT research institute. BOFIT now expects Russia's economic growth to once again only reach around 1 percent in 2026. Next year, it will even halve to only around 0.5 percent.

Russia's growth stabilizes at around 1 percent in 2026

According to the forecasts of the "Joint Economic Forecast", the OECD and the Institute of the Bank of Finland, Russia can expect the current rise in energy prices to stabilize its growth in 2026, which fell to only around 1% in 2025. According to the forecasts, growth in the Russian economy is expected to be similarly weak in 2027.

On April 1, the Moscow-based "Centre for Macroeconomic Analysis And Short-term Forecasting" (CMASF) raised its growth range for 2026 from 0.5 to 0.8 percent to 0.9 to 1.3 percent. It expects growth of up to 1.5 percent in 2027.

GDP forecasts for Russia 2024 to 2027Change in real gross domestic product compared to the previous year in percent

Joint Economic Forecast: Energy prices will fall again from the summer, but will still be noticeably higher at the end of 2027 than before the Iran war

The Joint Economic Forecast describes the "strong energy price shock" after the start of the Iran war as follows:

"The military conflict in the Persian Gulf has largely blocked one of the central transportation corridors of global energy supply, the Strait of Hormuz. As around a fifth of global crude oil and LNG production is concentrated in this region, the restricted transport capacities have led to a significant rise in energy prices and increased volatility on the commodity and financial markets.

The price of Brent crude oil surpassed the USD 100 mark, up from USD 65 in January. At the same time, the price of gas in Europe (Dutch TTF) doubled in the meantime to EUR 60 per MWh."

In the following two figures from the joint forecast with scenarios for the development of the Brent crude oil price and the natural gas price (Dutch TTF), the blue line for the base scenario shows the price development to date up to March 20 and the expected further price development up to the end of 2027 according to the market expectations of March 20.

German Institutes: Joint Economic Forecast, 01.04.26

The development of energy prices assumed in the baseline scenario in the Joint Economic Forecast according to the market expectations of March 20 is compared with a "pre-war scenario" based on the market expectations for price development at the end of February, i.e. before the outbreak of war (lower gray line).

Secondly, the energy price trend in the base scenario is compared with the price trend in an "alternative scenario", in which significantly larger and longer-lasting energy price increases are assumed (upper black line).

The Joint Economic Forecast describes its assumptions on the further development of energy prices up to the end of 2027 as follows:

"In their forecast, the institutes assume that the Strait of Hormuz will become fully passable again in the course of the second quarter and that exports of oil and liquid gas from the region will gradually return to pre-war levels in the second half of the year. In line with futures market prices, it is assumed that energy prices will fall again from the summer onwards, but will still be noticeably higher at the end of the forecast period than before the outbreak of war."

BOFIT: Russia's GDP growth stagnates at around one percent in 2026

At the end of March, BOFIT, the research institute of the Finnish central bank, published the "spring edition" of its semi-annual forecasts for the Russian economy. The institute does not expect the current sharp rise in energy prices to boost growth in the Russian economy. It is sticking to its October forecast that Russia's economic growth will again only reach around 1 percent in 2026. BOFIT has even halved its growth forecast for 2027 from 1.0% to just 0.5%. The Russian economy is expected to grow just as weakly in 2028.

According to BOFIT, the high commodity prices will only "support" Russia's economic growth in 2026, not accelerate it. However, the stabilizing effect of high commodity prices will diminish in 2027/2028.

A look back: How BOFIT assesses Russia's economic development in 2025

Last year, economic growth was primarily impacted by declines in production in the raw materials sector and production in wholesale trade.

In the manufacturing sector, the "polarization" of production intensified: value added in the "war-important sectors" of the manufacturing industry rose by 20%, while its total value added increased by just 0.4%.

Key economic indicators, changes compared to the previous year in %

Source: BOFIT Russia statistics

Private demand was the most important growth driver. In 2025, real wages and real disposable income continued to rise despite the weakening economy. At the same time, unemployment remained at a historic low. However, the annual increase in real retail sales also recorded a significant decline in 2025 compared to the previous year.

