Russia Economic Briefing

Economic trends in post-Soviet countries

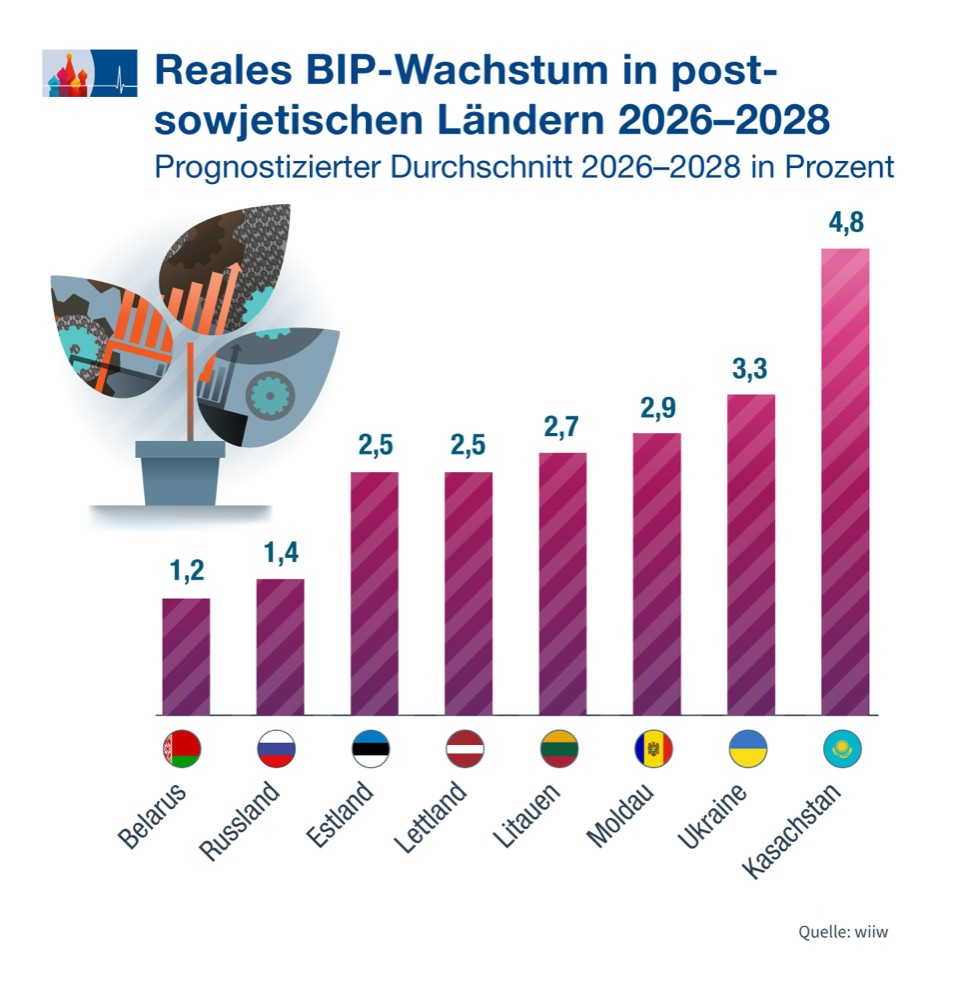

For the countries of Central, Eastern and South Eastern Europe, the Vienna Institute for International Economic Studies (WIIW) expects average annual growth of 2.6% for the years 2026 to 2028. The institute predicts that growth will slow down in many countries in the coming years. This is also due to increasingly strict fiscal policies in many places, with the aim of keeping the currency stable. In addition, companies in many countries will have to invest in automation, digitalization and the introduction of artificial intelligence in production. However, this will not have a short-term impact on growth.

No more peace dividend

In addition, the ongoing military conflict in Ukraine has exhausted the "peace dividend" in Central Eastern Europe. Even an end to the conflict will not automatically lead to an economic boom. Although "credible security guarantees" could create the conditions for investment in the country, it is not certain that this will happen. Conversely, a "fragile peace" could lead to a slow recovery in Ukraine, which would increase the risks and make the country less attractive for investments from Central and Eastern Europe.Irrespective of the Ukraine crisis, the customs conflict between the EU and the USA also poses considerable risks for growth and stability for the entire Eastern European and post-Soviet region. While most countries in Central, Eastern and South-Eastern Europe, especially those within the EU such as Poland, are showing solid growth, the forecasts for some post-Soviet countries outside the EU are mixed.

Belarus in decline

Belarus recorded a significant slump in economic growth in 2025, which fell from 4.3% in the previous year to 1.3%. The main reason for this was falling exports. The export volume of the Republic of Belarus shrank by 10% in 2025. Two thirds of this decline can be explained by falling exports to Russia and one third by declining exports to other countries. However, domestic growth also declined, with transportation and construction being the main drivers of growth. However, production shrank because, unlike in 2023/24, orders from Russia fell by around 2% and the Belarusian government is planning growth of 2.8% for 2026, which is well below the growth rate of 4.1% targeted for 2025. The government in Minsk is continuing to rely on rising exports, which should have a positive impact on average wages and purchasing power, and the Vienna Institute expects the slowdown in growth in Belarus to continue, at around 1.3% in 2026/27 and only 1.1% in 2028. The Vienna researchers assume that Russia's weak growth will inevitably have a negative impact on Belarus' growth rates. The fragile financial situation of many Belarusian companies will limit their ability to invest. The deterioration of the situation on the external markets could prompt Belarus to adopt a more restrictive monetary policy in order to limit inflation, while a possible easing of US sanctions remains a factor of uncertainty, while an easing of European sanctions against Belarus is unlikely. The official inflation forecast is 7% for this year, falling to 5.8% in the years 2027-2028. According to the WIIW, the Belarusian rouble will most likely align its stability with the Russian rouble, whose exchange rate is expected to fall only slightly.