Growth in fixed asset investments was subdued compared to previous years, mainly due to weak demand and restrictive monetary policy.

Net exports had a negative impact on GDP growth in 2025. Exports were impacted by new sanctions against the oil sector.

The labor shortage remains a significant problem for Russia, although economic growth slowed in 2025. Russia had virtually full employment at the end of 2025. Growing immigration did little to increase the supply of skilled labor. The labor shortage is mainly due to the exacerbation of long-term demographic trends over the last three decades caused by the war in Ukraine.

BOFIT forecasts for 2026 to 2028

BOFIT assumes that the sanctions pressure on the Russian economy will remain at the level of early 2026 and that the Russian economy will experience "no further significant external or internal shocks" during the forecast period.

BOFIT does not base its forecast on explicit assumptions regarding the further development of oil prices. The institute points out that oil prices rose sharply worldwide with the outbreak of the Iran war at the end of February. It is unclear how long this situation will last.

Based on these assumptions, BOFIT expects the economy to develop as follows:

Economic growth is likely to level off at around 1% this year. High commodity prices will support economic growth this year, but this effect will fade in 2027/28.

Annual change in real gross domestic product (in %)

Rosstat figures 2021-2025 (as at: 16.02.2026); BOFIT forecasts 2026-2028 (as at: 30.03.2026)

Declining private demand and the lack of growth in fixed asset investments are the main obstacles to growth. Growth in real wages is slowing. Companies' ability to invest continues to be restricted by low profitability and restrictive monetary policy.

Despite the ongoing restrictive monetary policy, the Russian central bank expects the key interest rate to fall gradually over the entire forecast period. It will average 13.5 % to 14.5 % this year, 8 % to 9 % in 2027 and 7.5 % to 8.5 % in 2028.

The combination of restrictive monetary policy and stricter government restrictions on the granting of subsidized loans this year is likely to reduce the incentives to borrow.

It will no longer be possible to promote economic growth through a strong expansion of public economic stimulus programs, as the government's options for deficit financing are limited. The production potential of the Russian working population has been almost completely exhausted. A further increase in government spending would therefore increase the risk of "economic overheating".

Growth in private household consumption is slowing down

Private consumption will continue to rise, but at a slower rate than in previous years. Household consumption will continue to be supported by real wage increases and savings. However, the rapid growth in wages in the years 2023 to 2025 is over, as companies are struggling with a weaker financial situation. The rise in VAT rates since the beginning of 2026 and fee increases for municipal services will also dampen consumption growth.

Growth in fixed asset investment could come to a standstill

The "priority" investments for the military sector will continue. However, they are unlikely to increase the future growth potential of the Russian economy, as large amounts of these investments will be destroyed in the war effort.

Other capital investments are likely to fall. The financial situation of many companies has deteriorated due to weak demand, high interest rates, increased labor costs and high tax burdens. This makes it more difficult for private companies that are not involved in military-industrial production chains or receive other state subsidies to make significant investments. The sanctions have also increased the prices of capital goods and reduced their availability.

BOFIT highlights an increasing division of the Russian economy into a "military-industrial complex" and a "civilian sector":

"Thus, a two-track economic structure is becoming entrenched: companies that profit from military spending are thriving versus those struggling to achieve market-oriented growth. The situation for private companies that are not involved in the war effort will become increasingly difficult. The gap between companies serving the military-industrial complex and those struggling in the civilian sector is growing."

The growth of government consumption is slowing down,

Defense spending is expected to fall in 2026

The increase in government spending was the main driver of growth in the Russian economy in 2023/24, but real growth in public consumption is now likely to slow. According to the 2026 budget plan, spending in the overall Russian budget (federal budget, regional budgets and social security institutions) is set to increase by 4% in 2026, which means a reduction in spending in real terms.

Defense spending is set to fall in nominal terms in 2026. However, this is unlikely if Russia continues the war this year. The country will be forced to,

to find new sources of income through additional taxes and the sale of state assets.