Kazakhstan seeks new paths to growth

After record growth of 6.5% in 2025, growth is expected to slow to 4.5% this year. The expansion of oil production at the Tengiz oil field has peaked, and the expected fall in oil prices will reduce export earnings and budget revenues. The Ukrainian drone attack on the Russian oil terminal in December led to a significant drop in oil production in January, and previous drone attacks on international tankers carrying Kazakh oil have fueled fears of further disruptions and losses. The problems in the oil sector are contributing to the low level of investment expected in Kazakhstan this year. However, according to the institute, investments in the construction, transport and production sectors will grow, partly due to the modernization of infrastructure, and sentiment in the services and production sectors improved in January. Credit-driven growth in private consumption is likely to level off in 2026 due to high interest rates, according to the researchers. Inflation has fallen only slightly in the last three months, reaching 12.5% in December, and the Kazakh government's long-term strategy is to move away from commodity extraction and attract foreign direct investment from the EU, the US, China and Russia, particularly for the manufacturing sector. However, the described disruptions at the oil terminals and the new sanctions against some Russian oil companies that also operate in Kazakhstan point to growing external risks.the national currency, the tenge, will probably soften in 2026, also due to the fall in the oil price, according to the Viennese researchers. This assessment was made before the Iran war was unleashed.

Baltic republics on course for growth

According to the Vienna Institute, the three post-Soviet republics in the Baltic states, Estonia, Latvia and Lithuania, can expect significantly stronger growth than Russia and Ukraine. Two factors play a key role here: integration into the EU market and access to EU funding to modernize infrastructure. Estonia has the most favorable prospects of all the Baltic republics. According to the Vienna researchers, the smallest country in the Baltic region with a population of just under 1.4 million is facing a phase of rising growth after a prolonged recession and stagnation. While Estonian economic growth was estimated at 1.4% in 2025, a rate of 2.3% is expected for this year and almost double that of 2025 to 2.7% in 2027, although growth will remain well below that of the period before February 2022. Negative factors include a lack of confidence in business and ongoing restrictions on competition. Estonia's economic recovery is expected to be driven primarily by an improvement in exports. Production, on the other hand, is developing more slowly, partly due to high wage costs. Inflation could remain a problem in the long term. Geopolitical tensions, particularly with neighboring Russia, could also have a negative impact. There are also risks due to the US tariff policy. Both factors could slow down export growth and lead to investments being postponed.Estonian military spending remains exceptionally high at more than 5% of gross domestic product.Lithuania has similarly favorable growth prospects to Estonia. Growth there is expected to reach 2.5% this year. Both private household consumption and investment are on the upswing. Real incomes are rising. Investment growth is mainly driven by public investment. However, strong export growth has slowed towards the end of 2025. However, the new coalition government led by the Social Democrats faces the problem of how to finance the significantly increased defense costs of more than 5% of gross domestic product.

According to the Vienna researchers, Latvia can hope for rapid growth. After a phase of recession and stagnation in the years 2023-2034, the institute expects stable growth rates of 2.5% in the coming years. In 2026, growth will be driven primarily by private household consumption and investments. According to WIIW estimates, real incomes in Latvia will rise this year. After a strong upswing, mainly due to the European Union's NextGeneration program, the institute estimates that investments will fall this year and next. According to the institute, an increase in the volume of loans to businesses and households will promote private investment and residential construction. At the same time, however, Latvian export growth will remain weak.

The ruling coalition of center-right and center-left parties will have to cope with the growing economic costs of decoupling from Russia, especially in the energy sector. In addition, the budget will be burdened by additional defense spending.

Moldova - a country of weather-sensitive growth

The former Soviet republic of Moldova, once considered the fruit and vegetable garden of the Soviet Union, is experiencing increasing growth. Gross domestic product grew by 5.2% in the third quarter of 2025, which equates to an average of around 2% for the first three quarters. Agriculture grew by 15% in the third quarter, while the construction industry grew by 8.3%. Good weather ensured an excellent harvest, which boosted food production and exports. Foreign capital flows, both aid and loans, boosted investment and the country has become independent of Russian gas imports. Growth is expected to accelerate in 2026 and investments will increase, financed by cheap loans and aid, including 1.9 billion from the EU's Reform and Growth Fund. However, the development of agriculture as the central core component of the economy depends to a large extent on the weather. The Viennese researchers consider the stability of the national currency, the leu, to be relatively stable. Strong currency inflows, particularly from the Moldovan diaspora, contribute to this, which has an anti-inflationary effect.WIIW believes that Moldova's political leadership's goal of EU membership in 2030 is "overambitious". The WIIW believes that Moldova's association negotiations with the EU will be "difficult", particularly in the areas of agriculture and legal reform.

This article first appeared in the exclusive newsletter of the German-Russian Chamber of Commerce Abroad

The post Economic trends in post-Soviet countries appeared first on ostwirtschaft.de.

This article first appeared in the exclusive newsletter of the German-Russian Chamber of Commerce.