The planned reduction in the budget deficit to 1.6% of GDP is uncertain

In order to reduce the budget deficit, taxes and fees will be increased this year. According to the budget plan, this could generate additional revenue of up to one trillion roubles (around 11 billion euros or 0.5% of GDP). However, actual tax revenues could fall short of the target due to slower economic growth and weak private consumption.

The public sector will continue to run a deficit in 2026 despite high oil prices. However, it is currently expected to fall to 1.6% of GDP. It is to be financed through increased public debt. The liquid assets of the National Welfare Fund have been reduced by the war from the equivalent of 6.5% of GDP before the invasion of Ukraine in 2022 to just 1.8% of GDP at the end of 2025. The Russian Ministry of Finance has declared that no further assets are to be withdrawn from the fund to cover financing gaps.

Russia's public debt is still relatively low by international standards (less than 20% of GDP). However, the cost of servicing the debt has risen due to increased borrowing and higher interest rates. The current budget assumes that these costs will amount to between 1.5% and 1.7% of GDP over the next three years. The implementation of the budget is uncertain, which is why a further increase in borrowing costs is to be expected.

BOFIT also notes the chances of realizing the budget plan:

"Significant increases in the budget, particularly military spending, have become a common feature of financial planning in recent years. If the war continues, we assume that this will not change in 2026 and that further adjustments will be made to the budget over the course of the year. The consolidated budget deficit for 2025 was originally planned at 0.8% of GDP, but reached almost 4% of GDP."

BOFIT sees Russia as "an increasingly isolated economy"

BOFIT expects net exports to have no impact on Russian economic growth over the entire forecast period. This is the institute's assessment of foreign trade developments:

The combined value of exports and imports in relation to GDP fell to around 33% last year - the lowest level in 15 years. Assuming that the pressure of sanctions remains at the current level throughout the forecast period, Russia's isolation from the global markets is likely to continue.

It is unlikely that Russia's export volume will increase significantly in the coming years. Oil and natural gas, Russia's most important export goods, remain subject to sanctions.

Import volumes are being held back by weaker overall demand, and the sanctions are keeping prices for imported products high.

However, Russia will continue to achieve considerable current account surpluses, even if these are likely to be lower than in the 2022-2024 period.

Reader tips:Forecasts:

German Institutes: Joint Economic Forecast: 01.04.26

CMASF: Basic version of the macroeconomic forecast, 01.04.26

BOFIT: BOFIT Forecast for Russia, 30.03.26

vz-nn.ru: The Ministry of Economic Development will lower its forecast for Russian GDP growth in 2026; 28.03.26

OECD: OECD Economic Outlook, Interim Report March 2026 – Testing Resilience, 26.03.26

en.euronews.com; Doloresz Katanich with AFP: OECD lowers eurozone growth forecast due to rising energy prices, 26.03.26

IEF RAS: Quarterly GDP forecast. Issue No. 69, 16.03.26; Nezavisimaya Gazeta; Mikhail Sergeev: Russians do not believe in a peace agreement for Ukraine. According to the survey participants, the most difficult times are still ahead for the economy, 17.03.26

Monthly and weekly economic reports:

Sergei Blinov: Macro Overview No. 13 (2026), 01.04.26

Politkom.ru; Marina Voitenko: Weekly economic report: Compromise under the pressure of uncertainty, 28.03.; Extremely high volatility of oil prices and extreme uncertainty of consequences,19.03.26

VEB Institute: World Economy and Markets, Weekly Report, 27.03.26

Economic Expert Group: Economic Analysis March 2026, 25.03.26

CMASF Monthly Report: "Analysis of macroeconomic trends", 24.03.26

GDP and industrial production in February 2026:

Finmarket.ru: Russia's GDP fell by 1.8% in January and February, 01.04.26

Finmarket.ru: Industrial production in Russia fell by 0.9 % in February, 25.03.26

Kommersant; Artem Chugunov: Industrialists do not expect the best. Industrial production in February and results of recent business surveys, 26.03.26

Hard figures: Industrial production in February: below trend, 25.03.26

The post New forecasts from Germany and Finland for Russia's economy appeared first on ostwirtschaft.de.

Original article (German):

Read on ostwirtschaft.de →